A US Ban on Chinese Solar Inverters Won’t Lift All Boats

4 hrs ago

A single infrastructure shift in how banks borrow intraday could drain $250 billion in idle cash from the Federal Reserve. This transition to tokenized repo markets would begin unwinding the federal funds rate’s dominance over United States monetary policy, according to a Deutsche Bank projection published on July 1, 2026.

The central bank has spent years trying to shrink its balance sheet while facing structural limits on how far it can go. This market plumbing upgrade is not a policy decision from Washington, but a private-sector development that could move those limits from the outside.

Here is what this finding tells you about where monetary policy infrastructure is heading. Understanding this mechanism matters before the Depository Trust and Clearing Corporation (DTCC) launches its full tokenization service in October 2026.

Financial institutions hold hundreds of billions in idle reserves at the central bank not by choice, but because the plumbing forces them to. Banks maintain these precautionary buffers against intraday payment needs they cannot refinance instantaneously. Under the current overnight settlement cycle, liquidity is locked into batch processes.

This creates a structural inefficiency baked into legacy architecture rather than a deliberate liquidity preference. Because the conventional overnight repo market only settles at the end of the day, banks must pre-position cash for needs that arise throughout the trading session.

Deutsche Bank puts the volume of precautionary reserve balances that an intraday borrowing model would render redundant at roughly ~$250 billion. The Bank for International Settlements (BIS) confirms that tokenized collateral networks allow banks to run leaner liquidity buffers because funding mobilizes on demand in real time.

That $250 billion figure represents a structural inefficiency with a concrete price tag. What this tells you is exactly how much the current market plumbing costs the financial system in idle capital.

Three operational constraints currently force this precautionary reserve-holding: No intraday refinancing capabilities within conventional overnight markets Legacy batch settlement cycles that execute only at end-of-day * Timing gaps between immediate payment obligations and delayed funding availability

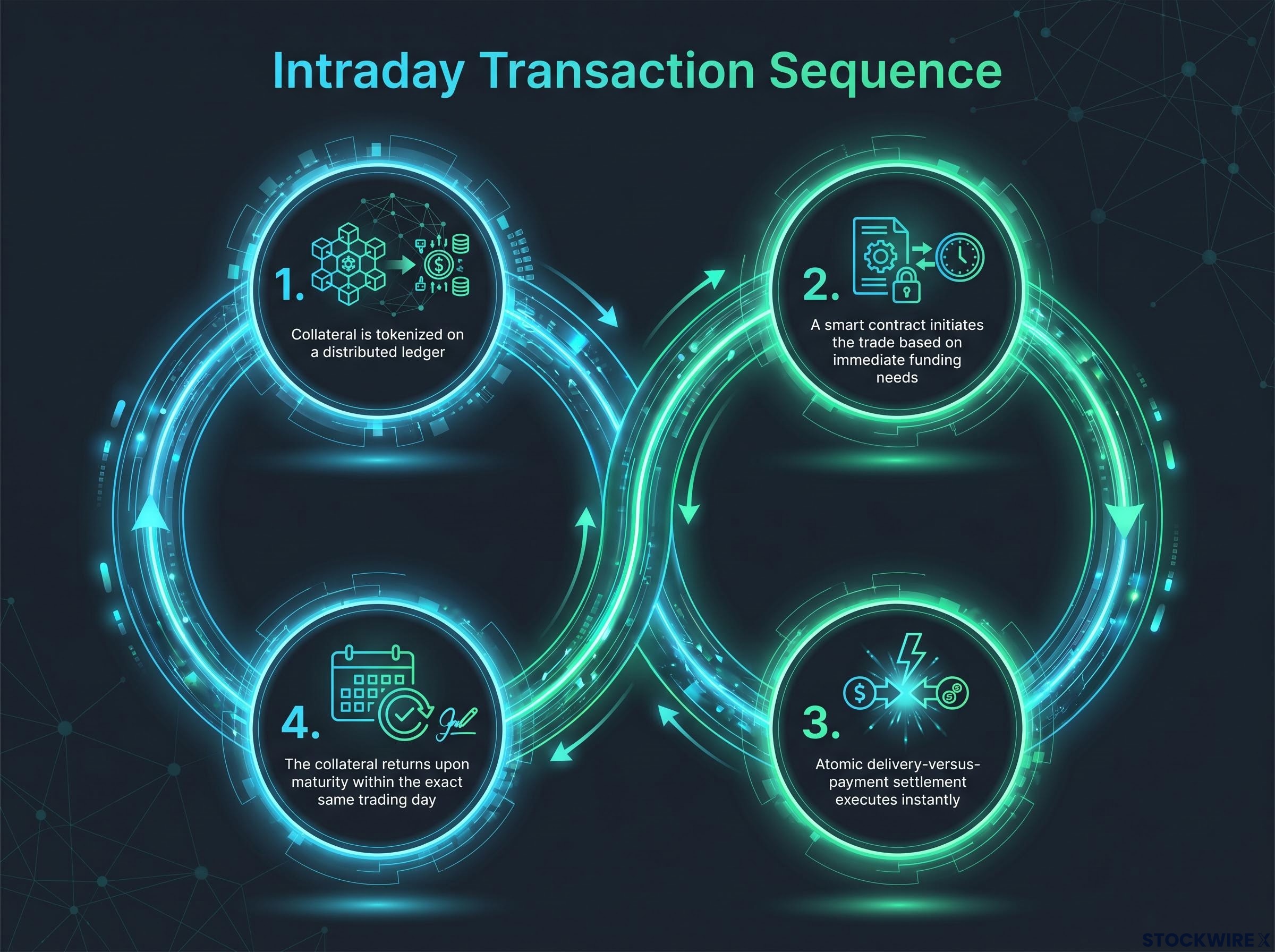

The mechanical substitution from overnight buffering to real-time borrowing relies on atomic delivery-versus-payment on a shared ledger. This core settlement innovation compresses collateral and cash movements from hours to near-instant execution. Smart contracts automate trade matching, collateral valuation, margining, and settlement in real time.

In an overnight repo market, a bank must pre-position collateral the night before. With intraday tokenized repo, that same bank can mobilize collateral on demand in the exact moment the need arises.

“Tokenizing repo markets is expected to automate processes that currently require manual intervention, fundamentally altering the traditional overnight borrowing model.”

The BIS highlights that this 24/7 availability removes the timing constraints of legacy batch-processing cycles, materially reducing intraday liquidity risk.

What this means for your understanding of market mechanics is that this is not a marginal speed improvement. It is a structural substitution of a buffering mechanism with an on-demand borrowing tool, changing the math of how much idle cash banks need to hold at all times.

The intraday transaction follows four sequential steps:

The Federal Reserve has been reducing reserves by allowing securities to roll off through quantitative tightening. However, officials remain cautious about how far this reduction can go before funding markets become stressed.

The political context behind Fed balance sheet reduction shifted materially in May 2026 when the Senate confirmed Kevin Warsh as Federal Reserve Chair with a mandate that explicitly prioritised shrinking the central bank’s $6.7 trillion asset portfolio through accelerated quantitative tightening.

Reserve balances are the central bank’s dominant liability category. Reduced bank demand for reserves directly translates to greater balance-sheet shrinkage capacity. The ~$250 billion reduction estimate represents the exact amount of additional quantitative tightening headroom created.

Quantitative tightening headroom is already a live policy variable: analysis published prior to Warsh’s confirmation identified accelerated balance sheet reduction as carrying a larger simultaneous market impact across fixed income, equities, and real estate than rate timing decisions, with yield curve steepening the most direct transmission mechanism.

This mechanism operates entirely through private-sector infrastructure development. It is contingent on widespread adoption, representing a long-term structural possibility rather than an immediate policy shift.

For your portfolio’s macroeconomic exposure, this tells you that the constraint limiting further quantitative tightening is a function of market plumbing. Private-sector tokenization progress could change the monetary math without a single central bank meeting.

| Current constraint on quantitative tightening | Constraint under intraday tokenized repo |

|---|---|

| High demand for precautionary reserves limits reduction | On-demand liquidity allows leaner reserve balances |

| Balance sheet floor sits higher to prevent stress | Balance sheet floor drops by up to $250 billion |

| Funding stress risk rises with batch settlement limits | Funding stress risk falls via real-time collateral mobility |

The relevance of the federal funds rate depends on an active market where banks lend and borrow reserve balances overnight. If banks manage liquidity intraday, overnight reserve trading volumes will shrink.

Dallas Federal Reserve President Lorie Logan identified this structural fault line well before tokenization made it concrete. In a September 2025 speech, she proposed shifting the central bank’s policy target from the fed funds rate to a Treasury repo-based rate.

Logan’s September 2025 speech to the Money Marketeers of New York University laid out the evidentiary case for replacing the federal funds rate with a Treasury repo benchmark, citing the repo market’s superior depth and transaction data as grounds for a formal policy shift.

“Treasury repo markets are deeper, more representative of actual funding conditions, and supported by significantly more transaction data than the federal funds market.”

Deutsche Bank explicitly flags this proposal as highly relevant in a scenario where tokenization increases repo activity relative to fed funds.

The Logan proposal arrives against a backdrop of a broader institutional shift: the FOMC communication regime was formally overhauled at the June 2026 press conference, with Warsh rejecting forward guidance entirely and launching task forces to review the dot plot’s continued role, removing the anchoring signals investors had relied upon to interpret rate expectations.

This signals to fixed income investors that the debate over what the central bank actually targets is no longer theoretical. It has a named proponent, a concrete research basis, and a market-infrastructure catalyst accelerating it.

The comparison between benchmarks breaks down across three dimensions: Market depth heavily favours Treasury repo over fed funds Transaction volumes in repo provide a more comprehensive daily data set * A secured rate aligns closer with actual bank funding behaviour than unsecured overnight lending

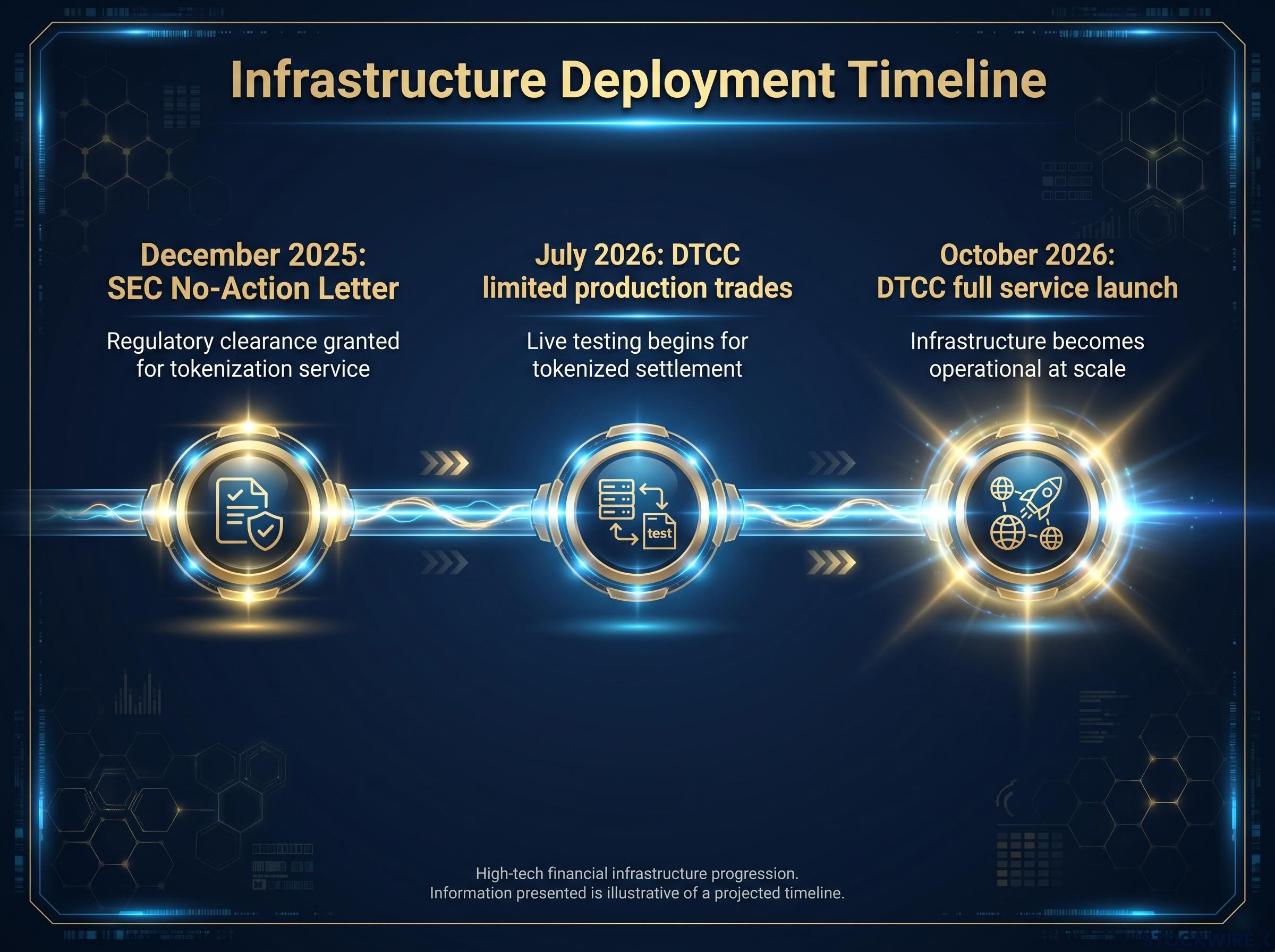

This infrastructure is not a theoretical roadmap for the next decade. The foundational components are being tested and deployed as of July 2026.

The U.S. Securities and Exchange Commission (SEC) issued a No-Action Letter in December 2025 authorising the DTCC to offer a tokenization service. This covers Russell 1000 constituents, major exchange-traded funds, and U.S. Treasuries for a three-year period.

Multiple Federal Reserve governors have publicly addressed programmable money in formal speeches, indicating active central bank evaluation. The DTCC has targeted limited production trades for this month, making the timeline immediate.

Major institutions are heavily investing in programmable cash layers, including tokenized deposits and money market funds. What this tells you is that the infrastructure enabling the $250 billion projection is moving into production right now, giving the forecast a material near-term basis.

| Date | Milestone | Significance |

|---|---|---|

| December 2025 | SEC No-Action Letter | Regulatory clearance granted for tokenization service |

| July 2026 | DTCC limited production trades | Live testing begins for tokenized settlement |

| October 2026 | DTCC full service launch | Infrastructure becomes operational at scale |

While the market infrastructure change is technically feasible today, the transition would touch every contract and derivative tied to fed funds. This shift mirrors the recent LIBOR transition in complexity and scale.

Migrating to a Treasury repo benchmark requires coordinated action across rate derivatives, money market fund reference rates, and legacy contracts. Secured funding costs would play a greater role in shaping rate expectations, while unsecured interbank lending would become less influential.

Deutsche Bank frames this as a long-term structural scenario where the direction of travel is already visible. For anyone with exposure to rate-sensitive instruments, this means the window for preparation is measured in years, but the time to understand the mechanics is now.

Three preconditions must align for this full structural shift to occur: Sufficient intraday repo volume migrating to distributed ledgers Central bank willingness to formally change its operating target * Massive market coordination across benchmark-referencing contracts

A private-sector infrastructure shift now has the potential to change central bank balance sheet math and reduce the centrality of the fed funds rate. These are long-term structural possibilities, but the catalysts driving them are live.

The DTCC full service launch in October 2026 stands as the first meaningful test of whether the collateral ecosystem can scale toward the volumes that make these projections operative. This event will reveal whether the tokenized infrastructure can absorb the transaction load required to alter banking reserve mechanics.

The variables shaping rate benchmarks and balance sheet capacity are no longer confined to Washington policy rooms. They now include infrastructure deployment timelines in lower Manhattan and smart-contract adoption curves in major bank treasury departments.

For investors wanting to map these structural changes onto their rate-sensitive exposures, our full explainer on Treasury yields as a policy lever details how the 10-year and 30-year yields have displaced equity markets as Washington’s primary forcing mechanism, covering the four equity tail risks that each loop back into the same yield-pressure framework.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Tokenized repo markets use distributed ledgers and smart contracts to settle repurchase agreements in real time, replacing the overnight batch-settlement cycle with atomic delivery-versus-payment that executes within the same trading day.

Banks pre-position that cash at the Fed because conventional overnight repo only settles at end of day, forcing institutions to buffer against intraday payment needs they cannot refinance instantaneously under legacy plumbing.

By allowing banks to borrow intraday on demand rather than holding idle reserves, tokenized repo could reduce precautionary reserve balances by roughly $250 billion, directly expanding the Fed's capacity to shrink its balance sheet through quantitative tightening.

The DTCC tokenization service received SEC regulatory clearance via a No-Action Letter in December 2025 and covers Russell 1000 stocks, major ETFs, and U.S. Treasuries; limited production trades began in July 2026 with full service launch targeted for October 2026.

A transition to a Treasury repo benchmark would require coordinated migration across rate derivatives, money market fund reference rates, and legacy contracts, a process Deutsche Bank compares to the LIBOR transition in scale and complexity.