Why AI Disruption Risk Is Mispriced Across Financial Data Stocks

1 hr ago

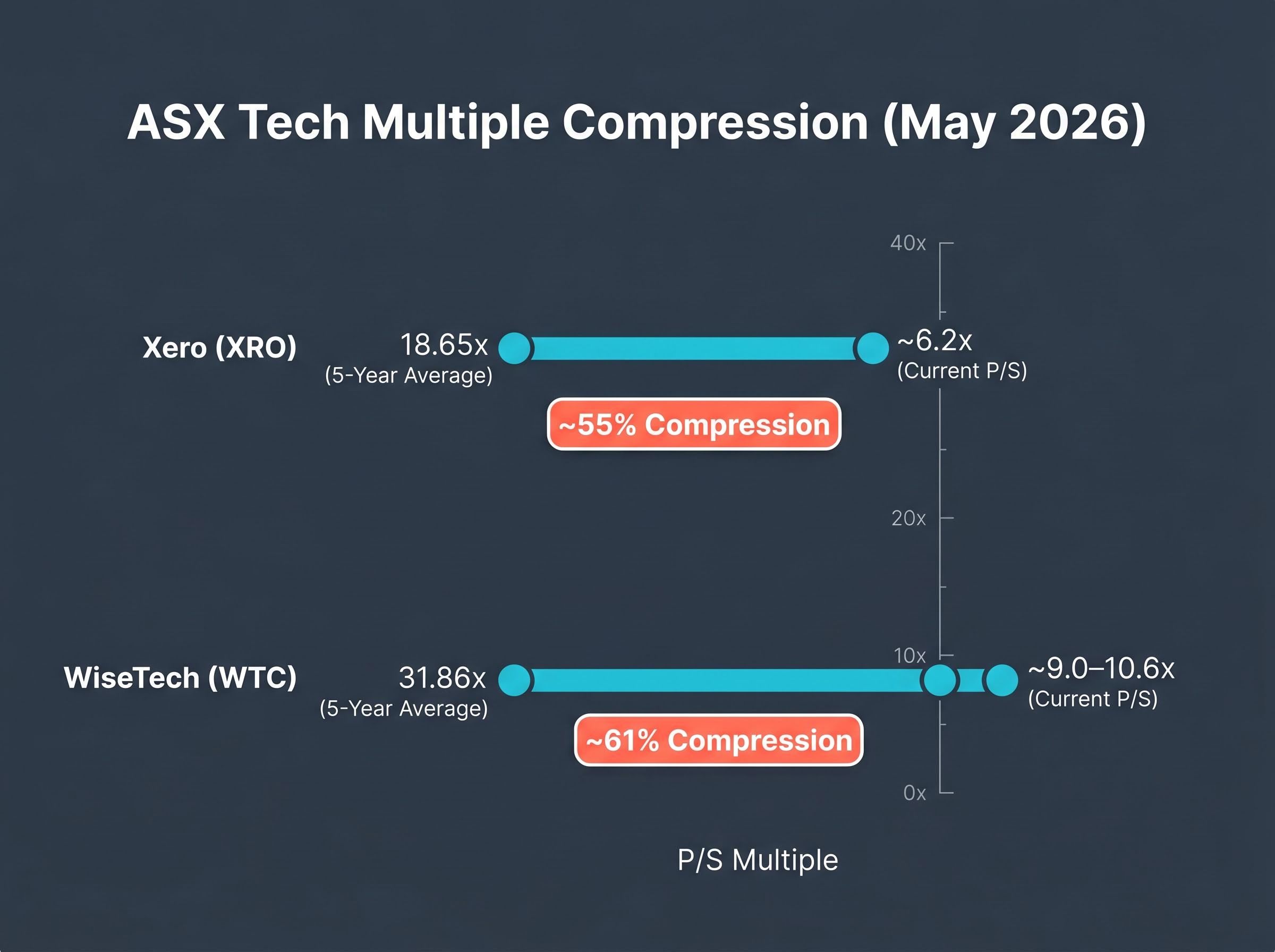

Two of the ASX technology sector’s most prominent names are now trading at price-to-sales multiples less than half their five-year historical averages. The compression took years to build and months to unwind. After the ASX Information Technology index returned 49.54% in 2024 and both Xero and WiseTech Global surged more than 50% and 60% respectively, both ASX growth stocks have since derated sharply. As of May 2026, Xero trades at a P/S of ~6.2x against a five-year average of 18.65x, and WiseTech at ~9.0–10.6x against a five-year average of 31.86x. The question before Australian investors is whether this represents a genuine re-rating opportunity or a fundamental repricing of what these businesses are worth.

What follows breaks down what price-to-sales multiples actually reveal about growth companies, traces the specific forces behind each stock’s decline, weighs the competing bull and bear cases, and offers a structured framework for deciding what comes next.

The price-to-sales ratio divides a company’s market capitalisation by its trailing twelve-month revenue, expressing the result as a multiple. A P/S of 8x means investors are paying $8 for every $1 of revenue the business generates.

For growth companies that reinvest heavily into expansion rather than maximising near-term profit, P/S is often more informative than earnings-based metrics. Earnings can be deliberately suppressed by reinvestment spending; revenue captures the underlying commercial momentum without that distortion. This makes P/S the valuation lens of choice for high-growth SaaS businesses like Xero and WiseTech.

The price-to-sales ratio is a more appropriate valuation starting point than earnings-based metrics for growth platform businesses precisely because reinvestment spending and amortisation can significantly suppress reported earnings without reducing revenue quality, a distortion that becomes especially pronounced for SaaS companies at the scale Xero and WiseTech have reached.

It also has meaningful limits.

| Company | Current P/S | Five-Year Average P/S | Compression (%) |

|---|---|---|---|

| Xero (XRO) | ~6.2x | 18.65x | ~55% |

| WiseTech (WTC) | ~9.0–10.6x | 31.86x | ~61% |

P/S compression can result from a falling share price, from revenue growing faster than market capitalisation, or from both happening simultaneously. Each tells a different story about the business underneath.

A below-average P/S ratio requires understanding whether it reflects genuine opportunity, revenue growth normalisation, or a structural re-rating of what the market is willing to pay. Without that distinction, a compressed multiple is a starting point for research, not a buy signal.

Xero gained 50.1% in calendar year 2024, entering 2025 at a stretched multiple that left almost no margin for negative surprise. The subsequent 30.4% decline from the start of 2025 through May 2026 is not one story but three overlapping ones.

The drivers break down as follows:

The underlying business, however, continued to perform. FY25 revenue reached NZ$2.1 billion, up approximately 23% year-on-year. In FY24, adjusted EBITDA grew 75% year-on-year to NZ$526.5 million, demonstrating operating leverage even as sentiment turned against the stock.

Morgan Stanley maintained an Overweight rating on Xero in April 2026 but cut its price target to A$130, citing an approximately 20% valuation reduction across ASX tech on AI disruption concerns. With the share price trading around A$78-83, that target implies meaningful upside, if the thesis holds.

The gap between the revenue trajectory and the share price trajectory is the core of the Xero debate. Investors need to determine whether the selloff is cyclical, and therefore potentially reversible, or structural, reflecting a permanent repricing of accounting software economics in an AI-disrupted environment.

WiseTech Global entered 2025 off a 60.6% gain in 2024. By late March 2026, the stock was trading only approximately 7.5% above its 52-week low, with P/S compressed from a five-year average of 31.86x to ~9.0–10.6x: a steeper derating than Xero’s by almost any measure.

The AI framing applied to WiseTech is, if anything, more direct than the case against Xero. CargoWise’s value proposition is heavily weighted toward processing-intensive compliance and documentation workflows, precisely the domain where AI automation is advancing fastest. If AI-powered logistics platforms can replicate customs compliance, freight management, and supply chain visibility at lower cost, the competitive moat narrows. That CargoWise is currently used by 24 of the 25 largest global freight forwarders and 46 of the top 50 third-party logistics providers globally speaks to the installed base at risk.

WiseTech’s AI transformation programme, announced in February 2026 alongside 76% reported revenue growth and a workforce reduction of up to 2,000 roles, signals a structural cost base reset with material margin benefits expected from FY27, a development that reframes the AI disruption narrative from external competitive threat to internal productivity catalyst for the CargoWise platform.

FY25 revenue came in at USD$778.7 million, up approximately 14% year-on-year, a notable deceleration from prior elevated growth rates that raised questions about whether historical premium multiples could be sustained.

The AI narrative, though, does not fully explain the severity of the derating. A separate, company-specific crisis does.

The sequence of events unfolded rapidly:

The ASIC investigation into WiseTech Global, covering market disclosures and share trading activity, added a formal regulatory dimension to the governance crisis that went beyond the internal board disagreements, compounding the uncertainty that institutional investors were already pricing into the stock.

The governance crisis introduced a distinct risk category that operates independently of the broader AI sentiment or tech sector rotation. For institutional investors subject to governance screening frameworks, and for retail investors assessing management stability, an ongoing founder-led structure without a permanent independent CEO creates uncertainty about strategic direction at a time when CargoWise’s global rollout demands execution clarity.

Investors who attribute WiseTech’s decline solely to sector-wide AI concerns may be underweighting a company-specific variable that has not fully resolved.

Reasonable investors disagree on both names, and the strength of each side is genuine.

| Stock | Bull Case | Bear Case |

|---|---|---|

| Xero | FY25 EBITDA of NZ$640.6 million; FY24 EBITDA growth of 75% confirms operating leverage is real, not theoretical. Recurring revenue, low churn, and global SMB accounting growth provide compounding optionality. P/S compression may overshoot fair value. | AI commoditisation risk to routine accounting workflows could structurally compress ARPU and pricing power. Entrenched North American competition from Intuit limits the largest addressable market. Morgan Stanley’s approximately 20% valuation cut reflects institutional conviction that AI risk is not fully priced. |

| WiseTech | 49% EBITDA margin in FY25 reflects a highly profitable software business even at decelerated growth. The $300 billion global SaaS market structural tailwind supports long-term adoption of CargoWise across global logistics. | Revenue growth deceleration to approximately 14% in FY25 questions whether historical premium multiples are achievable. Governance uncertainty is ongoing and independent of sector dynamics. AI-native logistics platforms represent a credible competitive threat to compliance-heavy workflows. |

The bull case rests on durable SaaS economics, recurring revenue, low churn, operating leverage, and offshore growth optionality. Both businesses retain genuinely strong underlying financials.

The bear case rests on the possibility that AI changes the competitive dynamics permanently. If it does, the five-year average P/S multiples may never be the right reference point again.

The central investor question: are the compressed multiples a cyclical sentiment opportunity, or do they reflect a structural repricing of what accounting software and logistics documentation businesses are worth in an AI-disrupted competitive environment?

A compressed P/S multiple is a signal to investigate further. The analytical work lies in determining what caused the compression and whether the cause is temporary or permanent.

Multiple compression caused ASX SaaS stocks to fall 18-82% from downtrend designations even as earnings forecasts for the majority of affected stocks remained stable or were revised upward during the same period, a pattern that illustrates why a falling share price does not necessarily signal a failing business and why distinguishing sentiment-driven derating from fundamental deterioration is the core analytical challenge.

For investors evaluating Xero and WiseTech, the following research steps provide a structured framework:

Xero’s current P/S of ~6.2x alongside FY25 revenue of NZ$2.1 billion still growing at approximately 23% year-on-year complicates a simple “value trap” reading. The business is not stalling; the market’s willingness to pay for its growth has compressed.

Xero’s financial year ends 31 March, differing from the ASX majority. FY26 results are expected around May 2027, meaning current FY25 data (published May 2025) is relatively fresh as of this writing.

WiseTech’s financial year ends 30 June. FY26 results will be published around August 2026, placing investors currently in the half-year period between full-year results. Any revision to forward revenue guidance at the interim stage will be a key indicator of whether the growth deceleration is stabilising or continuing.

The P/S discount is real and quantifiable. Xero at ~6.2x versus a five-year average of 18.65x. WiseTech at ~9.0–10.6x versus 31.86x. Coming after the ASX IT index returned 49.54% in 2024, the current derating feels particularly sharp.

The two stocks, however, present meaningfully different investment propositions. Xero’s risk profile is predominantly macro and competitive: a cyclical or structural AI threat to accounting software pricing, combined with entrenched competition from Intuit in North America. WiseTech carries an additional layer of company-specific governance risk that is independent of sector dynamics and has not fully resolved.

Both businesses retain strong underlying fundamentals: high EBITDA margins, recurring revenue, and demonstrated operating leverage. Morgan Stanley’s maintained Overweight on Xero with an A$130 price target is a marker of where at least one major institutional view currently sits.

Both stocks present compressed valuations, but the quality of the opportunity depends on the investor’s view of whether AI disruption is a cyclical sentiment risk or a permanent structural shift for each business. The P/S compression makes both worth examining carefully; it does not make the answer simple.

For investors wanting to place the Xero and WiseTech derating in a broader global context, our full explainer on the 2026 software selloff examines the record 133-percentage-point spread between the top and bottom deciles of US technology stocks, Morningstar’s moat downgrades for Adobe, Salesforce, and ServiceNow on generative AI grounds, and the evidence from Microsoft’s Azure results that established software companies can embed AI as a revenue accelerator rather than being displaced by it.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

—

A price-to-sales ratio divides a company's market capitalisation by its trailing twelve-month revenue, expressing how much investors pay per dollar of revenue. For high-growth SaaS companies like Xero and WiseTech, it is often more informative than earnings-based metrics because reinvestment spending can suppress reported profits without reducing revenue quality.

Both stocks surged more than 50% and 60% respectively in 2024, leaving stretched valuations with little margin for negative surprise. The subsequent declines reflect a combination of macro-driven sector rotation, AI disruption concerns targeting their core workflows, and in WiseTech's case an additional company-specific governance crisis involving founder Richard White and board resignations.

From October 2024, WiseTech experienced a rapid sequence of events including founder Richard White stepping down as CEO over personal misconduct allegations, four independent directors resigning in February 2025, and ASIC and police inquiries into share trading activity. White subsequently returned as Executive Chair without a permanent independent CEO being appointed, adding a distinct risk layer independent of broader sector dynamics.

A compressed P/S multiple is a starting point for research, not a conclusion. Investors should identify whether the compression stems from a falling share price, faster revenue growth, or both, then apply complementary metrics such as DCF analysis and EV/EBITDA, and for WiseTech specifically, monitor ongoing governance developments before drawing investment conclusions.

As of April 2026, Morgan Stanley maintained an Overweight rating on Xero but cut its price target to A$130, reflecting an approximately 20% valuation reduction across ASX tech driven by AI disruption concerns. With Xero trading around A$78-83 at the time, the maintained Overweight signals that at least one major institutional view sees meaningful upside if the AI disruption thesis does not fully materialise.