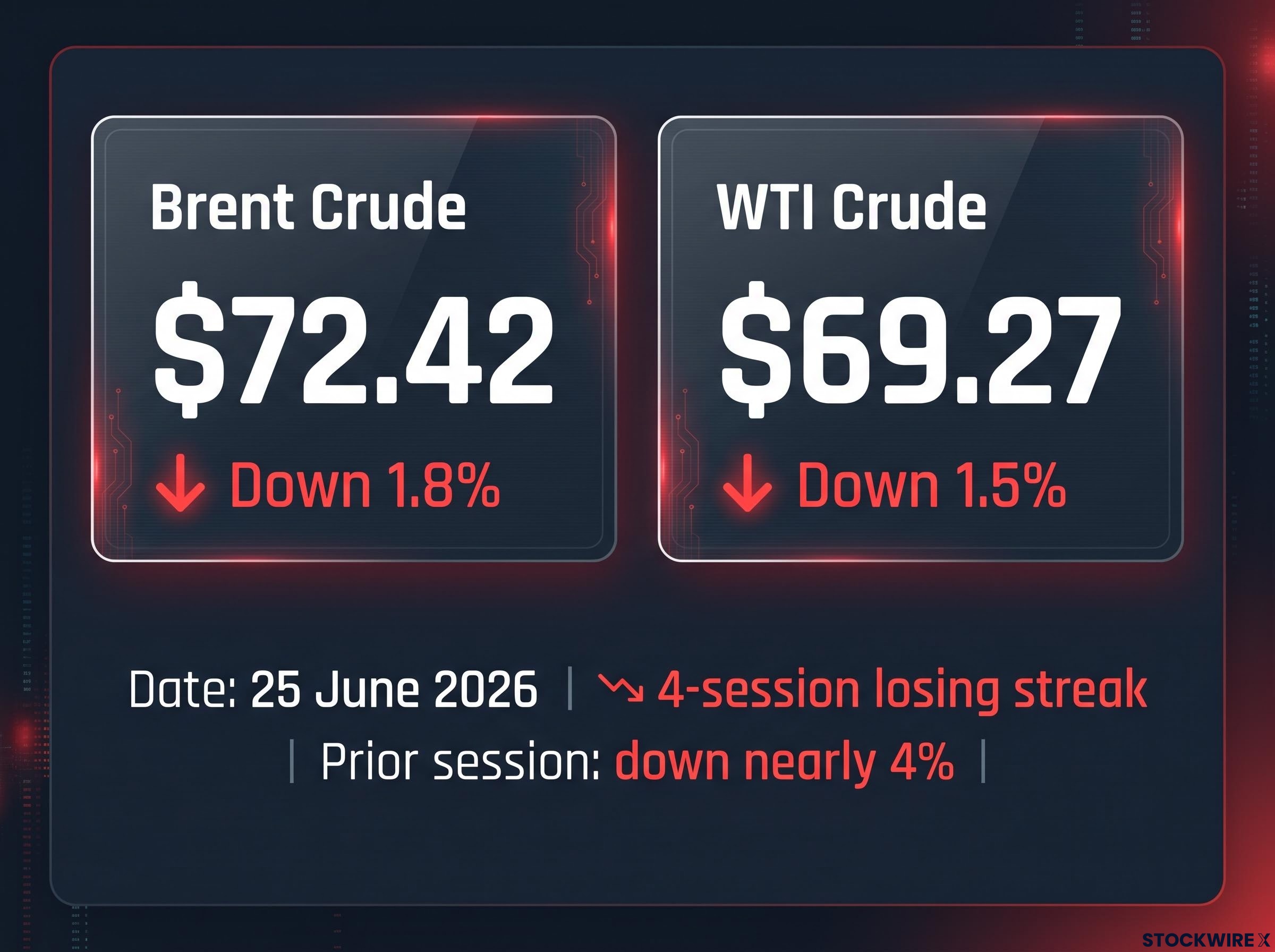

Brent crude fell to $72.42 and WTI slipped to $69.27 on 25 June 2026, extending a four-session losing streak that has now erased every dollar of the conflict-era run-up. The entire geopolitical risk premium that built during peak U.S.-Iran tensions is gone.

That alone would be a commodity story. But the same morning, the PCE price index, which serves as the Federal Reserve’s primary benchmark for tracking inflation, was due for publication at 08:30 ET. When oil prices fall at the same time as a high-stakes inflation print lands, the implications reach well beyond the energy sector and into rate expectations, equity valuations, and household budgets.

Here is what the price action means, why it happened, and how to position around it before the picture settles.

Four sessions, one complete reversal: what the oil price data actually shows

The numbers tell the story before any analyst needs to weigh in.

- Brent crude: $72.42 per barrel, down 1.8% on 25 June 2026

- WTI crude: $69.27 per barrel, down 1.5% on 25 June 2026

The session prior saw a decline of nearly 4%, the steepest single-day drop in the sequence. Across four consecutive sessions, both benchmarks have now reversed all gains accumulated during the period when fears of a supply disruption through the Strait of Hormuz were at their peak.

The four-session cumulative decline has fully erased the conflict-era premium. Pricing has returned to levels consistent with normal supply and demand conditions, stripped of crisis-era fear.

This was not a gradual drift lower. It was a rapid, near-complete reversal of a specific fear-driven premium, which tells you something precise about how markets priced the conflict risk in the first place: as a probability, not a certainty, and one that evaporated fast once conditions shifted.

Brent and WTI have now returned to the conflict-era baseline of approximately $72-74 per barrel from which the Iran-driven surge originally launched, a level that, as analysts noted at the time, reflected normal supply and demand conditions before the Strait of Hormuz closure introduced a structural shock of unprecedented modern scale.

When big ASX news breaks, our subscribers know first

What a geopolitical risk premium is and why it collapses so fast

A geopolitical risk premium is the extra price markets charge for crude to account for possible supply disruption. It reflects fear, not actual barrels removed from the market. When tensions escalate near a chokepoint that handles a significant share of global oil flows, traders price in worst-case scenarios. When those scenarios become less likely, the premium disappears, often faster than it built.

Why the Strait of Hormuz makes markets nervous

The Strait of Hormuz is a narrow waterway through which roughly one-fifth of globally traded oil transits. That concentration of supply through a single physical chokepoint means that even a credible threat of disruption, without a single tanker being stopped, is enough to embed a premium into global crude prices.

EIA data on Hormuz oil transit confirms that roughly 20 million barrels per day moved through the strait in 2024, equivalent to approximately 20% of global petroleum liquids consumption, which is why even a credible threat to that corridor is sufficient to embed a substantial premium into global crude benchmarks.

The current unwind traces to two proximate causes:

- Tanker and cargo movements through the Strait have picked up, pointing to a return to normal physical supply conditions

- Diplomatic talks have moved forward in a way that has lowered the market’s assessed probability of further escalation

For you, the practical lesson is this: waiting for a formal resolution before acting on oil price signals is the wrong framework. The market prices probability, not outcomes. The premium can be fully priced out well before a ceasefire is signed.

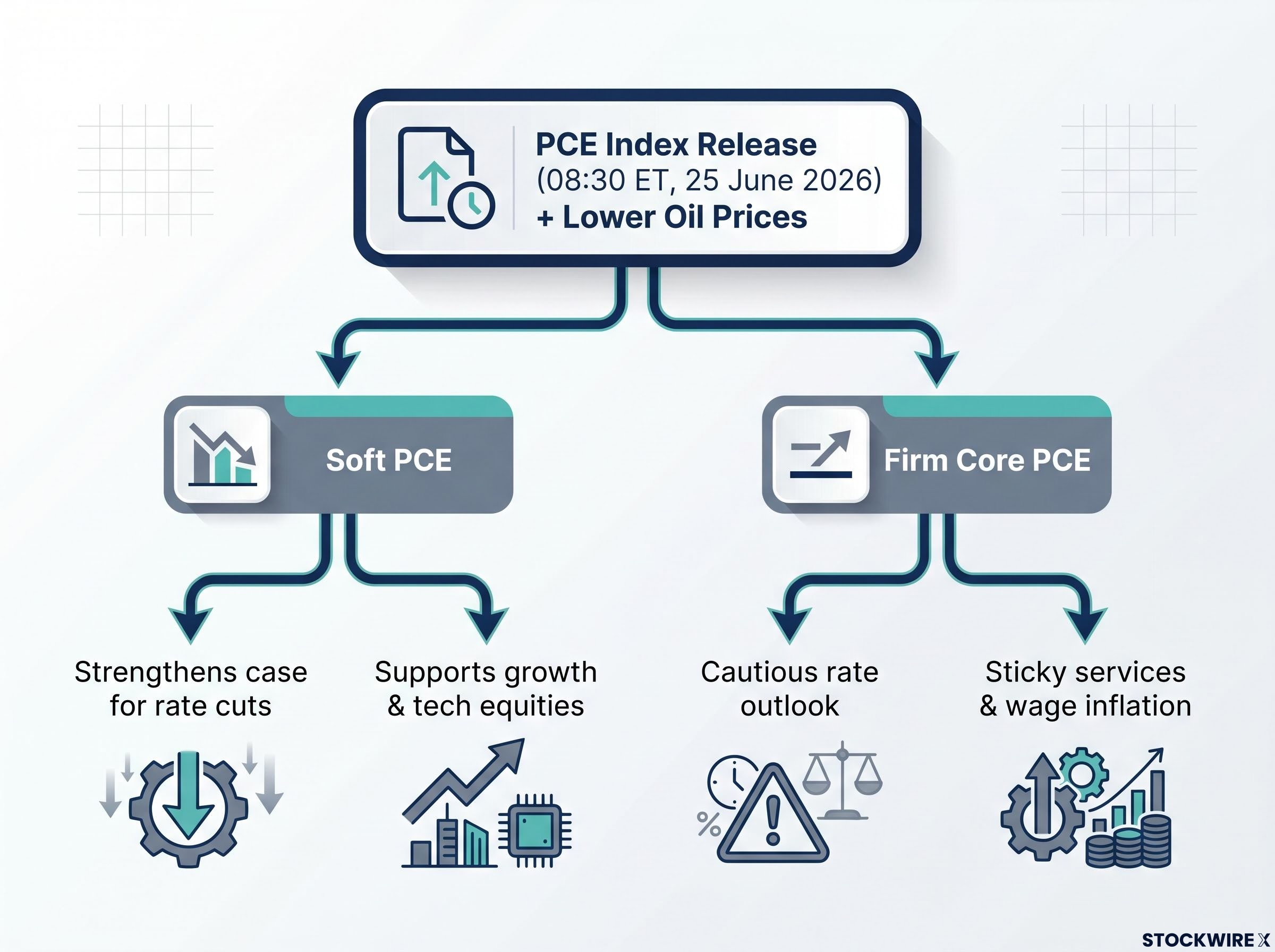

The PCE collision: why today’s inflation print makes the oil move matter more

Two independent data events arrived on the same morning and interact to produce a more consequential macro signal than either would generate alone.

The PCE price index, the Federal Reserve’s primary inflation gauge, was scheduled for release at 08:30 ET on 25 June 2026. Traders and analysts had been watching closely for signs that price pressures were proving harder to bring down than the Fed had expected, giving this particular release outsized importance.

The oil decline sharpens the PCE’s significance because energy prices feed directly into headline inflation measures. Two scenarios frame what comes next:

The distinction between headline versus core inflation has been central to reading the conflict-era data correctly: headline CPI reached 4.2% year-over-year in May 2026 on a 40.5% annual gasoline surge, while core held at a comparatively contained 2.9%, confirming the price shock was geopolitical and supply-driven rather than a sign of broad domestic overheating.

| Scenario | Market Implication |

|---|---|

| Soft PCE + subdued oil prices | Strengthens the case for eventual rate cuts, supporting long-duration assets including growth and tech equities |

| Firm core PCE + lower oil | The Fed may treat cheaper oil as helpful but not decisive; sticky services and wage inflation keep the rate outlook cautious |

A soft PCE reading combined with subdued energy prices would represent the strongest near-term catalyst for rate-cut expectations, directly supporting equity valuations and easing borrowing costs across mortgages and credit cards.

The oil move alone does not determine the Fed’s direction. It is the combination of oil and core PCE that will shape rate expectations over the coming weeks, and positioning before that combination is clear carries meaningful uncertainty.

Who absorbs the hit and who gets the tailwind?

At approximately $69 WTI, most U.S. shale producers remain profitable, but margins compress meaningfully versus higher-price scenarios. The damage, however, is not uniform across the energy sector.

Dallas Fed Energy Survey breakeven data from the first quarter of 2026 provides granular well-level profitability thresholds across major shale plays, offering a baseline for assessing which operators retain positive free cash flow at current WTI levels and which face meaningful margin compression.

- Integrated majors may see upstream earnings weaken but can partially offset through downstream refining, where lower feedstock costs support margins

- Pure-play upstream producers face the most direct revenue compression, though lower-cost operators with strong balance sheets absorb it better

- Oilfield services firms are the most exposed if producers respond to lower prices by trimming capital expenditure

| Sector | Direction of Impact | Key Reason |

|---|---|---|

| Energy producers (upstream) | Negative | Direct revenue compression at lower crude prices |

| Oilfield services | Most negative | Exposed to producer capex cuts if lower prices persist |

| Airlines / transport / trucking | Positive | Fuel cost relief flows directly to margins |

| Consumer discretionary | Positive | Households retain more disposable income beyond fuel costs |

| Tech / REITs / small caps | Conditionally positive | Benefit indirectly if lower oil supports rate-cut expectations |

The distinction that matters for your positioning is whether this is a temporary normalisation of a fear premium or the beginning of a prolonged lower-price environment. The earnings damage to energy names is vastly different in each scenario, and the sectors that benefit only capture sustained tailwinds if cheap oil persists.

Five things investors should track before drawing conclusions

- Separate risk premium reversal from fundamental oversupply. The current move is primarily a fear premium unwinding, not a collapse in underlying demand. Watch inventory data, OPEC+ behaviour, and demand forecasts to gauge whether fundamentals are weakening too.

- Focus on the duration of lower prices. A brief dip has modest earnings impact for energy companies. Sub-$70 WTI sustained over multiple quarters would materially change free cash flow, buyback capacity, and capex plans across the sector.

- Track the PCE print and Fed communication. Soft PCE plus cheaper oil strengthens the case for a dovish pivot over time. Sticky core inflation reduces that case, even with energy relief.

- Be selective within energy. Favour lower-cost producers with strong balance sheets that remain profitable at lower prices. Scrutinise high-cost, leveraged names and capex-heavy projects if the market starts pricing in a lower-for-longer environment.

- Remember that headline risk is two-sided. Any renewed escalation near the Strait of Hormuz can rapidly re-inflate the risk premium and reverse the price move.

Two-sided headline risk in this market is not theoretical: JD Vance’s withdrawal from Geneva peace talks on 19 June sent Brent below $80 per barrel in a single session, demonstrating how quickly diplomatic setbacks can re-inflate premiums even after the market appears to have fully priced in a resolution.

Geopolitical risk premiums can evaporate swiftly, but they can return just as quickly. Any incident affecting Hormuz shipping lanes changes the calculus overnight, making a one-directional bet on lower oil a position with asymmetric downside that is easy to overlook.

Each of these items represents a specific variable you can monitor in real time, turning an abstract macro event into a personal watchlist that tells you when the thesis changes.

What stabilises from here and what remains unresolved

The market has shifted from pricing tail-risk disruption back toward baseline supply and demand conditions. Both benchmarks have effectively reversed all conflict-era gains as of 25 June 2026, and the repricing of fear is largely complete for now.

What remains genuinely open is a separate question. Four variables will determine whether the energy sector pain deepens or stabilises:

- Hormuz stability: Whether shipping lanes through the Strait remain clear and unimpeded

- Diplomatic resolution durability: Whether the momentum in negotiations is sustained or breaks down

- Core PCE trajectory: Whether inflation outside energy remains sticky enough to keep the Fed cautious

- OPEC+ response: Whether the group adjusts output targets in response to lower prices

The easy part of this repricing, removing the fear premium, is done. The harder question, where oil finds a fundamental floor, is what determines whether energy sector earnings compress further or begin to recover. Treat the oil move as a macro shock absorber for inflation and rates, but a valuation headwind for energy names unless crude stabilises and demand confidence holds.

For investors wanting to model where crude settles once the fear premium is fully stripped out, our full explainer on post-ceasefire oil price floors examines the structural forces, including mine-clearing lags, war-risk insurance timelines, and SPR replenishment demand, that are keeping WTI and Brent above pre-conflict levels even as the risk premium unwinds.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.