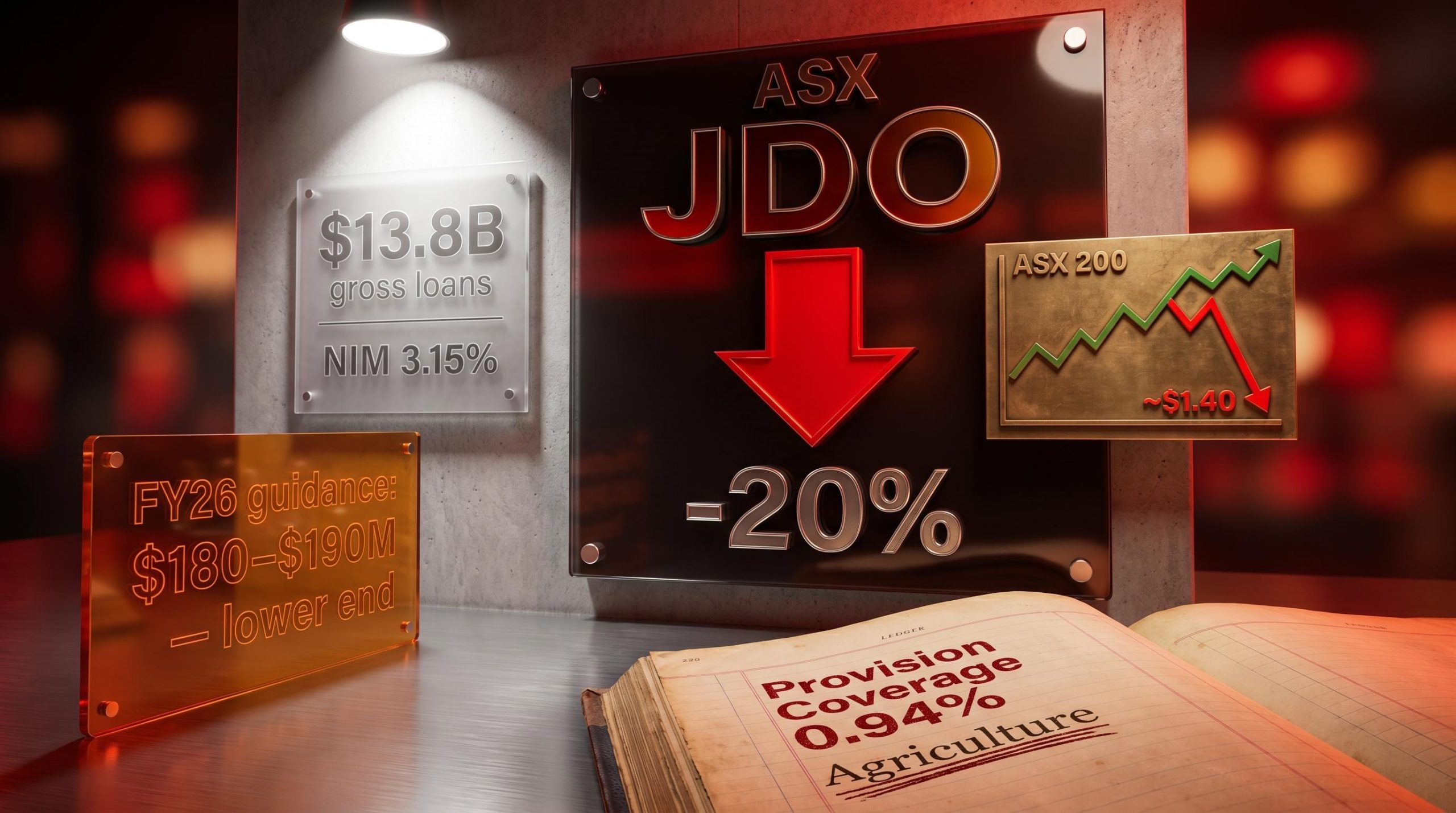

Judo Capital shares shed roughly 20% in a single session on 24 April 2026, one of the sharpest single-day declines the ASX-listed SME lender has experienced, despite management reaffirming its full-year profit guidance. The Q3 FY26 quarterly update, covering the period to 31 March 2026, landed as a mixed result: net interest margin improved materially, the loan book grew, and costs stayed on track. But an upward revision to collective provisions and a clear signal that profit would trend to the lower end of guidance unsettled the market.

What follows unpacks what the numbers actually show, why the market reacted so sharply, what brokers are saying now, and what the update means for investors evaluating JDO at current prices.

A 20% share price drop on a day guidance was reaffirmed

Single-session decline: approximately 20%, from a close of roughly $1.75 on 23 April to approximately $1.40 on 24 April 2026.

The scale of the selloff sits uncomfortably alongside the headline: FY26 profit guidance was technically intact. Both things are true, and the rest of this article explains why they are not contradictory.

The decline did not arrive in isolation. Over the trailing twelve months, Judo Capital shares have fallen approximately 21%, a period in which the S&P/ASX 200 gained roughly 10%. The Q3 update did not start the underperformance story; it accelerated it. For investors searching the Judo Capital share price after this session, the first task is understanding the gap between a guidance reaffirmation and a market that responded as though guidance had been cut.

When big ASX news breaks, our subscribers know first

What the Q3 numbers actually show

The quarterly update contained several data points moving in different directions. The table below captures the key metrics side by side.

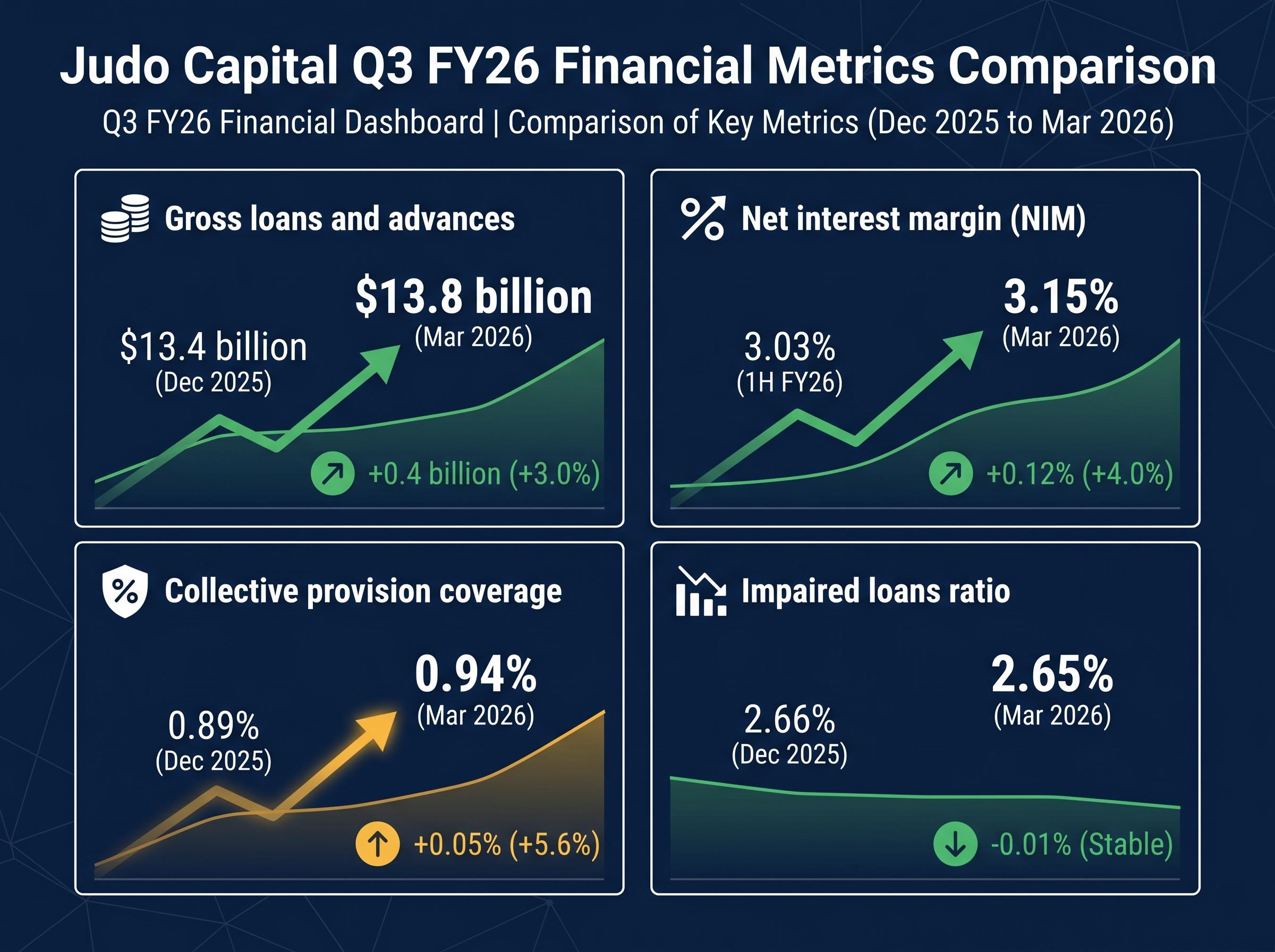

| Metric | March 2026 | December 2025 |

|---|---|---|

| Gross loans and advances | $13.8 billion | $13.4 billion |

| Net interest margin (NIM) | 3.15% | 3.03% (1H FY26) |

| Collective provision coverage | 0.94% | 0.89% |

| Impaired loans ratio | 2.65% | 2.66% |

Loan book and margin moving in the right direction

Gross loans and advances reached $13.8 billion at the end of Q3, up from $13.4 billion three months earlier. Lending growth is tracking in line with management’s own guidance, reinforcing execution credibility on the top line.

The customer attrition improvement disclosed in the Q3 update, from 33% annualised to 15%, is one of the more consequential data points for long-term investors assessing whether the relationship-banking model is genuinely taking hold, and it sits alongside a CET1 capital ratio that held steady at 12.6% through a quarter of active lending growth.

NIM expanded to 3.15% in Q3, up from 3.03% across the first half. Management indicated NIM was on track toward the upper end of its guidance range, a positive signal for revenue quality. Operating costs were confirmed as in line with guidance.

Provisions and the signals they send

The turning point in the data was the provision line. Collective provisions rose to 0.94% of gross loans (94 basis points) at 31 March, up from 0.89% (89 basis points) at December 2025, a five basis point increase.

Management attributed the uplift to economic uncertainty, naming agriculture and transport as the sectors of concern. A full loan portfolio review was conducted before the provision was raised, framing this as deliberate caution rather than reactive remediation. The impaired loans ratio, by contrast, improved marginally to 2.65% from 2.66%, indicating actual loan defaults had not accelerated.

Understanding what collective provisions are and why markets watch them

Collective provisions are money a bank sets aside against loans that have not yet defaulted but are judged to carry elevated risk in the current environment. They are a forward-looking estimate of potential losses across the loan book.

APRA Prudential Standard APS 220 sets out the credit risk management framework that Australian deposit-taking institutions must follow when assessing expected credit losses, including the methodology governing collective provision calculations of the kind Judo raised in Q3.

This matters because they differ from specific impairment charges in both direction and signal:

- Collective provisions: Forward-looking, applied portfolio-wide, based on management’s assessment of where credit conditions are heading

- Specific impairment charges: Backward-looking, tied to individual loans already in trouble

The two metrics can move in opposite directions simultaneously. That is precisely what happened at Judo in Q3: collective provisions rose while impaired loans marginally improved.

Investors wanting to understand how Judo’s provision uplift sits within the broader deterioration in ASX bank credit quality will find our full explainer on the Morgans sector-wide provisioning thesis, which covers the forecast rise in total Big Four provisions from approximately $2.4 billion in FY25 to approximately $5.5 billion by FY27, the earnings downgrade sequence across ANZ, CBA, NAB, and Westpac, and what the May 2026 reporting season is likely to confirm or challenge.

When a bank raises forward-looking provisions, it signals that management itself sees elevated uncertainty in near-term credit conditions. Markets tend to price that signal negatively even when headline asset quality remains stable, because provisions consume earnings and foreshadow potential write-downs. The sectors named by management, agriculture and transport, are both cyclically sensitive, which compounds the concern.

Guidance intact but skewed: what management’s lower-end signal means

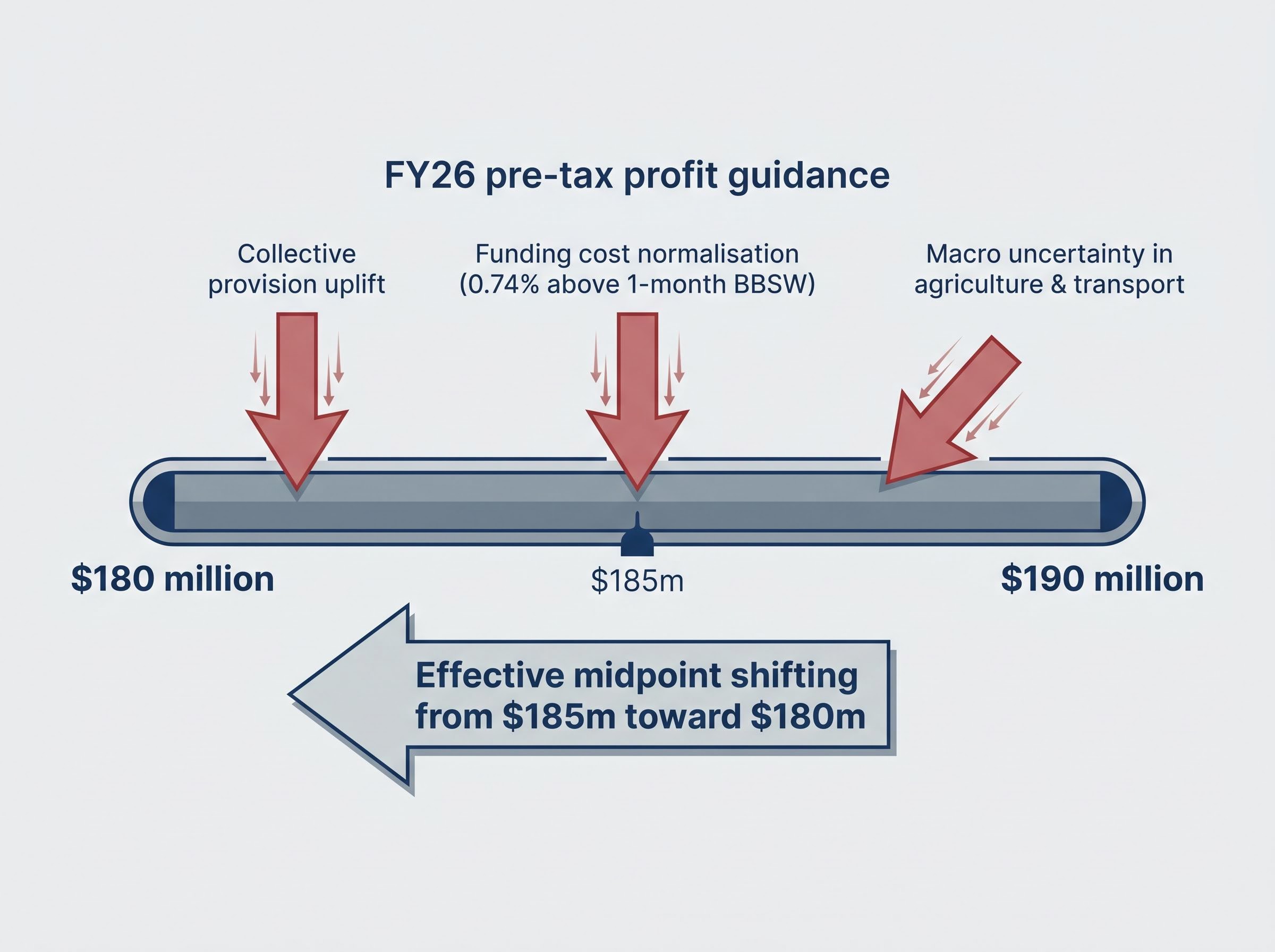

FY26 pre-tax profit guidance: $180-$190 million, reaffirmed in the Q3 update. Management language points toward the lower end of the range.

The distinction matters. A company reaffirming guidance and a company signalling it will land at the bottom of that guidance are two different messages. For investors, the effective midpoint of expectations has shifted from $185 million toward $180 million, and the market priced that shift on the day.

Three pressures are working against the upper end of the range:

- The collective provision uplift, which directly reduces pre-tax profit

- Funding cost normalisation, with the blended deposit cost sitting at 0.74% above one-month BBSW and expected to rise toward historical norms by year-end

- Macroeconomic uncertainty in the agriculture and transport segments that management itself has flagged

Total deposits reached $11.5 billion at the end of Q3, and new savings products launched by the bank have accumulated over $1.1 billion in balances within two quarters. The deposit growth is positive for long-term funding stability, but the near-term cost trajectory adds headwind to the NIM recovery that otherwise looked promising.

Broker consensus says the selloff overshot: the bull case at current prices

Implied upside: approximately 58% from the post-announcement close of roughly $1.40 to the average broker consensus target of $2.26.

Broker commentary following the update has characterised the 20% selloff as an overreaction. Lending growth, NIM expansion, and cost discipline are cited as evidence that the underlying business remains on track, with the provision uplift viewed as prudent rather than alarming.

Valuation divergence across ASX bank shares has widened sharply in 2026, with the Big Four delivering year-to-date returns ranging from positive 12.4% to positive 2.4% against a backdrop of unanimous or near-unanimous sell ratings, a dynamic that places Judo’s 20% single-session decline in the context of a sector where price momentum and fundamental valuation are broadly disconnected heading into May reporting season.

| Broker metric | Value |

|---|---|

| Average consensus price target | $2.26 |

| Target range (low) | $1.92 |

| Target range (high) | $2.62 |

| Confirmed Outperform-rated target | $1.85 |

| Post-announcement close | ~$1.40 |

One broker carrying an Outperform rating holds a price target of $1.85. Formal upgrade or downgrade actions from named firms following the update should be verified directly with broker research desks, as independent confirmation was not available at the time of writing.

The agribusiness expansion bet and what it signals about JDO’s risk appetite

Why management is leaning into agribusiness despite the headwinds

CEO Chris Bayliss has articulated a strategy centred on deepening Judo’s penetration into regional and agribusiness lending. The bank’s relationship-driven model, with a low customer-per-banker ratio, is positioned as the structural advantage that allows it to serve SME borrowers that larger institutions overlook.

Judo’s explicit focus on serving Australian SMEs during periods of elevated market volatility is framed as a mission-driven positioning choice. Management’s view, as expressed in the Q3 update, is that risk in the agriculture and transport segments remains manageable and that pricing is adequate at current margins.

The concentration risk investors should weigh

The tension is direct. Provisions are being raised against agriculture-exposed loans because management sees economic uncertainty in that segment. Simultaneously, the bank is deepening its strategic commitment to the same segment.

Capital adequacy remains healthy and operating costs are confirmed in line with guidance, providing a buffer for continued investment. Whether that buffer proves sufficient depends on whether the macro headwinds management has acknowledged remain contained or intensify through the final quarter of FY26.

Agricultural portfolio headwinds are surfacing across multiple ASX-listed specialty lenders in the same reporting period, with Heartland Group downgrading its Australian Livestock Finance growth guidance from above 20% to flat in its Q3 update while simultaneously reporting group NIM expansion to 4.06%, a pattern that suggests sector-level exposure rather than idiosyncratic credit management.

What the Q3 update leaves unresolved heading into the final quarter

The stock is trading roughly 37% below the average broker consensus target of $2.26, with identifiable downside risks that remain unresolved. Three questions will determine whether the current price represents an opportunity or a warning:

- Does FY26 pre-tax profit land at $180 million, or does the full $180-$190 million range remain achievable?

- Does funding cost normalisation in Q4 compress the NIM recovery that reached 3.15% in Q3?

- Does agribusiness credit quality hold at current provision levels, or does further deterioration require additional write-downs?

Investors evaluating JDO at current prices should verify the live share price via the ASX, the current RBA cash rate from the official RBA statistics page, and named broker research directly from broker platforms, given the speed at which data currency matters for this decision.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.