How Wesfarmers’ AI Strategy Is Built to Compound Returns

3 hrs ago

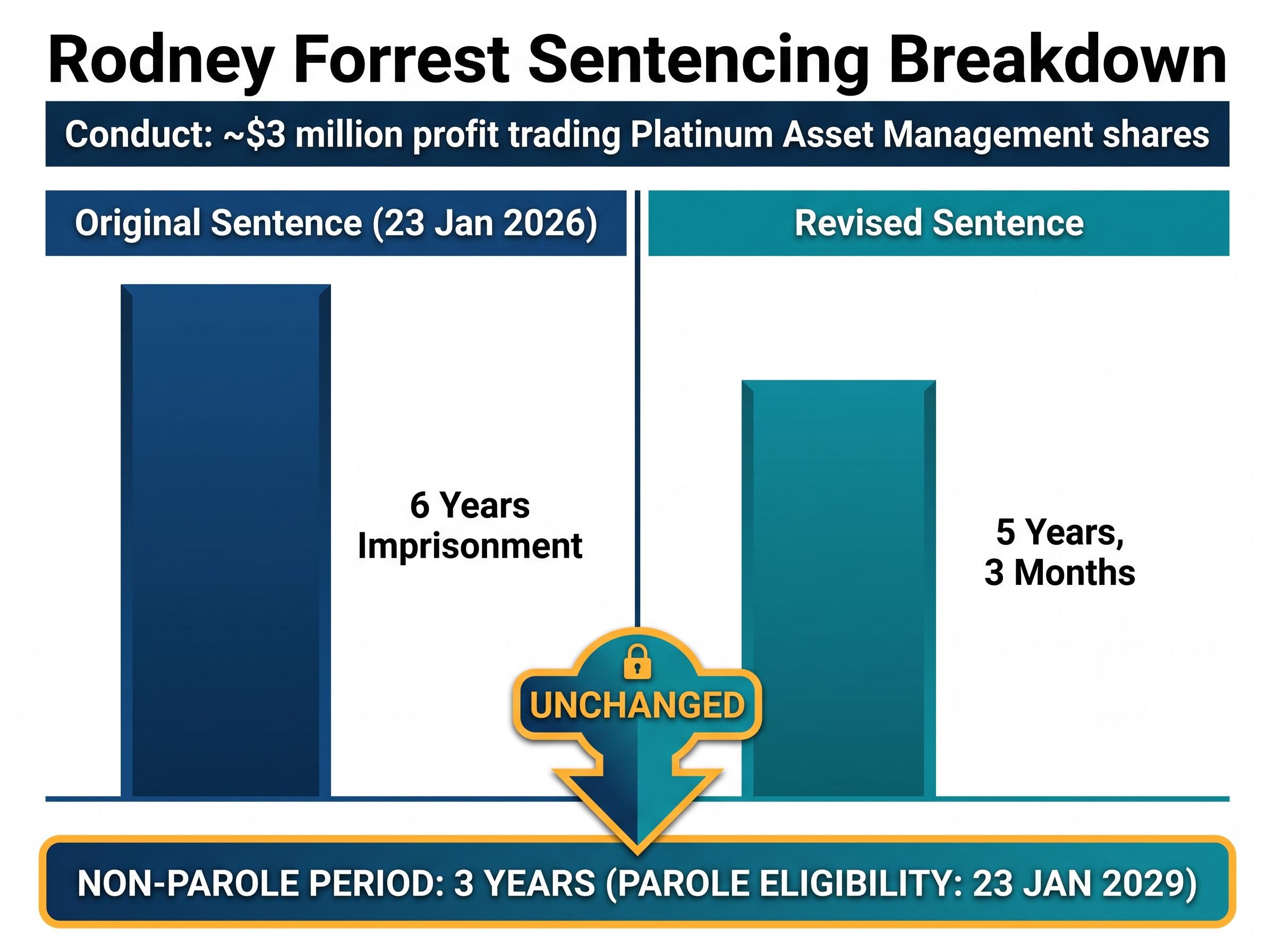

A fund manager who profited roughly $3 million trading on inside information about Platinum Asset Management was sentenced to six years’ imprisonment in an Australian court on 23 January 2026. Months later, the Full Federal Court reduced that sentence to five years and three months. The reduction was narrow, procedural, and precise. The court’s view of the conduct itself did not soften. What the Rodney Forrest re-sentencing reveals about insider trading enforcement in Australia extends well beyond one defendant: it marks the first completed prosecution by ASIC’s dedicated insider trading team, arrives as ASIC has formally designated insider trading as a 2026 enforcement priority, and offers a documented window into how Australian courts are calibrating punishment for serious market misconduct. What follows is an analysis of what the court decided, how ASIC built the case, what the legal framework permits, and what the outcome signals, and does not signal, about the enforcement environment finance professionals are operating in right now.

The end state is straightforward. Nine months were removed from the original sentence. The non-parole period was left untouched. Parole eligibility did not change.

The Full Federal Court accepted the appeal on a specific, narrow legal ground. It did not accept that the sentence was disproportionate to the conduct. It identified an error in how the original sentencing judge used certain evidence, corrected that error, and recalculated the term.

“A significant example of offences of this kind, requiring a substantial custodial term.”

That characterisation came from the court itself, after the reduction. The conduct involved more than $3 million in trades in Platinum Asset Management shares, deliberate planning, and a high degree of sophistication. The court found none of that diminished by the correction it applied. For finance professionals tracking this outcome, the reduction should be read as a legal adjustment, not a signal that Australian courts are retreating from substantial imprisonment for insider trading.

Rodney Forrest made false denials during an ASIC interview before eventually pleading guilty in August 2025, at the first court mention at Downing Centre Local Court. The sentencing judge treated those false statements as relevant to two separate sentencing considerations: Forrest’s lack of remorse, and the objective seriousness of the insider trading itself.

The second use was the problem. A defendant’s false statements to a regulator are legitimately relevant when assessing remorse, cooperation, and the weight given to a guilty plea. They cannot, however, be used to elevate the objective gravity of the underlying offence. The original judge conflated these two domains, importing conduct that belonged in one into a space where it does not.

The Full Federal Court corrected the error and still treated general deterrence as a primary sentencing factor.

The court emphasised that general deterrence remained a primary consideration in calibrating the sentence for this category of offence.

The conduct’s characteristics, deliberate planning, a significant violation of trust, and a high degree of sophistication, were unaffected by the correction. The non-parole period remaining at three years is the clearest signal: the court saw no reason to bring forward the earliest possible release date. For any professional facing an ASIC investigation, the principle is directly transferable. How a person responds to regulatory scrutiny will be weighed at sentencing, but within defined legal boundaries.

The Forrest conviction did not emerge from a reactive response to a single complaint. ASIC’s dedicated insider trading team, established in late September 2024, conducted a six-month investigation before referring the matter to the Commonwealth Director of Public Prosecutions (CDPP). The prosecution, through both the original sentencing and the appeal, was handled by the CDPP.

That timeline matters because it establishes an operational sequence for a team that had not previously completed a case.

| Milestone | Date | Significance |

|---|---|---|

| Dedicated team established; surveillance activity detected | Late September 2024 | First operational deployment of the specialist insider trading team |

| Six-month investigation completed; CDPP referral | Early-mid 2025 | Investigation-to-prosecution pipeline demonstrated |

| Guilty plea at first mention | August 2025 | Early plea reduced need for contested trial |

| Original sentencing | 23 January 2026 | First completed custodial sentence by the new team |

| Appeal and re-sentencing | 2026 | Sentence adjusted on narrow grounds; severity upheld |

The team’s formation in late September 2024 was a deliberate infrastructure investment, not a response to a single investigation. The ASIC Corporate Plan 2025-26 designates market misconduct, including insider trading, as a continuing enforcement priority. Forrest is the first public benchmark for what the team can deliver. For professionals in roles with access to material non-public information, the investigative infrastructure has changed.

The prohibition that underpins this prosecution is section 1043A of the Corporations Act 2001 (Cth), located in Part 7.10, Division 3. The provision covers both direct trading on inside information and procuring others to trade, which is the specific mechanism through which the offence operates. A person who possesses information that is not generally available, and that a reasonable person would expect to have a material effect on the price of a financial product, commits an offence by trading or causing another person to trade on that information.

The maximum criminal penalty for individuals was substantially increased by the Treasury Laws Amendment (Strengthening Corporate and Financial Sector Penalties) Act 2018 (Cth), which commenced on 13 March 2019. The ceiling is now 15 years’ imprisonment.

The Treasury Laws Amendment (Strengthening Corporate and Financial Sector Penalties) Act 2019 lifted the maximum custodial term for serious financial sector offences, including insider trading, to 15 years, establishing the sentencing ceiling that courts now apply when calibrating terms for conduct of this kind.

Forrest’s revised sentence of five years and three months sits well below the 15-year statutory maximum, calibrated in part by the guilty plea entered at first mention.

ASIC’s enforcement toolkit extends beyond criminal prosecution:

Market manipulation offences under sections 1041A and 1041B of the Corporations Act carry the same 15-year maximum custodial penalty as insider trading, and ASIC’s December 2025 data showed a notable rise in pump-and-dump reports, with four individuals pleading guilty in June 2025 to using Telegram groups to inflate small-cap share prices.

This layered framework means that even where a criminal prosecution does not proceed, or where a sentence falls short of the maximum, ASIC retains additional tools to remove offenders from the market. For finance professionals, directors, and advisers, the statutory ceiling and the breadth of the penalty toolkit clarify exactly how much sentencing room Australian courts have.

The dominant view among senior legal practitioners is direct: custodial sentences alter the risk calculus for market professionals in ways that monetary penalties cannot. The reasoning centres on what imprisonment adds beyond financial cost.

A fine, even a large one, can be absorbed or factored into a risk-reward calculation. A prison term cannot. It carries career destruction, public stigma, loss of professional standing, and a permanent criminal record. According to Clayton Utz’s 2025-26 regulatory advisory, “the prospect of jail time, reputational destruction and professional banning is now an explicit message to the market.” Jones Day’s December 2025 financial services update similarly noted that recent custodial sentences “underscore the Courts’ preparedness to impose actual custodial terms where there is significant gain or harm” and assessed this as “likely to have a meaningful general deterrent effect, particularly for professionals in regulated positions.”

The practitioner consensus is firmly held. Its empirical foundation is less certain.

ASIC Report 787 assessed Australian equity markets as among the cleanest globally for the period November 2018 to April 2024, using abnormal price run-up analysis as its primary diagnostic tool, a methodology that measures the extent to which prices move ahead of material announcements in ways inconsistent with public information alone.

ASIC Report 787’s finding is relevant context, but market cleanliness and proven deterrence are not the same claim. Clean markets may reflect effective deterrence, effective surveillance, cultural norms, or some combination. No post-2025 Australian study has empirically measured whether custodial sentences for insider trading have directly changed trading behaviour in Australian capital markets. Finance professionals weighing compliance risk should understand both the regulatory theory of deterrence and the limits of the evidence supporting it.

Investors exploring how Australian courts and regulators calibrate penalties across different types of market misconduct will find our deep-dive into the Macquarie short sale penalty useful context, as it applies the same deterrence framework to a $35 million civil penalty against a major institution and examines whether financial penalties alone change institutional behaviour.

The Forrest case is a genuine enforcement milestone. A specialist team detected the conduct, investigated it, referred it to the CDPP, secured a guilty plea, and delivered a substantial custodial sentence. The appeal did not unwind that outcome; it adjusted it by nine months on a narrow procedural ground. As a proof of concept, the case works.

What the Forrest case confirms:

What remains unknown:

One completed prosecution does not establish a systematic enforcement pattern. The 2026 priority designation and the specialist team’s continued operation are the most reliable forward-looking signals available, but the pipeline beyond Forrest is not yet publicly visible. For investors, compliance professionals, and advisers, the calibrated reading is this: ASIC has demonstrated both intent and capability. The full scale of the enforcement push remains unconfirmed and should be monitored through ASIC’s annual report and future enforcement media releases.

The criminal prosecution of financial directors under the Corporations Act has accelerated across multiple sectors in 2025-2026, with the Berndale Capital Securities case producing a 2 years and 11 months custodial sentence for co-director Daniel Kirby in July 2025 and a separate guilty plea from Stavro D’Amore in April 2026, providing the closest available sentencing benchmarks for professionals facing personal criminal exposure.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Insider trading in Australia is prohibited under section 1043A of the Corporations Act 2001, which makes it an offence for a person who possesses material non-public information to trade, or cause another person to trade, in a financial product where that information would reasonably be expected to affect the product's price.

Following amendments introduced by the Treasury Laws Amendment (Strengthening Corporate and Financial Sector Penalties) Act 2018, which commenced on 13 March 2019, the maximum custodial sentence for insider trading in Australia is 15 years' imprisonment for individuals.

The Full Federal Court identified a procedural error in which the original sentencing judge used Forrest's false denials to ASIC to elevate both his assessed lack of remorse and the objective seriousness of the offence itself, which is not legally permissible; correcting that error reduced the sentence by nine months, though the non-parole period remained unchanged.

ASIC's dedicated insider trading team, established in late September 2024, conducts surveillance and investigation before referring matters to the Commonwealth Director of Public Prosecutions; the Forrest case moved from surveillance detection through a six-month investigation to a guilty plea and custodial sentence within roughly one year.

Legal practitioners broadly argue that custodial sentences deter insider trading in ways that financial penalties cannot, because imprisonment adds career destruction, public stigma, and a permanent criminal record; however, as Jones Day noted in December 2025, empirical evidence on whether custodial sentences have directly changed trading behaviour in Australian capital markets remains limited.