How AI Capex Is Set to Compress the S&P 500 ROE Record

27 mins ago

Some of the worst-performing sectors on the ASX in mid-2026 may contain some of the most compelling value investing opportunities available to Australian investors right now. The disconnect between sentiment and fundamentals has rarely been this wide in healthcare and consumer-facing stocks, and for investors willing to separate price from quality, the current earnings season has created conditions worth examining closely. CSL Limited, the country’s largest healthcare company, serves as the most visible example: a franchise whose structural advantages have not materially changed, yet whose share price has absorbed months of earnings-season volatility. What follows is an analysis of why these sectors have fallen, how to distinguish a genuine entry point from a value trap, and a practical framework for evaluating whether any individual stock’s selloff has gone far enough to justify action.

Quality businesses with falling prices create a specific kind of dissonance. Healthcare and consumer-facing stocks have been among the weakest ASX performers in the mid-2026 earnings season, and the instinct for many investors is to treat the price decline as the signal. It is not.

The causes differ by sector. Healthcare underperformance has been driven primarily by earnings disappointments and valuation de-rating, as companies like CSL reported mixed results that triggered multiple compression. Consumer underperformance reflects a different set of forces: macro headwinds that are squeezing earnings from the outside rather than exposing internal weakness.

The three simultaneous pressures on consumer stocks are distinct in mechanism:

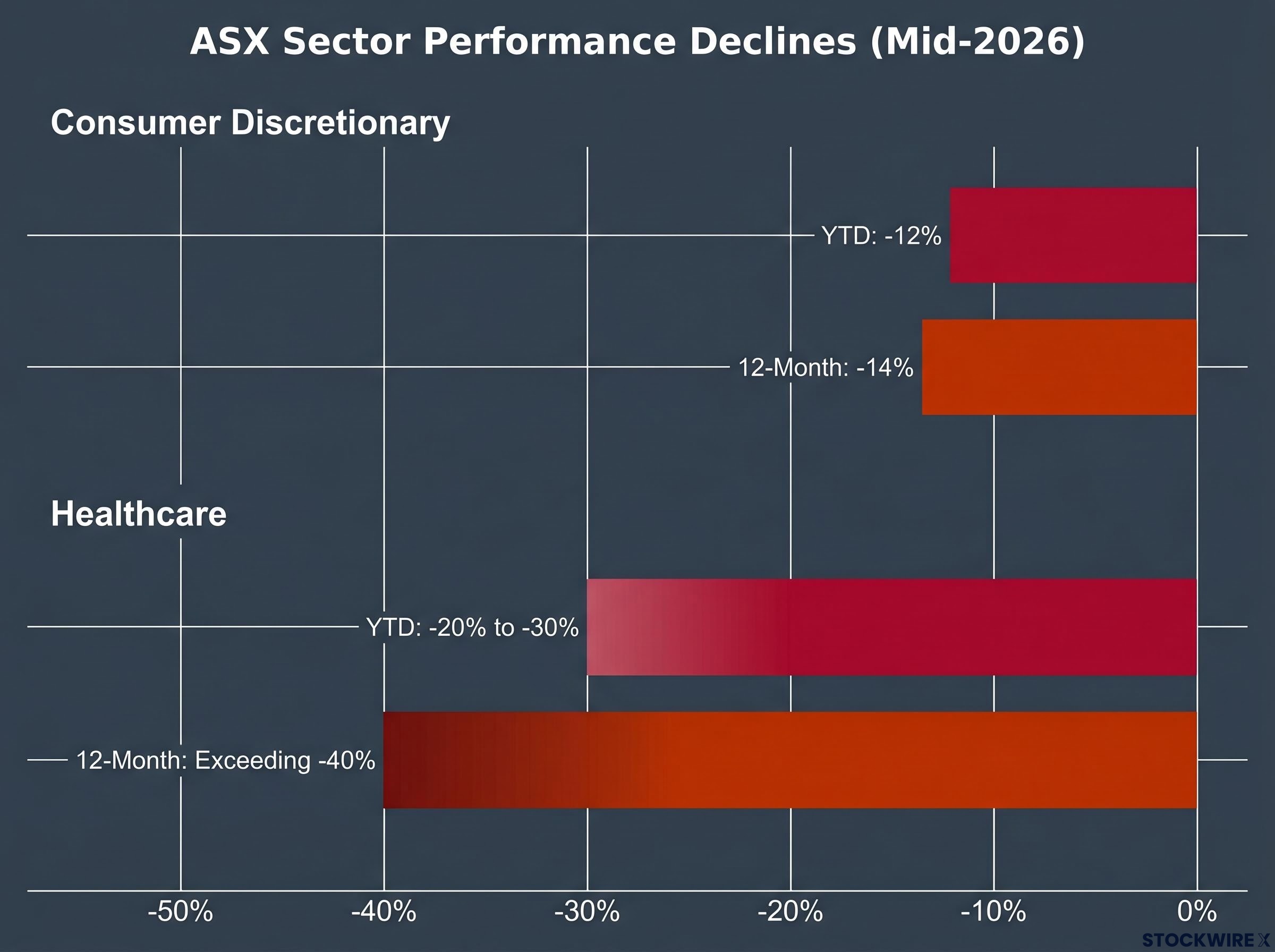

Available aggregate data paints the scale of the damage. The ASX Consumer Discretionary sector has returned approximately -12% year-to-date and approximately -14% over twelve months. ASX healthcare has fared worse, with year-to-date declines in the range of -20% to -30% in aggregate metrics and twelve-month declines exceeding -40% in some measures. These figures are sourced from available industry aggregates and should be treated as indicative rather than definitive.

Sector underperformance driven by sentiment and cyclical pressure is qualitatively different from sector underperformance driven by structural deterioration. The investment case only exists in the former.

What matters is that neither sector’s decline is being characterised in available commentary as permanent franchise erosion. That distinction is the foundation of the value argument.

The macro case for value investing in Australia has strengthened as trimmed-mean inflation held at 3.8% in the March 2026 quarter; research from Capital Group, Schroders, and Goldman Sachs Asset Management consistently shows value stocks outperforming growth when inflation runs above trend and rates remain elevated.

The most common error investors make in a selloff is treating a falling price as evidence that a business has lost quality. The reverse error is equally costly: assuming a high-quality business is always an attractive investment regardless of the price paid. Both errors stem from conflating two judgements that should be made separately.

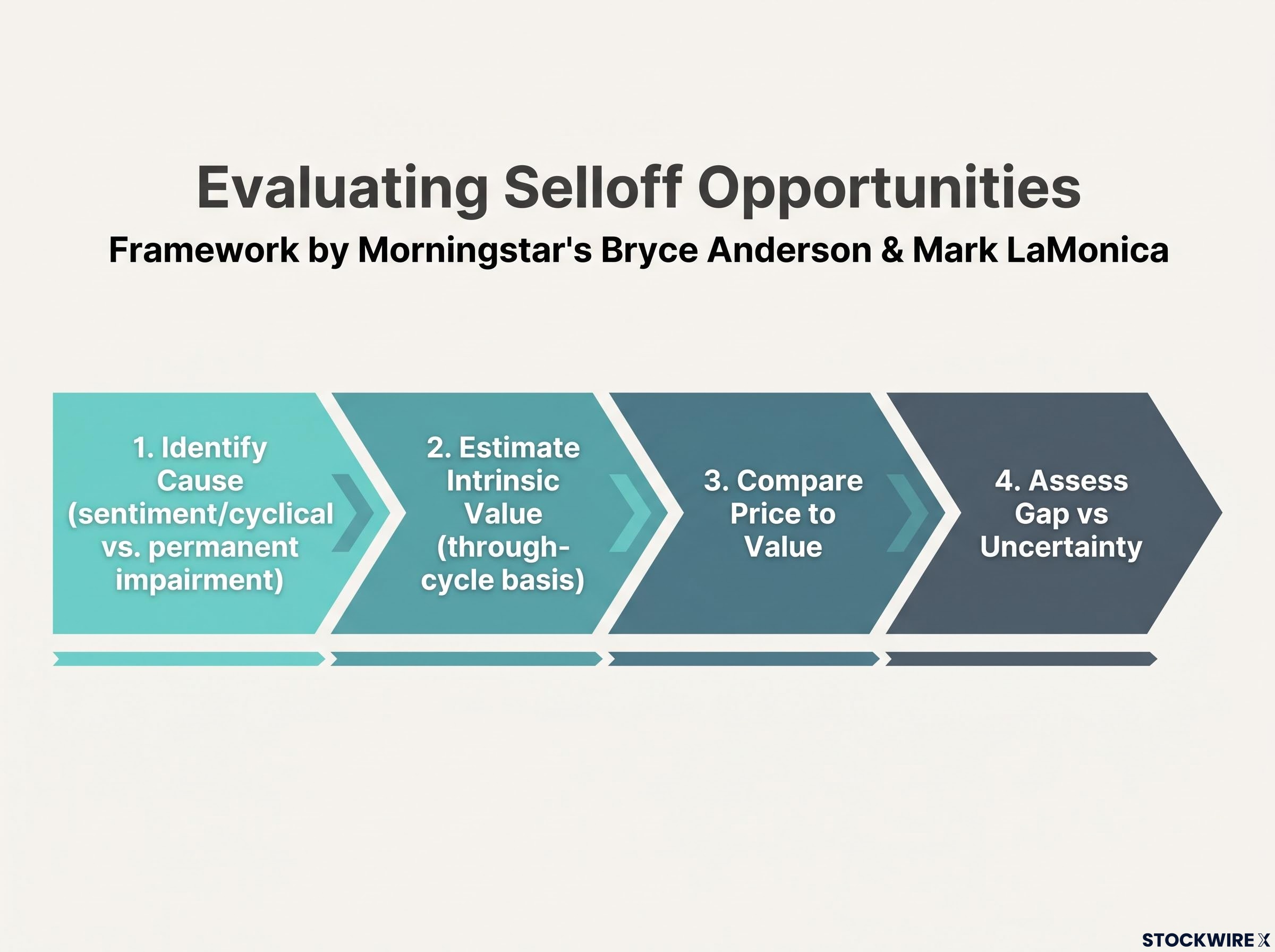

Bryce Anderson, Senior Portfolio Manager at Morningstar Investment Management, and Mark LaMonica CFA, Director of Personal Finance at Morningstar Australia, have both articulated this principle in the context of the mid-2026 ASX reporting season. The framework they describe is straightforward in concept but demanding in execution.

Intrinsic value is the present value of a business’s future cash flows, the amount all of its future earnings are worth in today’s dollars after accounting for the time value of money and the uncertainty of those earnings. Market price cycles around this estimate rather than tracking it precisely. Sentiment shifts, interest rate movements, and earnings-season volatility all create temporary dislocations between price and fundamental worth. Those dislocations are the mechanism through which opportunities arise.

Intrinsic value estimation using discounted cash flow analysis is structurally sensitive to the terminal value assumption, which typically drives 60-80% of any DCF model’s implied worth, making it the input most deserving of stress-testing when macro uncertainty is elevated.

Margin of safety is the buffer between the price paid and the estimated intrinsic value. It exists to absorb forecast error. When earnings visibility is lower or macro uncertainty is higher, a larger margin of safety is warranted because the range of plausible outcomes is wider.

The valuation process follows three steps:

CSL Limited reported FY25 results in August 2025 that showed a business executing on margin recovery. Revenue reached US$15.6 billion (up 6%), net profit after tax came in at US$3.0 billion (up 17%), and underlying NPATA hit US$3.3 billion (up 14%), driven by improvements in plasma collection efficiency.

The H1 FY26 update in February 2026 told a different story on the surface. Revenue fell to US$8.3 billion (down 4% at constant currency), and NPATA declined to US$1.9 billion (down 7%), with the decline attributed to one-off restructuring charges and impairments. Management maintained full-year FY26 guidance despite the half-year headwinds: group revenue growth of approximately 2-5% at constant currency and NPATA growth of 4-10% excluding one-off items.

ASIC’s continuous disclosure obligations require ASX-listed companies to lodge financial reports and immediately disclose material information that could affect their share price, which is the regulatory mechanism that makes earnings-season guidance updates from companies like CSL legally binding statements rather than aspirational commentary.

| Metric | FY25 Result | H1 FY26 Result | FY26 Full-Year Guidance |

|---|---|---|---|

| Revenue | US$15.6B (up 6%) | US$8.3B (down 4% CC) | Growth approx. 2-5% CC |

| NPATA (underlying) | US$3.3B (up 14%) | US$1.9B (down 7%) | Growth 4-10% ex one-offs |

| Growth drivers | Plasma collection efficiency | Restructuring charges, impairments | Plasma and cost dynamics |

The structural position has not materially changed. CSL retains global plasma and vaccine scale, high returns on capital, and a growth pipeline spanning its Behring, Seqirus, and Vifor divisions. The valuation de-rating of FY23-FY24 was driven by slower-than-expected margin recovery, FX headwinds, Vifor integration costs, and a rate-driven rotation away from defensive growth names. As of late May 2026, CSL’s trailing P/E sits in the range of approximately 24x.

Business quality is broadly regarded as intact. Investment attractiveness is the separate question, and it depends entirely on whether the current price embeds enough pessimism to offer adequate margin of safety.

The data tells the story: a franchise delivering mid-single-digit revenue growth and double-digit earnings growth on a normalised basis, trading at a multiple compressed by temporary headwinds rather than structural deterioration.

CSL’s revenue and earnings trajectory over the past five years reveals a structural tension that the headline results obscure: revenue compounded at 12.8% annually while net profit grew at only 3.6%, with plasma cost inflation, Vifor integration drag, and amortisation charges absorbing growth faster than the top line could expand.

Tariffs have raised landed costs for importers, forcing a binary choice between increasing shelf prices (which risks volume declines) or absorbing the cost increase (which compresses margins). Persistent inflation across freight, energy, and wages has amplified the squeeze. Cost-of-living pressure, driven by mortgage burdens, rent, and utility costs, has disproportionately reduced discretionary spending in mid-market retail, travel, leisure, and auto-related consumption.

Each channel compresses earnings through a different mechanism, but the combined effect has been a broad-based selloff that has not discriminated cleanly between businesses experiencing temporary volume softness and those facing permanent franchise erosion. The investment case only exists in the former category.

Three subsectors stand out as areas where the gap between cyclically depressed earnings and long-term franchise value may be widest:

The distinction in each case is the same: intact franchise or pricing power plus cyclically (not structurally) depressed earnings.

The analysis above is only useful if it translates into a repeatable decision-making process. The framework recommended by Anderson and LaMonica at Morningstar applies to any stock, not only healthcare or consumer names.

Four steps:

A falling price is not evidence of value, nor is it evidence of a problem. The work is in determining which it is.

For CSL, the question is not whether the business is high quality. It is whether the current price embeds enough pessimism about execution risk, FX headwinds, and Vifor integration to offer adequate margin of safety against the maintained FY26 guidance. For consumer names, the question is whether through-cycle cash flows justify a price materially higher than where the market has settled during a period of cyclically compressed margins.

The two failure modes sit at opposite ends. Buying a declining stock because it appears cheap without assessing quality is the value trap. Avoiding a declining quality stock because the price keeps falling, anchored to a previous high, is the missed opportunity.

Value investing reframes risk as the probability of permanent capital loss rather than price volatility, a definitional shift with significant practical consequences: a falling share price that reflects market panic rather than business deterioration actually widens the margin of safety and reduces value investing risk, the opposite conclusion from what standard volatility-based risk models produce.

Valuation insight without behavioural discipline produces no return. The market reprices quality businesses toward intrinsic value over time, but the timeline is uncertain, and investors who act on a valuation framework must be willing to hold a position through continued volatility after purchase.

The current healthcare and consumer selloffs may deepen before they reverse. That possibility is precisely what creates the margin-of-safety requirement. CSL’s maintained FY26 guidance suggests management believes the franchise’s earning capacity remains intact despite the H1 headwinds. The broader consumer sector contains names where cyclical earnings pain is being treated by the market as a permanent condition.

As Anderson and LaMonica have framed it, market prices cycle around intrinsic value estimates rather than tracking them in real time. The advantage available to Australian investors is not superior information about plasma margins or a retailer’s tariff exposure. It is the discipline to separate business quality from current price and act on that separation when the market is most uncomfortable.

ASX healthcare and consumer sector weakness in mid-2026 reflects sentiment and cyclical pressure, not a verdict on franchise quality in the names with genuine competitive advantages. The framework is consistent regardless of sector: estimate intrinsic value, compare it to current price, and require a margin of safety wide enough to absorb forecast error.

The opportunity window created by a selloff is time-limited. Markets do eventually reprice quality businesses upward as earnings stabilise and sentiment normalises. The four-step evaluation process outlined above applies to any healthcare or consumer stock currently on a watchlist. The more productive exercise for investors is to revisit their intrinsic value estimates rather than react to price movements alone.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

A margin of safety is the buffer between the price you pay for a stock and your estimate of its intrinsic value. It exists to absorb forecast error, and a larger margin is warranted when earnings visibility is lower or macro uncertainty is higher.

A value trap occurs when a stock is cheap because the business has suffered permanent franchise erosion, while a genuine opportunity exists when the price has fallen due to temporary sentiment or cyclical pressure on an otherwise intact business. The key is assessing whether the company's long-term cash-generating capacity has been structurally impaired or is only temporarily depressed.

CSL reported FY25 revenue of US$15.6 billion (up 6%) and NPATA of US$3.3 billion (up 14%), but its H1 FY26 update showed revenue down 4% at constant currency and NPATA down 7%, attributed to one-off restructuring charges. Management maintained full-year FY26 guidance for revenue growth of approximately 2-5% at constant currency and NPATA growth of 4-10% excluding one-off items.

Intrinsic value is the present value of a business's future cash flows, representing what all future earnings are worth in today's dollars after accounting for time value and earnings uncertainty. Investors typically estimate it using discounted cash flow analysis or normalised earnings multiples applied to mid-cycle profits rather than currently depressed margins.

The ASX Consumer Discretionary sector has returned approximately -12% year-to-date, driven by three simultaneous pressures: tariffs raising landed costs for importers, persistent inflation compressing margins through freight, energy, and wages, and cost-of-living stress reducing discretionary household spending across mid-market retail, travel, and leisure.