Inside ASIC’s Four-Stage Plan to Rebuild Australian Markets

19 mins ago

Gold has clawed back 4.4% across three sessions and is pushing toward US$4,200, with JPMorgan putting a US$4,500 quarterly average on the table for Q4 2026. That is not a fringe call. It sits at the lower end of the current bullish institutional consensus, which makes it conservative relative to where the broader forecasting community has landed.

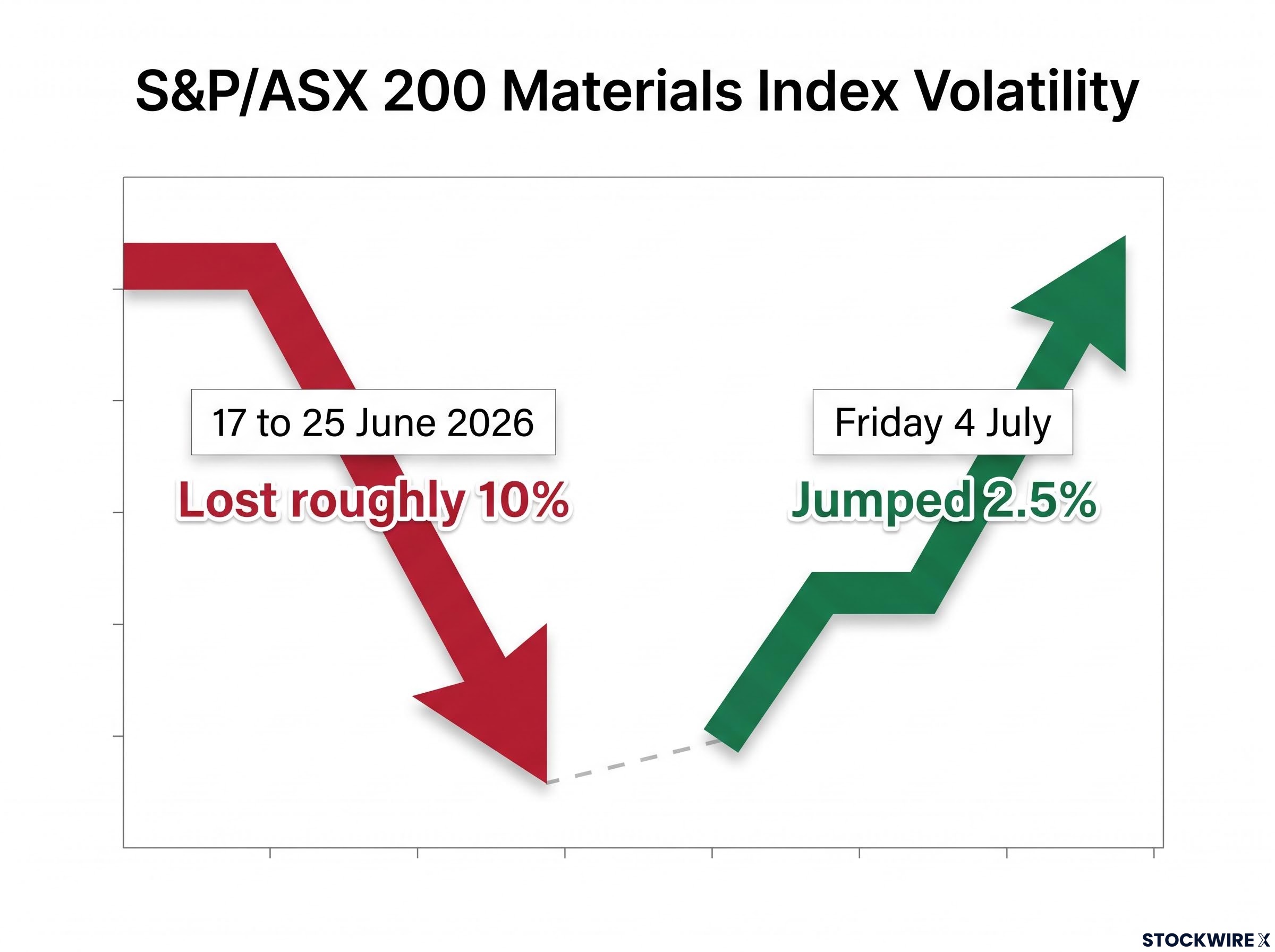

The move is not happening in isolation. Broader metals markets joined the advance in Monday’s early session, with silver, zinc, platinum and palladium all posting gains, while the S&P/ASX 200 Materials Index had already jumped 2.5% on Friday 4 July after losing roughly 10% of its value in the period from 17 to 25 June. For Australian investors with materials exposure, the commodity cycle is moving again, and the drivers behind it are structural rather than purely speculative.

Here is what is actually pushing metals higher, how much weight to place on JPMorgan’s gold price prediction of US$4,500, what could derail it, and what the rally means for ASX materials positions specifically. This is the context you need before deciding whether this move changes anything for your portfolio.

Gold was trading at US$4,170.25, up 1.15%, as of the morning of 6 July 2026. Separate reports had it at US$4,183, up 1.4%, in early Monday activity. The three-session gain of approximately 4.4% marks the sharpest short-term recovery since gold corrected from its all-time high above US$5,500 in January 2026.

Gold’s 2026 bear market, which saw the metal fall nearly 25% from its January peak despite active military conflict and elevated inflation, established the correction base from which the current three-session recovery is now building, and the same real-yield and dollar dynamics that drove that decline remain active risk factors for the second half.

JPMorgan’s forecast lays out a two-stage path for the second half of the year:

JPMorgan’s Q4 2026 target of US$4,500/oz represents approximately 7-8% upside from current levels, a measured institutional base case rather than a call for another parabolic run.

That gap between where gold sits today and where JPMorgan sees it by year-end is meaningful but modest. This is not a forecast built on momentum alone. It is conditional on central-bank demand holding, monetary policy evolving broadly in line with current expectations, and the US dollar staying contained. If any of those assumptions shift, the target shifts with them.

The breadth of the rally tells you something the gold price alone does not. As of early Monday 6 July 2026, every major metal was trading higher.

| Metal | Session gain | Price |

|---|---|---|

| Gold | +1.15% to +1.4% | US$4,170-4,183 |

| Silver | +3.2% | ~US$63/oz |

| Copper | +0.90% | US$6.17 |

| Zinc | +2.7% | — |

| Platinum | +2.0% | — |

| Palladium | +1.3% | — |

Three forces are converging. First, central-bank accumulation in emerging markets continues to provide a structural demand floor for gold. JPMorgan cites ongoing official-sector buying as a core pillar of its bullish forecast.

Second, macro and geopolitical uncertainty is driving safe-haven flows. The World Gold Council’s 2026 outlook models 5-15% upside for gold under a moderate slowdown and rate-cut cycle, rising to 15-30% in a more severe downturn with aggressive easing.

Third, real yield expectations are shifting. JPMorgan argues that as real yields and monetary policy paths become more supportive through the second half of 2026, the opportunity cost of holding gold falls, which historically pulls capital back into the metal.

Silver’s 3.2% gain stands out. Silver carries dual exposure as both a safe-haven asset and an industrial input for solar panels, electronics and batteries. Silver and copper moving together with gold tells you this rally has both defensive and growth-oriented legs, which makes it more durable than a fear-only spike and more relevant if you hold diversified materials exposure.

JPMorgan’s target sits at the lower end of the current bullish institutional consensus. The World Gold Council’s base-case modelling aligns with a move of this magnitude, suggesting 5-15% upside under moderate conditions. At approximately 7.4% above current levels of US$4,189, the US$4,500 target falls comfortably within that range.

The Goldman Sachs gold forecast of US$5,400 by late 2026, reaffirmed despite recent volatility, sits roughly 20% above JPMorgan’s Q4 target and illustrates how wide the institutional range has become, with peer banks clustering between US$4,900 and US$6,300 depending on their assumptions about central-bank demand and Federal Reserve policy sequencing.

That makes it a conservative call, not an aggressive one. But conservative does not mean guaranteed.

Four specific scenarios could prevent gold from reaching it:

JPMorgan’s explicit warning that gold’s renewed sensitivity to real yields is already capping near-term upside is the most immediate risk factor. The next Federal Reserve communications matter directly to this trade.

The fact that JPMorgan is simultaneously publishing a US$4,500 target and flagging real-yield sensitivity as an active cap tells you this is a forecast built on a specific macro path, not a blanket endorsement.

The S&P/ASX 200 Materials Index recorded a 2.5% advance on Friday 4 July, but that figure needs context. Between 17 and 25 June 2026, the index had shed roughly 10%, so Friday’s jump represented a bounce from a lower reset base rather than an unprompted spike higher.

That distinction matters for how you think about exposure. The June correction absorbed speculative excess. The Friday recovery suggests the sector is responding to commodity fundamentals again rather than retracing on momentum alone.

Within the materials sector, the type of exposure shapes the benefit:

For investors thinking about which bucket they sit in, the breadth of this metals rally favours diversified exposure over single-commodity bets, though pure-play names will outperform on the way up if the JPMorgan scenario materialises.

Two company-specific developments are worth noting:

One broader signal: on the morning of 6 July, ASX 200 futures were pricing in a drop of 52 points (-0.39%), which is a useful reminder that rising commodity prices alone cannot lift the whole market. The materials sector may be performing well, but it is doing so against a mixed backdrop across the broader index.

Sector divergence across the ASX 200 in June 2026 was more pronounced than the flat headline figure suggested, with Materials falling 6.7% and Energy falling 8.8% while Consumer Staples and Healthcare each surged 12-13%, a split that explains why commodity strength in early July does not automatically translate into a rising broader index.

Rather than treating the US$4,500 target as something to believe or dismiss, track these five indicators. Each one maps to a structural driver or downside risk covered earlier, and together they will tell you whether JPMorgan’s assumed macro path is holding or diverging.

| Signal | Favourable reading | Adverse reading |

|---|---|---|

| World Gold Council central-bank purchase data | Quarterly buying remains elevated or accelerates | Official-sector purchases decelerate materially |

| Fed and RBA rate decisions and guidance | Dovish tilt, real yields declining | Hawkish hold or tightening signals, real yields rising |

| US dollar index trajectory | Stable or weakening USD | Sustained dollar rebound above recent ranges |

| S&P/ASX 200 Materials Index price action | Reclaims and holds above pre-June-pullback levels | Fails to recover, confirms trend reversal |

| Global manufacturing and trade data | Stabilising or improving industrial activity | Deteriorating output, weakening risk appetite |

Including the RBA alongside the Fed matters for Australian investors specifically. Domestic rate decisions shape AUD-denominated gold returns and influence how ASX-listed miners translate commodity prices into earnings.

The RBA’s May 2026 Statement on Monetary Policy sets out the cash rate trajectory and inflation outlook that shapes how AUD-denominated gold returns translate into earnings for ASX-listed miners, making domestic rate guidance as consequential as Fed signals for Australian materials investors.

The June correction absorbed speculative excess across the materials sector. The current rally has structural support from central-bank buying, a broad metals recovery, and an institutional consensus that sees further upside through the second half of 2026.

But JPMorgan’s US$4,500 Q4 target remains conditional, not certain. The materials sector’s 2.5% Friday recovery after a 10% correction is evidence of resilience, while ASX 200 futures pointing to a 52-point Monday decline is a reminder that commodity strength does not carry the whole market.

The five signals above are the practical framework. Track them, and you will know whether the macro path JPMorgan has assumed is materialising on schedule or diverging from it. That is a stronger position than treating any single forecast as the final word.

For investors evaluating whether the current metals rally justifies a larger structural position in resources, our deep-dive into Societe Generale’s commodities allocation shift examines the bank’s five-driver thesis — including electrification, AI infrastructure, and defence spending — that underpins its move from 5% to 20% commodities weighting in a single rebalancing step.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

JPMorgan forecasts a quarterly average gold price of US$4,300 per ounce in Q3 2026 and US$4,500 per ounce in Q4 2026, representing approximately 7-8% upside from current levels near US$4,170-4,183. The bank describes this as a base case conditional on central-bank demand holding and real yields becoming more supportive through the second half of the year.

Three structural forces are converging: ongoing central-bank accumulation in emerging markets providing a demand floor, macro and geopolitical uncertainty driving safe-haven flows, and shifting real yield expectations that reduce the opportunity cost of holding gold. The breadth of the rally, with silver, copper, zinc, platinum and palladium all advancing together, signals the move has both defensive and growth-oriented drivers rather than being a fear-only spike.

JPMorgan identifies four key risks: stickier-than-expected real interest rates that raise the opportunity cost of holding gold, a sustained US dollar rebound that weighs on emerging-market demand, a deceleration in official-sector central-bank purchases, and crowded speculative positioning that could trigger fast liquidations after gold's multi-year run above US$5,500 in January 2026. JPMorgan explicitly warns that renewed sensitivity to real yields is already capping near-term upside.

The S&P/ASX 200 Materials Index jumped 2.5% on 4 July after losing roughly 10% between 17 and 25 June, suggesting the sector is responding to commodity fundamentals again rather than retracing on speculative momentum. Diversified resource groups benefit from the broad metals rally across gold, silver and copper, while pure-play gold miners offer higher leverage to the gold price but with concentrated single-commodity risk.

JPMorgan's Q4 2026 target sits at the conservative, lower end of the current institutional consensus. Goldman Sachs has a target of US$5,400 by late 2026, and peer banks cluster between US$4,900 and US$6,300 depending on their assumptions about central-bank demand and Federal Reserve policy, making JPMorgan's call the most measured rather than the most bullish.