How Dual-Class Shares Put $24 Billion in Gulf Capital at Arm’s Length

15 hrs ago

Private credit default rates reached a record 9.2% in 2025. Yale sold $3 billion in private equity stakes. Harvard unloaded another $1 billion. The institutions that built the playbook on alternative assets are quietly changing course, and the timing is not coincidental.

For more than a decade, private equity and private credit were positioned as the sophisticated investor’s edge: higher returns, lower correlation to public markets, and access reserved for the patient and well-connected. That narrative is now under sustained pressure. Bankruptcy filings among private credit-backed companies are mounting, valuation concerns are surfacing at systemic scale, and the liquidity structures sold as manageable are proving otherwise when tested.

What follows is a plain-terms explanation of how private equity and private credit actually work, where the structural risks sit, what the institutional retreat signals about forward conditions, and what any investor encountering these vehicles through retirement funds or direct platforms needs to understand before committing capital.

Two asset classes dominate the alternatives conversation, and both share structural features that make them simultaneously attractive and risky. Understanding the mechanics of each is necessary before any discussion of what can go wrong.

Private equity involves pooled capital raised by a general partner (GP) and deployed to acquire or invest in private companies. Returns are generated through operational improvement, financial engineering (typically adding debt to amplify equity returns), and eventual sale or initial public offering (IPO).

The standard fund operates on a 7-10 year cycle. Capital is called from limited partners (LPs) in tranches as deals are identified, and returns are distributed only when portfolio companies are sold or taken public. There is no real-time market price for these holdings. The fee structure follows the “2 and 20” model: a 2% management fee on committed capital (charged from commitment, not deployment) and 20% carried interest on profits above a hurdle rate.

Private credit grew substantially after the 2008 financial crisis as banks tightened lending under stricter regulation, creating a vacuum that unregulated lenders moved to fill. Private credit funds lend directly to companies that cannot access conventional bond markets or bank financing, positioning themselves as a yield-generating alternative to traditional fixed income.

The distinguishing feature is structural: private credit operates outside the regulatory framework governing banks. Borrower creditworthiness is not assessed by independent rating agencies. There is no standardised disclosure or prudential oversight equivalent to what applies to bank lending.

The key structural features of each asset class sit side by side:

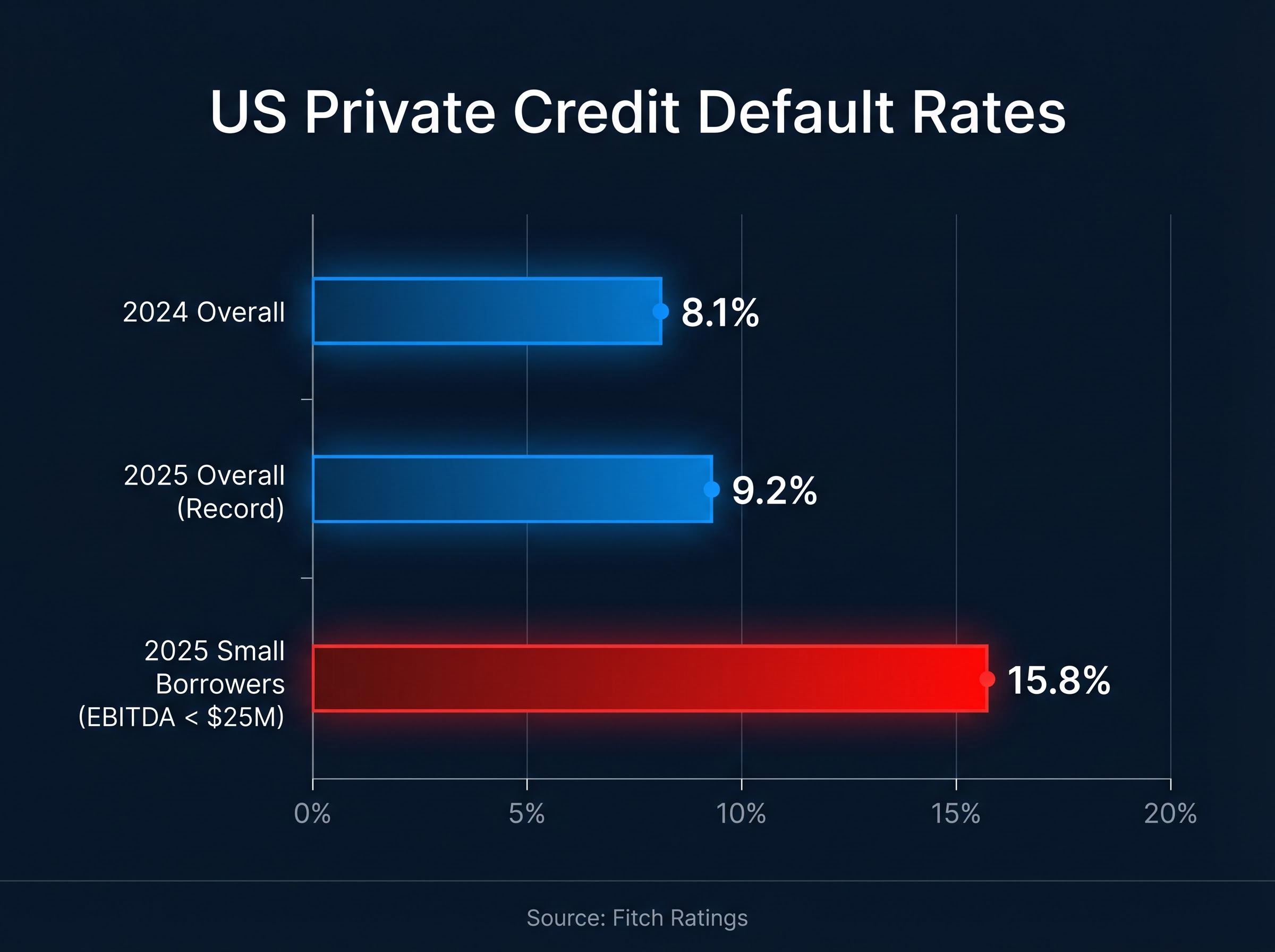

Fitch Ratings reported that US private credit defaults hit a record 9.2% in 2025, up from 8.1% in 2024. That headline number is concerning on its own. Where the defaults are concentrated tells a sharper story.

Companies with EBITDA under $25 million experienced a 15.8% default rate in 2025, nearly double the overall rate, according to Fitch Ratings.

The pattern is not random. PE-backed companies carry significantly higher debt loads than publicly traded peers. That leverage amplifies returns when revenue grows and interest rates cooperate. When either condition reverses, the same structure amplifies losses.

Federal Reserve Board research on private equity leverage and portfolio company distress finds that PE-owned companies carry substantially higher debt burdens than comparable publicly traded peers, a structural characteristic that amplifies both upside returns and downside losses when interest rates rise or earnings soften.

The causal chain follows a predictable sequence:

Named examples make this concrete. Envision Healthcare, a physician staffing company acquired by KKR in a leveraged buyout, filed for bankruptcy after its debt burden became unsustainable. Big Lots, a discount retailer backed by private capital, followed a similar trajectory. According to S&P Global Market Intelligence, US portfolio company bankruptcies totalled 66 in 2025, down from 81 in 2024, but rising “shadow” defaults (distressed restructurings conducted outside formal bankruptcy) indicate that headline figures understate the actual stress.

When investors chase yield through private credit vehicles, they are often taking on the credit risk of the most leveraged, least creditworthy segment of the corporate market. That context changes how the yield premium should be evaluated.

There is a second structural risk that operates independently of leverage, and it is arguably more difficult for investors to detect. Unlike public equities, where prices are set by independent market transactions every trading day, private assets are valued using internal models controlled by the GP.

McKinsey estimated approximately $6 trillion in unrealised private equity value potentially at risk of overstatement due to inflation and interest rate pressures.

That figure represents the gap between what fund statements show and what the market might actually pay. For any investor relying on private fund net asset value (NAV) figures to make allocation decisions, the mechanics behind those numbers matter.

EY reported increased scrutiny on earnings management during fundraising periods, noting that GP-controlled valuations create incentive misalignment. A GP raising its next fund has a material interest in showing strong, stable returns in the current fund. The valuation models that produce those returns are not independently verified by market transactions.

The Securities and Exchange Commission (SEC) intensified enforcement actions targeting private fund valuation practices in 2024-2025 and moved toward enhanced disclosure requirements for private fund advisers, including more granular reporting on fees, conflicts of interest, and valuation methodologies.

The SEC Division of Examinations 2026 priorities for private fund advisers explicitly target valuation of illiquid assets, fee calculation accuracy, and conflict-of-interest disclosures, placing private equity and credit managers under direct regulatory focus at precisely the moment when valuation opacity has become a systemic concern.

The following table contrasts how valuation works across public and private markets:

| Feature | Public equity | Private equity |

|---|---|---|

| Pricing mechanism | Market price (buyer-seller transactions) | GP internal model (“mark-to-model”) |

| Frequency | Real-time, continuous | Quarterly or less frequent |

| Independence | Independent (set by market participants) | Internally controlled by the GP |

| Transparency | Fully visible to all market participants | Disclosed to LPs on GP’s schedule |

| Regulatory oversight | SEC-regulated exchanges | Limited; SEC increasing scrutiny |

When a public stock falls 20%, the fund statement reflects that decline immediately. Every investor can see the loss in real time. When a private portfolio company deteriorates by the same amount, the GP updates its internal valuation model on its own schedule, which may lag reality by quarters or even years.

This does not necessarily mean fraud. It means that reported returns in private markets are smoother and more stable-looking than they may actually be. A private equity fund can report steady, low-volatility returns during a period when the underlying companies are experiencing genuine financial stress, simply because the valuation model has not yet caught up.

This feature makes private assets appear lower-risk than they are when measured by volatility, which is part of why they appeal to institutional allocators targeting risk-adjusted returns. The smoothness is a feature of the valuation methodology, not necessarily a reflection of the underlying reality.

The institutional retreat from private equity is real, but it is not universal, and the distinction matters. The sellers and the buyers are making rational decisions based on different constraints.

Yale explored selling up to $6 billion in PE stakes in 2025, ultimately finalising approximately $3 billion in secondary market sales at minimal discount. Harvard sold approximately $1 billion in PE holdings to boost liquidity and rebalance its $53 billion endowment. Both moves were driven by concerns over illiquidity and over-allocation relative to portfolio targets.

At the same time, the Washington State Investment Board (WSIB) maintained one of the largest public pension PE programmes in the country. As of year-end 2025, WSIB held $52 billion in private equity (approximately 22.6% of assets under management) with $17 billion in unfunded commitments. The PE portfolio generated a 9.6% annual return in 2025, yielding approximately $5.7 billion in net capital, though management fees totalled approximately $862.3 million in the same year.

The tension within the Washington programme is instructive. State Treasurer Mike Pellicciotti dissented on all new PE and credit recommendations at the April 2026 board meeting, citing concern over undue risk from over-reliance on private equity. WSIB’s target allocation was reduced from 25% to 23% in late 2024.

| Institution | Action taken | Scale | Stated rationale |

|---|---|---|---|

| Yale University | Secondary market PE sales | ~$3B finalised | Illiquidity concerns, portfolio rebalancing |

| Harvard University | PE holdings sale | ~$1B | Liquidity, endowment rebalancing |

| Washington State (WSIB) | Reduced target allocation; internal dissent | $52B portfolio, target cut from 25% to 23% | Over-reliance risk, fee burden, dissenting vote |

Several other states have also moved to reduce PE exposure:

The signal is worth careful examination rather than dismissal. When the most sophisticated long-term capital allocators in the world are reducing exposure, and an elected state official is publicly dissenting on new commitments, the conditions that justified aggressive allocation over the past decade may be shifting.

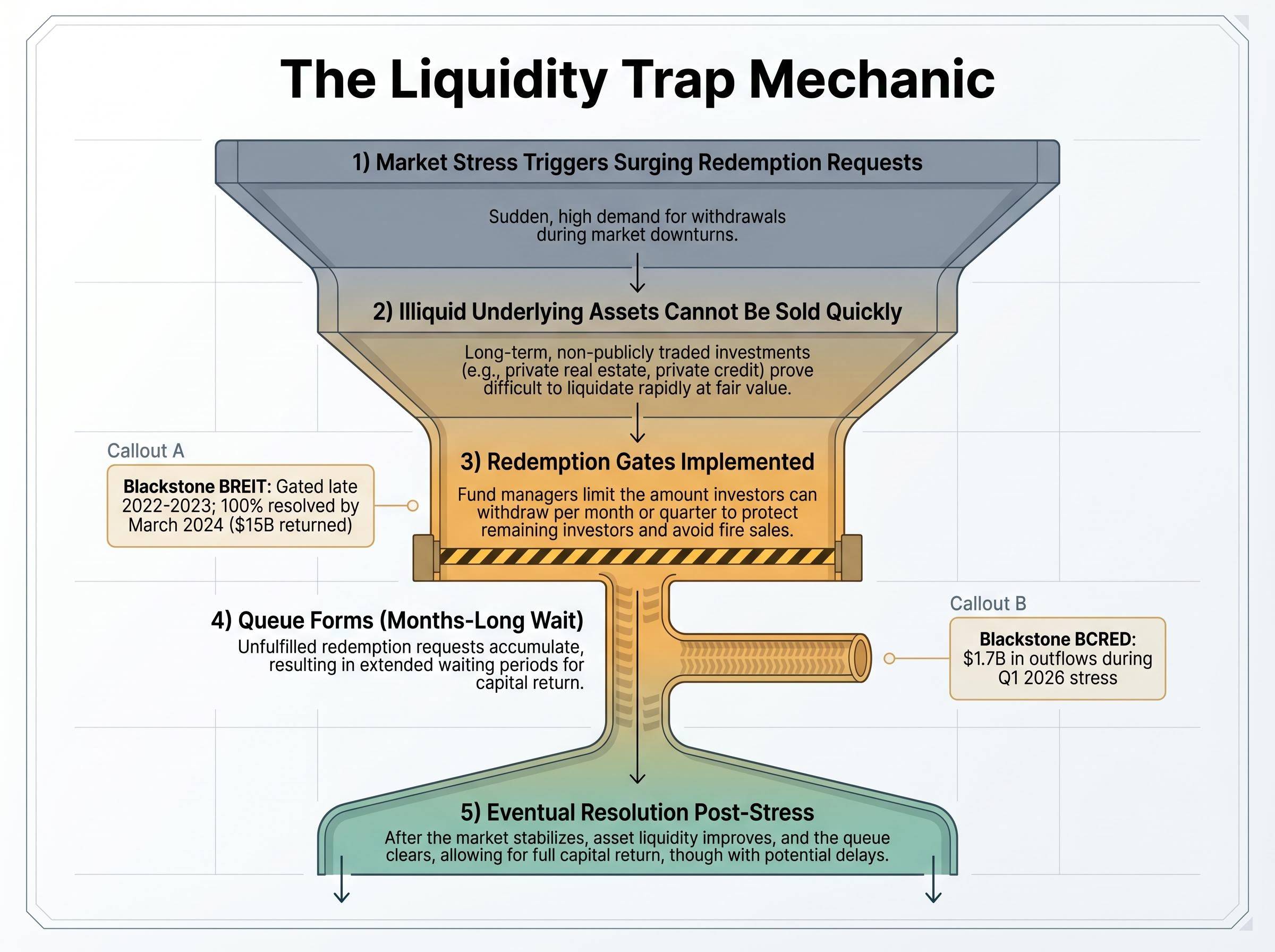

The promise was compelling: access to institutional-quality returns, previously reserved for endowments and pension funds, now available to individual investors through non-traded REITs, interval funds, and semi-liquid vehicles. The democratisation of alternative investments expanded access, but it did not change the underlying liquidity structure of the assets.

Blackstone’s BREIT, a non-traded real estate investment trust, demonstrated what happens when that mismatch is tested. After investor redemption requests surged in late 2022, BREIT implemented redemption gates that remained in place through 2023. The fund eventually met 100% of redemption requests by March 2024, returning approximately $15 billion to investors, but the experience for investors who needed liquidity during the gating period was materially different from what the prospectus language may have suggested.

The pattern resurfaced in 2026. Blackstone’s BCRED, a private credit vehicle, experienced approximately $1.7 billion in outflows in Q1 2026, driven by credit market stress. The sequence of events in these episodes follows a recognisable pattern:

“Retail investors face structural disadvantages relative to institutional investors when seeking liquidity during volatile markets.”

A secondary market for PE stakes exists, but it transacts at discounts. Yale’s sales finalised at minimal discount only because of its elite market position and the quality of its portfolio. Most retail investors would not command similar terms.

Publicly traded closed-end fund structures represent one approach to the liquidity problem that non-traded vehicles cannot solve: a secondary market exists by design, prices are set by independent transactions every trading day, and investors who need to exit can do so without triggering a redemption gate, though closed-end funds can and do trade at persistent discounts to their underlying net asset value.

Private equity and private credit offer genuine potential advantages: a yield premium over public fixed income, portfolio diversification, and return potential that has historically rewarded patient capital. Those advantages are real, but they are inseparable from three structural risks that are often underappreciated until they materialise.

The leverage risk is visible in a record 9.2% default rate and a 15.8% default rate among the smallest borrowers. The valuation opacity risk sits in an estimated $6 trillion in potentially overstated unrealised value. The liquidity risk was demonstrated in real time through the BREIT and BCRED episodes, where investors discovered the distance between prospectus terms and practical experience.

The institutional retreat is not a verdict on the entire asset class. It is a signal that even the most sophisticated allocators are recalibrating after a decade of aggressive expansion. As regulatory scrutiny increases, secondary market activity normalises, and default rates remain elevated, investors at every level are better served by understanding the mechanics than by relying on marketing narratives.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The three core private equity risks are leverage risk (portfolio companies carry high debt loads that amplify losses when earnings fall or interest rates rise), valuation opacity risk (GPs control their own internal pricing models rather than relying on independent market prices), and liquidity risk (capital is locked up for 7-10 years with limited ability to exit early without accepting significant discounts).

Fitch Ratings reported that US private credit defaults hit a record 9.2% in 2025, up from 8.1% in 2024, driven primarily by heavily leveraged smaller companies. Companies with EBITDA under $25 million experienced a 15.8% default rate, nearly double the overall rate, as rising interest costs and softer earnings made debt servicing unsustainable.

Yale finalised approximately $3 billion in secondary market PE sales in 2025, and Harvard sold around $1 billion in PE holdings, both citing illiquidity concerns and the need to rebalance their endowment portfolios back toward target allocation levels.

Mark-to-model means a private equity fund's portfolio companies are valued using internal models controlled by the general partner rather than by independent market transactions, which means reported returns can appear smooth and stable even when underlying companies are experiencing genuine financial stress. McKinsey estimated approximately $6 trillion in unrealised private equity value may be at risk of overstatement due to inflation and interest rate pressures.

Investors should confirm how and when capital can actually be accessed, who controls the valuation process, the full fee structure including how carried interest is calculated, and whether a secondary market exists for the position and at what typical discount it transacts. The BREIT and BCRED episodes illustrate that prospectus terms and practical liquidity experience can differ significantly during periods of market stress.