What History Really Shows About Rate Hikes and Stock Returns

28 mins ago

The S&P/ASX 200 rose 1.35% on 15 June 2026, the moment markets priced in a single announcement: the United States and Iran had reached a framework agreement to end their standoff, reopen the Strait of Hormuz, and begin formal nuclear talks.

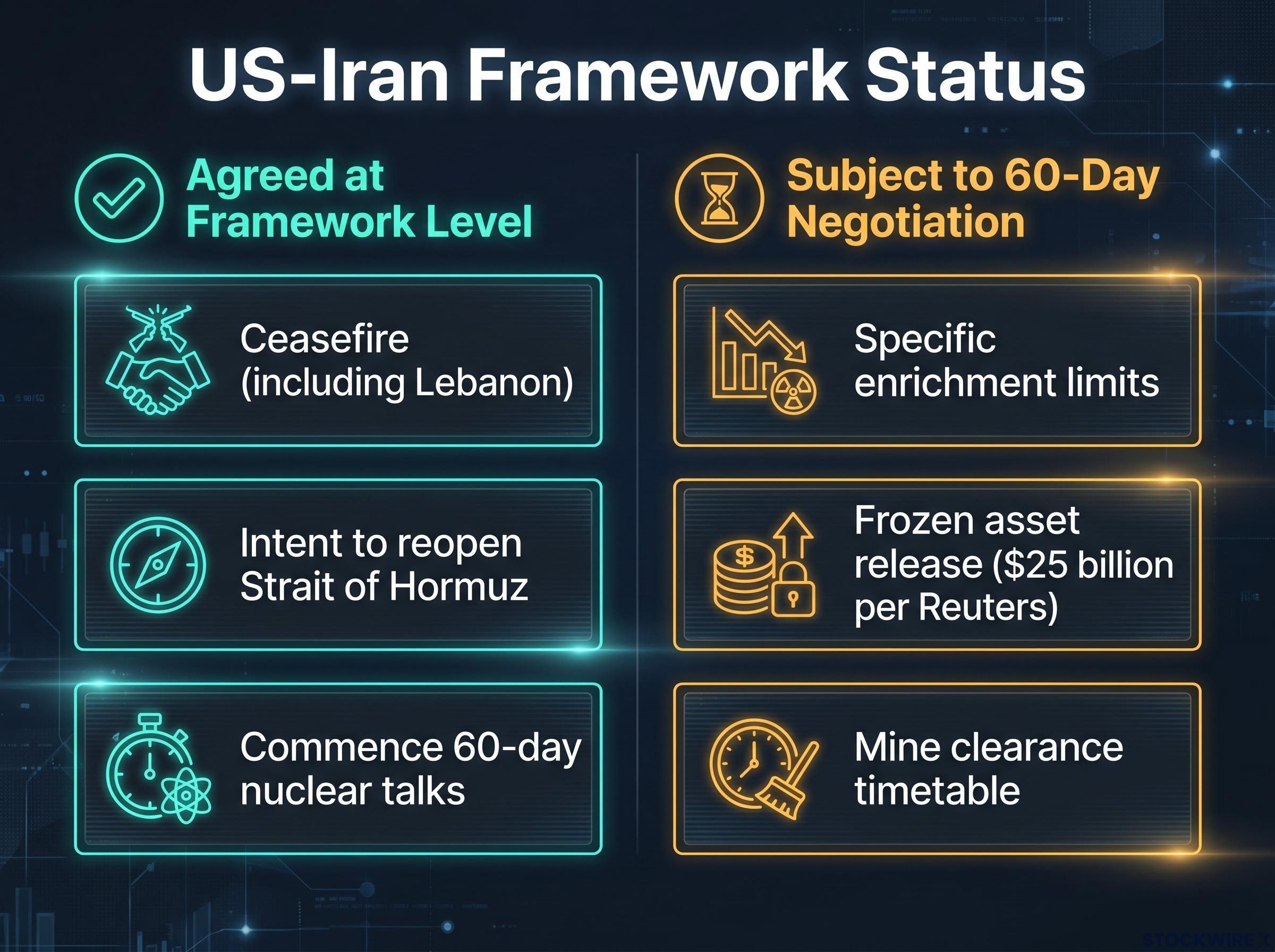

The deal, announced by President Trump via Truth Social and attributed to Reuters draft reporting, arrives after weeks of false starts and represents the most significant de-escalation in the Gulf in years. It is, however, an interim peace framework, not a fully ratified treaty. Specific enrichment limits, asset release timelines, and the operational timetable for mine clearance remain subject to a 60-day negotiation window.

What follows explains what the US Iran peace deal actually commits to, what remains unresolved, why a single announcement can move equity markets thousands of kilometres away, and what investors should watch in the weeks ahead.

President Trump’s Truth Social post described the agreement as finalised and specific, authorising the reopening of the Strait of Hormuz and the removal of the US naval blockade. A formal signing ceremony was indicated for the following Friday.

Independent reporting tells a more conditional story. Axios characterised the same framework as extending the ceasefire for 60 days and opening a negotiation window for nuclear and technical talks, not confirming those elements as completed, binding commitments. The gap between these two characterisations is where investor risk lives.

Iran’s Supreme National Security Council stated that “military operations on all fronts including Lebanon will cease immediately and permanently starting tonight,” the clearest binding language in the public record. Beyond the ceasefire extension, the framework commits in principle to facilitating the reopening of the Strait of Hormuz, ending the US naval blockade, commencing 60-day nuclear and sanctions talks, and addressing frozen asset releases contingent on compliance.

Specific uranium enrichment caps, verification and monitoring mechanisms, the exact amount and timing of frozen asset releases, and the mine clearance timetable for Hormuz normalisation all remain subjects for the 60-day negotiation window, not agreed terms.

| Element | Status |

|---|---|

| Ceasefire extension (all fronts including Lebanon) | Agreed at framework level |

| Intent to reopen Strait of Hormuz | Agreed at framework level |

| Commencement of 60-day nuclear talks | Agreed at framework level |

| Specific enrichment limits and verification | Still to be negotiated |

| Frozen asset release amounts and timing | Still to be negotiated |

| Mine clearance and Hormuz operational timetable | Still to be negotiated |

Investors pricing this deal as a completed agreement are making a fundamentally different risk assumption than those pricing it as a framework subject to breakdown.

Before the conflict, approximately 20% of the world’s oil and liquefied natural gas trade passed through the Strait of Hormuz. That single figure explains why the framework’s most market-relevant commitment, reopening the waterway, carries so much weight.

The Hormuz oil risk premium embedded in Brent crude did not form overnight; commercial war-risk insurers effectively closed the strait to standard tanker traffic even during periods when physical passage was technically possible, creating a price floor that persists independently of daily military developments.

The framework commits to facilitating that reopening and ending the US naval blockade. It does not guarantee an operational timeline. Axios reported that a complete reopening “may not occur right away” due to three specific prerequisites:

Axios reported that a complete reopening of the Strait of Hormuz “may not occur right away” due to mine clearance requirements, infrastructure repair, and security assurances.

No confirmed operational timeline for mine clearance or full transit normalisation has appeared in public reporting as of 15 June 2026. The distinction matters: today’s market moves reflect expectation pricing, not confirmed supply normalisation. Oil price movements and their downstream effects on inflation are the central transmission channel from this deal to equity markets, and that channel remains procedurally incomplete.

The nuclear and sanctions elements of the framework have been reported in two materially different ways, and neither source has withdrawn its characterisation.

Reuters draft deal reporting, cited in the original announcement coverage, described Iran as having committed to halting uranium enrichment, ceasing expansion of nuclear infrastructure, and diluting its existing stockpile within Iranian territory. Under the same reporting, the US agreed to release approximately $25 billion in frozen Iranian assets.

According to Reuters draft deal reporting, the US agreed to release approximately $25 billion in previously frozen Iranian assets as part of the framework terms.

Axios described these same matters as subjects for prospective negotiation over the 60-day window, not agreed terms. No specific asset figure appeared in Axios’s coverage of the underlying documentation.

The nuclear items explicitly on the 60-day negotiating agenda include:

A multilateral dimension adds further complexity. CNBC reported on 15 June 2026 that several European nations were weighing removal of their own sanctions on Iran in exchange for nuclear constraints, a potential second layer of supply-side relief that markets may not yet be fully pricing.

The S&P/ASX 200 rose 1.35% on 15 June 2026, according to Rask Media reporting by Jaz Harrison. An event in the Persian Gulf moved an Australian equity index because two distinct transmission channels connect geopolitical de-escalation to equity valuations, regardless of geography.

The Asian equity reaction to the same June 14-15 announcement showed significant dispersion across regional markets, with South Korea’s KOSPI rising approximately 4.6-5.6% due to near-total crude import dependence, while China’s CSI 300 lagged at roughly 1.2-1.3%, reflecting more diversified supply and state reserve buffers.

The mechanism operates in four sequential steps:

Geopolitical de-escalation compresses volatility premiums across asset classes. Risk appetite improves. Capital rotates from defensive assets (government bonds, gold, cash) into equities and credit. The ASX 200, as a broad equity index with meaningful exposure to energy-sensitive sectors, captures that rotation directly.

Weeks of false starts on Gulf negotiations had primed markets for sensitivity to any credible announcement, amplifying the single-session response. Understanding these two channels equips investors to apply the same framework to future geopolitical events, not just this one.

Expectation pricing ahead of the announcement had already begun compressing the Brent risk premium, with crude falling 3.3% to $91.15 on 9 June 2026 after White House signals of an imminent deal, meaning the June 15 equity rally was partly a continuation of a move that started six sessions earlier.

Markets are currently pricing expected outcomes, not confirmed facts, a distinction that carries direct implications for headline risk over the next 60 days.

The framework’s interim nature means the rally carries specific reversal conditions. Because the agreement opens a 60-day negotiation window rather than confirming binding terms, every session within that window is exposed to headline risk that a finalised treaty would not produce.

Investors should monitor the following near-term risk factors:

Formally ratified agreements with confirmed compliance tend to produce more durable market responses than announcement-phase frameworks. Retail investors who entered on the announcement-phase rally without understanding the framework’s conditional nature are carrying more headline risk than the initial price move implies.

For investors wanting to understand how to position around unverified peace frameworks more generally, our deep-dive into ceasefire announcement risk for investors covers BCA Research’s framework for distinguishing preliminary negotiations from confirmed resolutions, including the specific portfolio positioning signals the firm recommends waiting for before repositioning capital.

The current market move represents a bet on a specific sequence of events. Each milestone either confirms or undermines that wager:

The European sanctions dimension represents potential upside that sits outside the bilateral framework:

The European sanctions relief reporting from Reuters confirmed that the UK, France, Germany, and Italy were prepared to lift their own sanctions on Iran contingent on verifiable steps on its nuclear programme, a multilateral development that sits outside the bilateral US-Iran framework and could accelerate Iranian oil re-entry into global supply beyond what the bilateral deal alone delivers.

The 60-day window creates a defined monitoring horizon. The deal creates a structured period in which the market’s geopolitical risk premium on energy could either be confirmed and sustained, or partially reversed. A deal that is signed, operationally implemented, and backed by multilateral sanctions relief would represent a materially different macro input than today’s interim framework.

What is confirmed: a ceasefire across multiple fronts including Lebanon, a commitment to reopen the Strait of Hormuz, and a 60-day window for nuclear and sanctions negotiations. What requires that window to finalise: specific enrichment limits, verification mechanisms, asset release amounts, and the mine clearance timetable that determines when supply actually normalises.

The transmission channels that moved the ASX 200 by 1.35% in a single session (energy costs to inflation to rate expectations to equity valuations, and geopolitical risk appetite compression) are analytically sound. They are also contingent on the framework progressing through its next phases.

Three signals will determine whether the 15 June rally was the beginning of a sustained re-rating or an anticipatory move that gets partially corrected: the signing ceremony, mine clearance progress, and nuclear negotiation outcomes. Those are the milestones that convert expectation into fact.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. These statements regarding the framework’s potential market impact are speculative and subject to change based on geopolitical developments and negotiation outcomes.

The US Iran peace deal framework is an interim agreement that commits to a ceasefire across multiple fronts including Lebanon, an intent to reopen the Strait of Hormuz, and a 60-day window for nuclear and sanctions negotiations. It is not a fully ratified treaty; specific enrichment limits, asset release timelines, and mine clearance schedules remain to be negotiated.

The S&P/ASX 200 rose 1.35% on 15 June 2026 because a credible Hormuz reopening compresses the oil and LNG risk premium, which lowers energy costs, reduces inflation expectations, shifts rate cut probabilities, and mechanically raises equity valuations. A secondary channel of geopolitical risk appetite compression also rotated capital from defensive assets into equities.

A full reopening of the Strait of Hormuz requires mine clearance operations throughout the waterway, infrastructure repair at affected port and terminal facilities, and security assurances from both parties. No confirmed operational timeline for any of these three prerequisites had been established as of 15 June 2026.

Investors should watch for stalled or collapsed nuclear talks, a delayed or cancelled formal signing ceremony, operational incidents during mine clearance, and compliance failures on the Lebanon ceasefire front. Any of these events could partially reverse the rally that priced in a completed deal rather than an interim framework.

CNBC reported on 15 June 2026 that the UK, France, Germany, and Italy were prepared to lift their own sanctions on Iran contingent on verifiable nuclear steps, a multilateral layer sitting outside the bilateral US-Iran framework. If agreed separately, this could accelerate Iranian oil re-entry into global supply beyond what the US deal alone delivers.