AI Chip Rally Up 50% in Two Months: Barclays Sees Cracks

7 hrs ago

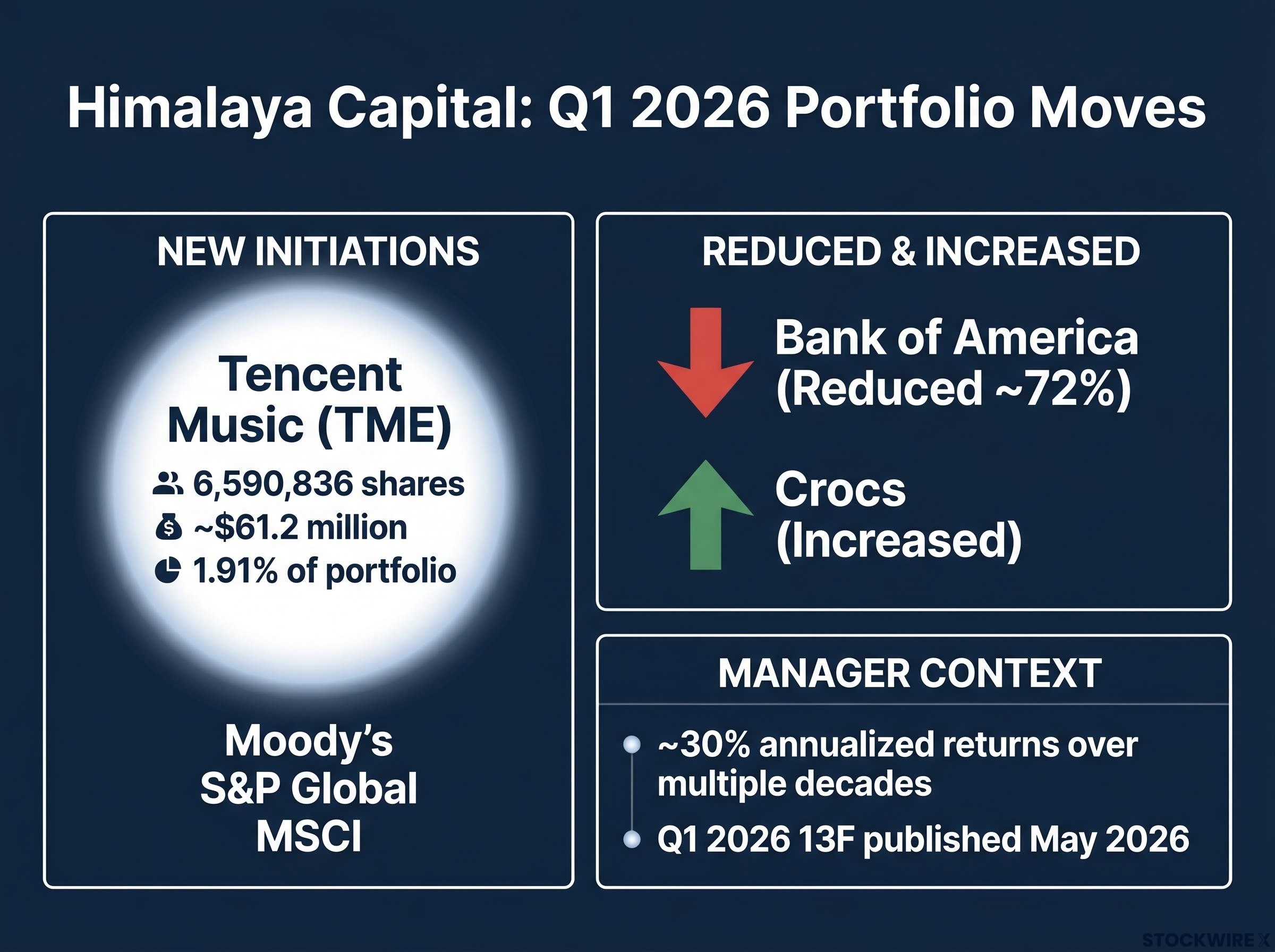

One of the most respected value investors alive, a man Charlie Munger trusted with his own capital, recently initiated a position in a Chinese music streaming company trading at roughly 10 times free cash flow with more cash on its balance sheet than total debt. Li Lu’s portfolio moves are rare and closely watched. His Q1 2026 13F filing, published in May 2026, revealed a new stake in Tencent Music Entertainment (TME) worth approximately $61 million, alongside initiations in Moody’s, S&P Global, and MSCI. That cluster of moves reflects a deliberate search for durable, cash-generating businesses at discounted prices. For U.S. retail investors, the question is whether TME’s valuation gap reflects a genuine mispricing or a risk premium that is entirely justified.

This analysis walks through the investment case: who Li Lu is and why his initiation matters, what TME’s business actually does and how it generates cash, what the numbers show across three valuation scenarios, why the company’s capital return posture is worth noting, and what the honest risk picture looks like for investors weighing a China-listed ADR.

Li Lu, founder of Himalaya Capital, has reportedly generated annualised returns of approximately 30% over multiple decades. He publishes no investor letters. He gives almost no interviews. His moves surface only through quarterly 13F filings with the SEC, and even then, the positions are concentrated enough that each new initiation carries weight.

Charlie Munger trusted Li Lu with his own personal capital, a distinction shared with almost no other external manager. That single fact remains the clearest shorthand for Li Lu’s standing in value investing circles.

The Q1 2026 filing revealed a coherent set of decisions, not a scattershot quarter:

The pattern is legible. Moody’s, S&P Global, and MSCI are toll-booth businesses that collect fees regardless of market direction; their recent price declines, driven by AI competitive concerns, created a discounted entry. TME fits the same framework: a dominant market position generating growing free cash flow at a price that reflects China-specific discount rather than business-specific deterioration. Li Lu does not initiate positions casually. When he does, the signal-to-noise ratio is higher than most 13F disclosures warrant.

Tencent Music Entertainment operates QQ Music, Kugou, and Kuwo, the three dominant music streaming platforms in China, serving hundreds of millions of users. The business sits within Tencent’s majority-controlled ecosystem (the parent holds over 50%), and Mohnish Pabrai has previously described Tencent’s management as among the best in the world.

The revenue mix tells the story of a business in active transition. Online music services, which include subscriptions and advertising, represent the higher-margin, faster-growing segment. Legacy social entertainment revenue, once a meaningful contributor, is in structural decline. The investment case rests on which segment is driving the trajectory, and the recent financials answer that clearly.

Fortune Business Insights’ China music streaming market projections, covering growth through 2033, indicate that subscription revenue expansion is the dominant structural driver for the category, reinforcing why TME’s ongoing shift toward higher-margin online music services is aligned with the broader market trajectory rather than running against it.

| Metric | Value | YoY growth |

|---|---|---|

| FY 2025 total revenue | RMB 32.90 billion (US$4.71 billion) | +15.8% |

| Q1 2026 online music revenue | RMB 6.51 billion | +12.2% |

| Q1 2026 membership services revenue | RMB 4.57 billion | +6.6% |

The highest-margin business is the one growing fastest. A reader evaluating the valuation multiples in the next section needs that context, because margin trajectory depends entirely on revenue composition.

TME’s ownership of three separate platforms creates scale advantages in licensing negotiations and user acquisition costs that no single-platform competitor can replicate. NetEase Cloud Music is the primary direct competitor, differentiated through community features and younger-skewing playlists. Douyin and short-video platforms compete indirectly for user attention rather than subscription dollars.

Regulatory changes in prior years forced TME to end exclusive licensing arrangements, normalising the competitive environment. That intervention removed a tail risk: the prospect of further regulatory action on this specific front has diminished. The playing field is now more level, but TME’s three-platform scale still commands superior negotiating leverage with labels and publishers.

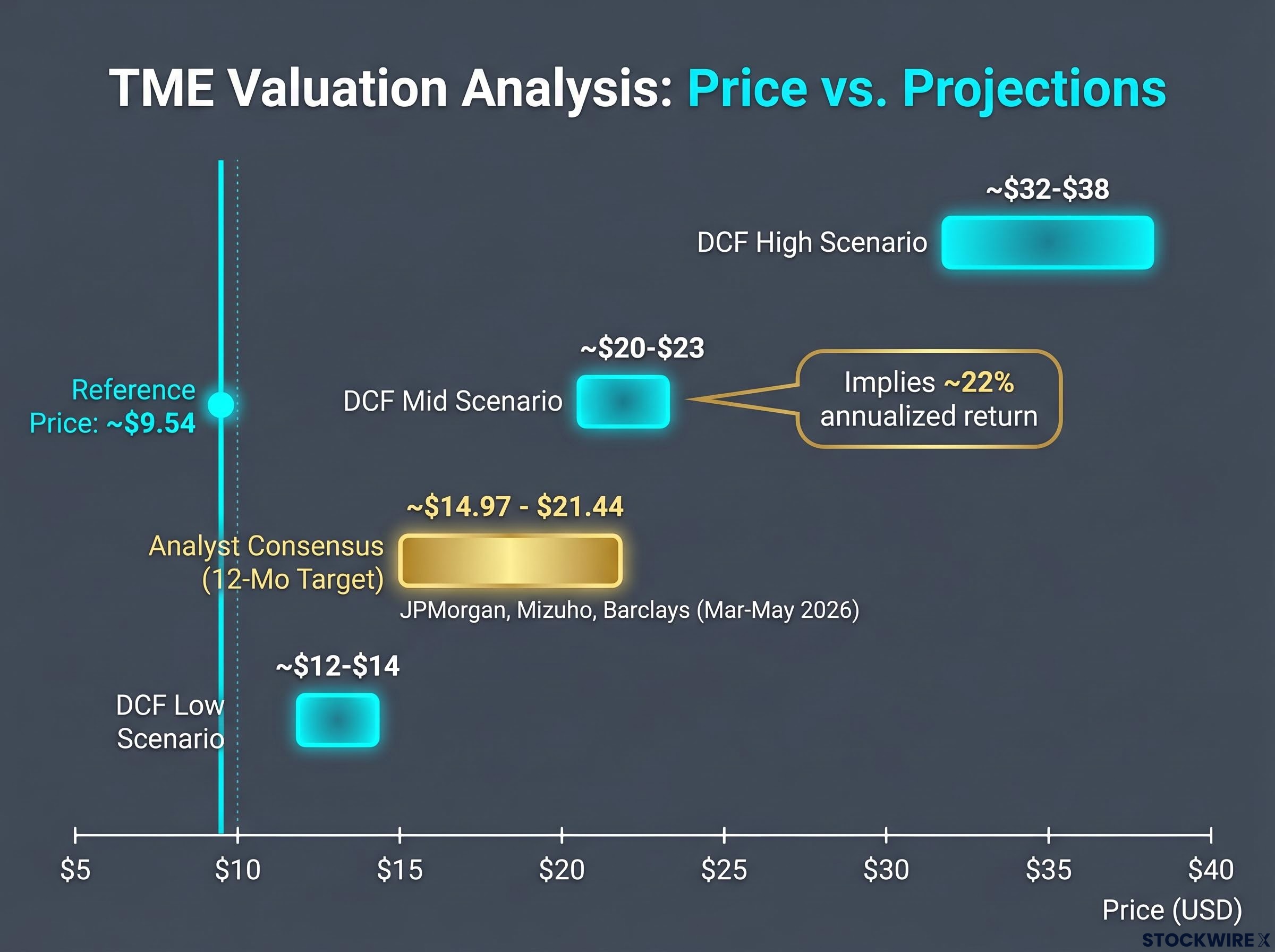

The starting point is a structural observation that changes how the valuation reads. TME’s enterprise value falls below its market capitalisation because the RMB 38.04 billion in cash and short-term investments (as of 31 December 2025) exceeds total debt. A buyer of TME stock at the reference price of approximately $9.54 is effectively acquiring the operating business at a discount to the stated market cap of roughly $15 billion.

Free cash flow has averaged approximately $1.2 billion annually over the prior five years, rising to approximately $1.5 billion in the most recent reported year. Net profit margin has expanded from a five-year average of approximately 20% to approximately 26.5% most recently, confirming the operating leverage thesis: cash flow and earnings growth are outpacing revenue growth.

A three-scenario discounted cash flow model, applied over a 10-year horizon, produces the following range:

| Scenario | Revenue growth | Profit margin | FCF margin | Implied intrinsic value |

|---|---|---|---|---|

| Low | 5% | 22% | 26% | ~$12-$14 |

| Mid | 8% | 25% | 29% | ~$20-$23 |

| High | 11% | 28% | 33% | ~$32-$38 |

The mid-case scenario implies approximately 22% annualised returns from the reference price of $9.54, a figure that becomes more notable when considered alongside analyst consensus 12-month price targets ranging from approximately $14.97 to $21.44, with recent updates from JPMorgan, Mizuho, and Barclays in March to May 2026.

Even the low scenario suggests the stock is trading near fair value rather than at a premium, which narrows the downside asymmetry for a value-oriented investor.

For investors wanting to stress-test the assumptions behind the three-scenario model, our dedicated guide to intrinsic value estimation and margin of safety walks through DCF construction, terminal value sensitivity, and the specific discount-to-intrinsic-value thresholds that value practitioners use before committing capital.

A company that returns hundreds of millions of dollars to shareholders annually while maintaining a net cash balance sheet is making a statement about its confidence in cash flow durability. TME’s capital return programme has three components:

At the reference price, the dividend yield sits at approximately 2.5%. Under the mid-case DCF scenario, yield on cost would increase meaningfully as share price appreciation compounds alongside growing distributions.

One caveat belongs in this section rather than buried later: capital repatriation from China is subject to regulatory, foreign exchange, and capital-control considerations. Analyst commentary consistently notes that management may balance distributions against content investment and strategic initiatives, and that the mechanics of returning cash from a China-domiciled business to U.S. ADR holders carry friction that domestic dividend payers do not face.

Capital repatriation constraints are not abstract: Chinese companies are subject to legal frameworks that can prioritise state directives over shareholder interests, and the foreign exchange mechanics of moving cash from a China-domiciled entity to U.S. ADR holders carry friction with no direct equivalent in developed-market dividend payers.

The valuation discount relative to global streaming peers such as Spotify exists for reasons that are specific, structural, and ongoing. Understanding the shape of these risks, rather than a generic warning, allows a more informed sizing decision.

Chinese regulators have signalled a posture of supporting China’s digital economy while retaining content and data security oversight, a stance that has benefited platform companies broadly but remains contingent on political priorities that can shift without the advance signals investors in OECD markets typically receive.

The SEC’s HFCAA compliance list confirmed that as of December 2022 the PCAOB vacated its prior determinations, meaning no Chinese issuers currently face a trading prohibition under the Holding Foreign Companies Accountable Act, a development that materially reduced one of the more acute delisting risks that had weighed on China ADR valuations through 2021-2022.

Major U.S. asset managers, including BlackRock Investment Institute, Charles Schwab, and Fidelity, have noted in 2024-2026 commentary that concerns about China’s property sector, local government debt, and longer-term growth prospects continue to weigh on Chinese equity valuations broadly, even where company-specific fundamentals are solid. Policy measures by Chinese authorities to support capital markets and consumer confidence have received mixed investor reception.

Douyin and short-video platforms represent an attention-economy threat rather than direct subscription competition. The risk is user time displacement: hours spent on short-form video are hours not spent on music streaming, which can slow engagement metrics and advertising revenue growth even if subscription counts hold.

The legacy social entertainment segment is in structural decline, visible in reported financials. That transparency partially reduces its surprise potential; the decline is already priced into forward estimates rather than lurking as an unrecognised headwind.

The value trap distinction sits at the heart of the TME investment case: a business trading cheaply because its core segment is in structural decline is a categorically different opportunity from one trading cheaply because country-level risk has compressed the multiple on a growing cash flow stream.

Three conditions would need to hold for the mid-case DCF scenario to materialise:

Analyst consensus 12-month price targets range from approximately $14.97 to $21.44, broadly consistent with the DCF mid-case range of approximately $20-$23. That independent corroboration from JPMorgan, Mizuho, Barclays, and others strengthens the model’s credibility rather than simply restating it.

Consensus forward projections estimate EPS growing from approximately $1.20 to $1.76 over four years, with revenue expanding from approximately $5.5 billion to $8.3 billion over the same period. FY 2025 actual revenue of US$4.71 billion suggests the company is tracking within that corridor. Q1 2026 IFRS net profit of RMB 2.09 billion (US$303 million), with diluted EPS per ADS of RMB 1.34 (US$0.19), provides the most recent data point.

Li Lu’s initiation is one input in the investment process, not a sufficient condition for investment. 13F disclosures are backward-looking by design, and position sizes can and do change between filing periods.

TME holds a dominant market position in Chinese music streaming, generates strong and growing free cash flow at a low multiple, and has attracted a smart-money initiation from an investor whose track record earns that label. The valuation gap relative to global peers exists for reasons that are real: geopolitical risk, regulatory uncertainty, and capital repatriation constraints. The investment decision is a judgement call about whether that risk premium is currently too wide.

Investors evaluating a position may consider monitoring TME’s subscription growth and margin trajectory through subsequent quarterly earnings reports. Changes in Himalaya Capital’s 13F disclosures would serve as a secondary signal of whether the thesis that prompted Li Lu’s initiation remains intact.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Tencent Music Entertainment operates QQ Music, Kugou, and Kuwo, the three dominant music streaming platforms in China, generating revenue primarily through subscriptions, advertising, and legacy social entertainment services. The higher-margin online music and membership segment is growing fastest, with Q1 2026 online music revenue up 12.2% year over year.

Li Lu's Himalaya Capital initiated a position of approximately 6.59 million shares worth around $61.2 million in Q1 2026, representing roughly 1.91% of the reported portfolio, alongside similar initiations in Moody's, S&P Global, and MSCI. The move reflects a search for dominant, cash-generating businesses trading at discounted multiples due to country-level risk rather than business-specific deterioration.

At a reference price of approximately $9.54, TME trades at roughly 10 times free cash flow, with a net cash balance sheet where cash and short-term investments of RMB 38.04 billion exceed total debt, meaning the operating business is effectively acquired at a discount to the stated market cap. A three-scenario DCF model produces implied intrinsic values ranging from $12-$14 in a low case to $32-$38 in a high case.

The primary risks include Chinese regulatory and policy uncertainty, U.S.-China geopolitical tensions that could affect ADR structures, capital repatriation constraints when moving cash from a China-domiciled entity to U.S. shareholders, and competition from short-video platforms like Douyin displacing user attention. The legacy social entertainment segment is also in structural decline, visible in reported financials.

TME paid a 2025 annual cash dividend of US$0.24 per ADS, totalling approximately US$368-370 million, paid in April 2026, which at the reference price of around $9.54 represents a dividend yield of approximately 2.5%. The company also runs ongoing share buyback programmes and holds substantial cash reserves providing capacity for continued or expanded distributions.