What the SpaceX IPO Actually Means for Australian Investors

3 hrs ago

Between 95% and 99% of retail clients at EuropeFX and TradeFred lost money trading contracts for difference (CFDs). The firms on the other side of those trades profited directly from every dollar their clients lost. On 11 June 2026, Australia’s Federal Court put a number on what that business model cost: $300.2 million in civil penalties against Union Standard International Group (USG), EuropeFX, and TradeFred, the largest monetary sanctions ever connected to an ASIC enforcement matter. The penalty orders are stayed until 13 July 2026, making this a live and consequential outcome for anyone trading leveraged products through Australian-licensed providers. What follows is a breakdown of what the court found, how these firms structured their operations to profit from client failure, what the penalty actually means for harmed investors, and what specific warning signs retail CFD traders can use to protect themselves.

The penalty orders break down across three entities, each reflecting a distinct role in the misconduct structure.

| Entity | Penalty | Role |

|---|---|---|

| Union Standard International Group (USG) | $156.7 million | AFS licensee; bore systemic responsibility for authorised representatives’ conduct |

| EuropeFX | $114.1 million | Authorised representative; primary retail client-facing operation |

| TradeFred | $29.4 million | Authorised representative; secondary retail operation |

The combined $300.2 million total follows a liability judgment delivered on 20 December 2024 in ASIC v Union Standard International Group Pty Ltd (No 4) [2024] FCA 1481, which found systemic unconscionable conduct, misleading and deceptive conduct, and provision of unlicensed personal advice. The penalty hearing took place on 1-2 July 2025, with orders issued yesterday.

ASIC’s December 2024 media release on the liability judgment confirmed that combined client losses exceeded $83 million and that the court found systemic unconscionable conduct, misleading and deceptive conduct, and provision of unlicensed personal advice across the three entities.

ASIC Chair Sarah Court confirmed the penalties represent the highest monetary sanctions ever achieved in connection with an ASIC enforcement matter. The scale was not arbitrary.

Justice Wigney characterised EuropeFX’s breaches as deliberate, flagrant, and among the most serious contravening conduct he could envisage, warranting maximum deterrence.

That language from the bench signals how the court weighted the conduct: not as a compliance lapse at the margins, but as a systematic operation the court treated as warranting the most severe response available.

The structure that drove both the misconduct and the penalties rests on a single mechanism: B-book dealing. When a CFD provider operates a B-book, it does not pass client trades through to external markets. Instead, the provider takes the opposite side of every client trade. If the client loses, the provider profits. If the client wins, the provider loses.

That is not, on its own, unlawful. Many CFD providers operate B-book models. What matters is what happens when that structural conflict shapes the entire sales strategy, and when 95-99% of clients lose money while the provider’s revenue depends on exactly that outcome.

The leverage and margin mechanics that sit beneath the B-book conflict are not incidental technical detail; at 20:1 leverage, a 5% adverse price move wipes out the entire margin deposit, a mathematical reality that explains why client capital erodes so rapidly when account managers are simultaneously incentivised to encourage larger positions.

| When a client loses money… | Client’s position | B-book provider’s position |

|---|---|---|

| Trade closes at a loss | Capital erodes; incentive to reduce risk or exit | Revenue increases; incentive to encourage more trading and deposits |

Combined client losses across EuropeFX and TradeFred exceeded $83 million during the misconduct period. The court found that this conflict was not incidental to operations. It underpinned the entire sales and advice strategy.

The business model’s conflict extended to the individuals making the phone calls. Staff remuneration at EuropeFX and TradeFred was tied to client deposit volumes and trading activity, not to client outcomes or satisfaction. Account managers earned more when clients deposited more and traded more frequently, regardless of whether those clients were losing money.

This made individual staff behaviour a systemic conduct risk. The pressure to push deposits and trading volume was not the work of a few rogue employees; it was structurally embedded in how staff were paid.

The court’s finding of unlicensed personal advice sounds abstract until the specific conduct is described. Account managers at EuropeFX and TradeFred were giving individual clients tailored recommendations on position sizes, trading strategies, and funding decisions, calibrated to each client’s circumstances. Under Australian law, that constitutes personal financial advice requiring an Australian Financial Services (AFS) licence or proper authorisation. These account managers held neither.

The specific misconduct patterns identified by the court included:

Customers were falsely assured that CFD products were appropriate for their individual financial circumstances and tolerance for risk, despite no proper assessment having been conducted.

The firms deliberately targeted inexperienced or financially vulnerable customers who did not understand the risks of leveraged products. What was presented as “account support” or “mentoring” was, in practice, unlicensed and incentivised financial advice designed to keep clients depositing and trading.

USG’s $156.7 million penalty is the largest of the three, yet USG was not the entity making the phone calls or giving the personalised recommendations. That apparent mismatch raises a question worth understanding.

USG held the AFS licence. EuropeFX and TradeFred operated as its authorised representatives, providing financial services under USG’s licence. Under the AFS regime, the licensee bears full legal accountability for the conduct of authorised representatives operating under its licence. That accountability cannot be delegated away.

AFS licensee obligations under s 912A of the Corporations Act do not disappear when a business winds down; reporting, competence, and breach-notification duties continue until ASIC formally cancels the licence, which is part of why the USG enforcement record remained actionable even after the company entered administration.

The court held USG liable for the systemic unconscionable conduct of its representatives and assigned the largest penalty accordingly. For retail investors, this distinction matters practically:

The case also produced a significant legal first. EuropeFX and TradeFred marketed CFDs to clients in China despite knowing, or having reasonable grounds to know, that those clients may have been breaching Chinese domestic law by trading offshore CFDs.

The court found this breached the obligation under Australian financial services law to provide services “efficiently, honestly and fairly” (the EHF obligation). This marked the first civil penalty imposed for breaching the EHF obligation specifically in the context of exposing foreign clients to legal risk under their own domestic law. Providers cannot treat foreign clients’ domestic legal exposure as irrelevant to their own compliance obligations.

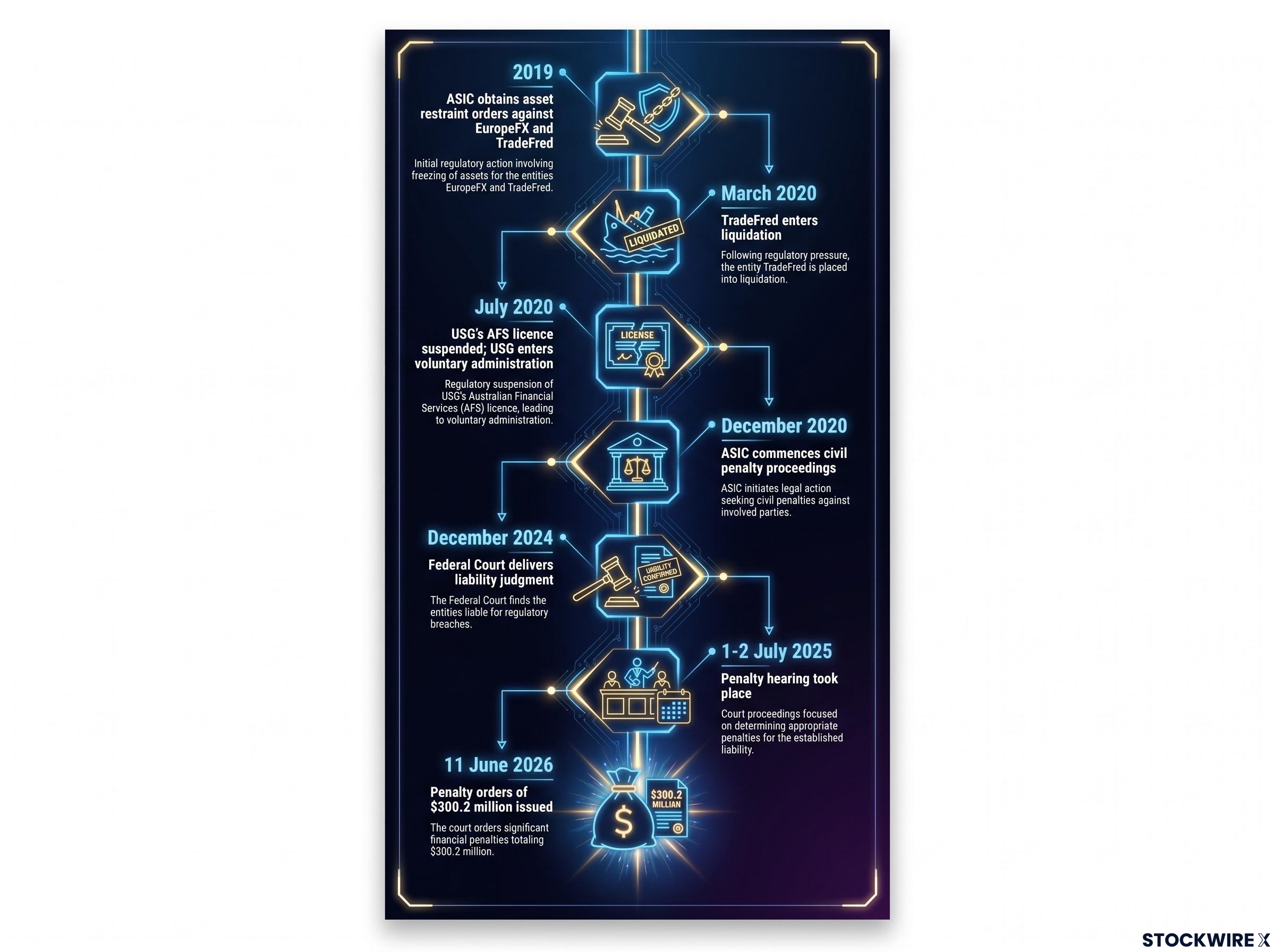

The enforcement effort behind these penalties spanned more than six years, reflecting the scale and complexity of the case.

| Date | Event |

|---|---|

| 2019 | ASIC obtains asset restraint orders against EuropeFX and TradeFred |

| March 2020 | TradeFred enters liquidation |

| July 2020 | USG’s AFS licence suspended; USG enters voluntary administration |

| December 2020 | ASIC commences civil penalty proceedings |

| December 2024 | Federal Court delivers liability judgment |

| 11 June 2026 | Penalty orders of $300.2 million issued |

The timeline demonstrates sustained regulatory commitment. It also reveals the structural limitation that the reader most needs to understand.

Director misconduct patterns across Australian CFD enforcement cases share structural similarities: AFS licence failures tied to net tangible asset breaches, personalised pressure on retail clients, and criminal proceedings following civil enforcement, a sequence the Berndale Capital Securities collapse and subsequent guilty plea of Stavro D’Amore traced in detail.

By the time the Federal Court delivered its liability judgment in December 2024, both TradeFred and Union Standard were already in liquidation or administration.

The $300.2 million headline and the amount harmed investors can realistically recover are two different figures. Civil penalties against insolvent entities deliver deterrence and public accountability. They do not function as a compensation mechanism. Combined client losses exceeded $83 million, but the insolvency of two of the three defendants severely constrains what can be returned to those who lost money.

Regulatory enforcement provides accountability after harm occurs. The most effective protection for retail investors remains front-end caution rather than reliance on enforcement outcomes to recover losses after the fact.

Each of the warning signs below is drawn directly from conduct the Federal Court identified in this case, not from generic risk disclaimers.

The 95-99% client loss rate in this case is an extreme figure, but it reflects a structural reality of retail CFD trading that extends beyond these specific firms. The three risk dimensions this case illustrates, market risk, conduct risk, and structural risk, apply to every provider relationship a retail CFD trader enters.

The $300.2 million in penalties represents the most severe financial consequence ASIC has ever secured. The case establishes that AFS licensees cannot insulate themselves from the conduct of their authorised representatives, that B-book business models combined with pressure selling and vulnerable clients attract maximum enforcement responses, and that cross-border client legal exposure is now a conduct obligation with real penalty consequences.

ASIC’s increasing use of civil penalty proceedings and expanding application of the EHF obligation signals a materially stricter regulatory environment for CFD issuers than existed a decade ago. The 13 July 2026 stay deadline marks the formal end of this penalty chapter.

Client misclassification penalties have become a recurring feature of ASIC’s Federal Court enforcement program, with Binance Australia Derivatives ordered to pay $10 million in March 2026 after 524 retail investors were illegally classified as wholesale clients, a separate conduct vector from the unlicensed advice and pressure selling seen in the EuropeFX matter but one that carries equivalent enforcement consequences.

The structural risks the case exposed, however, remain present in the retail CFD market. For retail investors, the most durable protection is not the prospect of enforcement after losses have occurred, but the front-end scepticism and due diligence that might prevent those losses in the first place.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

On 11 June 2026, Australia's Federal Court ordered $300.2 million in civil penalties against Union Standard International Group, EuropeFX, and TradeFred, representing the largest monetary sanctions ever connected to an ASIC enforcement matter, following findings of systemic unconscionable conduct, misleading conduct, and unlicensed personal advice.

B-book dealing is a CFD provider model where the firm takes the opposite side of every client trade, meaning the provider profits directly when clients lose money. In this case, the court found that this structural conflict underpinned the entire sales and advice strategy at EuropeFX and TradeFred, where between 95% and 99% of retail clients lost money.

Recovery is severely constrained because both TradeFred and Union Standard International Group entered liquidation or administration before the penalty orders were issued, meaning the $300.2 million headline figure does not translate into a realistic compensation pool for the more than $83 million in combined client losses.

Key warning signs identified by the court include persistent calls urging deposits after losses, suggestions to fund trading via superannuation or credit cards, personalised trading recommendations from staff without verified AFS authorisation, and any discouragement from raising formal complaints.

You can confirm the AFS licensee name and licence number on ASIC's public register, verify whether the entity you are dealing with is the licensee itself or an authorised representative authorised for personal advice, and review ASIC's published enforcement notices for that licensee before committing any funds.