What Domino’s Q1 Results Reveal About the Consumer Spending Slowdown

15 hrs ago

In March 2026, Saba Capital Management offered to buy shares in a private credit fund at a 33.2% discount to their stated value. Fewer than 1% of shareholders accepted.

That near-total refusal tells one story. The fact that Saba made the offer at all tells another. The OBDC II tender offer episode is a precise diagnostic of how liquidity risk accumulates inside private credit vehicles marketed to everyday investors, and why institutional players are now circling those positions. What follows maps Saba Capital’s strategy, explains the structural conditions in private credit that make it viable, walks through the OBDC II episode as a detailed case study, and translates all of it into practical implications for retail investors who may hold exposure to similar vehicles.

$3.80 per share: Saba Capital’s tender offer price for OBDC II, a 33.2% discount to the fund’s stated net asset value.

Saba Capital has not stumbled into a single discounted trade. The firm has built an entire thesis around a structural feature of the private credit market: that retail investors in non-traded funds frequently have no efficient way out.

The strategy is systematic. Saba targets private credit fund shares trading at 30-40% below net asset value (NAV), specifically in vehicles where secondary market exit routes for retail holders are constrained or absent. In March 2026, alongside Cox Capital Partners, the firm launched an unsolicited tender offer for up to 8 million shares of Blue Owl Capital Corporation II (OBDC II), less than 7% of the fund’s outstanding shares, at $3.80 per share.

The approach positions Saba as a liquidity provider of last resort, stepping in where fund-controlled redemption windows are the only formal exit mechanism. The strategy only works if retail investors are genuinely constrained. The illiquidity of these vehicles is the precondition, not incidental background. If a sophisticated hedge fund is pricing these assets at 30-40% below stated value, that gap is worth interrogating.

U.S. retail investors access private credit primarily through three vehicle types:

The scale of retail exposure is considerable. The total U.S. private credit market stands at approximately $1.7 trillion as of early 2026, with semi-liquid vehicles (interval funds and non-traded BDCs) comprising roughly 14% of assets under management.

Each of these structures promises some form of periodic access to capital. The underlying assets, direct loans and private lending positions, may take years to monetise. That tension between the liquidity the fund offers and the liquidity the assets actually provide is where the structural risk lives.

The vehicle structures that carry private credit risks for retail investors, interval funds, non-traded BDCs, and perpetually non-traded BDCs, each embed a version of the same core tension: the fund promises periodic liquidity while the underlying loan book operates on a fundamentally different timeline.

A redemption gate activates when investor withdrawal requests exceed a threshold percentage of the fund’s NAV within a given period. Once triggered, the fund caps total redemptions and investors join a queue with no guaranteed timeline for exit.

The timing compounds the problem. Adverse market conditions increase investor demand for redemptions at precisely the moment funds are least able to sell underlying assets without accepting steep losses. The gate tightens when pressure is highest.

The structural risks outlined above are not theoretical. Q1 2026 produced documented evidence across the sector.

In March 2026, BlackRock capped withdrawals from its $26 billion HPS Corporate Lending Fund, one of the largest private credit vehicles of its kind. The decision sent a signal well beyond a single fund, reinforcing concerns about redemption pressure across the broader private credit industry.

The picture extends further. Across perpetually non-traded BDCs, Q1 2026 saw widespread redemption caps that effectively constrained over $4.6 billion in investor capital. Private credit fund shares have been trading at steep discounts on secondary markets, underscoring the structural liquidity gap for retail investors seeking exits outside of fund-controlled windows.

Sector-wide redemption gating across major private credit funds extends well beyond the BlackRock HPS event; simultaneous gate triggers at Blue Owl, Blackstone, and Ares in Q1 2026 confirm that the liquidity mismatch the current article describes is not isolated to a single manager or fund structure.

| Fund / Entity | Event | Scale |

|---|---|---|

| BlackRock HPS Corporate Lending Fund | Capped withdrawals, March 2026 | $26 billion fund |

| Perpetually non-traded BDCs (sector-wide) | Redemption caps triggered, Q1 2026 | $4.6 billion+ in capital constrained |

| OBDC II (Saba Capital tender offer) | Unsolicited tender at 33.2% discount, March 2026 | Up to 8 million shares targeted |

Fitch Ratings assigned a “deteriorating” sector outlook for perpetually non-traded BDCs in 2026, citing negative net flows and rising redemption caps across the sector.

The accumulation of these signals, a major institutional fund capping withdrawals, billions locked sector-wide, and a ratings agency formalising its concern, confirms that the liquidity mismatch is manifesting in real investor accounts.

The sequence of the OBDC II episode is instructive:

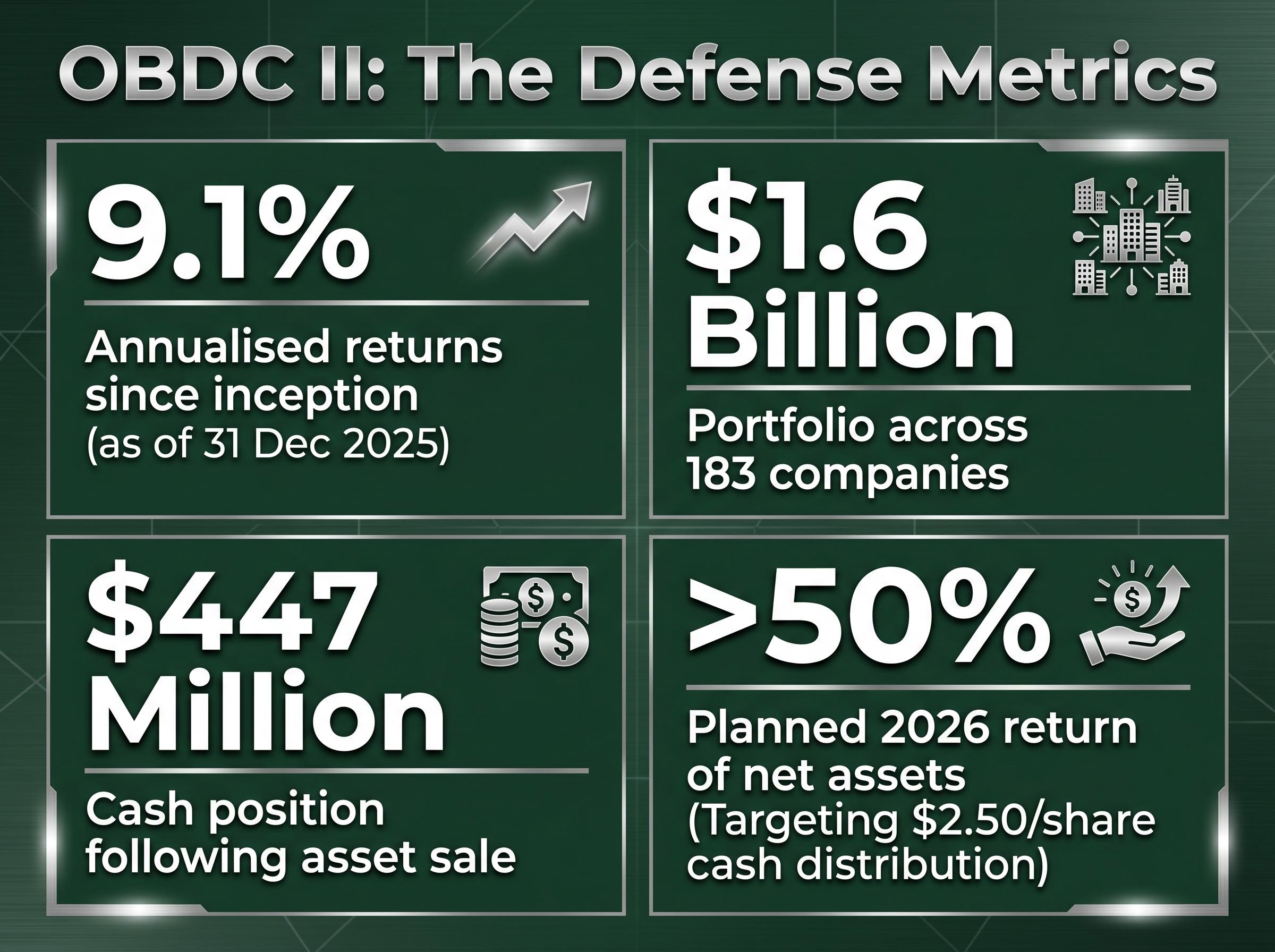

The fund’s counter-argument carried weight. OBDC II reported 9.1% annualised returns since inception (as of 31 December 2025), a $1.6 billion portfolio across 183 companies, and $447 million in cash following an asset sale. The board presented shareholders with a clear case that holding was rational.

The OBDC II outcome reflected a specific set of favourable conditions: a responsive board, active distributions, transparent performance data, and a cash position that made the distribution plan credible. Shareholders had the information needed to reject a deeply discounted exit.

Not all funds will present those conditions. Where boards are slower to act, distributions are suspended, redemption queues are long, and investor communications are opaque, the calculus shifts. Saba Capital’s broader thesis depends on conditions varying across the sector, not being uniform. The OBDC II rejection is a data point about what happens when a fund works well, not a refutation of the structural vulnerability the strategy targets.

Retail investors in private credit vehicles can apply a concrete framework to assess their own exposure. Three questions matter most:

In October 2025, LODAS Markets expanded its secondary marketplace through a partnership with CAIS, creating a practical liquidity path for financial advisers and their clients in alternative investments, including private credit. The marketplace remains early-stage and thinly traded relative to the capital locked in these vehicles, but it represents one of the more concrete infrastructure developments in this space.

The risk calculus is not straightforward. Private credit can generate strong returns; OBDC II’s 9.1% annualised performance since inception demonstrates this. The illiquidity is not inherently a flaw. It is a design feature that enables the yield premium these vehicles offer. The question is whether investors are genuinely comfortable with constrained exit options, particularly if they may need liquidity in the near term.

An SEC proposal in February 2026 to reduce reporting burdens for fund portfolio holdings could affect the transparency available to retail holders, making independent due diligence more important rather than less.

The SEC Form N-PORT proposed rulemaking on portfolio holdings disclosure, released in February 2026, would shift public reporting of fund portfolio positions from monthly back to quarterly, a change that reduces the granularity of data available to retail investors assessing the composition of their private credit holdings.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Saba Capital’s strategy is a rational institutional response to a structural design feature of private credit vehicles: the liquidity mismatch built into the product. That framing matters. The firm is not exploiting an anomaly; it is pricing a feature that retail investors may not have fully considered when they entered these positions.

The OBDC II outcome demonstrates that retail investors are not helpless when they are informed and when funds act transparently. A functioning fund with active distributions and a responsive board gave shareholders the information to reject a 33.2% discount. That near-total rejection, however, also required an unusually proactive board response.

Fitch’s deteriorating outlook, the BlackRock withdrawal cap, and $4.6 billion in constrained capital across the sector confirm that the stress conditions Saba Capital is positioning for are not hypothetical. They are current. Retail investors in these vehicles should treat liquidity risk as a first-order consideration, not a disclosure footnote buried in the offering documents.

Investors wanting to understand why institutional buyers like Saba consistently price these assets at 30-40% below stated values will find our full explainer on private credit NAV valuation gaps, which covers the GP-controlled valuation models that allow reported NAV to diverge from market prices, the 2026 maturity wall forcing concrete price discovery, and the SEC enforcement actions targeting advisers who misapplied their own stated valuation policies.

Past performance does not guarantee future results. Financial projections and forward-looking statements in this article are subject to market conditions and various risk factors.

Private credit liquidity risk refers to the difficulty of exiting positions in private credit vehicles such as non-traded BDCs and interval funds, because the underlying loan assets cannot be quickly sold. Retail investors may find redemption windows capped or queued, meaning they cannot access their capital when needed.

In March 2026, Saba Capital and Cox Capital Partners made an unsolicited offer to buy up to 8 million shares of Blue Owl Capital Corporation II at $3.80 per share, a 33.2% discount to the fund's stated net asset value. Fewer than 1% of shareholders accepted, largely because OBDC II's board responded with a credible distribution plan and transparent performance data.

A redemption gate activates when investor withdrawal requests exceed a set percentage of the fund's NAV in a given period, causing the fund to cap total redemptions and place investors in a queue with no guaranteed exit timeline. This typically occurs during periods of market stress, precisely when investors most want to exit.

Investors should check three things: the fund's redemption window and notice period, whether the fund has triggered its redemption cap in the past 12 months, and the current length of the redemption queue. These factors indicate how easily capital can be accessed if liquidity is needed.

Sector-wide stress is significant: BlackRock capped withdrawals from its $26 billion HPS Corporate Lending Fund in March 2026, and perpetually non-traded BDCs collectively constrained over $4.6 billion in investor capital during Q1 2026. Fitch Ratings also assigned a deteriorating outlook to the sector, citing negative net flows and rising redemption caps.