A single contract worth $300 billion anchors Oracle’s record $638 billion backlog. That contract is with OpenAI, a company whose ability to sustain $60 billion per year in cloud charges depends on something historically difficult to hold onto: a performance advantage over free alternatives. The deal, signed in September 2025 and ramping from 2027, is one of the largest cloud contracts ever recorded, and it has reshaped how investors read Oracle’s forward revenue story. But beneath the headline figures sits a structural question about AI business models that neither party has fully answered: can frontier AI pricing hold for five years in a market where open-source models have repeatedly closed the capability gap within 6 to 12 months of each new frontier release? What follows maps the underlying logic of where durable economic value actually accumulates across the AI stack, and what the Oracle-OpenAI deal reveals about which positions in that stack are structurally strong and which are structurally exposed.

A $300 billion bet on the durability of frontier AI pricing

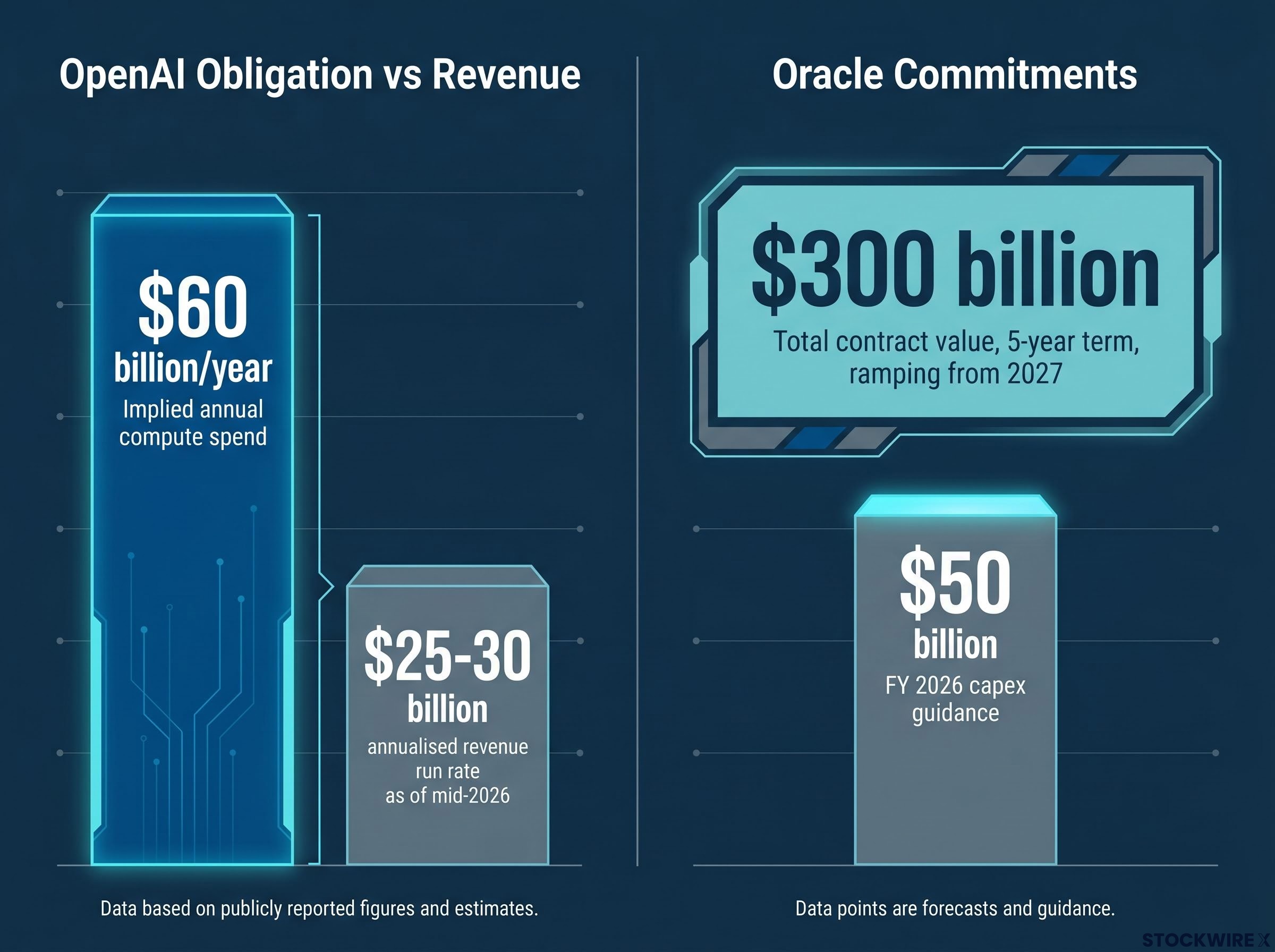

The deal’s terms are worth pausing on. Over five years, Oracle has committed to supplying roughly 4.5 GW of data-centre capacity per year to OpenAI, equivalent to the power consumption of approximately four million homes. At $300 billion over that period, the implied obligation is around $60 billion per year in cloud charges. For Oracle to build the infrastructure to fulfil this, FY 2026 capital expenditure guidance has been pushed to approximately $50 billion, meaning the company is deploying hard capital well ahead of the revenue it expects in return.

$60 billion per year in compute charges against a current revenue base of $25-30 billion: the deal requires OpenAI to more than double its annual revenue simply to cover the compute obligation, before any margin is earned.

Moody’s has already flagged counterparty risk and leverage concerns around the arrangement. The table below outlines the core arithmetic.

| Item | Figure | Context | Risk Implication |

|---|---|---|---|

| Total contract value | $300 billion | Five-year term, ramping from 2027 | Scale creates deep counterparty dependency |

| Implied annual compute spend | $60 billion/year | Largest single-customer commitment in Oracle’s backlog | Requires sustained OpenAI revenue scaling |

| Oracle FY 2026 capex guidance | $50 billion | Capital deployed ahead of contracted revenue | Sunk cost exposure if utilisation disappoints |

| OpenAI annualised revenue run rate | $25-30 billion | Current run rate as of mid-2026 | Revenue must more than double to cover compute obligation |

The gap between what OpenAI currently earns and what the contract implies it must earn is not a marginal concern. It is the foundational arithmetic of the risk.

OpenAI’s compute commitments, described in pre-IPO disclosures as tens of billions of dollars that analysts believe exceed near-term revenue, sit at the centre of the structural discount argument; the company reported approximately $1.8 billion in operating losses for 2024 and expects to remain loss-making through at least 2026, which makes the $60 billion annual obligation to Oracle the single largest lever in its unit economics.

When big ASX news breaks, our subscribers know first

How open-source models erode frontier AI pricing over time

The structural pattern is already observable, and it has repeated across multiple model generations. Open-source models from the LLaMA family, Mistral, and others have consistently closed most of the benchmark gap to prior-generation frontier models within approximately 6 to 12 months of release. The capability that commanded premium pricing from OpenAI or Anthropic last year is, with regularity, available at near-zero marginal cost this year.

The dynamic resembles a pharmaceutical patent that expires within a year of being granted. A frontier lab releases a model that outperforms all alternatives. Within months, open-source developers replicate most of the performance gains through distillation, fine-tuning, and architectural adaptation. The pricing window for charging a meaningful premium above open-source alternatives compresses accordingly.

AI commoditisation has already produced measurable structural damage in adjacent layers of the stack, with autonomous AI agents dismantling traditional per-seat SaaS models and accelerating a reallocation of institutional capital away from established software providers toward AI-native alternatives, a dynamic that foreshadows what frontier model pricing could face as open-source capability closes the benchmark gap.

Epoch AI’s open models research quantifies this convergence pattern, finding that open LLMs have lagged closed frontier models by 5 to 22 months in benchmark performance, a range that confirms both the reality of the gap and the speed at which it closes.

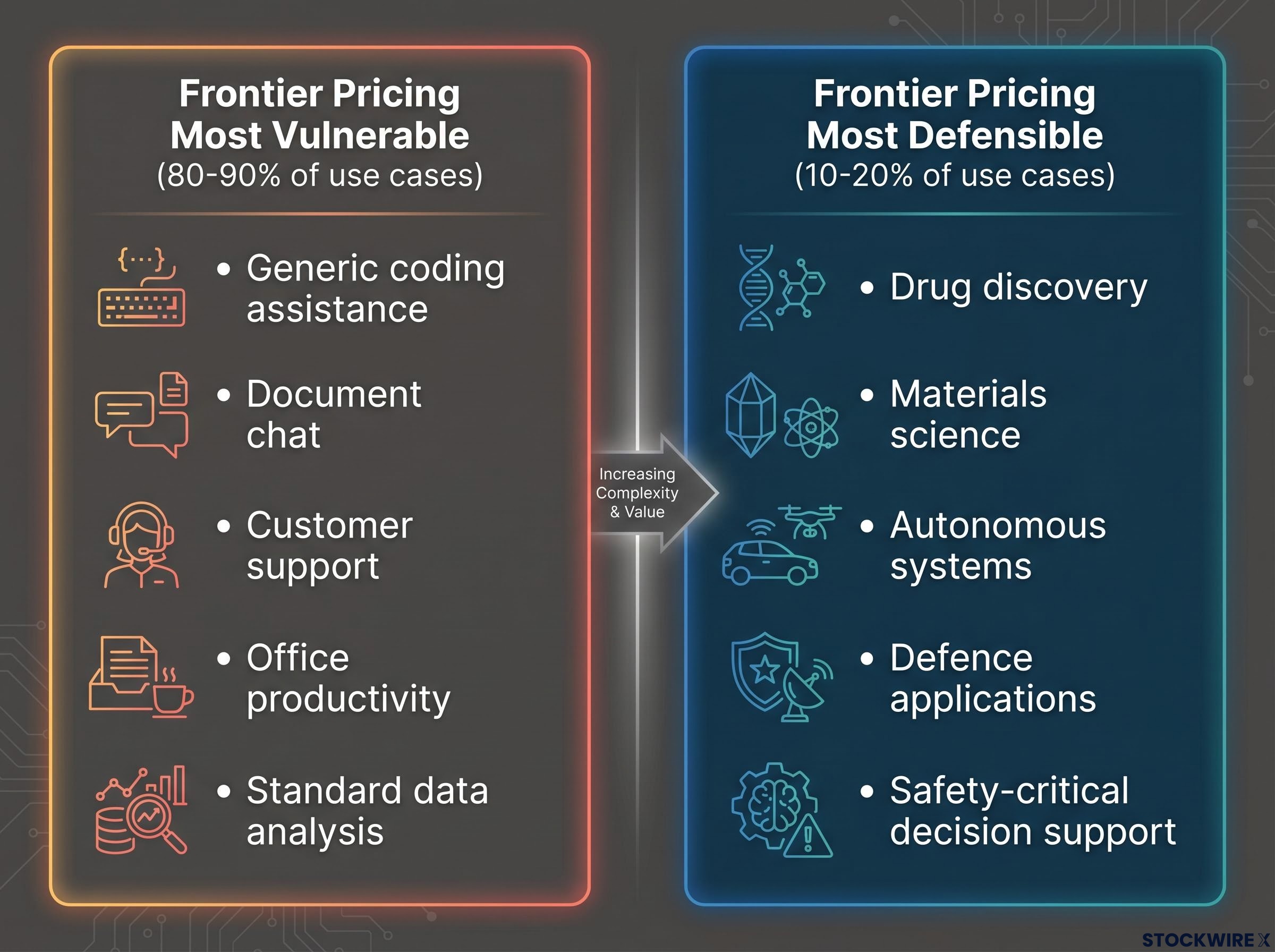

The distinction that matters is not between the absolute capability frontier and everything else. It is between the absolute frontier and the “good enough for most enterprise workloads” threshold. Open-source models cross that threshold reliably, and the workloads most susceptible to substitution are the ones that represent the bulk of enterprise AI spending:

- Coding assistance and developer tools

- Document chat and internal knowledge retrieval

- Customer support and ticket resolution

- Office productivity and workflow automation

- Generic data analysis and reporting

What this means for enterprise procurement decisions

Once an enterprise conducts an honest internal pilot and discovers that an open-source model handles 80-90% of its use cases at a fraction of the cost, the conversation at contract renewal changes materially. The frontier vendor’s pricing power depends not on absolute model superiority but on whether the performance gap in the remaining 10-20% of use cases justifies the total cost differential. For most organisations, it does not.

Where durable economic value actually sits in the AI stack

Concern about a specific contract is one thing. A sharper question is where, structurally, moats in the AI value chain are deep versus shallow. The answer depends on the layer.

| AI Stack Layer | Moat Strength | Primary Source of Defensibility | Key Vulnerability |

|---|---|---|---|

| Model | Weak | Temporary performance lead | Open-source convergence within 6-12 months |

| Data | Strong (where proprietary) | Clinical records, transaction histories, sensor data, internal logs | Requires genuine proprietary datasets; public data moats erode quickly |

| Workflow / Distribution | Very strong | Deep integration into ERP, CRM, developer tools, IDEs | Execution risk; integration must be deep enough to create switching costs |

| Infrastructure | Conditionally durable | Physical scale and long-lived capital assets | Durability depends entirely on utilisation; idle capacity generates no return |

The model layer is the weakest. Performance advantages are measured in months, not years, and the innovation cycle is accelerating. The data layer is strong only where firms possess truly proprietary datasets that cannot be replicated from public sources. The distribution and workflow layer, where AI is embedded into daily operating systems, generates the highest switching costs and the most durable competitive position.

Proprietary data is increasingly the scarce input in AI, not model architecture. Firms that control unique datasets (clinical records, transaction histories, internal operational logs) hold a structural advantage that model commoditisation cannot erode.

Oracle occupies the infrastructure layer. That position is historically reasonable, but infrastructure returns are always conditional on the utilisation economics of the layer above. If that layer is exposed to rapid commoditisation, infrastructure durability becomes contingent rather than guaranteed.

The narrowing case for frontier pricing power

The analysis so far could read as unidirectional: frontier pricing is doomed, full stop. The reality is more specific than that.

There are domains where frontier model performance differences translate into outsized value, and where “good enough” is commercially unacceptable. Drug discovery, materials science, autonomous systems, and certain defence and safety-critical applications represent the clearest examples. In these fields, small performance margins can mean the difference between identifying a viable drug candidate and missing it, or between a safe autonomous navigation decision and a catastrophic one.

Frontier pricing is likely to remain defensible in these domains because the cost of using a slightly inferior model is disproportionately high relative to the savings.

- Frontier pricing most vulnerable: Generic coding assistance, document chat, customer support, office productivity, standard data analysis

- Frontier pricing most defensible: Drug discovery, materials science, autonomous systems, defence applications, safety-critical decision support

The market size constraint

The problem is not that defensible frontier niches do not exist. It is that they may not be large enough. Even if frontier pricing holds durably in pharmaceutical discovery and materials science, the total addressable market for high-margin frontier APIs concentrated in those domains is materially smaller than the capital expenditure volumes currently being deployed implicitly assume.

Oracle’s FY 2026 capex guidance of approximately $50 billion is being built on the assumption that frontier AI compute demand will persist at scale. Once OpenAI’s own investors apply pressure for profitability rather than pure growth, $60 billion per year in compute costs becomes very difficult to sustain unless revenue scales proportionally. The defensible niches are real, but whether they are large enough to support the capital already committed is a genuinely open question.

How Oracle is managing the exposure it has accepted

Oracle is not unaware of the risks embedded in this position. Three structural features of its current contract portfolio shift the severity of the exposure:

- Prepaid and bring-your-own-hardware structures: The bulk of new AI backlog additions in the most recent fiscal quarter are structured as prepaid arrangements or bring-your-own-hardware deals. These limit Oracle’s direct balance-sheet exposure if a customer under-uses committed capacity. They do not, however, protect against the reputational and utilisation damage of large-scale underuse.

- Customer diversification: Oracle has been actively courting additional AI customers and hyperscalers. Cloud backlog growth is not solely attributable to OpenAI, and management has acknowledged the concentration concern publicly. Additional AI companies are reportedly showing interest in Oracle’s infrastructure offerings.

- Contracted margin stability: Oracle has stated that margins on new AI deals are stable or improving, suggesting the company is not buying backlog through unsustainable pricing.

These structures shift Oracle’s exposure from existential to uncomfortable, not from present to absent.

The distinction matters for investors evaluating Oracle’s risk profile. Existential risk, meaning stranded and unfinanced idle data centres, is reduced. Uncomfortable risk, meaning underutilisation relative to projections and a slower-than-expected revenue ramp, remains firmly in play. Moody’s counterparty risk and leverage flagging reflects the credit market’s reading of precisely this residual exposure.

What the Oracle-OpenAI deal tells enterprises about AI procurement in 2026

The structural argument above has practical implications for any organisation making AI vendor commitments or evaluating AI infrastructure investments over the next 12 months.

The value chain hierarchy established earlier provides the clearest guide: invest above the model layer, in data pipelines, workflow integration, and governance infrastructure. These assets compound over time. Model subscriptions may not.

The Andreessen Horowitz 2025 enterprise AI survey of 100 CIOs found that procurement patterns have shifted to mirror traditional software buying, with rigorous internal evaluations and explicit switching cost analysis, a structural change that makes the frontier versus open-source cost-benefit calculation a standard part of renewal negotiations rather than an edge-case consideration.

- Audit use case fit before committing to premium frontier spend. Conduct internal pilots comparing frontier and open-source model performance on actual workloads. Use the 80-90% coverage threshold as the benchmark; if open-source models handle the vast majority of use cases adequately, the premium may not be justified.

- Invest above the model layer in durable workflow assets. Data pipelines, security architecture, governance frameworks, and organisational change management are the investments that accumulate value regardless of which model sits underneath.

- Build open-source benchmark monitoring into contract renewal cycles. Treat open-source benchmark performance and internal pilots as regular inputs to procurement decisions, not one-time evaluations. The capability gap narrows on a cadence measured in months, not years.

- Scrutinise infrastructure provider concentration risk. If a provider’s growth story depends heavily on a single AI customer whose unit economics remain speculative, that dependency should be factored into pricing discussions and contract terms.

The concentration risk signal embedded in the Oracle-OpenAI deal is not unique to Oracle. Any infrastructure provider whose forward revenue story depends disproportionately on one customer operating at the model layer faces the same structural exposure. Enterprises negotiating with such providers should treat that dependency as a material input to their risk assessment.

Compute concentration risk appears in similar form at Microsoft, where approximately 45% of Azure’s reported backlog is attributed to OpenAI; any further diversification of OpenAI’s compute spend toward Oracle, AWS, or Google Cloud directly erodes the exclusivity assumption that has underpinned Azure’s competitive narrative.

When infrastructure returns depend on a customer’s unproven revenue model

Oracle’s infrastructure position is technically sound. The data centres are real, the capacity is committed, and the contract terms include structural protections. None of that is in dispute.

What is in dispute is whether the business model of Oracle’s largest forward customer can sustain $60 billion per year in compute charges over a five-year horizon in which open-source models have historically closed the capability gap to prior-generation frontier models within 6 to 12 months. The pace of enterprise procurement shift from frontier APIs to open-source alternatives, the outcome of Oracle’s customer diversification efforts, and whether defensible frontier niches in drug discovery and materials science are large enough to sustain current pricing structures at scale all remain genuinely open questions.

The question is not whether the infrastructure is real, but whether the business model of the primary customer can sustain the compute spend it has committed to, over the timeline the capital investment requires.

That principle extends well beyond this specific deal. Every AI infrastructure announcement at scale, from every provider, carries the same embedded dependency. The infrastructure layer’s returns are always conditional on the economic health of the layers above it. When those layers are exposed to commoditisation dynamics that have already played out repeatedly, the conditionality is not theoretical. It is the central investment question.

For investors wanting to apply this stack analysis to specific position sizing decisions at current valuations, our dedicated guide to moat-driven AI investing examines which AI infrastructure and semiconductor holdings carry Morningstar wide-moat ratings, how the technology sector’s margin of safety has compressed since March 2026, and where the value and growth barbell strategy currently finds the best risk-adjusted entry points.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.