Peak Processing Hits Third Straight Positive Month as Production Jumps 14%

Peak Processing delivers third consecutive month of positive EBITDA as production guidance lifts

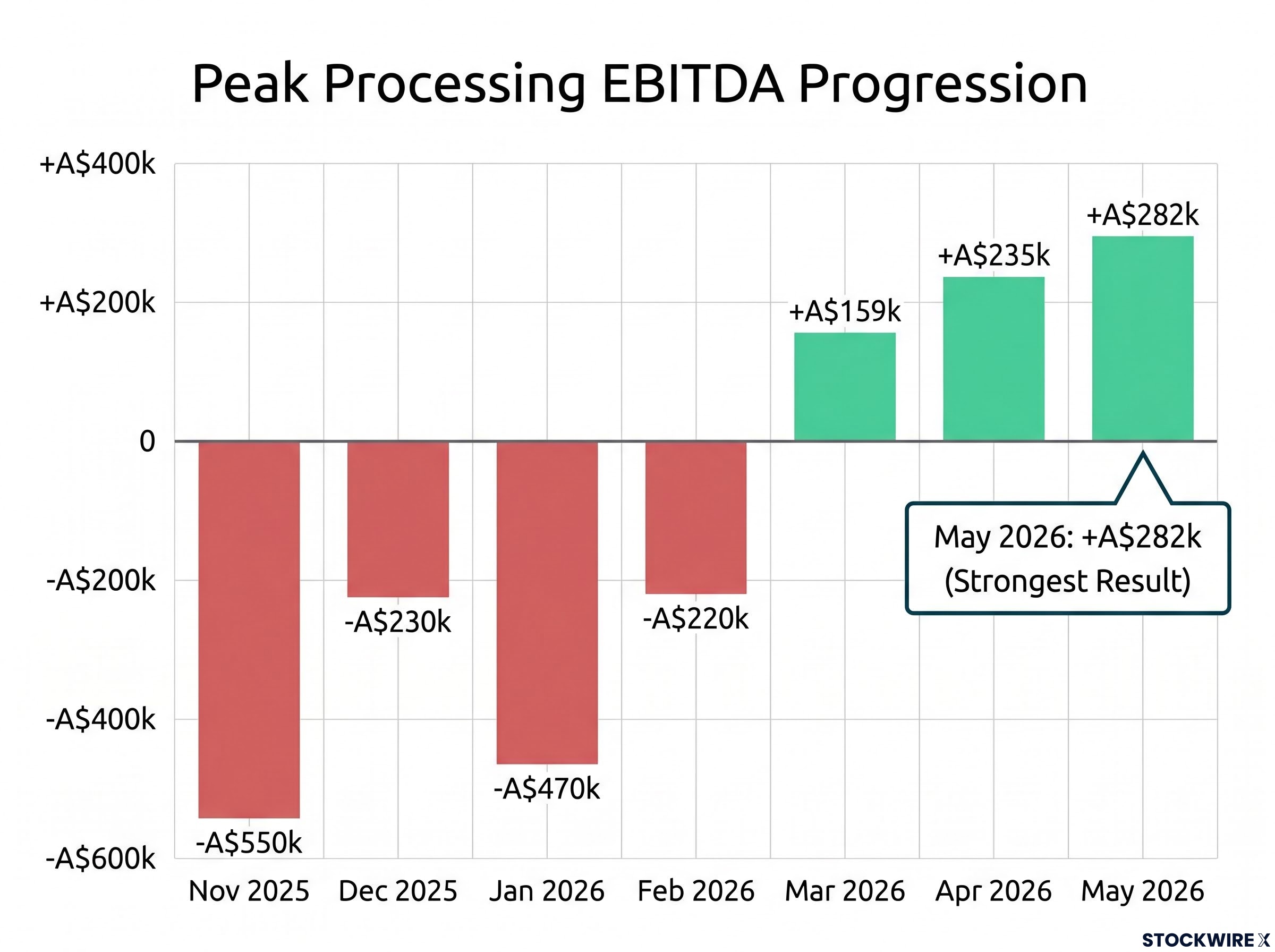

Peak Processing has achieved three consecutive months of positive EBITDA at the consolidated Group level, with May 2026 marking the strongest result at A$282,000 (unaudited). The FMCG manufacturer has lifted Q4 FY26 production guidance to approximately 1.6 million beverage units, up from the original 1.4 million units provided in March 2026.

The EBITDA progression demonstrates accelerating momentum rather than a one-off result. March 2026 delivered A$159,000, followed by A$235,000 in April, before May’s A$282,000 — each month materially stronger than the last. May revenue reached A$1.71 million, the highest monthly result of FY26.

The production guidance upgrade of approximately 200,000 units is based on confirmed customer purchase orders, providing near-term revenue visibility.

When big ASX news breaks, our subscribers know first

What is EBITDA and why does it matter for small-cap investors?

EBITDA (Earnings Before Interest, Tax, Depreciation and Amortisation) measures a company’s operating profitability before accounting for financing decisions, tax obligations, and non-cash charges. For growth companies in FMCG manufacturing — where fixed costs are high — turning EBITDA positive signals the business model is generating enough gross profit to cover operating costs.

Key aspects of EBITDA:

- What it includes: Revenue minus direct costs (materials, labour, overhead) minus operating expenses (sales, marketing, administration)

- What it excludes: Interest payments, tax, depreciation of equipment, and amortisation of intangible assets

- Why it matters: It isolates operating performance from financing structure and non-cash accounting items

For companies like Peak Processing that have been investing in production capacity, crossing into positive EBITDA demonstrates the business has reached a scale where each incremental unit of production contributes to covering fixed costs — a prerequisite for sustainable profitability.

Monthly performance breakdown shows clear H2 earnings inflection

The second half of FY26 reveals a sharp inflection point in Peak Processing’s operating performance. The company moved from four consecutive months of negative EBITDA (November through February) to three consecutive months of positive results, with each positive month showing sequential improvement.

| Month | Revenue (A$m) | EBITDA (A$) | EBITDA Status |

|---|---|---|---|

| November 2025 | 0.85 | -550,000 | Loss |

| December 2025 | 1.22 | -230,000 | Loss |

| January 2026 | 1.43 | -470,000 | Loss |

| February 2026 | N/D | -220,000 | Loss |

| March 2026 | N/D | +159,000 | Positive |

| April 2026 | N/D | +235,000 | Positive |

| May 2026 | 1.71 | +282,000 | Positive |

The trend demonstrates genuine operating leverage rather than a temporary margin spike.

Production guidance upgrade signals demand strength

Q4 FY26 production has been lifted to approximately 1.6 million beverage units from the original 1.4 million guidance provided on 17 March 2026. The upgrade is based on confirmed customer purchase orders rather than forecasts.

Key figures:

- Original Q4 guidance: ~1.4 million units (17 March 2026 announcement)

- Revised Q4 guidance: ~1.6 million units

- Uplift: ~200,000 additional units

Guidance upgrades backed by confirmed purchase orders provide visibility into near-term revenue. This represents demand-driven growth rather than production-push, indicating customer adoption is accelerating across Peak Processing’s product range.

The Electric Brands manufacturing agreement, covering 1.4 million units annually with exclusivity provisions and up to eight-year renewal options, represents one of the anchoring customer relationships driving the confirmed purchase order pipeline behind the guidance upgrade.

The Q4 production ramp built on a 28% quarter-on-quarter surge in Q3 and a near-perfect 99.75% OTIF delivery rate, with the St. Peter’s Beverages manufacturing agreement expanding by 250% to underpin the volume uplift.

Cost base reset and product pipeline underpin outlook

The reduced fixed-cost structure established in H1 FY26 has been a key enabler of the EBITDA turnaround. With more than 30 additional product listings scheduled to launch between June and September 2026, management expects the operating leverage demonstrated in H2 FY26 to support continued positive trading into Q4 FY26 and beyond.

The combination of a lower cost base, rising production volumes, and an expanding product range creates a compounding effect on operating margins. Each incremental unit of revenue carries higher margin contribution due to fixed costs being spread across a larger production base.

The H1 FY26 cost restructuring referenced in the announcement provides the foundation for current leverage, allowing volume growth to convert directly into improved profitability.

Managing Director commentary

Barry Katzman, Managing Director & CEO

“March marked a clear turning point for Peak, and delivering positive EBITDA in each of the three months since, each stronger than the last, shows the inflection is real and holding. With Q4 production now tracking ahead of our original guidance and a materially lower cost base, we are now converting volume growth into sustainable positive performance.”

Management’s emphasis on the inflection being “real and holding” distinguishes this from a one-off result. The statement frames the turnaround as sustainable rather than temporary, with production momentum and cost discipline both contributing to the positive trajectory.

The next major ASX story will hit our subscribers first

Investment outlook

For investors tracking Peak Processing’s turnaround, this update provides multiple confirming data points rather than a single milestone. The trajectory matters more than any individual month, and the consistency of improvement suggests the inflection is structural rather than cyclical.

Key takeaways for investors:

- Consecutive positive EBITDA: Three months of positive results with month-on-month improvement (A$159k → A$235k → A$282k) demonstrates genuine operating leverage

- Production guidance upgrade: The increase to 1.6 million units for Q4 FY26 is backed by confirmed customer purchase orders, providing near-term revenue visibility

- Expanding product pipeline: More than 30 additional product listings scheduled for June-September 2026 support continued revenue growth

- Cost base reset: The H1 FY26 restructuring enables each incremental revenue dollar to contribute more meaningfully to profitability

The combination of rising volumes, lower fixed costs, and an expanding product range creates a compounding effect on margins. Management expects this operating leverage to support continued positive trading into Q4 FY26 and beyond.

Want the Next FMCG Turnaround in Your Inbox?

Join 20,000+ investors receiving FREE breaking ASX news delivered within minutes of release, complete with in-depth analysis. Click the “Free Alerts” button at StockWire X to get real-time alerts covering Tech, Healthcare, Finance, Consumer, and Manufacturing sectors the moment market-moving announcements drop.