What the Semiconductor Selloff Reveals About the AI Trade

54 mins ago

A cumulative return of 10,423%. That is what Fidelity Contrafund produced under Will Danoff across 35 years, a stretch during which the consensus view in finance hardened into near-orthodoxy: active managers cannot beat the market at scale, for long, without luck eventually catching up.

The timing of his departure makes the record worth more than a retrospective. Index funds have crossed the threshold of representing more than half of all fund assets, and the model built around individual star managers has given way to team-based, process-driven structures at most major firms. Danoff is stepping away as one of the last credible counterexamples to the strongest version of the case against active management, and that makes his record worth examining on its own terms.

This piece dissects what Danoff actually did, why it is so difficult to replicate, and what current Contrafund holders need to think through before year-end. The goal is not a tribute. It is a practical lens for evaluating active management itself, grounded in the most complete real-world case study the industry has produced.

The empirical literature on active management is clear: as a fund’s asset base grows, its ability to outperform shrinks. Liquidity constraints, market impact costs, and the sheer difficulty of finding enough high-conviction ideas at scale all conspire against the large active manager. Contrafund, at roughly $176-$177 billion in assets (with Danoff overseeing more than $300 billion total), should have been average years ago.

The ICI 2025 Fact Book, which tracks total net assets across US-registered investment companies, places the industry at $39.2 trillion at year-end 2024, a figure that contextualises how significant Contrafund’s roughly $176-$177 billion asset base is relative to the broader landscape it must navigate.

It was not.

The empirical baseline for active vs passive investing, built from two decades of SPIVA scorecards, shows that over 90% of large-cap active managers underperform the S&P 500 over a 20-year horizon; Danoff’s record does not overturn that finding but it does sharpen the question of what separates the rare exceptions from the structural underperformers.

10,423% cumulative return from October 1990 through 2025, a figure so large that Morningstar concludes luck alone cannot plausibly account for it, given the length and breadth of the performance record.

From September 1990, when Danoff assumed management, through 2025, the fund delivered an annualised return of 14.1% against the S&P 500’s 11.28% over the same period. That gap, approximately 2.75 percentage points of annualised outperformance, sounds modest in any single year. Compounded across 35 years at this asset scale, it represents a structural anomaly that challenges the strongest form of the argument against active management.

| Metric | Danoff / Contrafund | S&P 500 | Context |

|---|---|---|---|

| Annualised return (Oct 1990-2025) | 14.1% | 11.28% | Held through 2008 crisis, pandemic, rate-hiking cycle |

| Annualised alpha | ~2.75 percentage points | Benchmark | At $300B+ scale, a documented statistical outlier |

| Cumulative return | 10,423% | Below comparable period | Spans five distinct market regimes |

The record was not unblemished. Weaker performance years offer necessary context:

Those years matter because they confirm the outperformance was not a product of a single favourable regime. It survived regime changes that ended many peers’ records entirely.

The process behind the numbers sounds almost disappointingly conventional. Earnings-growth-oriented, bottom-up fundamental analysis. Management meetings. Company reports. Competitive moat assessments. There was no proprietary algorithm, no quantitative black box.

The distinguishing feature was how consistently and how long Danoff applied that framework. His approach centred on a five-to-ten-year earnings horizon, seeking out businesses with the capacity to grow earnings per share at rates exceeding the broader market across that timeframe, and then building conviction through exhaustive fundamental research.

Core daily process elements included:

According to Morningstar, the source of the edge was consistent, rigorous fundamental analysis applied day after day, a mastery of craft built through repetition rather than any proprietary model or system. Fidelity’s analyst platform functioned as a force-multiplier, but the multiplication applied to conviction-building rather than idea generation.

What makes this relevant when evaluating any active manager is the stability. Danoff did not reinvent the approach when growth or value rotated in or out of favour. He refined within a stable conceptual framework across the dot-com boom and bust, 2008, post-GFC low rates, the pandemic, and the rate-hiking cycle. That process stability across market regimes is a more reliable signal of genuine skill than a short-term track record compiled in a favourable environment.

Low turnover was not a strategy Danoff chose. It was a consequence of how he invested.

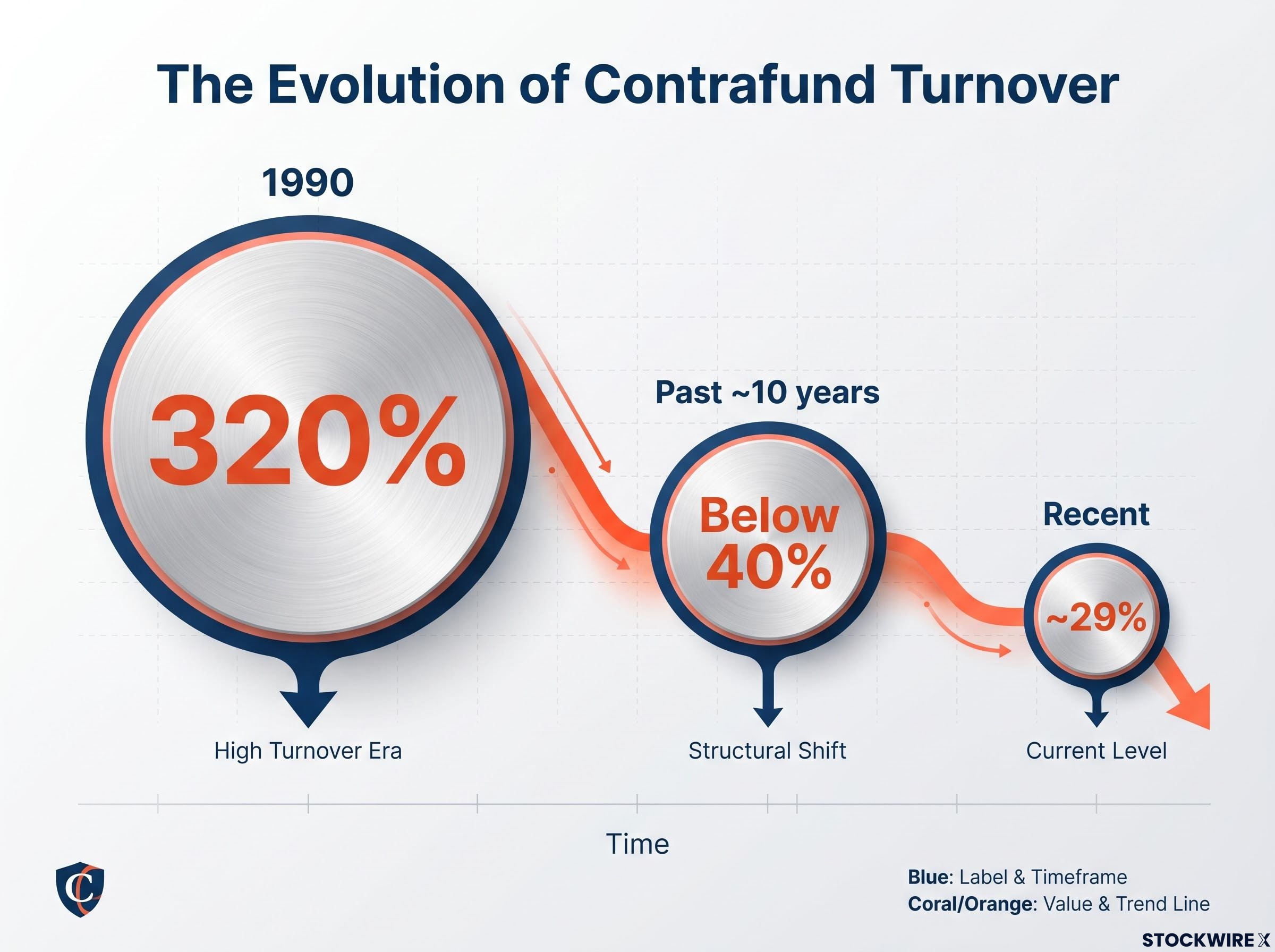

Annual portfolio turnover, the percentage of the fund’s holdings replaced in a given year, tells you whether a manager is investing or trading. In 1990, the fund’s turnover stood at 320%, meaning positions were being cycled at more than three times the full portfolio over a single year. Over the following decades that figure fell sharply, dropping below 40% across the past ten years and settling at around 29% more recently.

| Period | Approximate Turnover | Context |

|---|---|---|

| 1990 | 320% | Early tenure, smaller fund, active trading |

| Past ~10 years | Below 40% | Fund growth forces selectivity; ownership mindset matures |

| Recent | ~29% | Holding periods reflect compounding thesis, not trading thesis |

That decline reflects a shift from trading around price movements to owning businesses through their compounding cycles. At Contrafund’s scale, rapid trading is also operationally destructive; the fund’s size made patience not just philosophically sound but practically necessary.

When Meta Platforms shares dropped 64% during 2022, amid investor concern over slowing growth and rising capital expenditure, Danoff maintained his position throughout. His underlying earnings thesis remained intact and he treated the price weakness as an expected cost of holding with conviction rather than a reason to sell. The subsequent recovery flowed in full to the fund.

The behavioural costs of premature selling are measurable: research from the University of Chicago found that randomly selected sell decisions outperformed those of professional portfolio managers by up to 150 basis points annually, a finding that reframes Danoff’s decision to hold Meta through a 64% drawdown not as exceptional courage but as a systematic avoidance of a documented portfolio destruction mechanism.

Three forces push managers toward activity even when inactivity is the superior choice. Career risk punishes short-term underperformance, regardless of long-term thesis quality. Client redemption pressure forces selling into weakness. And benchmarking conventions reward managers who look active, not managers who are patient.

The willingness to hold through price weakness is not a personality trait to admire in isolation. It is a structural advantage that compounds directly into returns by allowing underlying business growth to be fully captured rather than sold prematurely. For any active fund you hold, turnover rate is a diagnostic worth checking: it tells you whether the manager is investing or trading, with direct implications for after-fee, after-tax returns.

The broader active management data remains unfavourable. Most managers underperform after fees over long horizons. Passive investing now represents more than half of total fund assets. Danoff’s record does not overturn that conclusion. It clarifies the conditions under which active management can still work, and those conditions are narrow.

Three structural factors made his success rare:

The structural barriers to active outperformance, including regulatory position caps under the Investment Company Act of 1940 that prevent funds from matching index weights when single names exceed 6-7% of benchmark weight, have grown more binding as megacap concentration has intensified, making Danoff’s ability to sustain alpha at scale an increasingly rare data point rather than a replicable model.

Morningstar labels Danoff a legendary manager and one of the strongest long-tenure performers in large-cap equity, emphasising that the length and breadth of the record make luck an implausible primary explanation.

There is a practical dimension here that often goes unasked. Morningstar analyst Robby Greengold has noted that Contrafund’s mega-cap growth concentration creates meaningful overlap with broad U.S. equity index funds, limiting incremental diversification value. For investors already holding index products, Contrafund’s value proposition was never diversification. It was alpha, and that alpha was inseparable from Danoff personally.

Asher Anolic and Jason Weiner were named co-managers in 2025 and have been operating alongside Danoff with growing decision-making authority. The transition is deliberate and staged, not abrupt. Danoff’s planned exit by year-end 2026 gives both managers a full operating period under shared responsibility before they assume full control.

Fidelity’s broader research infrastructure, risk controls, and investment philosophy around Contrafund remain in place. The institutional scaffolding that supported Danoff’s process, the analyst bench, the research platform, the risk framework, transfers with the fund.

Danoff’s accumulated pattern recognition, personal management relationships built over decades, and individual judgment cannot be institutionalised by handing over a portfolio. Anolic and Weiner may prove capable in their own right, but there is no empirical basis yet to assume they can replicate his level of long-term alpha.

For current holders, three questions deserve attention before year-end:

Morningstar and Barron’s guidance is direct: future assessments should be based on the incoming managers and Fidelity’s process, not Danoff’s historical record. Continuing to hold based on past returns rather than a view on the incoming managers is a form of performance chasing in reverse.

For investors now reassessing Contrafund or evaluating replacement options, our dedicated guide to screening funds before looking at performance walks through the people, process, and parent quality framework that Morningstar’s own analysts apply, including how team stability, fee structure, and strategy continuity predict long-term outcomes more reliably than historical return tables.

Danoff’s record is not an argument for active management as a category. It is a precise map of the conditions under which it can work.

Active management does not routinely fail because the approach is wrong. It fails because the conditions required for success almost never align for 35 years in a single manager. Those conditions are identifiable, and they function as a screening checklist when evaluating any active fund:

The annualised alpha of approximately 2.75 percentage points serves as a calibration tool for what genuine active edge looks like at scale. It is not an expectation to set for other managers. It is a benchmark for what is possible when every condition aligns, and a reminder of how rarely they do.

Morningstar’s framing puts it clearly: the qualities most important to active management outperformance, patience, discipline, and process stability, are temperamental as much as analytical. That makes them difficult to screen for, difficult to institutionalise, and difficult to sustain across decades.

The informed conclusion is neither that active management is vindicated nor that it is impossible. It is that success requires a very specific and rare alignment of conditions. Readers who understand those conditions can now identify and screen for them, rather than relying on backward-looking return tables that tell you what happened but not whether it can happen again.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results.

Will Danoff managed Fidelity Contrafund from September 1990 through 2025, delivering a cumulative return of 10,423% and an annualised return of 14.1% against the S&P 500's 11.28% over the same period, representing approximately 2.75 percentage points of annualised outperformance at a fund size exceeding $176 billion.

Asher Anolic and Jason Weiner were named co-managers in 2025 and have been operating alongside Danoff with growing decision-making authority, with Danoff's planned exit by year-end 2026 giving both managers a full operating period before they assume full control.

Turnover dropped from 320% in 1990 to around 29% in recent years, reflecting a shift from trading around price movements to owning businesses through their compounding cycles; at Contrafund's scale, rapid trading also became operationally destructive due to market impact costs.

Holders should evaluate three factors: how large Contrafund is relative to their total equity exposure, how much overlap it creates with existing index holdings (particularly large-cap U.S. growth), and whether substantial embedded capital gains make selling tax-inefficient relative to the risk of staying through the management transition.

His 35-year record shows active outperformance requires an earnings-focused bottom-up process applied consistently across market regimes, low portfolio turnover driven by genuine conviction, willingness to hold through deep drawdowns, strong institutional support, and sufficient career length for compounding to actually compound, conditions that almost never align for three decades in a single manager.