SpaceX’s Real Business Model Goes Far Beyond Rockets

4 hrs ago

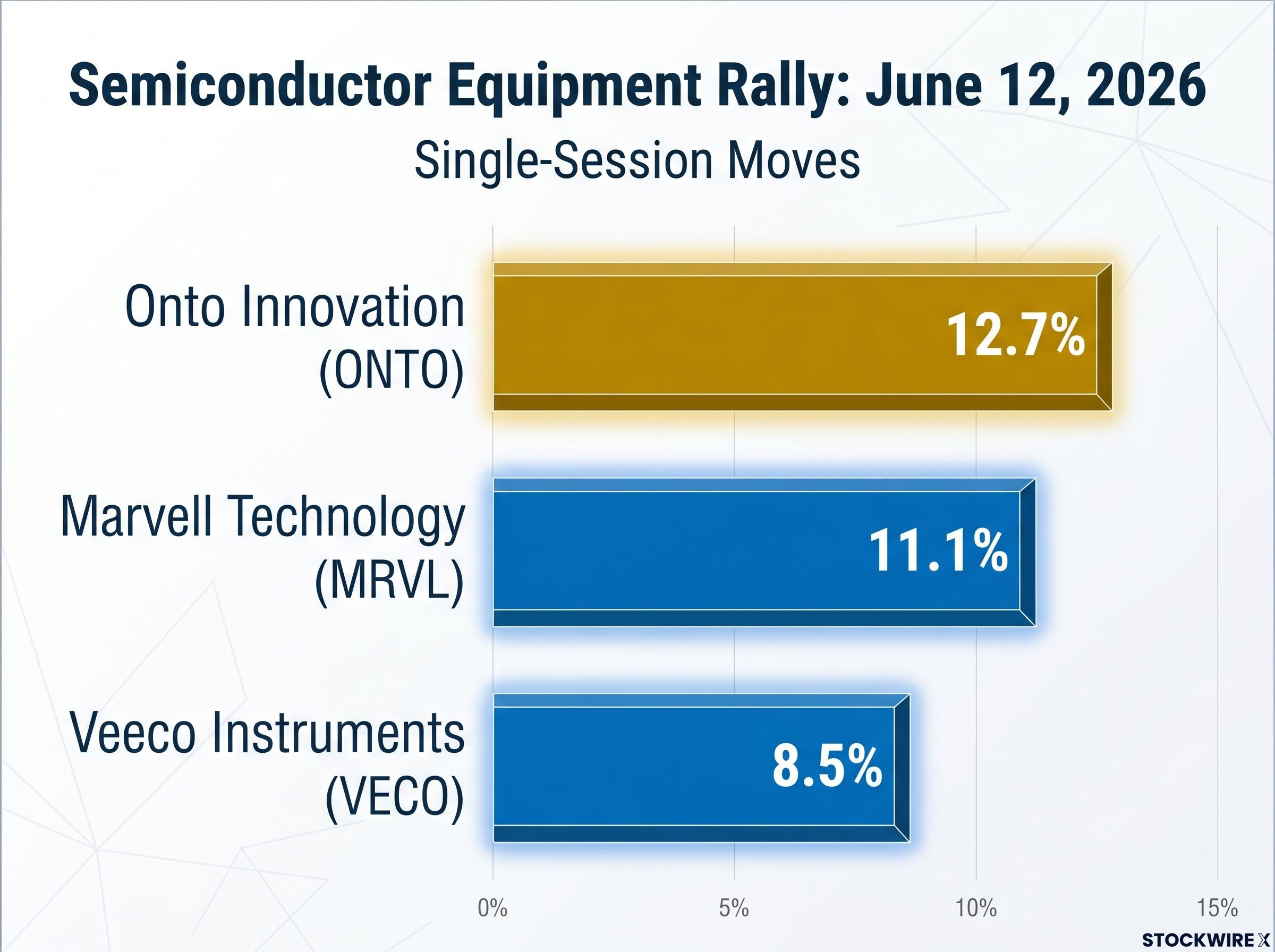

On 12 June 2026, a semiconductor equipment company most retail investors had never encountered surged approximately 12.7% in a single session, capping a 144% run over the prior twelve months. Wall Street’s highest price target sat at $350 per share. The company was Onto Innovation (NYSE: ONTO), and it does not design chips or run hyperscale data centres. It builds the inspection and metrology tools that catch defects in AI accelerator packages before they become billion-dollar write-offs. As TSMC scales its 2.5D advanced packaging lines to meet AI compute demand, the tools Onto sells have become structurally non-negotiable in the supply chain. This analysis breaks down what drove the ONTO move, why the fundamentals justified it, how an AI model flagged the opportunity before the breakout, and what risks investors should monitor before acting.

The session itself was decisive but not isolated. Onto Innovation climbed approximately 12.7% on 12 June 2026, one of the largest single-session moves across the semiconductor equipment space. It was not alone. The broader market rallied across sectors including healthcare, energy, financials, and industrials, with President Trump’s cancellation of planned military action against Iran providing a risk-on backdrop. Within the semiconductor equipment cohort, the leadership cluster was specific:

That peer grouping is telling. Three names tied to the AI hardware supply chain moved in tandem, signalling institutional conviction in the picks-and-shovels layer, not a random spike in a single ticker.

Onto Innovation’s trailing twelve-month gain of approximately 144%, with a year-to-date gain of approximately 87%, places the 12 June session as an acceleration of an ongoing trend, not the start of one.

The distinction matters for position sizing and entry timing. Investors evaluating ONTO are not looking at a trade that has already happened. They are looking at the continuation of a structural repricing.

Onto Innovation was formed in 2019 through the merger of Rudolph Technologies and Nanometrics. It occupies the inspection, metrology, and process control layer of the semiconductor supply chain, a segment that sits between wafer fabrication and final chip assembly. Its tools detect defects at extremely fine geometries, both in front-end wafer processing and in advanced packaging structures.

That distinction, process control rather than chip design, is what makes the company easy to overlook and difficult to replace.

Advanced packaging structures such as 2.5D CoWoS (chip-on-wafer-on-substrate) and high-bandwidth memory stacks are the primary mechanisms by which NVIDIA, AMD, and other accelerator designers increase compute density without waiting for new process nodes. These structures layer multiple chiplets and memory dies into a single package, and any defect at this stage is catastrophically expensive.

The average selling price of an AI accelerator makes each defective package a disproportionate loss relative to the cost of the inspection step itself. This makes process control spend a fixed cost of doing business at advanced nodes, not a variable line item that gets trimmed in a down quarter.

TSMC’s CoWoS capacity expansion roadmap projects CoWoS and SoIC capacities growing at 80% and 90% CAGR respectively through 2027, a supply ramp that makes embedded process control suppliers like Onto structurally indispensable to every wafer-out target TSMC intends to hit.

Once a tool is qualified and embedded in a process recipe, swapping vendors mid-ramp is prohibitively risky. That creates durable switching costs, and it is the foundation of the bull case for Onto’s revenue visibility.

The AI supply chain capex cycle that underpins Onto’s revenue ramp is larger than most retail investors appreciate: the four largest US hyperscalers are on track to commit a combined $630 to $725 billion to AI infrastructure in 2026 alone, and foundries plus their qualified equipment vendors sit at a structurally protected layer of that spend because every custom and third-party AI chip depends on the same fabrication ecosystem.

Crossing a billion dollars in annual revenue is partly symbolic. It changes where a company sits in institutional portfolio mandates, analyst coverage universes, and index eligibility screens. For Onto Innovation, the $1.005 billion in full-year 2025 revenue was that threshold.

The mechanics beneath the milestone matter more than the headline. Onto is a semiconductor capital equipment company with high fixed costs in R&D, engineering, and support infrastructure. Once revenue clears the breakeven level, incremental dollars flow disproportionately to the bottom line. That is why earnings growth of approximately 27% outpaced revenue expansion, a direct consequence of operating leverage rather than cost-cutting.

| Metric | Value | Period | Significance |

|---|---|---|---|

| Full-year revenue | $1.005 billion | FY 2025 | First time crossing the $1B threshold |

| Q4 revenue | $266.87 million | Q4 2025 | Record quarterly revenue |

| Q2 2026 guidance | $320-$330 million | Q2 2026 | Sequential acceleration, not deceleration |

| Earnings growth | ~27% | Trailing estimate | Outpacing revenue; reflects operating leverage |

Q2 2026 guidance of $320 million to $330 million confirms the ramp is continuing. The revenue trajectory is not flattening after the milestone; it is steepening, which is consistent with a TSMC advanced packaging ramp entering volume production.

In April 2026, TSMC’s New Tool Selection Committee approved Onto Innovation’s next-generation Dragonfly G5 inspection platform for use in 2.5D advanced packaging production lines. Stifel’s research note covering the qualification was explicit: the broader market had not fully priced this event despite its full public disclosure.

Stifel characterised the Dragonfly G5 qualification as “a core catalyst the market missed,” raising the ONTO price target from $220 to $350 and upgrading the stock to Buy.

The Dragonfly G5 product line was projected to grow over 50% during the current year, driven specifically by the TSMC qualification. Stifel’s framing tied the platform directly to TSMC’s advanced packaging roadmap, positioning Onto as a direct equipment lever on the world’s most advanced AI chip packaging ramp.

This was not a cold commercial relationship. TSMC’s own award history corroborates a sustained, multi-year partnership:

That timeline reframes the Dragonfly G5 qualification. It is not a new vendor winning a trial. It is a deeply embedded supplier receiving confirmation that its next-generation platform will carry through the most significant packaging ramp in the industry’s history.

The InvestingPro AI model flagged Onto Innovation prior to its price surge. The identification was not a single insight. It was the convergence of three discrete, publicly available signal categories:

Every input was public. The TSMC qualification was disclosed. The Stifel target revision was published. The $1 billion revenue milestone was reported in earnings filings. Stifel’s own research note explicitly acknowledged that the Dragonfly qualification appeared underappreciated by the broader market despite being fully available.

The edge was not access to non-public information. It was the ability to weight multiple public signals simultaneously and without behavioural bias. A multi-factor model that treats established momentum as confirmation, recognises a gap to upgraded targets, and understands what a TSMC advanced packaging qualification implies for multi-year tool demand could flag ONTO while the sell-side itself was still calling the catalyst underpriced.

Semiconductor equipment peer valuations have been under active revision across the cycle, with ASML’s premium over US peers collapsing from a 10-year average of 84% to roughly 6-15% by mid-2026, a compression that reflects both China export control headwinds and a market still recalibrating which equipment suppliers capture the most durable margin from the AI packaging ramp.

The Dragonfly G5 growth projection of over 50% is tied specifically to a single customer qualification. That is both the thesis and its primary vulnerability.

Risk-aware investors who identify the specific monitoring variables, TSMC packaging capex guidance, Dragonfly G5 quarterly shipment rates, Taiwan geopolitical developments, can hold the position with discipline rather than reacting to price volatility.

The Onto Innovation case is instructive because the pattern is repeatable. The stock’s repricing followed a specific configuration:

The same AI infrastructure buildout that drove ONTO is still expanding. The broadening of equity leadership from mega-cap semiconductors like NVIDIA into suppliers such as ONTO, VECO, and MRVL is consistent with prior cycle dynamics. Once the core theme is established and the headline names are priced for it, capital rotates into the picks-and-shovels layer where operational torque is higher.

Picks-and-shovels AI suppliers have been the standout performers of 2026, with five infrastructure names at least doubling in the first five months of the year while hyperscalers absorbed the bulk of institutional attention, a pattern that mirrors the rotation dynamic described in Onto’s trailing twelve-month run.

The question to apply to other names is specific: does this company have a qualification event with a major customer, an analyst re-rating with a substantial gap to target, and a momentum profile that suggests systematic buying? If all three are present, multi-factor models are likely already building positions.

Onto Innovation’s 144% trailing twelve-month run was not a speculative spike. It was the market repricing a fundamental shift in who captures value from AI infrastructure spending, specifically the process control suppliers that are structurally embedded in TSMC’s packaging ramp. The Dragonfly G5 qualification, the $1 billion revenue milestone, and the Stifel target revision to $350 were all public. The edge was in synthesising those signals before the broader market acted on them.

What has changed since the AI model identified the opportunity is that the stock is now widely covered, the catalyst is reflected in the current price, and the thesis shifts from “undiscovered” to “monitor execution against elevated guidance.” Investors who want to apply the same systematic, multi-factor approach to finding the next ONTO before its breakout may find value in exploring what AI-driven stock screening tools can surface across the semiconductor supply chain.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results.

Onto Innovation builds inspection and metrology tools that detect defects in semiconductor packages before they become costly failures. Its tools are embedded in TSMC's 2.5D advanced packaging lines, which are the primary structures used to increase compute density in AI accelerators from companies like NVIDIA and AMD.

The 12 June 2026 surge reflected a combination of a broader risk-on market rally following the cancellation of planned US military action against Iran and sustained institutional conviction in AI hardware supply chain names, with ONTO, MRVL, and VECO all moving sharply higher together as a peer group.

The Dragonfly G5 is Onto Innovation's next-generation inspection platform, which was approved by TSMC's New Tool Selection Committee in April 2026 for use in 2.5D advanced packaging production. Stifel projected the product line would grow over 50% in the current year and raised its ONTO price target from $220 to $350, calling the qualification a core catalyst the market had missed.

The three primary risks are customer and node concentration (the Dragonfly G5 growth projection is tied specifically to TSMC's packaging ramp), semiconductor equipment cyclicality (even strong beneficiaries experience drawdowns when capex cycles turn), and elevated valuation expectations where any guidance shortfall could trigger outsized price declines.

The InvestingPro AI model converged on three publicly available signals: sustained price momentum consistent with institutional accumulation, a measurable gap between the share price and Stifel's revised $350 target, and the Dragonfly G5 TSMC qualification as a structural revenue catalyst. Every input was publicly disclosed; the advantage was in weighting multiple signals simultaneously without behavioural bias.