Why DDM Gives ASX Bank Shares a $7 to $32 Valuation Range

1 hr ago

With A$14.14 million in cash against A$59.68 million in annual operating outflows, Imugene entered 2026 with less than three months of runway. The company was not in clinical trouble. It was in a funding trap.

For Australian retail investors, the most misunderstood risk in ASX small-cap biotech investing is not trial failure. It is the near-certain dilution that occurs when a company exhausts its cash before reaching the next value-creating catalyst. That dilution erodes investor returns even when the science ultimately works. In 2026, the gap between well-funded and dangerously underfunded ASX biotechs has never been more visible, or more instructive.

This guide teaches investors how to read cash position data, model burn rate risk, and distinguish adequate funding from dangerous funding, using three real ASX companies as contrasting case studies: PYC Therapeutics (runway to 2030), Kazia Therapeutics (runway to H2 2028), and Imugene (months of runway at time of writing). The analytical framework that follows is designed to be applied to any ASX biotech position, current or prospective, in under 30 minutes.

The headline always lands first. A Phase 2 readout. A regulatory submission. A partnership announcement. ASX biotech investors understandably anchor on pipeline news because it promises the largest single-day share price moves, up or down. Balance sheet data, by comparison, feels like background noise.

That instinct creates a blind spot. Dilution from emergency capital raises is not an exceptional event in pre-revenue biotech. It is a structural feature of the model. Companies with no revenue must raise equity to survive, and the terms of those raises depend almost entirely on how much cash remains when the raise occurs.

Imugene’s share price declined approximately 87% over the 12 months prior to April 2026, a period in which compounding dilution from repeated raises at low cash levels ran alongside clinical uncertainty. The Opthea Phase 3 failure in March 2025 is the kind of event investors instinctively fear most: a binary clinical outcome that wipes out value overnight. But that kind of failure is relatively rare. Dilution, by contrast, is near-universal across pre-revenue biotechs.

The ASX small-cap biotech segment typically carries market capitalisations ranging from below A$100 million to approximately A$1 billion, with no or minimal revenue. At that scale, balance sheet health is the primary survival variable.

ASIC’s MoneySmart investment warnings classify speculative small-cap equities as high-risk investments requiring investors to understand the full range of ways capital can be eroded, a category that encompasses the dilution mechanics described throughout this guide as much as the binary clinical failure events that typically attract more investor attention.

Three categories of risk apply to every ASX biotech position:

Dilution risk is more frequent and more predictable than trial failure risk. It can be measured from publicly available filings, modelled forward with basic arithmetic, and monitored quarterly. Investors who do not assess it are making decisions with an incomplete picture.

Three metrics form the foundation of any biotech funding analysis. Each builds on the one before it, and together they convert raw financial filings into a readable signal about a company’s near-term survival.

Cash burn rate is the total operating cash outflows per quarter (or annualised), sourced directly from the company’s ASX Appendix 4C quarterly cash flow report. This is the filing ASX-listed companies are required to lodge each quarter, and it is freely available on the ASX company announcements platform. It should be the first document an investor reads before any broker research or company presentation.

Cash runway is the result of dividing current cash holdings by the quarterly burn rate, expressed in quarters or months. The output tells an investor how long a company can continue operating at its current spending rate before it must raise new capital.

Dilution risk is the proportional reduction in each existing shareholder’s ownership stake when new shares are issued. The mechanism is straightforward: more shares outstanding means each existing share represents a smaller fraction of the company. Emergency raises, typically conducted at a discount to market price, amplify the dilutive effect because more shares must be issued per dollar raised.

The calculation itself takes three steps:

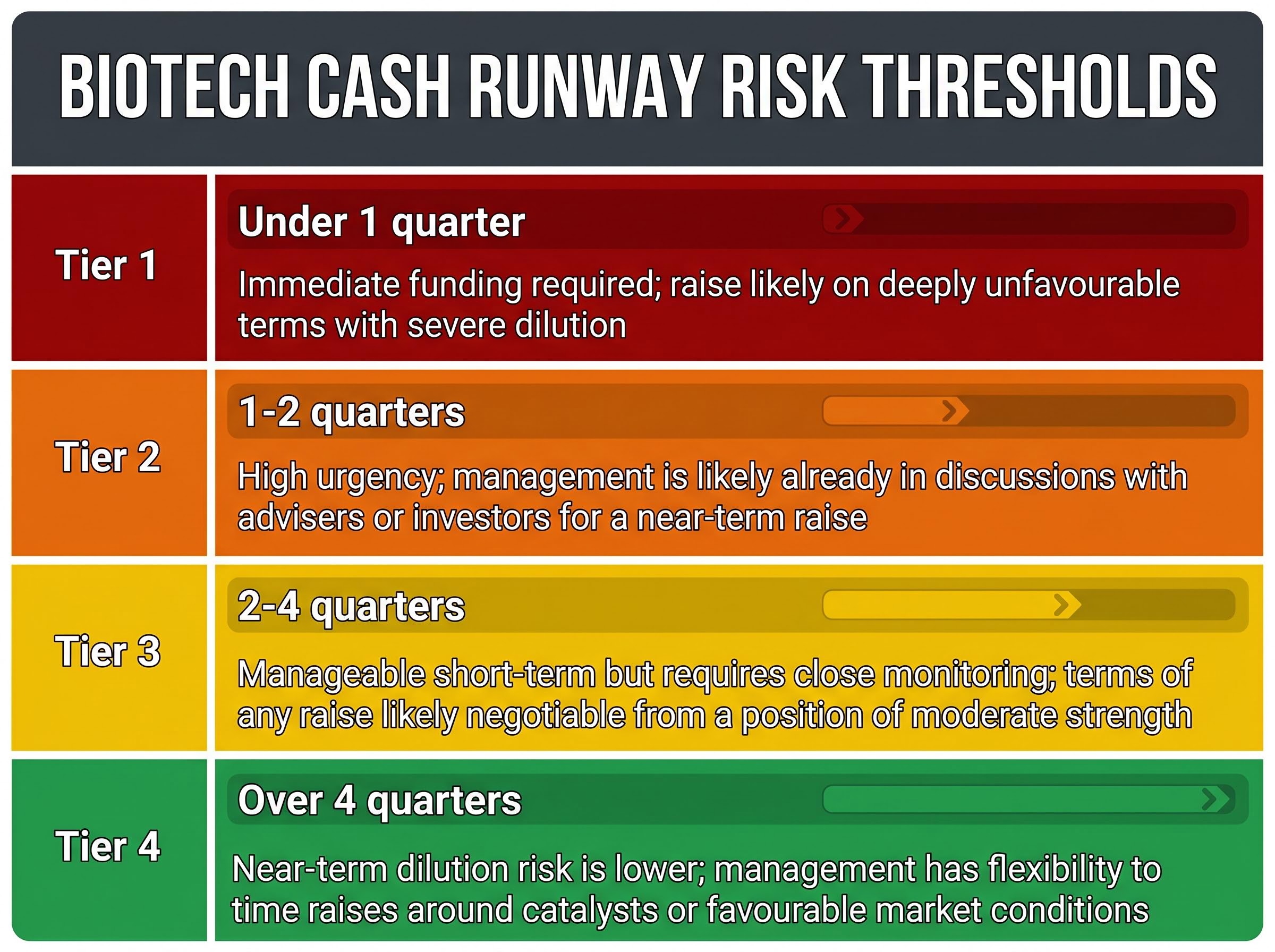

As a worked example: Imugene’s March 2026 4C showed A$5.96 million in cash against A$9.67 million in quarterly outflows. That implies less than one quarter of runway without a raise, placing the company firmly in the most critical threshold band.

| Runway Threshold | Investor Implication |

|---|---|

| Under 1 quarter | Immediate funding required; raise likely on deeply unfavourable terms with severe dilution |

| 1-2 quarters | High urgency; management is likely already in discussions with advisers or investors for a near-term raise |

| 2-4 quarters | Manageable short-term but requires close monitoring; terms of any raise likely negotiable from a position of moderate strength |

| Over 4 quarters | Near-term dilution risk is lower; management has flexibility to time raises around catalysts or favourable market conditions |

Simply Wall St tracks net loss trajectory and price-to-book (P/B) ratio as secondary signals for monitoring dilution accumulation over time, providing an additional layer beyond the raw 4C data.

The three companies profiled below span the full spectrum from well-capitalised to critically underfunded. The contrast is deliberate. Read together, they reveal how a company’s position on the funding spectrum shapes the mechanics, terms, and shareholder impact of every capital event that follows.

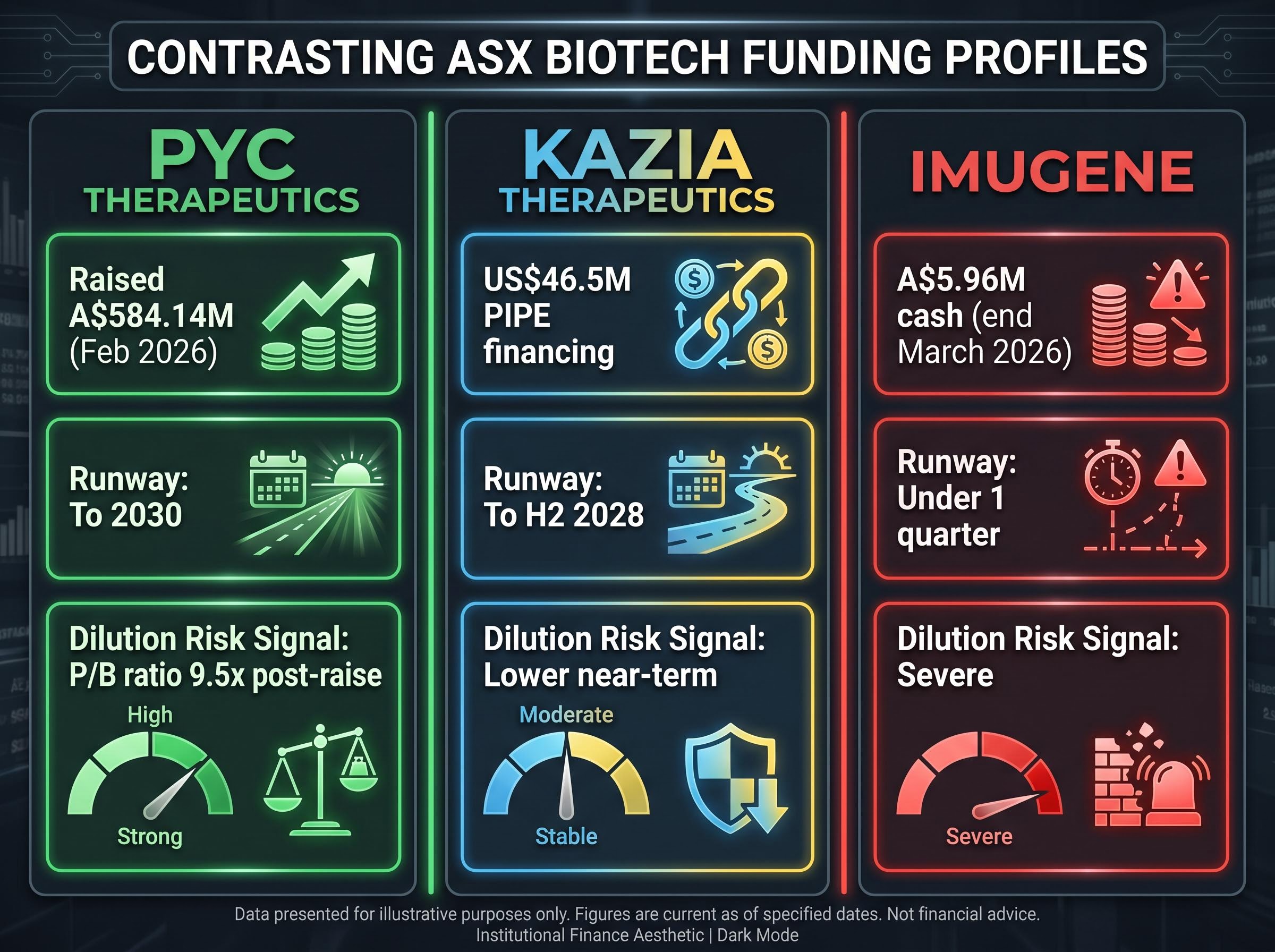

| Company | Cash Position / Raise | Runway | Raise Type | Dilution Risk Signal |

|---|---|---|---|---|

| PYC Therapeutics | A$584.14M raised (Feb 2026) | To 2030 | Placement + entitlement offer with US healthcare specialists | P/B ratio 9.5x post-raise |

| Kazia Therapeutics | US$46.5M PIPE financing | To H2 2028 | PIPE with institutional investors (dual ASX/NASDAQ listed) | Lower near-term; structured capital access |

| Imugene | A$5.96M cash (end March 2026) | Under 1 quarter | Emergency-style raises (March + April 2026) | Severe; repeated raises at low cash levels |

PYC Therapeutics announced a capital raise on 2 February 2026 for up to A$653 million through a placement and entitlement offer. By 4 February, the placement and institutional entitlement offer had secured approximately A$537 million, with total equity raised reaching approximately A$584.14 million. The raise was conducted with leading US healthcare specialist investors, a participation profile described as a signal of platform credibility.

The result: cash runway exceeding A$750 million, extending operations to 2030. Against an annual net loss of approximately A$50.3 million for full-year 2025, the buffer is substantial. Dilution has already occurred, and Simply Wall St flagged a post-raise P/B ratio of 9.5x relative to peers. But the terms were favourable, the investor base institutional, and the multi-year runway eliminates near-term emergency funding pressure.

For investors who want to understand what a well-structured ASX biotech raise looks like in full detail, our dedicated guide to the PYC Therapeutics $653M raise examines the specialist US life sciences investor composition, the equal-terms retail entitlement offer structure, and why the four-program pipeline architecture made the raise credible to institutional allocators.

Kazia Therapeutics secured PIPE (private investment in public equity) financing of US$46.5 million, extending its cash runway to H2 2028. The company’s dual listing on both the ASX and NASDAQ provides access to Australian retail and US institutional capital pools, a structural advantage when negotiating raise terms.

An April 27, 2026 investor update highlighted the strong runway alongside a multi-modal oncology pipeline. A runway extending more than two years from the current date provides meaningful insulation from the kind of near-term dilution events that compress share prices in underfunded peers.

Imugene’s cash position deteriorated rapidly through early 2026. By the end of March 2026, cash had fallen to A$5.96 million against quarterly operating outflows of A$9.67 million, implying less than one quarter of runway.

The company launched a A$20 million raise on 11 March 2026, followed by completion of a A$16 million package on 22 April 2026 (including A$2.18 million from a share purchase plan). The structural disadvantage of raising at critically low cash levels was visible in the mechanics: smaller raise amounts relative to annual burn (A$59.68 million), higher dilution per dollar raised, and a market signal of financial distress that compresses pricing power on every subsequent raise.

The pattern across all three cases is clear. The terms, timing, and depth of capital raises are profoundly different when conducted from strength versus desperation. Funding risk is not binary; it is a spectrum, and a company’s position on that spectrum shapes every capital event it undertakes over the following one to three years.

For investors wanting to understand the structural mechanics behind the funding pressure, our full breakdown of Imugene’s March 2026 capital raise details the convertible note restructuring, the SPP underwrite terms, and the cascading option incentives that shaped the deal, providing the complete picture behind the numbers referenced in this case study.

The following five-step process converts the framework above into a repeatable pre-investment check. Each step uses ASX-specific data sources, and the entire process takes under 30 minutes once the sources are familiar.

Algorae Pharmaceuticals’ April 2026 raise demonstrates discount placement mechanics at the smaller end of the ASX biotech scale: shares priced at A$0.012 represented a 25% discount to the last traded price, a discount level that signals weak demand or urgency and directly reduces the dollar-per-dilution efficiency of the raise for existing shareholders.

A common and costly mistake is accepting company-stated runway guidance at face value. Presentations frequently describe funding as “sufficient to advance our pipeline” without specifying a runway date in quarters or months. Independently calculating the burn rate from the 4C, then comparing it to the company’s stated position, reveals whether the characterisation is supported by the numbers.

Warning signal: A company whose independently calculated runway is under two quarters, but whose presentations describe funding as “sufficient” without a specific runway date, warrants immediate deeper investigation rather than reassurance.

Platforms including Simply Wall St, InvestingPro, and Kalkine provide secondary analytical layers, tracking metrics such as P/B ratios, net loss trajectories, and share issuance histories that supplement the 4C-based runway calculation.

Short interest data provides a complementary institutional signal that can precede the balance sheet deterioration visible in 4C filings: as the Lotus Resources case from April 2026 illustrates, institutional short sellers had lifted short interest to approximately 11% weeks before the stock fell 34%, suggesting that funding stress and commercial headwinds were being priced by sophisticated participants before retail investors had identified the risk.

Calculating runway is the mechanical step. The qualitative step, distinguishing genuine financial security from the language of financial security, is where the real analytical skill lies. ASX biotech communications are designed to present the most positive framing available, and the difference between a company that is funded and a company that describes itself as funded can be measured in years of runway.

Five characteristics define genuinely adequate funding:

PYC’s runway to 2030 represents a benchmark for genuinely adequate funding in a multi-programme early-stage context. The caveat is that a net loss of A$22.83 million for H1 2025 alone illustrates why the raise needed to be large. Clinuvel Pharmaceuticals, with A$233 million in cash, 20 consecutive profitable half-years, and zero equity raises since 2016, represents a fundamentally different category of ASX biotech financial health, though it is atypical for early-stage companies.

At the other end, Imugene’s sequence (A$14.14 million cash, A$59.68 million annual burn, cash falling to A$5.96 million by end of March 2026 before emergency raises) represents the benchmark for inadequate funding management.

Four phrases commonly found in ASX biotech announcements should prompt deeper investigation rather than reassurance:

Even well-funded companies carry dilution risk. PYC’s post-raise P/B ratio of 9.5x illustrates that a large successful raise is not costless to existing shareholders. But the terms are categorically better than emergency dilution, and the multi-year buffer transforms the company’s negotiating position for any future capital event.

Funding risk operates independently of clinical quality. A company can have genuinely promising science, strong trial data, and a credible management team, and still destroy investor value through repeated dilutive raises before any catalyst is reached. The funding clock does not pause for promising interim readouts or conference presentations.

The three companies profiled in this guide will continue to evolve. Cash positions will change, new raises will be announced, and clinical timelines will shift. The specific snapshots captured here reflect conditions as of early May 2026. The analytical framework, calculating runway from 4C filings, interpreting the result against the threshold bands, and reading the qualitative signals around raise terms and investor composition, is the durable takeaway.

Apply the runway calculation to any ASX biotech currently held or under consideration. The 4C is public. The arithmetic takes five minutes. The insight it provides may be the most consequential variable in the position.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Cash runway is the number of quarters a company can continue operating before it must raise new capital, calculated by dividing its current cash balance by its quarterly operating outflows. For ASX biotech investors, a short runway signals imminent dilutive capital raises that can erode shareholder value even when the underlying science is sound.

Download the company's most recent Appendix 4C quarterly cash flow report from the ASX announcements platform, identify the quarterly operating cash outflow, then divide the closing cash balance by that figure to get the runway in quarters. A result under two quarters warrants immediate deeper investigation before investing.

Clinical risk is the possibility a drug fails its trial endpoints, while funding risk is the possibility a company exhausts its cash before reaching a value-creating milestone, forcing dilutive raises on unfavourable terms. Funding risk is more frequent and more predictable than clinical failure, and can be measured directly from public filings.

Imugene held just A$5.96 million in cash against quarterly outflows of A$9.67 million at the end of March 2026, giving it less than one quarter of runway, while PYC Therapeutics raised approximately A$584 million in February 2026, securing a cash runway extending to 2030. The contrast illustrates the extreme range of funding risk across ASX biotech companies.

Phrases such as 'well-funded to advance our pipeline' without a specific runway date, 'sufficient cash to reach key milestones' without naming those milestones, and 'strategic placement' conducted at a significant discount during a period of low cash should all prompt deeper investigation rather than reassurance. These expressions often obscure a deteriorating cash position that independent 4C analysis would reveal.