What Domino’s Q1 Results Reveal About the Consumer Spending Slowdown

15 hrs ago

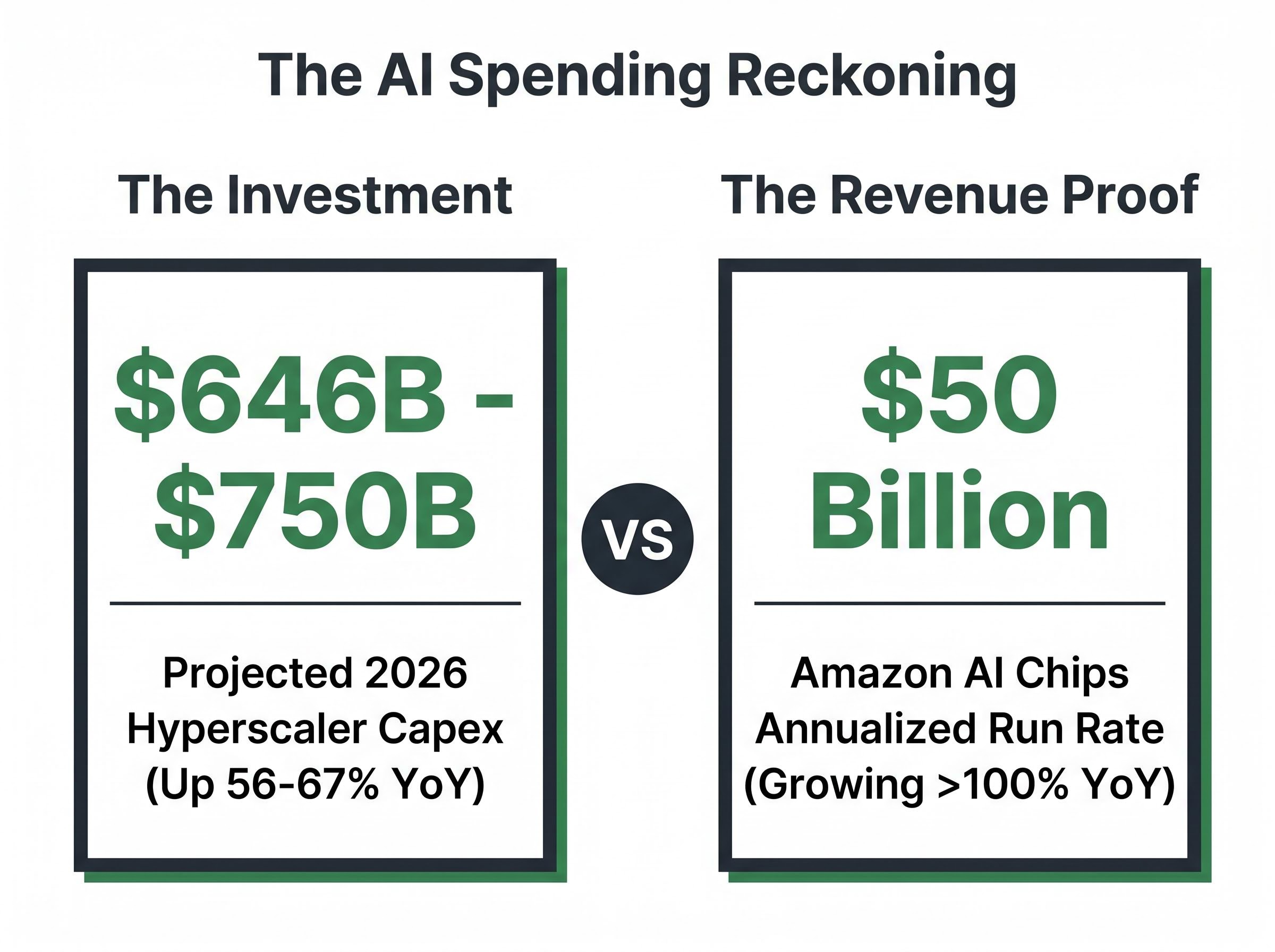

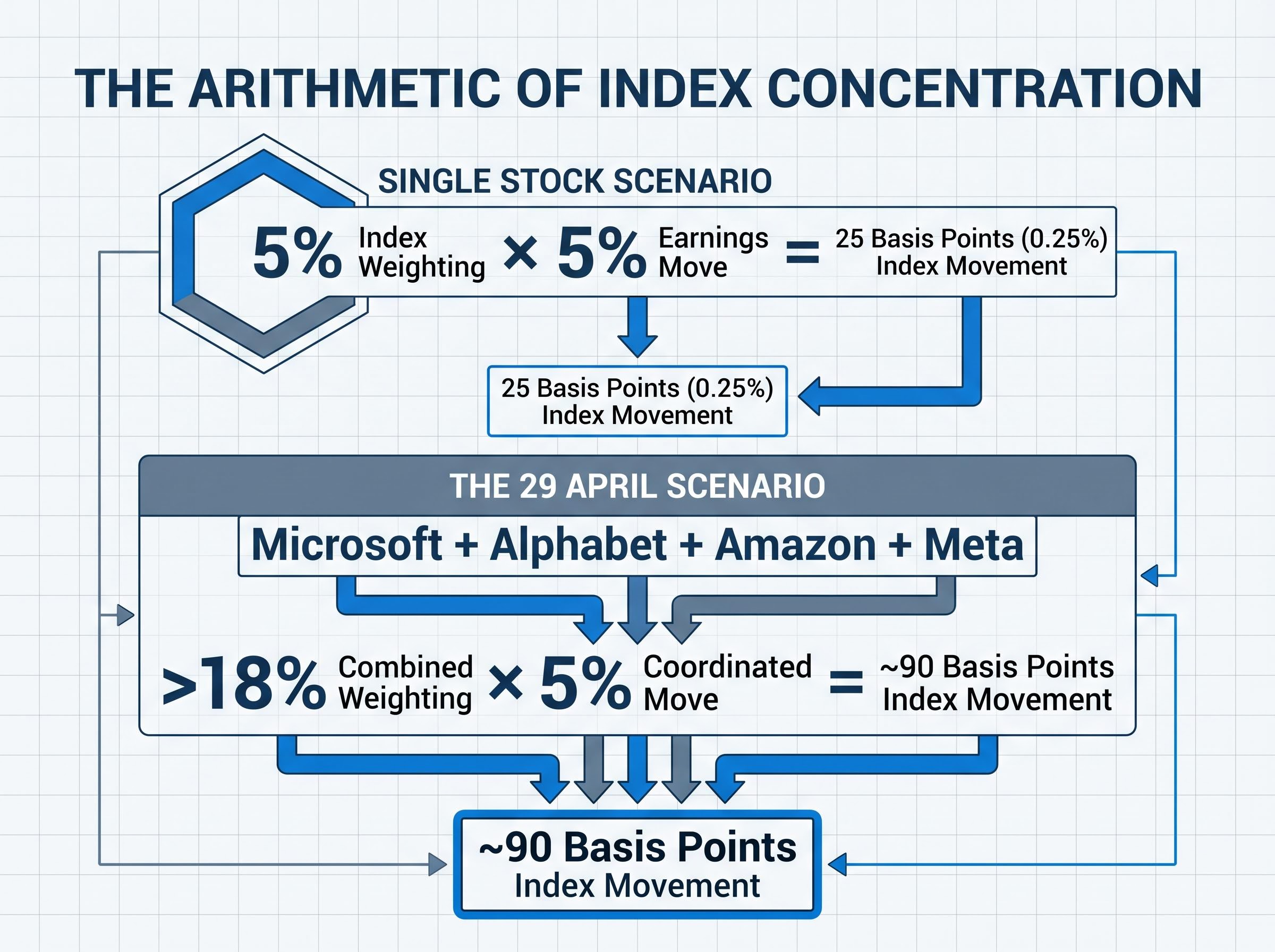

“`json { “fact_checked_full_article”: “Four of the most heavily weighted companies in the S&P 500 report earnings on the same day this week, and the combined result could shape the direction of U.S. equities for the remainder of the quarter. Microsoft, Alphabet, Amazon, and Meta all release Q1 2026 numbers after the close on Tuesday, 29 April. Together, these four names account for more than 18% of the S&P 500’s market capitalisation, meaning the after-hours session that follows will carry index-level consequences for any investor holding a broad U.S. equity fund. With blended S&P 500 earnings growth tracking at approximately 15.1% through 24 April and aggregate hyperscaler capital expenditure projected between $646 billion and $750 billion for 2026, the central question is no longer whether these companies are spending on artificial intelligence. It is whether that spending is converting into revenue. What follows is a breakdown of what analysts expect from each company, the macro risks that could complicate strong results, and the specific signals to watch when the numbers arrive.\n\n## Why 29 April is the most consequential earnings day of the year\n\nHaving four Magnificent Seven constituents report on the same calendar day is historically unusual. It concentrates index-level risk into a single after-hours window, and the arithmetic alone explains the stakes.\n\n> Combined S&P 500 weighting: Microsoft, Alphabet, Amazon, and Meta together represent more than 18% of the index. A collective miss or beat does not stay contained to four stock charts; it ripples mechanically into index funds, 401(k) balances, and broadly diversified portfolios.\n\nThe broader earnings season is providing a supportive backdrop. S&P 500 Q1 blended earnings growth sits at approximately 15.1% on 9.7% revenue growth as of 24 April, with Q2 2026 consensus already pointing to +20.6% earnings growth. The Magnificent Seven group is expected to outperform both figures materially, with consensus net income growth of roughly 25% for the full year.\n\n- Microsoft: Reports 29 April; Azure AI growth rate and Copilot monetisation are the primary watch items\n- Alphabet: Reports 29 April; Google Cloud AI revenue and the expanded Anthropic partnership announced 22 April set the narrative\n- Amazon: Reports 29 April; AWS AI services uptake and the credibility of the $200 billion capex plan are in focus\n- Meta: Reports 29 April; operating margin trajectory post-layoffs and the new Muse Spark AI platform frame the dual cost-discipline and investment story\n\nQ1 2026 functions as a gut check. Investor attention has shifted from raw AI spending totals to demonstrable returns on that capital, and the $646-$750 billion in projected 2026 hyperscaler capex demands evidence that revenue is following the investment.\n\n## What the numbers show: analyst expectations for all four companies\n\nConsensus estimates heading into the 29 April reports reveal a group delivering strong revenue growth, but with a widening gap between top-line expansion and bottom-line delivery in several cases.\n\n

| Company | EPS Consensus | Revenue Consensus | YoY Revenue Growth | Key Pre-Earnings Development |

|---|---|---|---|---|

| Microsoft | $4.04-$4.06 | $81.4B | ~16-17% | Copilot standalone sales reportedly meeting aggressive internal targets |

| Alphabet | $2.67-$2.68 | $106.88-$107B | ~19-20.6% | Expanded Anthropic/TPU partnership announced 22 April |

| Amazon | $1.65 | ~$177B | ~14% | Globalstar acquisition ($10.8B) announced 14 April; AI chips business at $50B annualised run rate |

| Meta | $6.71 | $55.36-$55.57B | ~16% | ~8,000 layoffs announced ~24 April; Muse Spark AI platform launched in April |

\n

\n\n### Where the surprises might come from\n\nThe table tells the consensus story. The divergence risks sit underneath it. Meta’s revenue growth of roughly 16% is the strongest in the group, yet EPS growth tracks at only approximately 3%, a compression that reflects the scale of AI infrastructure investment eating into margins. Amazon faces a similar dynamic: 14% revenue growth paired with roughly 4% EPS growth, weighed down by its $200 billion 2026 capex plan and tariff exposure across its retail segment.\n\nAlphabet’s 22 April announcement of an expanded Anthropic and TPU partnership has lifted sentiment, but it also raises the bar for management to demonstrate that cloud AI partnerships are converting into product revenue, not just strategic positioning. Microsoft’s Copilot reportedly meeting aggressive internal sales targets, according to Bloomberg reporting, could provide the clearest near-term evidence that enterprise AI tools are generating incremental revenue at scale.\n\n## The AI spending reckoning: from capital expenditure to proof of returns\n\nThe investor psychology around AI spending has shifted decisively. Eighteen months ago, the market rewarded ambition. Companies that announced larger AI infrastructure budgets saw their share prices rise. That dynamic has inverted.\n\nThe market’s central question for all four companies reporting on 29 April is no longer whether they are investing in AI but whether that investment is generating measurable revenue and margin contribution. The combined $646-$750 billion in projected 2026 hyperscaler capex, up 56-67% year-over-year, demands justification.\n\nThree specific AI monetisation metrics will matter most across the four earnings calls:\n\n1. Azure AI growth rate (Microsoft): The single clearest read on enterprise AI adoption at scale, particularly when paired with Copilot product attach rates\n2. AWS AI annualised revenue run rate and Google Cloud AI product revenue (Amazon, Alphabet): Amazon’s AI chips business reportedly runs at a $50 billion annualised rate, growing over 100% annually; Alphabet’s expanded Anthropic partnership needs to show cloud revenue follow-through\n3. Meta ad-targeting return on investment from AI tooling (Meta): With ~8,000 layoffs signalling cost discipline, management needs to demonstrate that AI-driven advertising improvements are translating to measurable yield gains for advertisers\n\n> Amazon CEO Andy Jassy has characterised the stock’s post-capex-disclosure selloff as unwarranted, noting that customer commitments already cover nearly the full $200 billion capex plan. That claim will face its sharpest test on the earnings call. If management can substantiate it with specific contract or backlog data, it could recalibrate how the market prices AI infrastructure spending across the group.\n\nConsensus net income growth for the Magnificent Seven sits at approximately 25% for full-year 2026. Delivering on that figure requires AI capital expenditure to begin converting into visible revenue, and Q1 is where the conversion evidence either appears or does not.\n\n## Understanding index concentration risk: how four stocks can move the whole market\n\nMarket-cap-weighted indices allocate more weight to larger companies. The S&P 500 does not hold 500 equal slices; it holds 500 slices sized by market capitalisation. When a company grows large enough to command 4-5% of the index on its own, its earnings move the index mechanically.\n\nThe maths is straightforward. Consider the following illustrative scenario:\n\n- A stock with a 5% S&P 500 weighting moves 5% after earnings. That single stock contributes approximately 25 basis points (0.25%) of index-level movement.\n- If all four reporting companies (combined weighting above 18%) move 5% in the same direction, the index-level impact approaches 90 basis points before any broader market reaction.\n- Market concentration analysis from Capital Group has shown that Magnificent Seven earnings weeks have increasingly moved the broader index, amplifying individual company results into index-level events.\n\nThe post-1 April Nasdaq breakout reinforced institutional positioning in these names, meaning momentum and positioning effects could amplify the moves further.\n\n### What this means for index fund investors specifically\n\nS&P 500 index funds (SPY, VOO, IVV) carry the full concentration exposure described above. Nasdaq-100 funds (QQQ) carry even higher Magnificent Seven weighting than the broader index.\n\nThis is not a reason to avoid index funds. It is a reason to understand the headline risk that comes with concentrated earnings weeks. An investor who holds no individual Magnificent Seven positions but owns a standard index fund portfolio still has meaningful exposure to what happens after the bell on 29 April.\n\n## Macro headwinds that could complicate strong results\n\nStrong Q1 numbers may not automatically translate into post-earnings rallies. Several headwinds make \”beat and raise\” harder to achieve than the consensus estimates suggest.\n\n- Tariff exposure: Amazon’s retail segment faces direct margin pressure from the 2025-2026 tariff environment. Apple’s recent tariff-related stock pressure, with shares trading near period lows at points during the escalation, serves as a precedent for how tariff costs can overshadow otherwise solid fundamental results across Magnificent Seven names.\n- Regulatory overhang: Ongoing antitrust scrutiny across search (Alphabet), social media (Meta), and cloud services (Microsoft, Amazon) could surface in guidance language, particularly if management teams signal increased compliance costs or operational constraints.\n- Capex discipline signals: After months of rewarding spending announcements, the market now punishes capex plans that lack specific revenue commitments. Management commentary on Q2 and full-year spending discipline will be parsed closely.\n- Forward guidance tone: Tesla’s Q1 result illustrates the dynamic. The company beat on top-line revenue at $22.387 billion but the stock dipped on guidance concerns. Headline beats do not guarantee rallies when forward commentary disappoints.\n\nFor investors interpreting post-earnings price action on 30 April, the distinction matters. A stock that beats estimates but trades lower is often responding to guidance language on tariffs, capex trajectories, or macro outlook rather than the headline numbers themselves. Geopolitical volatility, including ongoing uncertainty around the Iran ceasefire, adds a background risk factor that could amplify negative reactions to any cautious guidance.\n\n## What to watch after the bell: the signals that will move markets on 30 April\n\nThe after-hours session on 29 April will deliver a high volume of data in a compressed window. Knowing which signals carry the most weight helps separate noise from signal in real time.\n\nThe single most important data point from each report:\n\n- Microsoft: Azure AI revenue growth rate and Copilot enterprise adoption metrics. Bloomberg reporting indicates Copilot standalone sales are meeting aggressive internal targets; confirmation on the call would be a positive catalyst.\n- Alphabet: Google Cloud AI product revenue and any update on the Anthropic investment trajectory. Alphabet holds a 14% stake, with an additional $40 billion investment reportedly planned and a potential Anthropic IPO in 2026.\n- Amazon: AWS AI annualised revenue run rate and the credibility of capex guidance. Management needs to substantiate the claim that customer commitments cover the $200 billion plan.\n- Meta: Operating margin trajectory following the ~8,000 layoffs announced around 24 April, paired with any early monetisation signals from the Muse Spark AI platform launched in April.\n\nSeven investor watch points for the 29 April calls:\n\n1. Management guidance language on AI revenue conversion, moving from capex spend to revenue attribution\n2. Azure, Google Cloud, and AWS growth rates; any deceleration would be a significant negative signal\n3. Meta’s cost structure post-layoffs and operating leverage trajectory\n4. Tariff impact quantification, particularly for Amazon’s retail segment\n5. Copilot, Gemini, and AI product adoption metrics, including enterprise attach rates\n6. Capex guidance for Q2 and full-year 2026\n7. Advertising market health signals from Meta and Alphabet as proxies for broader digital ad spending\n\n> The stakes for the 2026 AI thesis: Collective beats accompanied by raised guidance would reinforce the AI investment case and likely support the S&P 500 on 30 April. A pattern of beats paired with cautious guidance, or missed revenue in one or more names, would test recent market highs and raise questions about whether the 2026 tech rally has fundamental support beneath it.\n\n## What it all means for investors\n\nFour companies representing more than 18% of the S&P 500 report on the same day, making 29 April one of the highest-stakes single sessions in the 2026 earnings calendar. The revenue growth expectations are strong across the group, but the market’s real test lies deeper: whether $646-$750 billion in projected AI capital expenditure is converting into durable revenue and margin expansion.\n\nInvestors do not need to own any of these four stocks individually to be affected. Broad index fund holders carry direct exposure through market-cap-weighted concentration.\n\nThe watch-point framework above provides a structure for interpreting the after-hours results as they arrive. Look beyond headline EPS to guidance language on AI monetisation, tariff cost impact, and Q2 forward estimates. The morning of 30 April will tell investors a great deal about whether the 2026 tech rally is built on fundamental evidence or forward-looking optimism that still needs to be earned.\n\nThis article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.\n\n—” } “`

For investors wanting to understand the post-earnings positioning debate in detail, our full explainer on SocGen’s hyperscaler free cash flow warning covers Societe Generale’s projection that hyperscaler FCF turns negative by late 2026 before recovering in Q1 2027, including the specific capex-to-revenue ratio signals that Manish Kabra has identified as the confirmation threshold for re-entering technology equities.

The Magnificent Seven concentration inside broad index funds is more pronounced than most investors appreciate: despite VTI holding approximately 3,500 stocks, its top 10 holdings account for 31.60% of the portfolio, with Nvidia, Apple, and Microsoft alone representing 16.7% of the fund’s total weight.

Investors focused purely on headline EPS risk misreading the results: how accelerated depreciation suppresses reported earnings is the mechanical story beneath the numbers, with each new tranche of infrastructure spend adding to a compounding depreciation base that appears on the income statement years before revenue attribution catches up.

The revenue-to-earnings divergence across all four companies has a structural explanation: successive depreciation cycles from AI infrastructure investment compound on reported profits even as top-line growth accelerates, a dynamic that Societe Generale has warned could push hyperscaler free cash flow negative by late 2026 before any recovery.

the DOJ’s landmark antitrust ruling against Google, confirmed in April 2025, established a legal precedent with direct implications for Alphabet’s advertising and search operations, meaning any guidance language on compliance costs or structural remedies on the 29 April call will carry weight beyond a single quarter’s results.

FactSet’s S&P 500 earnings season update for April 24, 2026 confirms blended Q1 earnings growth of approximately 15.1% on 9.7% revenue growth, with Q2 2026 consensus already pointing to 20.6% earnings expansion, providing the aggregate benchmark against which the Magnificent Seven’s projected 25% net income growth will be measured.

The magnificent seven earnings preview refers to the collective analyst expectations for the largest U.S. mega-cap tech companies ahead of their quarterly results. On 29 April 2026, four of these companies, Microsoft, Alphabet, Amazon, and Meta, report simultaneously, representing more than 18% of the S&P 500 by market capitalisation, meaning their results carry index-level consequences for any broad equity fund holder.

All four companies report after the market close on Tuesday, 29 April 2026, making it one of the most concentrated earnings events in recent history and a key date for investors tracking the 2026 AI spending narrative.

Because the S&P 500 is market-cap weighted, a stock with a 5% index weighting that moves 5% after earnings contributes approximately 25 basis points of index-level movement. If all four reporting companies move 5% in the same direction, the combined index impact could approach 90 basis points, directly affecting holders of funds such as SPY, VOO, and IVV without them owning any individual stock.

The three most important signals are Azure AI revenue growth and Copilot enterprise attach rates from Microsoft, AWS and Google Cloud AI annualised revenue run rates from Amazon and Alphabet, and Meta's operating margin trajectory following its roughly 8,000 layoffs alongside any early monetisation data from its Muse Spark AI platform.

Yes. Tesla's Q1 2026 result demonstrated this dynamic: the company beat on top-line revenue at $22.387 billion but the stock dipped on guidance concerns. Investors will be scrutinising forward commentary on tariff cost impact, capex discipline, and AI revenue conversion rather than headline EPS figures alone.