The S&P/ASX 200 Consumer Discretionary Index has delivered annualised returns of just 0.90% over five years, compared with 4.21% per year for the broader ASX 200. Australians shop at JB Hi-Fi, Harvey Norman, and Rebel Sport constantly, yet the stocks housing those brands have chronically trailed the index. With the RBA cash rate back at 4.35% following three consecutive hikes in 2026, and the XDJ sitting approximately 17.5% below its 52-week high as of mid-May 2026, the sector’s structural sensitivity to rate cycles is playing out in real time. The 2025 easing cycle briefly lifted hopes. The reversal erased them.

This article explains what consumer discretionary stocks on the ASX actually are, why they are wired to underperform during high-rate environments, what the current macro backdrop means for the sector, and how investors should frame their thinking about discretionary exposure in a portfolio.

What “consumer discretionary” actually means on the ASX

Most retail investors recognise the brands. Fewer understand what links them as an investment category, or why familiarity with a shop front tells them almost nothing about the stock behind it.

The ASX Consumer Discretionary sector covers goods and services that consumers purchase with income left over after essentials such as groceries, utilities, and rent. This distinguishes it from Consumer Staples, which captures the non-negotiable spending categories. The benchmark tracking these names is the S&P/ASX 200 Consumer Discretionary Index (XDJ), and it spans a wide range of subsectors:

- Electronics and technology retail

- Travel and leisure

- Apparel and fashion

- Furniture and homewares

- Recreational goods and sporting equipment

- Automotive accessories

That breadth creates a counterintuitive reality. Names as different as JB Hi-Fi (JBH), Harvey Norman (HVN), Flight Centre (FLT), Super Retail Group (SUL), Premier Investments (PMV), Temple and Webster (TPW), and Wesfarmers (WES) via Kmart and Target all sit inside the same sector classification, making blanket comparisons between constituents difficult.

Over five years, the XDJ has returned just 0.90% annualised, versus 4.21% per year for the ASX 200. Brand recognition has not translated into index-beating returns.

When big ASX news breaks, our subscribers know first

Why interest rates are the sector’s most powerful external force

The link between rates and discretionary spending is not abstract. It operates through three specific channels, each compounding the others.

- Mortgage repayments. When the RBA raises rates, Australian variable-rate mortgage holders face higher repayments immediately. The cash that would have funded a new television, a holiday booking, or a wardrobe refresh gets redirected to the bank. Discretionary retailers feel the withdrawal within weeks.

Headline inflation reaching 4.6% in March 2026 provided the primary justification for the May hike, though the trimmed mean held at 3.3%, meaning the acceleration reflects volatile energy components rather than a broad deterioration in underlying price pressures, a distinction with direct implications for how many further hikes the RBA is likely to deliver.

- Consumer confidence. Even households without mortgages defer big-ticket purchases when sentiment is depressed. The Westpac-Melbourne Institute Consumer Sentiment Index sat at 82.9 in May 2025, well below the neutral 100 level. The ANZ-Roy Morgan Consumer Confidence reading for April 2025 came in at 80.1, against a long-run average of approximately 112. Confidence had been stuck around 80 for much of 2024 and 2025, according to ANZ commentary.

- Housing turnover. Fewer property sales mean fewer purchases of furniture, appliances, and homewares. This channel hits home-related discretionary names such as Harvey Norman and Temple and Webster directly.

The Westpac-MI “time to buy a major household item” sub-index was hovering near GFC-era lows as of May 2025, highlighting the depth of pressure on discretionary retailers.

CBA Household Spending Insights data for March 2025 confirmed the pattern: household goods, clothing and footwear, and recreation all lagged, while essential categories led. Understanding these three transmission channels gives investors a diagnostic toolkit. Rather than reacting to quarterly earnings in isolation, they can read macro signals to anticipate sector-wide pressure before it appears in results.

Five years of evidence: how the rate cycle shaped sector returns

The relationship between rates and discretionary performance is not theoretical. Company-level earnings data and index returns have moved in lockstep through the cycle.

JB Hi-Fi reported group sales up 1.2% in the first half of FY25 (to 31 December 2024), but net profit fell approximately 7%, with management citing cautious consumer behaviour around big-ticket electronics. Harvey Norman’s Australian franchisee sales declined approximately 3-4% over the same period, with profit down by double digits and particular weakness in furniture and household goods. Chair Gerry Harvey noted the business is “highly sensitive to the interest rate cycle.”

Flight Centre posted stronger revenue and profit growth, benefiting from continued post-COVID travel recovery, though CEO Graham Turner flagged that “sustained pressure on disposable incomes could temper leisure travel growth.” Super Retail Group saw modest sales growth, but like-for-like performance slowed across Supercheap Auto, Rebel, and BCF as higher rates and living costs weighed on volumes.

| Company | Category | 1H FY25 Profit Direction | Key Headwind Cited |

|---|---|---|---|

| JB Hi-Fi (JBH) | Electronics | Down ~7% | Cautious consumer, big-ticket weakness |

| Harvey Norman (HVN) | Furniture / homewares | Down double digits | Housing turnover, mortgage pressure |

| Flight Centre (FLT) | Travel | Up (travel recovery) | Disposable income pressure on leisure |

| Super Retail Group (SUL) | Sports / auto / leisure | Modest growth, slowing | Weak consumer, promotional intensity |

The Australian Bureau of Statistics reported that per-capita household consumption fell for four consecutive quarters through the end of 2024. ABS retail trade data for March 2025 showed trend spending broadly flat in per-capita terms, with discretionary categories described as “subdued.”

Australia’s per-capita recession, confirmed by ABS data showing GDP per capita growth of only 0.4% even as headline output expanded on population growth, forms the structural backdrop that makes the discretionary sector’s underperformance more than a simple rate story: corporate insolvencies set an all-time record in 2025, and NAB capacity utilisation fell to levels consistent with unemployment above 5%, pointing to demand deterioration that extends beyond mortgage belt households.

What the XDJ’s 52-week drop tells investors

The XDJ reached a 52-week high near 4,620 before the 2026 rate reversal took hold. As of mid-May 2026, the index sits around 3,367-3,377, a decline of approximately 17.5%.

That drawdown reflects the market repricing the sector as the anticipated easing cycle proved temporary. For context, the XDJ was up approximately 3.1% year-to-date and 6.8% over the prior 12 months as of May 2025. The contrast illustrates how quickly rate sentiment can reverse sector fortunes.

The 2025-2026 rate reversal: a case study in why timing matters

The RBA held the cash rate at 4.35% through mid-2025, then implemented a cutting cycle that provided the monetary relief forecasters had been anticipating. The XDJ responded. Consumer sentiment showed early signs of stabilisation. Broker upgrades followed.

Then inflation resurfaced. The RBA reversed course with three consecutive hikes in 2026, the most recent being a 25 basis point increase on 5 May 2026, restoring the cash rate to 4.35%. The entire easing cycle was unwound.

The RBA monetary policy decision of 5 May 2026 confirmed the 25 basis point increase that restored the cash rate to 4.35%, completing the full reversal of the 2025 easing cycle and resetting the sector’s macro headwind to its prior level.

The Westpac-MI Consumer Sentiment Index for April 2026 came in at 80.1, confirming that confidence remained depressed as hikes resumed. The sector’s brief recovery and subsequent re-collapse carries a specific investor lesson: a single rate cut, or even a short cutting cycle, is not sufficient to structurally re-rate consumer discretionary stocks. Durability matters more than direction.

ANZ Research noted in April 2025 that the environment implied “a prolonged period of restraint on discretionary spending.” The subsequent 2026 reversal has brought the sector back to a similar juncture.

Before increasing discretionary exposure, investors should look for:

- A sustained RBA easing cycle with multiple consecutive cuts, not a single move

- Consumer confidence recovering above the 100 neutral level on a sustained basis

- Per-capita consumption returning to positive growth

- Housing turnover lifting, particularly for home-related names

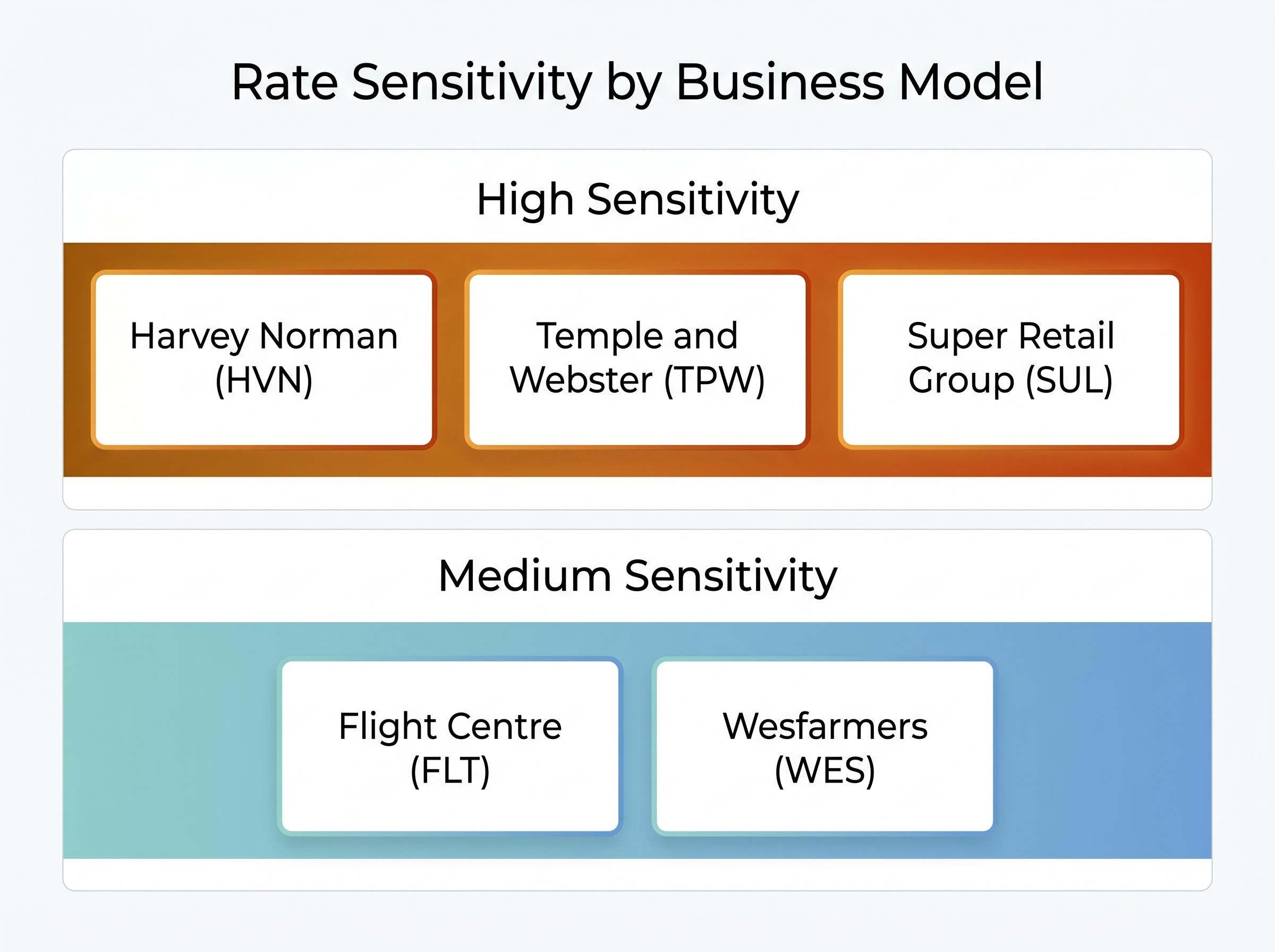

Not all discretionary stocks move the same way

Rate sensitivity within the sector varies meaningfully by business model. Treating the XDJ as a monolithic bet misses important distinctions.

Harvey Norman and Temple and Webster sit at the high end of the sensitivity spectrum. Both are directly linked to housing turnover and big-ticket deferred purchases, the categories that compress first when mortgage repayments rise. Morgan Stanley noted in March 2025 that Harvey Norman’s earnings were “geared to a recovery in housing turnover and a lower cash rate.”

Flight Centre occupies a different position. Its fortunes are more exposed to post-COVID travel normalisation and corporate travel demand than to mortgage rates directly. Goldman Sachs observed in February 2025 that Flight Centre was considered less rate-sensitive than electronics or furniture retailers, though discretionary travel “has historically softened when interest rates stay restrictive for an extended period.”

Why sector classification can mislead

Wesfarmers illustrates the point most clearly. Despite sitting within the consumer discretionary classification via Kmart and Target, Bunnings contributes over half of the group’s total operating profit, and the business spans chemicals, industrial safety, and fertilisers. Wesfarmers achieved annualised revenue growth of 9.2% across the three years preceding May 2026, even through an elevated-rate environment.

Retail REIT landlords such as Scentre Group and Vicinity Centres sit at an unusual intersection with the discretionary sector: their near-100% occupancy rates and positive leasing spreads of 3.3-4.6% as of early 2026 confirm that physical foot traffic into discretionary retail remains structurally sound even as the listed retailers inside those centres report earnings pressure from cautious consumer spending.

Yet even that operational resilience could not insulate the share price entirely. WES declined 12.3% from the start of 2025 through May 2026, demonstrating that sector-level de-rating can drag operationally strong constituents lower.

| Company | Primary Rate Sensitivity Channel | Degree of Sensitivity | Key Differentiating Factor |

|---|---|---|---|

| Harvey Norman (HVN) | Housing turnover, mortgage burden | High | Big-ticket furniture and appliance focus |

| Temple and Webster (TPW) | Housing turnover, deferred purchases | High | Online homewares leveraged to housing cycle |

| Flight Centre (FLT) | Disposable income, travel sentiment | Medium | Corporate travel provides partial buffer |

| Wesfarmers (WES) | Discretionary retail (Kmart, Target) | Medium | Bunnings and industrial diversification |

| Super Retail Group (SUL) | Discretionary sports, auto, leisure | High | Cyclical, leveraged to easing (Macquarie) |

Macquarie described Super Retail Group in February 2025 as “a cyclical discretionary name likely to benefit meaningfully from any easing in monetary policy.” UBS noted JB Hi-Fi was “highly leveraged to any improvement in discretionary demand once rate cuts arrive.” The implication runs both ways: names most leveraged to a recovery are also most exposed when the recovery stalls.

The next major ASX story will hit our subscribers first

How to think about discretionary exposure from here

With the cash rate at 4.35% as of 16 May 2026, consumer sentiment still around 80, and the XDJ down approximately 17.5% from its highs, the sector sits in a structurally challenged position. Some of that difficulty may already be reflected in prices.

The distinction that matters is between a valuation signal and a macro catalyst. A depressed share price, or a dividend yield above historical averages for some discretionary names, signals the market has already repriced risk. Wesfarmers, for instance, trades at a current dividend yield of approximately 2.76-2.80%, compared with a five-year historical average of approximately 3.36-3.40%. The current yield sitting below its long-run average may indicate the share price remains above long-run valuation norms even after the recent decline.

Contrarian positioning in consumer staples has attracted institutional capital precisely because the same rate environment depressing discretionary names has pushed staples price-to-earnings multiples near multi-year lows, with Morningstar Investment Management and Franklin Templeton both selectively increasing exposure to Woolworths and household goods stocks as of early 2026, treating the weak macro backdrop as an entry signal rather than a warning.

Valuation is a necessary condition for a recovery thesis, not a sufficient one. The macro catalyst has to arrive as well. Investors should monitor four conditions before increasing discretionary exposure:

- A credible RBA easing cycle with multiple consecutive cuts

- Consumer confidence recovering sustainably above 100

- Per-capita retail spending returning to positive growth

- Housing turnover lifting, particularly for home-related names

CBA Economics Head of Australian Economics Gareth Aird noted in April 2025: “The consumer remains the weakest part of the economy… interest rate relief is still some way off, which will cap any meaningful recovery in discretionary outlays.” The subsequent 2026 rate reversal has brought the sector back to a similar juncture.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results.

The rate cycle is the story, not the brands

The ASX Consumer Discretionary sector’s structural underperformance over five years is not a reflection of poor management or unrecognised brands. It is a reflection of the sector’s fundamental wiring to household cash flow and rate cycles.

Sector-level thinking requires reading the macro environment first, then assessing individual business models for their specific sensitivity profile, before evaluating valuation signals. As of May 2026, the sector faces the same restrictive backdrop it faced through much of 2024 and 2025, with the added lesson that a single easing cycle is no guarantee of a durable recovery. The conditions worth watching are a sustained rate descent, genuine consumer sentiment recovery, and positive per-capita spending trends.

Investors seeking to go deeper on specific names within the sector should consult company ASX announcements, current broker research, and updated earnings releases for the most recent trading conditions. The macro framework provided here should serve as the lens through which that stock-level analysis is interpreted.