Ten analysts collectively rate Zip Co a Buy and see 63-67% upside from current prices. The stock has fallen 31% since January 2025. Both things are true at once, and that tension is exactly what makes the current valuation worth examining. Zip Co (ASX: ZIP) closed at A$2.25 on 19 May 2026, giving the company a market capitalisation of approximately A$2.8 billion. That price reflects a sharp discount from earlier levels, despite the company reporting total income of A$1.08 billion in FY2025 and H1 FY2026 income of A$664 million, already annualising well above that figure. For retail investors watching a growth fintech shed a third of its value while posting record revenue, the question is not abstract: is the market pricing in risks the numbers have not yet revealed, or is this a mispricing? This analysis works through Zip’s financial trajectory, the structural risks embedded in the buy now, pay later (BNPL) model, the current valuation relative to broker consensus, and what a genuinely balanced assessment looks like for an investor deciding whether to act at current prices.

From A$678 million loss to A$1 billion in revenue: how Zip’s financial story changed shape

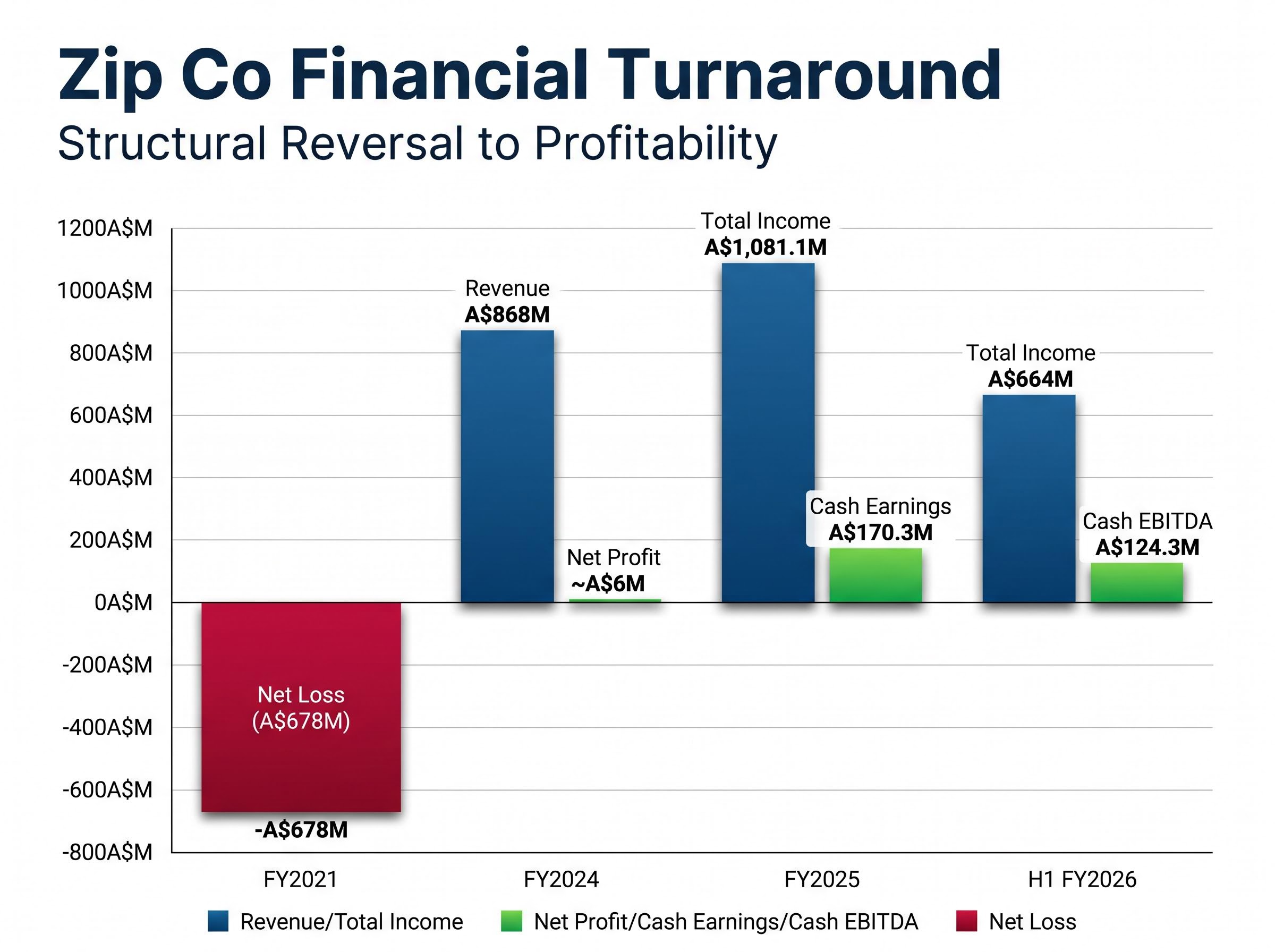

In FY2021, Zip Co posted a statutory net loss of A$678 million. By FY2024, the company reported a statutory net profit before tax of A$25.1 million, approximately A$6 million at the net profit line. That is not a gradual improvement; it is a structural reversal.

The revenue trajectory underpinning that shift was equally steep. Between FY2021 and FY2024, Zip grew revenue at a compound annual growth rate of 75.7%, reaching A$868 million in FY2024. Rather than plateauing at that level, the growth steepened: FY2025 total income reached A$1,081.1 million, up 23.5% year-on-year, and H1 FY2026 income of A$664 million (up 29.2%) puts the annualised run-rate above A$1.3 billion.

Operating leverage in action: Zip’s cash earnings grew 147% year-on-year in FY2025, reaching A$170.3 million, the single clearest signal that revenue growth is now converting into profit at an accelerating rate.

H1 FY2026 cash EBITDA of A$124.3 million reinforces that trajectory. The table below traces the progression across six reporting periods.

| Financial Year | Total Income / Revenue | Net Profit (Loss) | Cash Earnings | TTV |

|---|---|---|---|---|

| FY2021 | — | (A$678M) | — | — |

| FY2024 | A$868M | ~A$6M | — | — |

| FY2025 | A$1,081.1M | Profitable | A$170.3M | A$13.1B |

| H1 FY2026 | A$664M | — | — | A$8.4B |

An investor who only sees the 31% decline is missing the context that the business producing those results looks fundamentally different from the one that was losing A$678 million a year.

The April 2026 surge of approximately 66%, driven by record quarterly cash EBTDA of A$65.1 million and a FY2026 guidance upgrade to a minimum of A$260 million, preceded the subsequent pullback that leaves the stock at its current A$2.25 level, making the recent 31% decline a product of compressed valuation after a sharp re-rating rather than a gradual deterioration.

When big ASX news breaks, our subscribers know first

What Zip Co actually does, and why the BNPL model is harder to sustain than it looks

Zip Co, founded in 2013, operates a buy now, pay later platform. Customers purchase goods or services immediately and repay in interest-free instalments over a short period. Zip earns revenue through several channels:

- Merchant fees charged to retailers for each transaction processed

- Consumer fees applied to certain product tiers

- Interest income earned on longer-term credit arrangements

The company entered the US market through its acquisition of Quadpay in September 2020 and has since scaled to 6.6 million active customers (up 4.1% year-on-year) and 90,600 merchant partners (up 10.5%) as of H1 FY2026. Total transaction volume reached A$8.4 billion in the half, growing 34.1% year-on-year.

Those figures describe a business that is still compounding. The complication is in what the model requires to sustain that growth.

Where the BNPL model is most vulnerable

BNPL businesses scale by extending credit. That creates three structural pressure points.

First, funding cost sensitivity. The Reserve Bank of Australia has maintained relatively elevated cash rates through 2024 into 2025-2026. Higher rates increase the cost of capital underpinning Zip’s loan book, compressing the margin between what the company earns on transactions and what it pays to fund them.

Second, credit loss exposure. Household budget stress flows directly into arrears. When consumers face tighter financial conditions, BNPL repayment rates are among the first indicators to soften.

Third, competitive intensity. Afterpay (via Block’s Square and Cash App ecosystem), Klarna, and bank-backed BNPL alternatives all compete for the same merchant and consumer relationships. Switching costs in the sector remain low, which means network advantages can erode faster than they accumulate.

The regulatory overhang that the share price may already be pricing in

The Australian Government has signalled its intention to bring BNPL products under the National Consumer Credit Protection Act 2009 (NCCP), the same framework that governs traditional consumer lending. Consultation papers and exposure drafts released in 2023-2024 outlined three core obligations:

The Treasury Laws Amendment (Responsible Buy Now Pay Later) Bill 2024 formally proposes amending the National Consumer Credit Protection Act 2009 to capture BNPL contracts, establishing the legislative vehicle through which affordability assessments, hardship provisions, and enhanced disclosure requirements would become mandatory obligations for providers like Zip.

- Affordability and suitability assessments: BNPL providers would need to assess whether a product is appropriate for an individual customer’s financial situation before extending credit

- Mandatory hardship provisions: Providers would be required to offer structured support for customers experiencing financial difficulty

- Enhanced product disclosure: Clearer presentation of fees, repayment schedules, and the consequences of missed payments

Regulatory watchlist item: The direction of reform is clear, but the precise legislative timeline and final form of the NCCP amendments remain unconfirmed. Until the law passes, the risk is live but not fully quantifiable.

The dual nature of regulation complicates the investment calculus. On one hand, compliance costs and product redesign pressures could compress margins. On the other, formal regulation may function as a barrier to entry, entrenching incumbents like Zip that have the scale and infrastructure to absorb compliance requirements while smaller competitors cannot.

How much of the 31% share price decline already reflects regulatory risk, and how much remains unpriced, is one of the harder questions an investor faces at current levels. The answer depends partly on whether the reforms arrive in a form closer to the consultation drafts or are diluted during the legislative process.

A further structural development not fully captured in revenue or regulatory risk discussions is the Australian rebrand order issued by the High Court of Australia in May 2026, requiring Zip to cease using its trade mark in Australia within 28 days; the financial impact is structurally contained given the US business generates approximately 80% of divisional cash earnings, but the transition adds operational complexity to an already closely watched period.

What analysts see that the market does not: the bull case unpacked

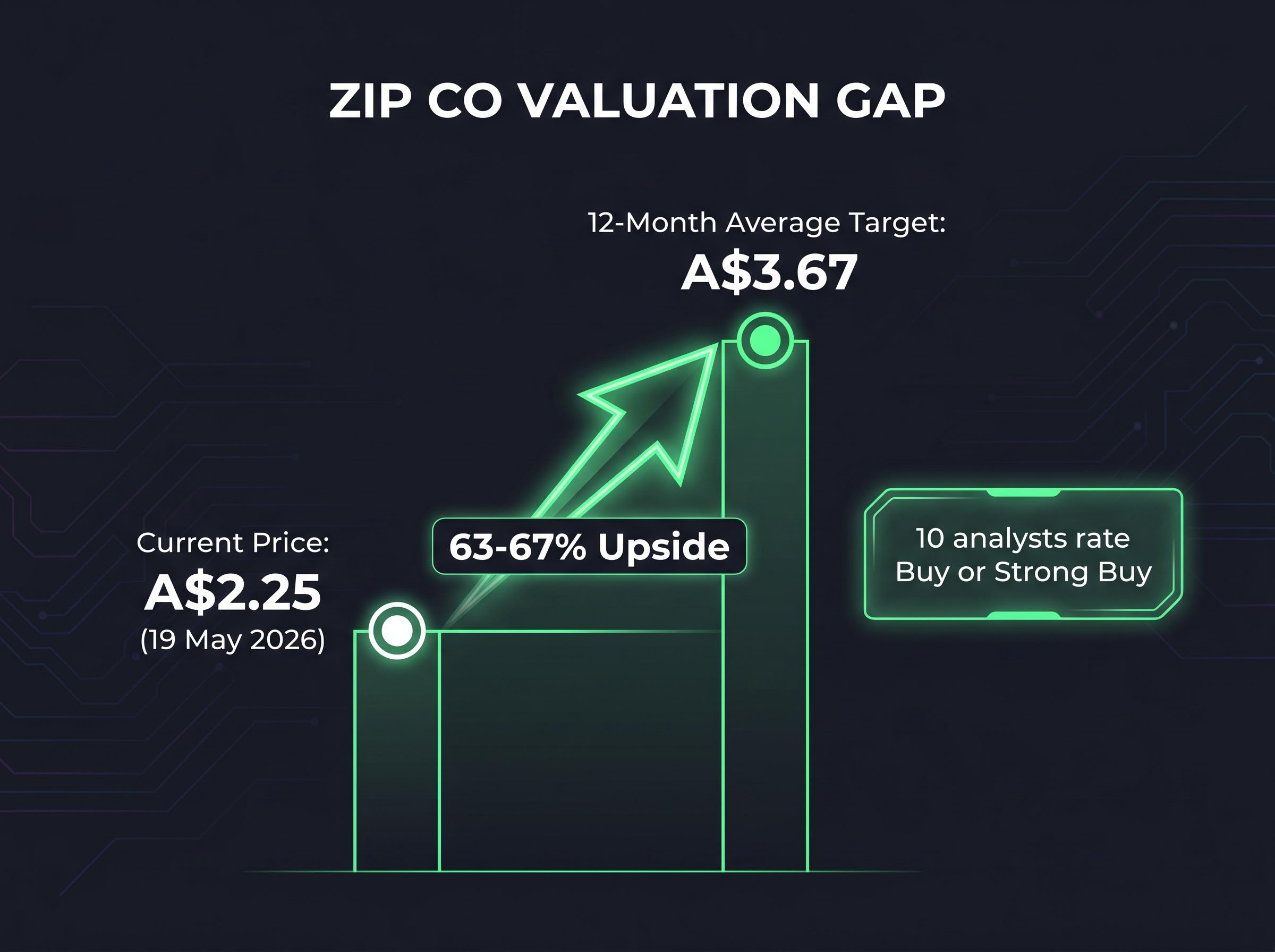

The mispricing thesis in one number: Ten analysts rate Zip Co a Buy or Strong Buy, with an average 12-month price target of A$3.67, implying 63-67% upside from the current price of approximately A$2.25.

That consensus target, compiled by Investing.com and MarketScreener as of May 2026, represents the aggregated view of ten professional analysts. The gap between A$2.25 and A$3.67 is not a signal to act without scrutiny, but it does demand an explanation for why the market disagrees with a consensus of that breadth.

The bull case rests on three specific drivers:

- Revenue run-rate acceleration: H1 FY2026 total income of A$664 million annualises above A$1.3 billion, a meaningful step-up from the A$1.08 billion reported for full-year FY2025

- Operating leverage demonstrated in cash earnings: The 147% year-on-year cash earnings growth in FY2025, followed by H1 FY2026 cash EBITDA of A$124.3 million, shows revenue growth converting into profit at scale

- Network expansion momentum: TTV growth of 34.1% in H1 FY2026, alongside continued customer and merchant additions, signals the platform is still compounding rather than maturing

At a market capitalisation of approximately A$2.8 billion against FY2025 total income of A$1,081 million, the implied trailing price-to-sales ratio sits at roughly 2.6x. That multiple reflects significant execution risk being priced in relative to broker targets. The question for a potential buyer is whether that risk premium is proportionate to the actual remaining uncertainties or whether it overshoots.

For investors wanting to examine the full statutory profit picture alongside the cash earnings metrics covered here, our full explainer on Zip Co’s FY25 earnings breakdown details the A$79.9 million net profit after tax result, the US segment’s contribution of more than US$100 million in cash earnings, and the credit loss data tracking through early FY26 that bears on the durability of the profitability inflection.

The bear case, and why the 31% decline is not obviously irrational

A 31% decline in a company posting record revenue demands more than a vague reference to “market sentiment.” Three specific concerns underpin the market’s caution.

The first is macroeconomic sensitivity. Elevated RBA cash rates increase funding costs across Zip’s loan book, and household financial stress translates directly into arrears and credit losses. Revenue growth can coexist with deteriorating credit quality, a scenario where top-line strength masks bottom-line fragility.

US credit loss performance provides one of the more concrete data points for tracking the bear case risk: April 2026 trading data shows US credit losses tracking below the management target of 1.75% of transaction volume, while US transaction volume grew above 40% year-on-year, together representing early evidence that the credit quality deterioration scenario has not materialised in the most recent operating period.

The second is regulatory uncertainty. As outlined above, the NCCP reforms remain unresolved. Until investors can quantify compliance costs and assess the final legislative form, the overhang persists.

The third is competitive structure. Afterpay (integrated into Block’s Square and Cash App ecosystem), Klarna, and bank-backed BNPL alternatives all target the same merchant and consumer relationships. Low switching costs in the sector mean that Zip’s network of 6.6 million customers and 90,600 merchants is an asset, but not necessarily a durable moat.

The ROE gap and what it reveals about profitability maturity

Return on equity (ROE), which measures how much profit a company generates relative to the capital shareholders have invested, tells a more cautious story than headline cash earnings.

Zip’s most recently reported ROE stands at 1.8%. The commonly referenced threshold for mature businesses generating adequate returns on capital is 10%. That gap is significant. It indicates the business is generating only marginal returns on the capital it employs, even as revenue and cash earnings accelerate.

The FY2025 cash earnings growth of 147% is encouraging directional evidence, but it does not yet translate into a compelling ROE. For long-term equity investors who use capital efficiency as the measure of a business’s ability to compound value over time, Zip has not yet cleared the bar. The profitability journey is real; it is also incomplete.

Weighing the evidence: what a considered position on Zip looks like in May 2026

The core investor question is one of sequencing. Zip’s business fundamentals are improving materially. Revenue is accelerating. Cash earnings are scaling. The customer and merchant networks are expanding. The question is whether the rate of improvement is fast enough to justify current prices before regulatory, competitive, or macro headwinds create a more severe reset.

Three conditions would validate the bull case over the next 12 months:

- Sustained TTV growth above 25%, confirming the platform’s compounding trajectory

- Continued cash earnings expansion toward a level that begins to improve ROE meaningfully above 1.8%

- Regulatory clarity that removes rather than extends the NCCP overhang

Three signals would validate the bear case:

- Rising arrears or credit losses indicating that revenue growth is being offset by deteriorating credit quality

- Regulatory compliance costs materialising in margin compression before the benefits of incumbency take effect

- Competitive volume loss to Afterpay, Klarna, or bank-backed alternatives visible in slowing TTV or customer growth

At 2.6x trailing revenue with 63-67% analyst upside, the risk-reward profile is more interesting than the 31% decline suggests on its own. But an ROE of 1.8% and unresolved regulatory uncertainty mean conviction requires patience over a multi-year horizon rather than a near-term trade.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

The verdict is still being written, but the numbers are no longer working against Zip

The 31% decline and the 63-67% analyst upside consensus are not contradictory. They reflect a genuine disagreement about how much execution risk remains in a business that has already completed the hardest part of its transformation, moving from a A$678 million loss to over A$1 billion in annual revenue and accelerating cash profitability.

The data points that will most directly test whether the bull or bear case is correct are approaching: H2 FY2026 total income, full-year cash earnings, and any regulatory announcements from Treasury regarding the NCCP amendments.

Investors interested in Zip Co at current prices should review the full H1 FY2026 results presentation available via the ASX and assess their own risk tolerance for a high-growth fintech still early in its profitability journey. The numbers have turned in Zip’s favour. Whether the share price follows depends on variables that remain, for now, unresolved.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.