One of the most-watched equity benchmarks in the world uses a methodology that makes a $46 stock nearly irrelevant to its own index. Meanwhile, a company worth more than $2 trillion is nowhere on the list. That structural oddity sits at the centre of the loudest composition debate in U.S. index investing right now: whether Alphabet belongs in the Dow Jones Industrial Average, and whether Verizon should make room.

The stakes are not abstract. Millions of ETF holders, retirement accounts, and retail portfolios carry some exposure to DJIA-linked products. When the index’s 30 components shift, so does the implicit bet those investors are making about what “the U.S. economy” actually means. A swap here changes what you own, not just what you read about.

What follows is the analytical case being made across markets, what it would change in practice if confirmed, and how to think about it before anything is official.

The price-weighting quirk that makes Verizon almost invisible

The Dow Jones Industrial Average does not work the way most investors assume. Unlike the S&P 500, which weights companies by market capitalisation (the total value of all their shares), the DJIA is price-weighted. That means a stock trading at $200 moves the index roughly four times more than a stock at $50, regardless of how large or economically significant either company actually is.

This methodology has been in place since May 1896, when the index launched as a simple average of 12 industrial stock prices. The U.S. economy has shifted entirely away from industrial goods since then. The weighting convention has not shifted at all.

The DJIA’s status as a price-weighted benchmark rather than a market-cap-weighted one is the root cause of every composition anomaly the index produces, and institutional investors at firms like Morgan Stanley, J.P. Morgan, and Fidelity have largely set it aside as an economic proxy for exactly this reason, relying instead on the S&P 500 for macro analysis.

The result is a benchmark where share price, not economic importance, determines influence. The table below makes this visible:

| Component | Approx. share price | Approx. index weight | Market cap tier |

|---|---|---|---|

| UnitedHealth | ~$340 | ~5.0% | Mega-cap |

| Goldman Sachs | ~$290 | ~4.3% | Large-cap |

| Verizon | ~$46 | ~0.6% | Large-cap |

What this means for Verizon specifically

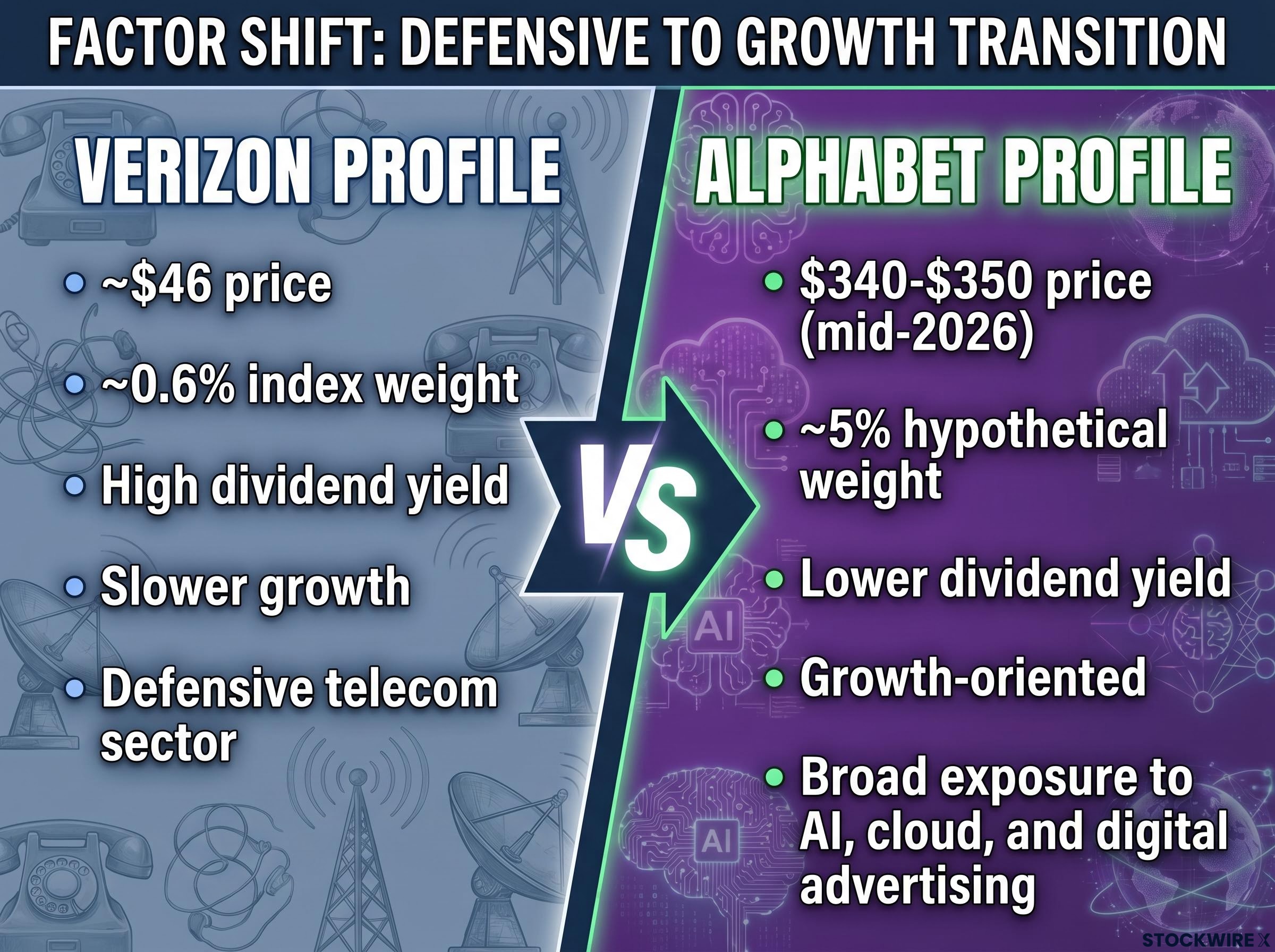

With its share price sitting near $46, Verizon commands a DJIA weighting of just over half a percentage point, meaning its daily price movements register as little more than background noise across the index’s 30 constituents. A 5% move in Verizon’s stock, whether up or down, shifts the Dow by a fraction of a point. The same 5% swing in a higher-priced component produces several times more impact on the index’s daily level.

If you hold a Dow-tracking ETF, Verizon’s performance is contributing almost nothing to what you actually own. Good quarters and bad quarters alike pass through the index nearly unnoticed.

When big ASX news breaks, our subscribers know first

How the Dow’s sector map fell out of date

Verizon’s problem is not only its price. The sector it represents no longer resembles what “Communication Services” has become. The category has shifted dramatically from legacy telephony toward a set of business models that Verizon does not operate in:

- Digital advertising (search, social, programmatic)

- Video streaming and interactive content

- Internet platforms and cloud-delivered media

- AI-powered content recommendation and distribution

Alphabet and Meta are the companies that now define Communication Services by revenue scale and market capitalisation. Verizon, with its capital-intensive wireline and wireless operations, increasingly resembles a regulated utility rather than a dynamic representative of the sector it occupies in the index.

This is not a new pattern for the committee to recognise. It has acted on sector drift before.

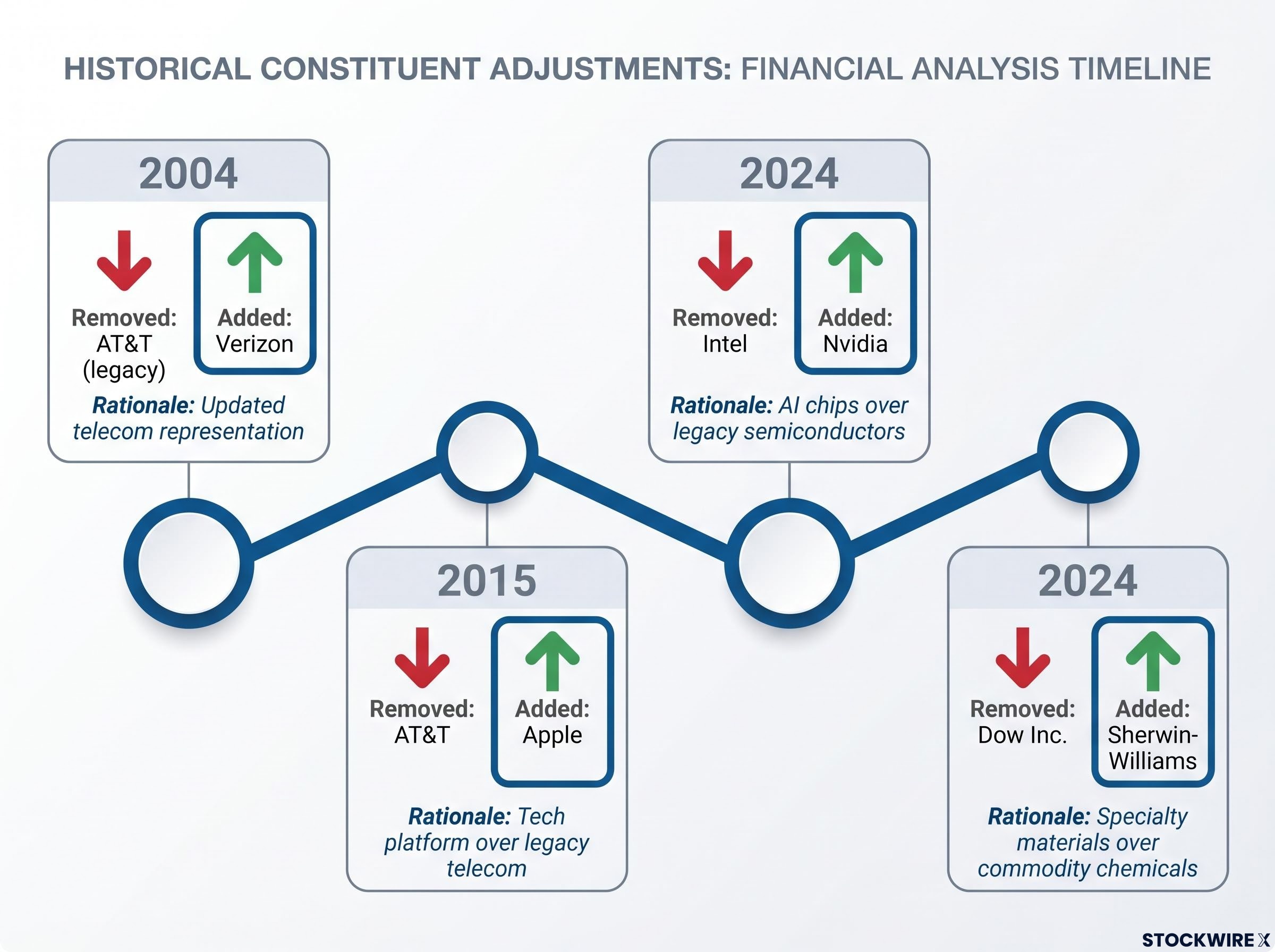

In November 2024, S&P Dow Jones Indices replaced Intel with Nvidia and Dow Inc. with Sherwin-Williams, both moves interpreted as acknowledging that AI-era semiconductors and specialty materials better represent the economy than their predecessors did.

The 2015 precedent is even more directly relevant: Apple replaced AT&T, the same directional logic of swapping a legacy telecom position for a technology platform. The sector drift argument means Verizon’s vulnerability is structural. Even a recovery in its stock price would not resolve the representational mismatch, which changes how you should assess the probability and permanence of any removal.

Washington Post reporting on the November 2024 DJIA changes confirmed that S&P Dow Jones Indices framed the Intel-to-Nvidia and Dow Inc.-to-Sherwin-Williams swaps as moves to better represent modern industry composition, the same committee logic that the Verizon-to-Alphabet case rests on.

Why Alphabet fits where Verizon does not

The price mechanics come first. Alphabet trades in the $340-$350 range as of mid-2026, which would immediately give it several times Verizon’s index weight. From day one of any inclusion, Alphabet would be a top-tier influence on the Dow’s daily movement, not a rounding error.

The price mechanics of Alphabet’s hypothetical inclusion

At $340-$350, Alphabet would rank among the higher-weighted components in the index, sitting alongside names like UnitedHealth and Goldman Sachs in terms of price-driven influence. That is a direct upgrade from a component contributing roughly 0.6% to one contributing in the range of 5%. The committee has managed high-priced inclusions before, and nothing in Alphabet’s price level would be unprecedented.

But the case extends well beyond mechanics. Alphabet’s operations span the dominant growth themes of the current U.S. market, each representing an index exposure the Dow currently lacks:

Alphabet’s cloud and AI revenue profile has changed substantially in the past 12 months: Google Cloud posted 63% year-over-year growth in Q1 2026 with operating margins expanding to 32.9%, and Waymo surpassed 100,000 paid rides per week across ten U.S. cities, a set of business lines that would give the Dow exposure it currently has no path to through any of its existing 30 components.

- Google Search and YouTube: digital advertising at global scale

- Google Cloud: cloud infrastructure, competing with AWS and Microsoft Azure

- AI platforms and models: embedded across products and infrastructure

- Waymo: autonomous mobility, with commercial robotaxi deployments already operational

- Hardware and devices: consumer products and custom chips

What this means for you is direct: adding Alphabet would make the Dow a more accurate expression of where U.S. earnings growth and technological leadership are actually concentrated today. That is the implicit bet you are making when you hold a Dow-tracking product, and the current composition is not delivering it.

What the DJIA’s history of changes actually tells us

The Dow’s component history reads like a running editorial about what “the U.S. economy” looks like at any given moment. Changes are infrequent and deliberate. Across the index’s history, the committee has made approximately 59 component changes (a figure cited in analyst commentary, though not independently verified), reflecting a preference for considered moves rather than reactive ones.

The most instructive recent precedents follow a clear directional pattern:

| Year | Removed | Added | Rationale |

|---|---|---|---|

| 2024 | Intel | Nvidia | AI chips over legacy semiconductors |

| 2024 | Dow Inc. | Sherwin-Williams | Specialty materials over commodity chemicals |

| 2015 | AT&T | Apple | Tech platform over legacy telecom |

| 2004 | AT&T (legacy) | Verizon | Updated telecom representation |

The historical irony is worth noting: Verizon itself joined the Dow in April 2004 by replacing the legacy AT&T. Now it faces the prospect of being replaced for the same category of reason, a sector that moved on while the component stood still.

The pattern tells you this is not a question of whether this category of change happens. It is a question of when. The structural case for Verizon’s removal has been building for several years, which is relevant to how long-term DJIA investors should frame their expectations. The committee has no fixed schedule, and timing remains genuinely unpredictable.

What actually changes in a DJIA-linked portfolio if this happens

If S&P Dow Jones Indices confirms an Alphabet-for-Verizon swap, the mechanical consequences are specific. ETFs and index funds tracking the Dow would be required to sell Verizon and buy Alphabet on or before the effective date. That creates directed price pressure: buying flows into Alphabet and selling flows out of Verizon around the transition window.

Index concentration dynamics in cap-weighted products like the S&P 500 already give Alphabet roughly 4% exposure in broad market funds, which means investors holding both S&P 500 and Dow-tracking products would see their Alphabet weighting increase materially if the inclusion is confirmed, compounding a position many passive portfolios already carry without realising it.

The factor shift is equally concrete. Dow-linked portfolios would move away from high-dividend, defensive-income characteristics and toward growth and momentum exposure:

- Verizon profile: high dividend yield, slower growth, defensive telecom sector

- Alphabet profile: growth-oriented, lower dividend yield, broad exposure to AI, cloud, and digital advertising

For a reader who holds a Dow-tracking product, this answers the question that directly affects your position: you would own less defensive-income telecom exposure and more growth-oriented technology exposure. Whether that is a change you want depends on your portfolio’s existing factor balance.

No official announcement has been made. As of 23 June 2026, S&P Dow Jones Indices has not confirmed any component change. The committee could delay, select a different company, remove a different component, or leave the index unchanged. Any positioning ahead of an announcement carries event risk.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Reading the signals before the committee decides

The two-factor case is clear. The price-weighting problem makes Verizon nearly invisible in its own index. The sector representation problem means the category it occupies has moved on without it. Together, these make Verizon one of the most structurally exposed components in the current Dow.

What to watch for as events develop:

- An official press release or announcement from S&P Dow Jones Indices naming new components and an implementation date

- Any public committee statement or commentary that signals a review is underway

- Material changes in Alphabet’s share price that would alter its hypothetical index weight and the committee’s mechanical calculus

- Alternative outcomes: the committee could select a different Communication Services or technology name, or remove a different component entirely

Alphabet’s AI talent losses on 23 June 2026, including the departure of transformer paper co-author Noam Shazeer to OpenAI, sent the stock down roughly 5% in a single session and serve as a reminder that any committee timing assessment must account for share price volatility that could shift Alphabet’s hypothetical index weight in the weeks between speculation and announcement.

Morningstar’s coverage of the official DJIA announcement explicitly cites S&P Dow Jones Indices’ rationale that Verizon’s minimal index impact stems directly from its lower share price in a price-weighted system, confirming that the structural vulnerability outlined here translated into a formal committee decision.

One final point of context. For investors whose primary exposure runs through S&P 500 or Nasdaq-100 products, Alphabet is already a significant holding. That affects how urgently you need to act on a potential DJIA change. The analytical case here is strong, but the timing is genuinely uncertain, and the committee operates on its own schedule. Knowing exactly what to watch for, and understanding the structural logic behind the speculation, puts you in a more useful position than either dismissing the thesis or acting prematurely on it.

These statements are speculative and subject to change based on market developments and index committee decisions. Past index composition changes do not guarantee future adjustments.