Gold Falls to $4,072 as Iran Strikes Lift Yields, Not Safe Havens

45 mins ago

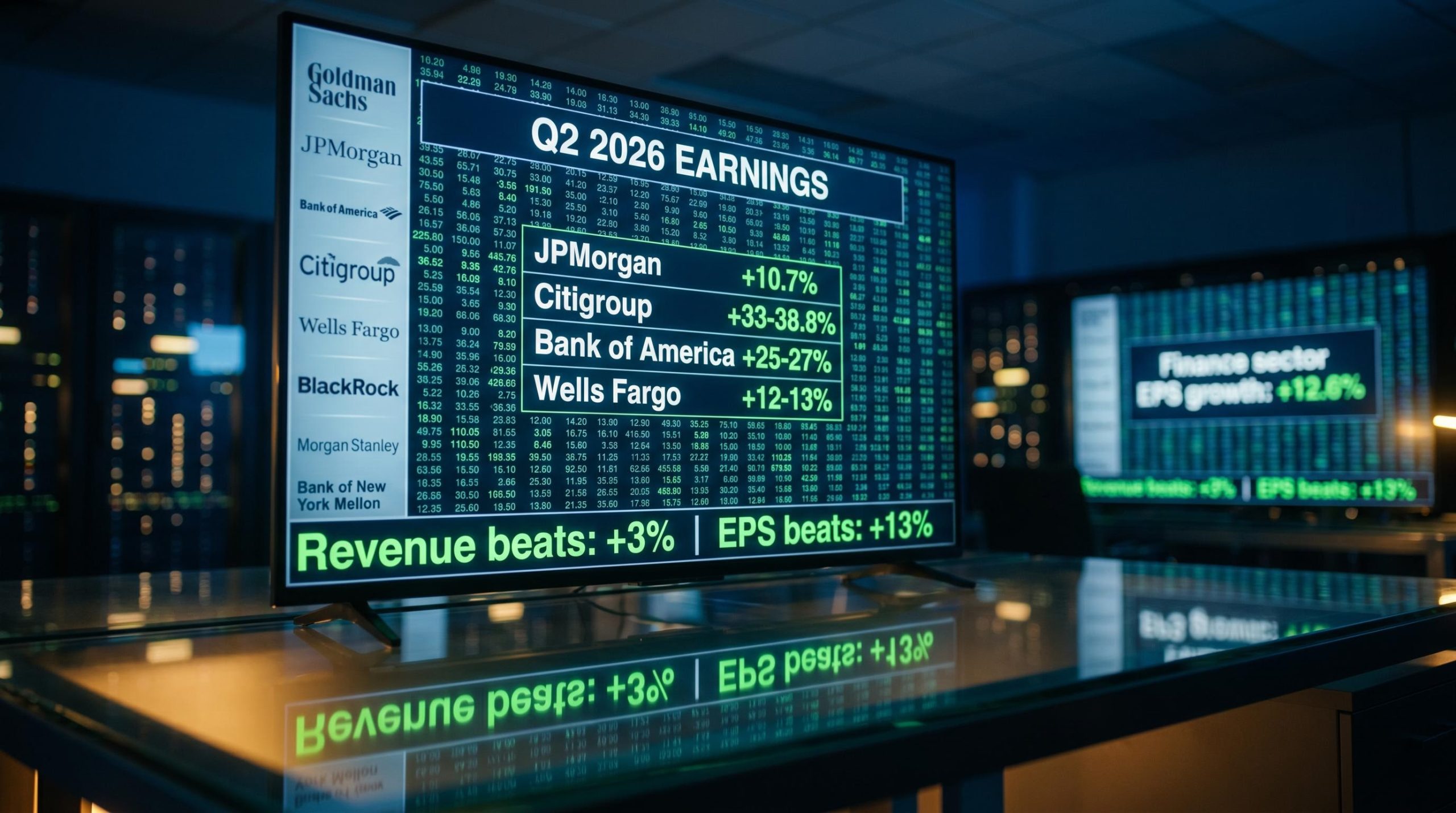

US banks are opening Q2 2026 earnings season with revenues beating analyst estimates by 3% and earnings clearing the bar by 13%. Those are not forecasts. Those are the early numbers already on the board as the first results land.

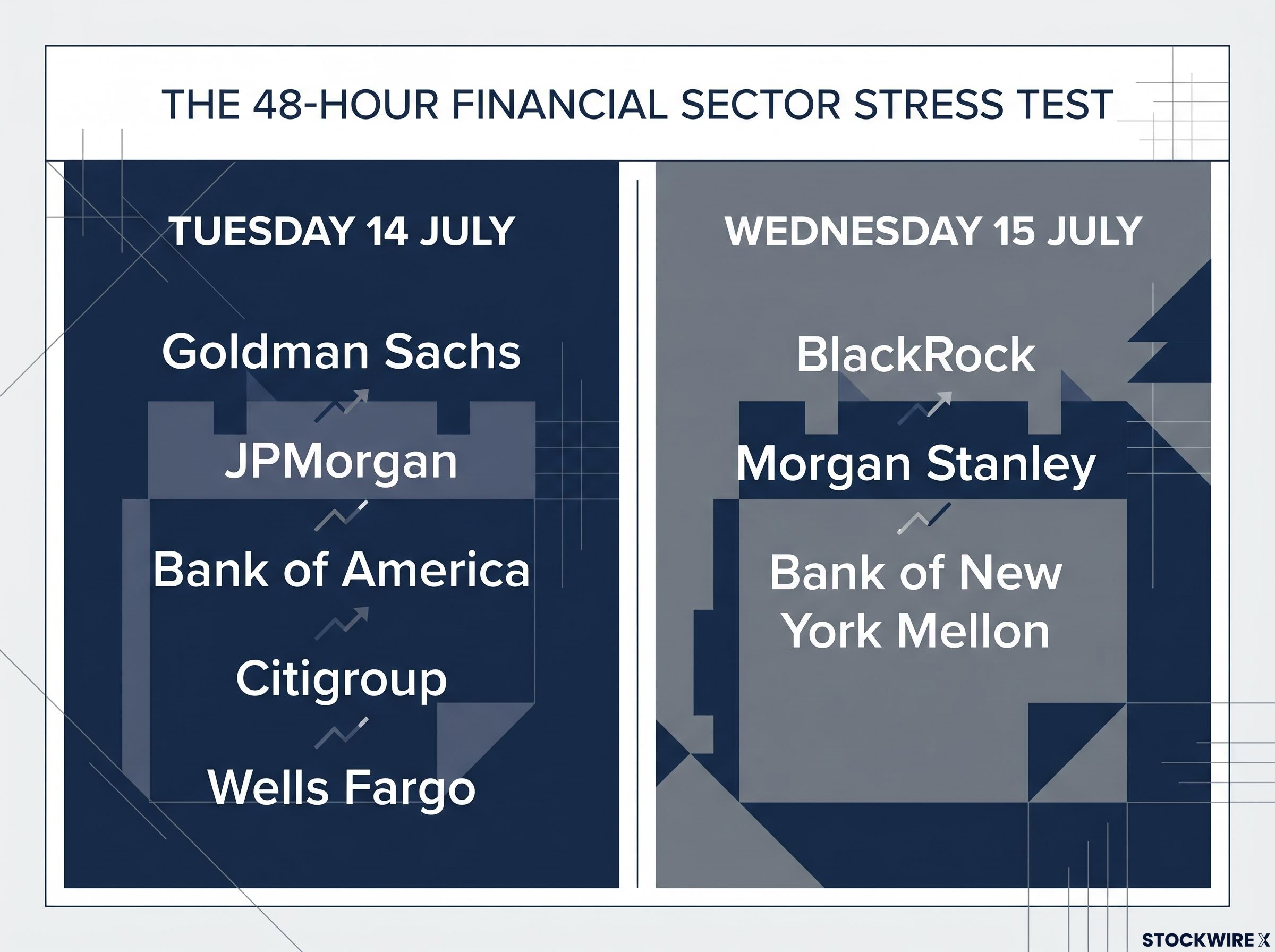

The week of 14-15 July 2026 is unusually front-loaded with financial sector weight. Tuesday’s roster includes five major institutions: Goldman Sachs, JPMorgan, Bank of America, Citigroup, and Wells Fargo. Wednesday then brings a further trio in BlackRock, Morgan Stanley, and Bank of New York Mellon. The finance sector is the second-largest contributor to S&P 500 earnings after technology, which means this week’s results will set the tone for the full season’s narrative before most other sectors have even opened their books.

Here is what the early data tells you about the health of the US financial system, and here are the specific line items worth watching as results land over the next 48 hours.

The early beat rates are not just encouraging; they are arriving against a backdrop where analysts had already raised their estimates. That combination is the more meaningful signal.

For the full S&P 500, Q2 2026 consensus forecasts project:

Those estimates have been revised upward in recent months, not cut. When analysts raise their numbers heading into a reporting window rather than trimming them for safety, it signals that the macro environment is firmer than expected.

FactSet Earnings Insight data for Q2 2026 shows 89% of early S&P 500 reporters beating EPS estimates and 72% beating revenue estimates, providing the statistical foundation for the beat rates cited at the opening of this week’s reporting window.

JPMorgan’s private bank describes US earnings growth as “robust and broad-based,” noting a sixth consecutive quarter of double-digit EPS growth and margin expansion across most sectors.

That context matters for this week. You are not watching bank results land against a cautious consensus. You are watching them land against a bar that has quietly risen, which makes genuine strength harder to fake and genuine weakness harder to hide.

Eight systemically significant financial institutions reporting within 48 hours is not a scheduling coincidence. It is a compressed stress test. By Wednesday evening, investors will have a near-complete picture of US financial sector health across commercial banking, investment banking, asset management, and wealth management.

| Reporting Date | Institutions Reporting |

|---|---|

| Tuesday 14 July | Goldman Sachs, JPMorgan, Bank of America, Citigroup, Wells Fargo |

| Wednesday 15 July | BlackRock, Morgan Stanley, Bank of New York Mellon |

Approximately 30 S&P 500 companies report this week in total, but these eight carry disproportionate weight. The finance sector is the index’s second-largest earnings contributor after technology, so its results do not just reflect banking conditions; they shape index-level sentiment for weeks.

These banks have also consistently beaten expectations in recent quarters, which has raised the bar but conditioned markets to treat current consensus figures as potentially conservative. The 48-hour window means the market will not have to wait long for confirmation or disruption of its current constructive view. Sentiment shifts this week are effectively a real-time verdict on the financial sector’s narrative.

Sentiment shifts from this week’s bank results will land inside a broader market leadership rotation already underway: the Nasdaq fell 4.6% in the final week of H1 2026 while the Dow gained roughly 0.6%, a divergence that signals institutional capital was already moving toward financials and cyclicals before Q2 results confirmed the earnings thesis.

Two structural indicators matter before any individual bank reports a single number.

First, industry deposits have recovered to record levels, according to aggregate banking data, which has allowed banks to reduce deposit costs (the rates they pay customers to hold their money) and support net interest margins (NIM), the gap between what a bank earns on loans and what it pays on deposits. A wider NIM means more profit on every dollar lent.

Second, loan demand has rebounded. After a slow start to 2026 as tariff-related uncertainty weighed on corporate borrowing appetite, commercial loan pipelines have grown. Aggregate data point to what market expectations describe as the strongest loan growth in almost three years at the major money-centre banks, though this characterisation has not been independently confirmed ahead of reporting.

The loan demand recovery at major US banks sits against a housing sector that has weakened materially without dragging the broader economy: new single-family home sales fell 17.6% in January 2026, yet housing’s direct GDP contribution has shrunk to the low single digits from a pre-GFC peak of roughly 6.5%, limiting its drag on commercial credit pipelines.

These two conditions together are not coincidences. Strong funding and rising credit demand mean the credit channel, the mechanism through which banks transmit monetary policy into real economic activity, is functioning. That has implications well beyond bank profits.

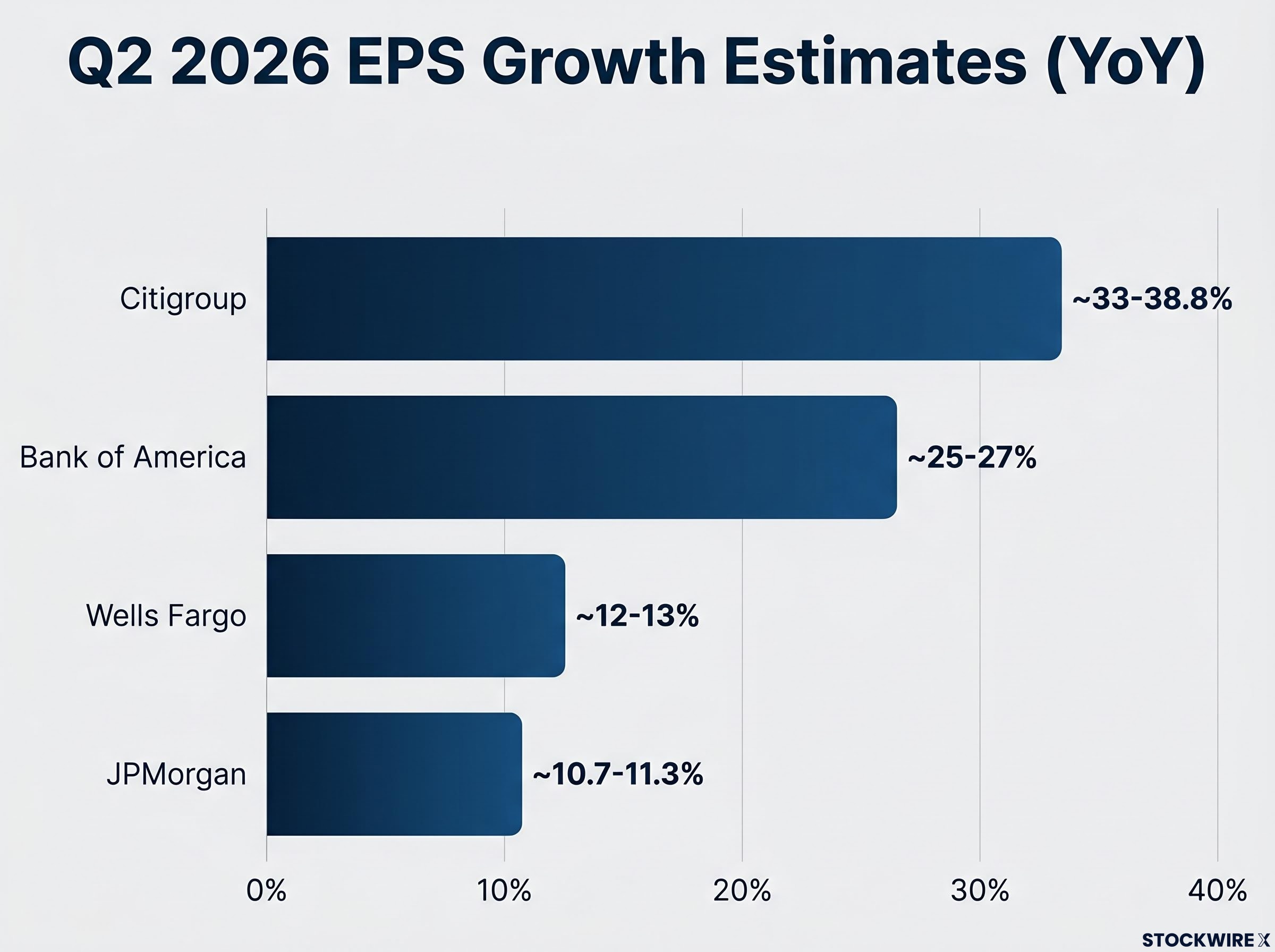

The finance sector overall is expected to post approximately 12.6% EPS growth and 8.4% revenue growth year-on-year for Q2 2026.

The individual estimates tell a more textured story.

| Bank | Q2 2026 EPS Growth Estimate (YoY) | Key Driver |

|---|---|---|

| JPMorgan | ~10.7-11.3% | Diversified revenue base; trading and NII balance |

| Bank of America | ~25-27% | Consumer banking sensitivity to rate environment |

| Citigroup | ~33-38.8% | Restructuring gains and improving cost discipline |

| Wells Fargo | ~12-13% | Loan growth recovery; deposit cost normalisation |

Citigroup’s 33-38.8% estimate is the standout, reflecting restructuring benefits translating into earnings leverage. Bank of America’s 25-27% speaks to its consumer-banking sensitivity in a still-favourable rate environment. JPMorgan and Wells Fargo are more moderate but still comfortably in double digits. All four estimates have moved higher during the quarter, which means the bar these banks face on Tuesday is not stale.

If rising loan demand combines with lower funding costs in Tuesday’s actual results, it confirms that bank profitability is being driven sustainably, not just riding a single favourable rate lever that could reverse.

Headline EPS beats are not enough. These are the five line items that will tell you whether the results reflect genuine health or a flattering quarter that masks emerging pressure.

The provisions picture at commercial banks cannot be read in isolation: consumer credit quality across the US household sector shows stress concentrated in younger and lower-income cohorts while aggregate net worth and mortgage delinquency rates remain at historically healthy levels, complicating any single-variable read of the credit cycle.

If banks revise NII guidance for H2 2026 downward, that is the most important signal to watch this week, regardless of how strong the Q2 headline numbers look. Forward guidance on NII tells you where margin pressure is heading; backward-looking beats tell you where it has been.

A result where NII holds, loan growth lands near expectations, and provisions rise only modestly would be the clearest possible signal that the US banking system is in genuine health, not just performing well on a single favourable input.

Tuesday’s results measure the credit engine. Wednesday’s results measure something different: investor confidence and the health of capital markets.

Bank of New York Mellon adds a custodial and asset-servicing lens, though its results carry less directional weight than the other two.

If BlackRock reports meaningful AUM growth and Morgan Stanley shows stable wealth management inflows, it confirms that investors are not retreating from risk assets. That is a forward-looking positive signal for market conditions in H2 2026, and it tells you something the commercial banking numbers alone cannot: that money is moving toward opportunity, not away from it.

The constructive baseline heading into this week is clear. Estimate revisions have moved upward. Early beat rates are strong. Deposits have recovered to record levels. Loan demand is rebounding. Six consecutive quarters of double-digit S&P 500 EPS growth have conditioned markets to expect strength.

The bank results this week arrive at a moment when broader H2 2026 positioning decisions hinge on an amber-light macro environment: recession odds sit at 30-35% according to RSM US, S&P Global, and JPMorgan, a range that demands the financial sector’s earnings signal be read carefully rather than treated as unambiguous confirmation of economic health.

That is the hypothesis. Here is what would challenge it:

By Wednesday 15 July, investors will have results from eight systemically significant institutions covering commercial banking, investment banking, asset management, and wealth management. That is enough information to decide whether the US financial sector’s current optimism is earnings-validated or whether it has run ahead of the fundamentals.

The verdict will shape positioning for the rest of the Q2 season. You do not need to wait for sell-side summaries if you know which signals matter. The five metrics above are your framework; the results landing over the next 48 hours are the test.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Financial projections referenced are subject to market conditions and various risk factors. Past performance does not guarantee future results.

The major US bank earnings for Q2 2026 land across two days: Tuesday 14 July brings Goldman Sachs, JPMorgan, Bank of America, Citigroup, and Wells Fargo, while Wednesday 15 July adds BlackRock, Morgan Stanley, and Bank of New York Mellon.

Net interest margin (NIM) is the gap between what a bank earns on loans and what it pays on deposits; a wider NIM means more profit on every dollar lent, making it the primary profitability indicator for commercial banks and the first place analysts look for signs of pressure.

The finance sector is projected to post approximately 12.6% EPS growth and 8.4% revenue growth year-on-year for Q2 2026, with individual bank estimates ranging from around 10.7-11.3% for JPMorgan up to 33-38.8% for Citigroup.

The five critical line items are net interest income and margin, loan growth volumes, credit quality and loan-loss provisions, investment banking and trading revenues, and capital and liquidity ratios; a headline EPS beat without strength across these metrics is not a reliable signal of genuine financial health.

The finance sector is the second-largest contributor to S&P 500 earnings after technology, so eight major institutions reporting within 48 hours will set the tone for the full earnings season and directly influence index-level sentiment before most other sectors have reported.