Why Fed Forward Guidance Is Gone and What Investors Must Build

5 hrs ago

Goldman Sachs analyst Brian Lee published a note on 1 July 2026 responding to reports that the Trump administration is drafting a ban on Chinese solar inverter imports. His conclusion was precise and counterintuitive: the benefit to the two dominant US-listed players would be real, but modest, and unevenly distributed in ways that matter for investors.

Chinese manufacturers Sungrow and Chint have built meaningful positions in US commercial, industrial, and utility-scale inverter markets. A ban framed as a national security measure could reshape those competitive dynamics. But the segment where Chinese firms are weakest, US residential rooftop solar, is the segment where Enphase and SolarEdge already dominate. The gap between the headline and the underlying market structure is where the investment analysis begins.

Here is what the market share data actually tells you about who benefits, how much, and under what conditions. The picture is segmented, not binary, and the distinction between competitive relief and stock attractiveness is sharper than most coverage suggests.

The Trump administration is drafting the measure through the Federal Communications Commission (FCC), the US agency that regulates communications infrastructure, framing it as a grid security initiative targeting foreign-controlled hardware connected to the US power network. Reuters reported the proposal on 30 June 2026, and Goldman Sachs responded with a same-day analyst note on 1 July 2026.

Goldman Sachs analyst Brian Lee was explicit about what his firm does and does not know. Lee declined to vouch for the accuracy of the Reuters report and flagged that the rule could be narrowed, delayed, or abandoned before finalisation.

The solar inverter proposal follows a structural template visible across multiple sectors: Chinese technology import barriers in the US now typically operate through independent legal authorities, meaning a single policy change rarely removes the restriction entirely, and scope, timing, and exemptions routinely shift between draft and enforcement.

Three sources of uncertainty deserve attention before investors assign any probability to this proposal becoming policy:

Until the rule is finalised and tested in trade and legal channels, this is a probability to model against segment exposure, not a confirmed tailwind to build a position around.

Executive Order 13920 on bulk-power system security established the legal template for restricting foreign-sourced hardware from US grid infrastructure, empowering the Secretary of Energy to block transactions involving equipment from foreign adversaries on national security grounds, a precedent that the FCC-led inverter proposal follows in structure if not in agency.

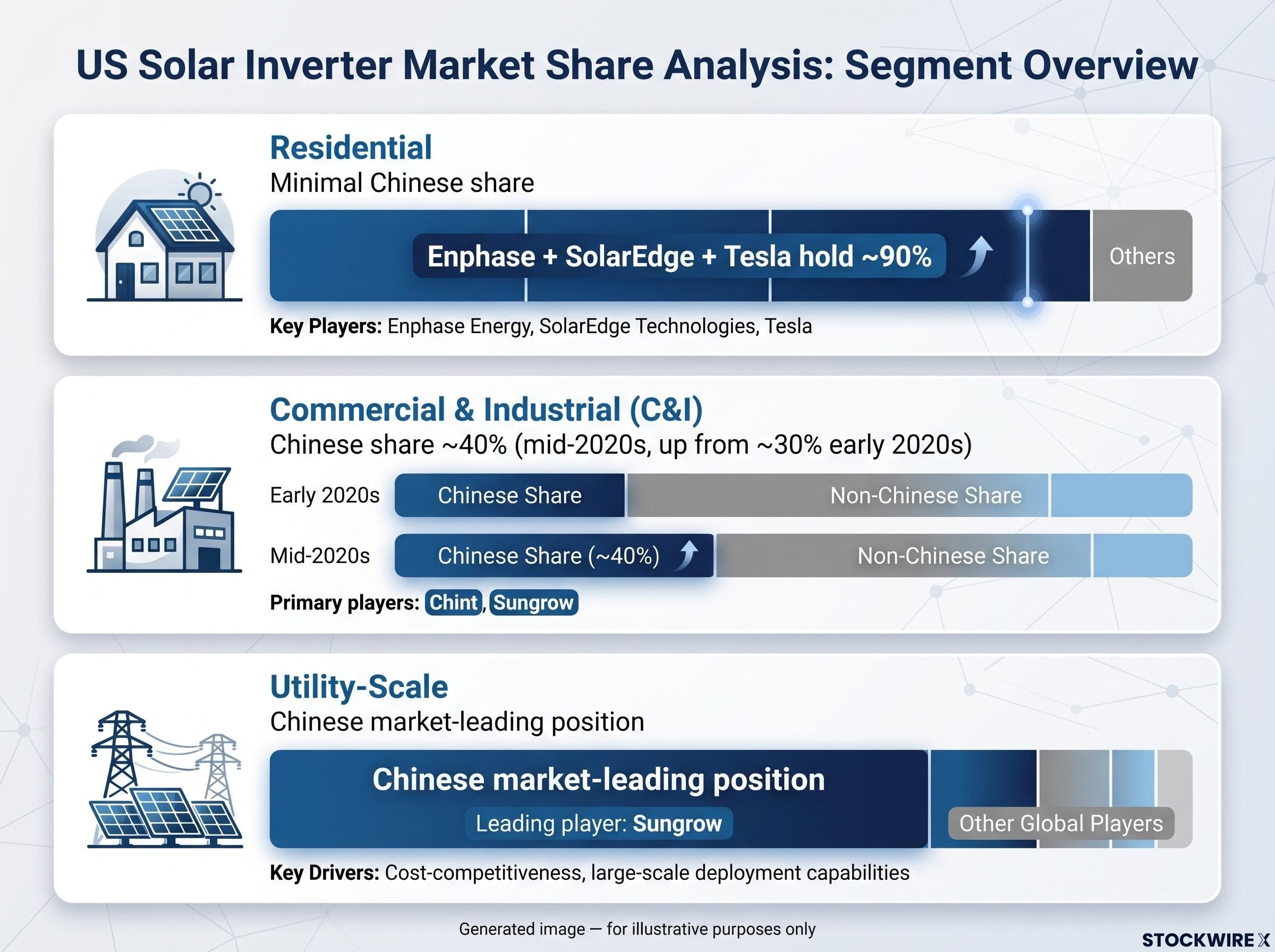

The impact of any ban hinges on where Chinese manufacturers have real share today. That picture is sharply differentiated by segment, and the differentiation is what determines who benefits and by how much.

| Segment | Chinese manufacturer share | Primary Chinese players |

|---|---|---|

| Residential | Minimal (Enphase + SolarEdge + Tesla hold ~90%) | None with significant presence |

| Commercial & Industrial (C&I) | ~40% (mid-2020s, up from ~30% early 2020s) | Chint, Sungrow |

| Utility-Scale | Market-leading position | Sungrow (leading) |

The C&I share gain from approximately 30% to approximately 40% over the first half of the 2020s is the trend that matters most. Chint and Sungrow built that foothold largely on price and increasingly credible product performance, and it is the segment where any ban would most directly alter competitive dynamics.

At utility-scale, Sungrow holds the leading position in the US market. That dominance in large, grid-connected infrastructure is precisely the type of presence that triggers national security concerns and forms the core rationale for the proposed restriction.

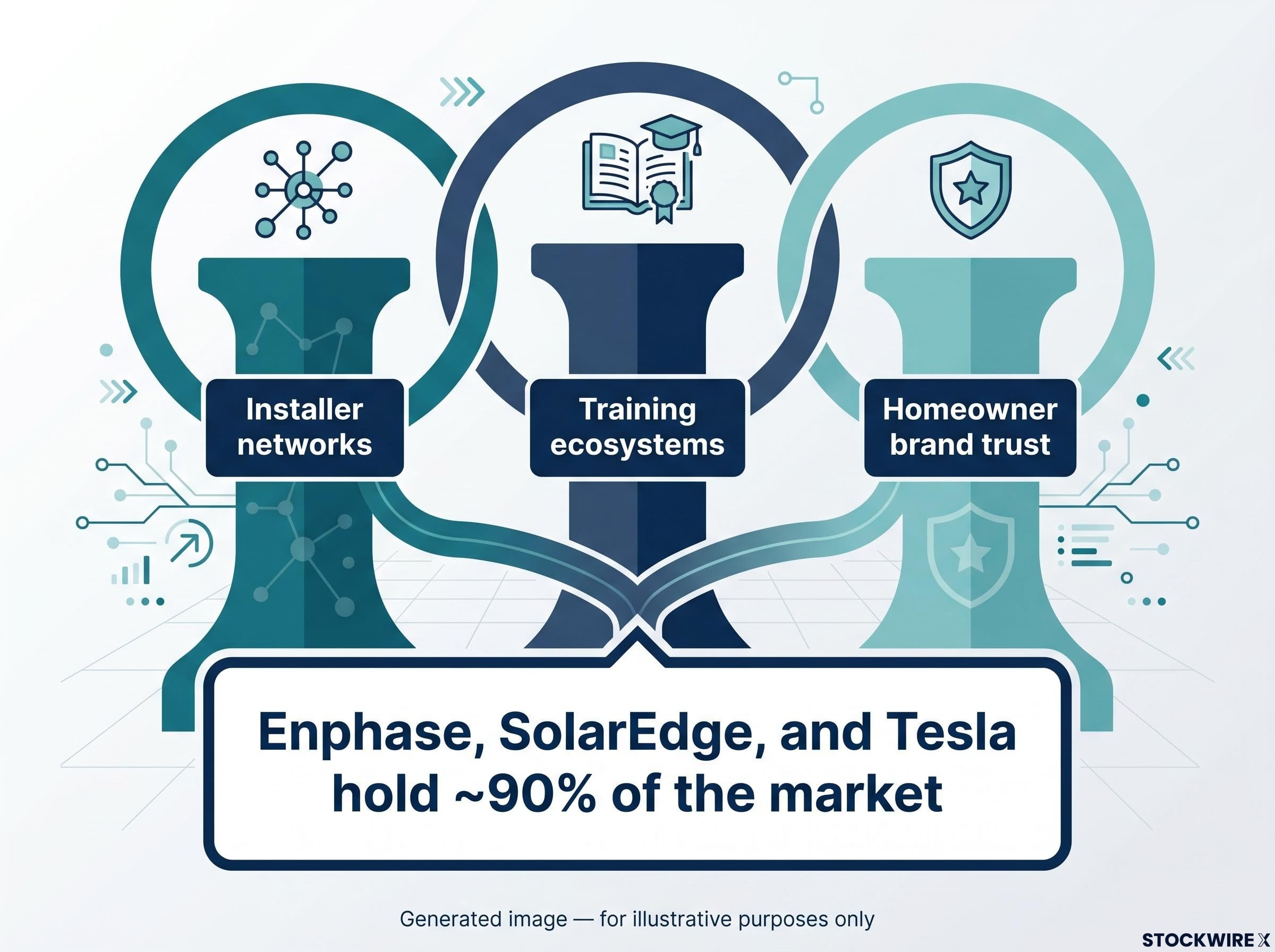

Three factors explain why Chinese firms never gained traction in residential despite their success elsewhere. Domestic installers and distributors have deep, long-standing relationships with Enphase and SolarEdge that new entrants cannot replicate quickly. Training ecosystems, including certifications, support infrastructure, and troubleshooting tools, create switching costs that protect incumbents even when a lower-cost alternative arrives. And homeowners, who rarely select inverter brands independently, rely on installer recommendations, which means brand trust flows through the channel rather than around it.

The residential moat was built by ecosystem depth, not protected by policy. A ban reinforces a wall that was already standing rather than constructing a new one.

SolarEdge competes more directly against Chint and Sungrow in commercial and industrial projects, making it the larger near-term beneficiary of a ban. Reduced price pressure, a cleaner opportunity to reclaim lost share, and a stronger position when bidding for new C&I projects are all plausible outcomes if Chinese competitors are removed or materially constrained.

Goldman Sachs analyst Brian Lee’s 1 July 2026 note identified SolarEdge as standing to benefit more than Enphase from the proposed restriction, given its larger C&I presence. The competitive relief case is straightforward.

The stock case is not.

Goldman Sachs maintains a Sell rating on SolarEdge with a price target of $31-$34 (as of April 2026; sources conflict on the exact figure). The ban is, in Lee’s framing, “a tactical tailwind, not a cure-all.”

The Sell rating reflects concerns about demand visibility, execution challenges, margin and cost structure pressures, and product and geographic mix. None of those are problems a regulatory ban resolves. A regulatory tailwind and a weak fundamental profile can coexist, and SolarEdge is the case study in why you should not conflate one for the other.

This is the distinction that matters for portfolio decisions. Positive regulatory news is not the same thing as a reason to upgrade a stock. Goldman Sachs’s own framework explicitly holds both views simultaneously.

The residential inverter market operates on fundamentally different competitive logic to C&I or utility-scale. Understanding why explains both the strength of the incumbents’ position and the limited relevance of a ban to that segment.

The installer and distributor network is the primary gatekeeping layer. Homeowners rarely research or select inverter brands independently. Instead, they rely on their solar installer’s recommendation, which means the installer’s preference becomes the structural competitive advantage. If an installer has trained on Enphase microinverters, built troubleshooting workflows around Enphase’s platform, and earned certification through Enphase’s programmes, the cost of switching to a new brand is not just financial; it is operational.

Three factors sustain this concentration:

Enphase, SolarEdge, and Tesla together hold approximately 90% of this market. Chinese manufacturers have not achieved significant penetration despite competitive pricing in other segments.

For investors evaluating Enphase, the lesson is that a ban protecting the residential market is largely redundant. But the same ecosystem depth that makes the residential moat durable is what makes the company’s planned C&I expansion credible. The skills, relationships, and brand equity transfer.

Enphase has set a target of capturing approximately 40% of the C&I market within a three-year horizon. Today, Chint and Sungrow together hold approximately 40% of that same segment. The arithmetic is obvious: removing or limiting those incumbents reduces the competitive friction Enphase faces in executing its C&I plan.

Two time horizons frame how this plays out:

Goldman Sachs maintains a Buy rating on Enphase with a $57 price target as of May 2026.

That Buy rating was established without assuming the ban happens, which tells you the ban is an incremental positive to an existing thesis, not the foundation of it. For Enphase investors, the ban is best read as a path-of-least-resistance improvement to a growth narrative already in motion, not a new reason to own the stock if you were not already constructive on the C&I execution story.

The pattern that has emerged across this analysis is the one Goldman Sachs built its framework around: asymmetric benefit meeting asymmetric fundamental quality.

SolarEdge benefits more directly from a ban, particularly in C&I. Goldman Sachs rates it Sell. Enphase benefits less immediately, but Goldman Sachs rates it Buy. The analyst’s framework holds both truths simultaneously, and that is precisely the complexity you need to hold as well.

| Metric | Enphase | SolarEdge |

|---|---|---|

| Goldman Sachs rating | Buy | Sell |

| Price target | $57 (May 2026) | $31-$34 (April 2026) |

| Primary market exposure | Residential (~90% share with peers) | C&I (direct Chinese competition) |

| Ban benefit magnitude | Moderate (C&I expansion path clears) | Larger near-term (C&I competitive relief) |

| Key risk factor | C&I execution timeline | Demand visibility, margins, cost structure |

The market is not just pricing regulatory outcomes. It is pricing execution capacity and fundamental health, and the ban cannot substitute for either. Goldman Sachs analyst Brian Lee’s note explicitly cautions against treating this analysis as a standalone investment signal; it should be combined with independent fundamental work on demand, margins, valuation, and policy risk.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. These statements are speculative and subject to change based on market developments and company performance.

The proposed ban would improve competitive conditions selectively, in C&I and potentially utility-scale, without touching the already-secured residential market that anchors both companies’ current revenue bases. That distinction is the entire analytical finding in one sentence.

What the ban changes is real: competitive friction in specific segments, addressable market openness for expansion plans, and the viability of longer-dated utility-scale strategies. What it does not change is equally real: fundamental demand cycles, margin structures, execution risk, and valuation.

Three forward-looking variables will determine whether the competitive relief, if it arrives, translates into earnings:

The regulatory narrative is real but conditional. The investment case is dependent on fundamentals the ban cannot fix. Separating those two is what turns headline-driven positioning into informed solar sector analysis.

For investors wanting to stress-test how structurally durable these restrictions are across a full trade negotiation cycle, our deep-dive into US-China tech restriction durability examines why national-security-grounded controls sit outside the jurisdiction of trade negotiators and how that changes the probability framework for any rollback.

—

The Trump administration is drafting a measure through the Federal Communications Commission framing it as a grid security initiative to block foreign-controlled hardware, specifically Chinese-made solar inverters from Sungrow and Chint, from connecting to the US power network. As of early July 2026, the rule remains in draft form and has not been finalised.

SolarEdge would see the larger near-term benefit because it competes directly against Chint and Sungrow in the commercial and industrial segment, where Chinese firms hold roughly 40% share. Enphase benefits more modestly, as Chinese manufacturers never gained meaningful penetration in its core residential market, though a ban would ease Enphase's planned expansion into C&I.

Goldman Sachs analyst Brian Lee describes the ban as a tactical tailwind, not a cure-all. The Sell rating reflects persistent concerns about SolarEdge's demand visibility, margin pressures, and execution challenges, none of which a regulatory restriction resolves. Competitive relief and fundamental stock quality are separate questions.

Chinese manufacturers have minimal presence in US residential solar. Enphase, SolarEdge, and Tesla together hold approximately 90% of that market, a dominance built on deep installer networks and training ecosystems that create switching costs no pricing advantage can easily overcome.

Enphase has set a target of capturing approximately 40% of the commercial and industrial inverter market within a three-year horizon, the same share Chint and Sungrow currently hold together. A ban removing those competitors would reduce the friction Enphase faces in executing that plan, though execution, pricing, and product performance still determine whether the target is reached.