The Case Against Thematic ETFs After 2026’s Sector Rotation

3 hrs ago

Wall Street awoke on 29 April 2026 to a massive earnings beat from power equipment manufacturer Generac Holdings Inc., triggering minimal changes in early trading. The broader equities market approached this Generac earnings report with distinct caution following a fourth-quarter 2025 performance that missed consensus estimates.

However, the underlying financial data reveals unexpected revenue drivers and a strategic corporate pivot that is transforming the company’s historical reliance on residential home generators. This detailed analysis breaks down the blowout quarter, examines the rapid expansion into commercial data centre infrastructure, and explores what the upgraded annual guidance means for investors positioning their portfolios for the remainder of the year.

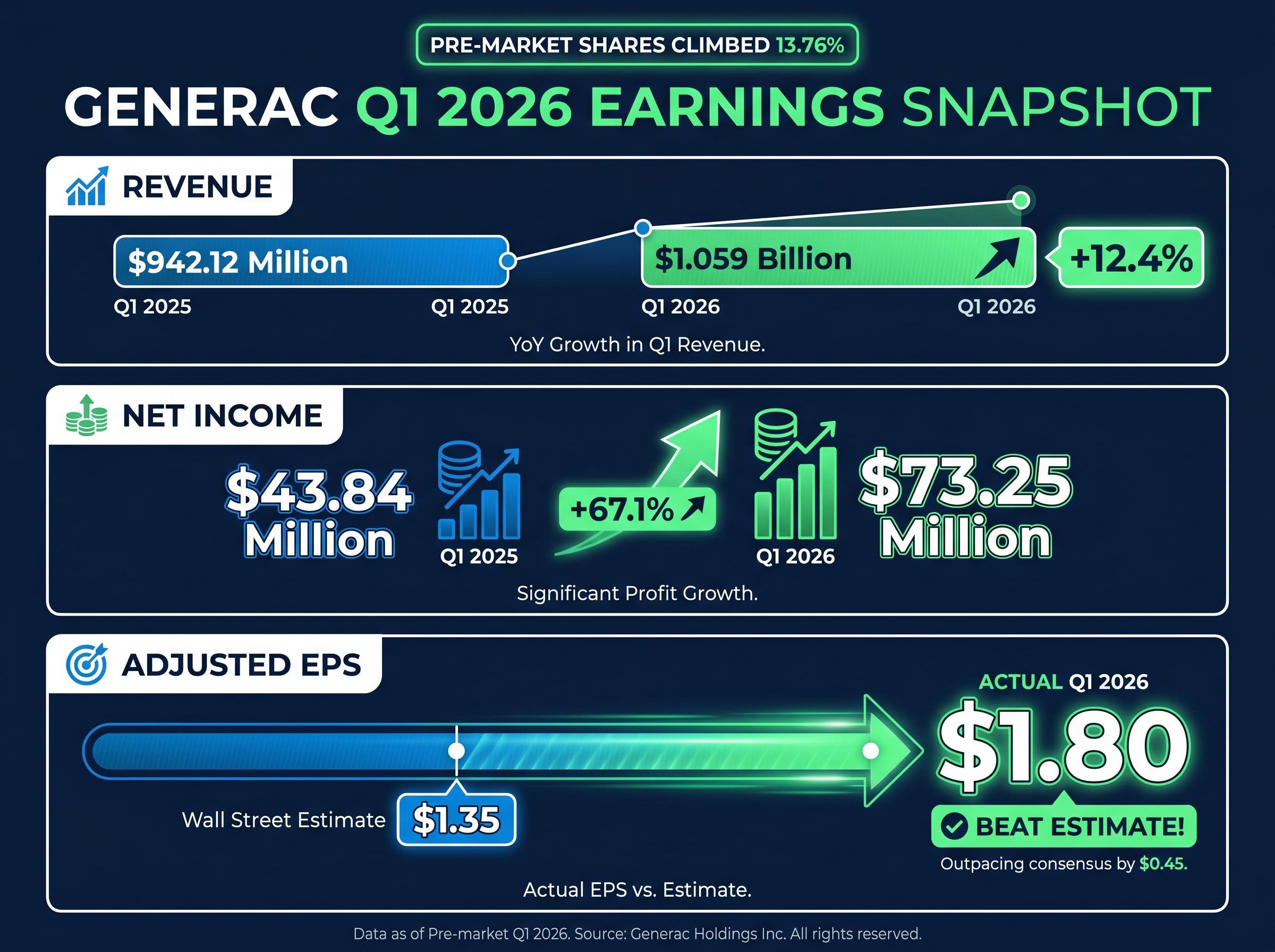

The sheer magnitude of the financial beat forced an immediate repricing of the stock during pre-market trading hours. Shares climbed 13.76% before the opening bell, erasing the lingering pessimism from the previous quarter’s earnings miss.

The top-line figures exceeded all major institutional projections by a comfortable margin. The company reported $1.059 billion in consolidated revenue, representing a 12.4% year-on-year increase from the $942.12 million recorded in the first quarter of 2025.

Profitability metrics delivered an even sharper divergence from standard analyst expectations. Adjusted earnings per share reached $1.80. Net income rose to $73.25 million, up substantially from the $43.84 million reported during the same period last year.

For investors assessing the valuation, this margin of outperformance provides fundamental justification for the double-digit equity surge. It demonstrates a clear operational turnaround from the end of 2025, confirming that management has successfully absorbed previous supply chain inefficiencies to deliver expanded profit margins.

The official Q4 2025 financial results revealed a notable decrease in residential sales, making this subsequent quarterly rebound a critical validation of the new commercial focus.

| Financial Metric | Q1 2026 Results | Q1 2025 Results | Wall Street Estimates |

|---|---|---|---|

| Revenue | $1.059 billion | $942.12 million | N/A |

| Adjusted EPS | $1.80 | $0.73 | $1.35 |

While the headline earnings numbers captured immediate market attention, the underlying product mix reveals a fundamental shift in the broader corporate structure. The commercial manufacturing division, which produces industrial-scale power solutions, is rapidly eclipsing the consumer home division as the primary growth engine for the business.

This strategic transition is a direct result of the escalating electrical power demands originating from artificial intelligence infrastructure and cloud computing server farms. These massive technology facilities require robust, uninterruptible backup power systems to prevent catastrophic data loss during regional grid failures. Generac has successfully capitalised on this emerging requirement by securing crucial vendor authorisations with tier-one technology clients.

The latest IEA projections on global electricity forecast that data centre consumption will double by 2030, a macroeconomic tailwind that directly supports the expanded manufacturing focus on uninterruptible backup systems.

The financial impact of these data centre authorisations is explicitly clear in the divisional revenue breakdown. According to company data, commercial division revenue grew by a massive 28%, reaching $510.1 million, a sharp increase from the $399.0 million reported in the previous year.

CEO Commentary “Our ongoing progress in securing major vendor authorisations with large-scale computing clients has positioned us at the centre of the data infrastructure buildout,” stated Aaron Jagdfeld, Chief Executive Officer.

While the commercial sector expanded at a rapid pace, the traditional home generator market saw minimal upward movement. According to company data, consumer division sales increased by just 1%, reaching $552.2 million compared to $548.7 million in the prior year.

This flatline performance strongly indicates that overall revenue growth now depends entirely on commercial sector execution. The company is no longer functioning primarily as a residential standby power business; it is actively transitioning into a critical infrastructure provider for the global technology sector.

Executive management did not rely solely on organic product sales to drive this quarter’s accelerated commercial performance. Instead, they actively bought their way into the data centre sector through a series of highly targeted corporate acquisitions.

These recent buyouts provided the immediate manufacturing capacity and specialised engineering talent required to service hyperscale technology clients. The 28% jump in commercial revenue correlates directly with the rapid integration of these newly acquired subsidiaries into the broader corporate supply chain.

As major technology firms dramatically accelerate their capital expenditures, the ongoing hardware supplier capex cycle is heavily rewarding companies that can physically deliver specialized data centre equipment without supply chain delays.

5 January 2026: The company completed the acquisition of Allmand, bringing in specialised industrial power equipment capabilities that immediately expanded the commercial product portfolio. 19 February 2026: Management finalised the buyout of Enercon, a strategic transaction specifically designed to accelerate operational growth within the highly lucrative data centre backup power market.

Understanding this precise acquisition timeline helps institutional and retail investors accurately evaluate management’s capital allocation strategy. The enhanced forward-looking financial projections rely heavily on the continued successful integration of these entities, proving that external capital deployment serves as the primary catalyst for current top-line expansion.

Financial markets inherently price in future performance expectations over historical quarterly results. Consequently, the most material aspect of the first-quarter update was management’s bold decision to issue significant upward revisions to their full-year financial forecasts.

The company now faces newly elevated operational targets that it must consistently achieve to maintain its current premium market valuation. These upgraded projections validate the aggressive commercial expansion strategy but also introduce new execution risks, as any failure to meet these heightened expectations next quarter could trigger sharp equity pullbacks.

The revised annual outlook includes two critical upward adjustments for the 2026 fiscal year:

These upgraded forecasts align closely with the bullish pre-earnings price targets established by major financial institutions. Canaccord Genuity had maintained a $300 price target heading into the morning report, while Needham held a $277 target alongside a maintained “Buy” rating. Following the 45-cent earnings beat, analysts across Wall Street are highly likely to recalibrate their financial models to accurately reflect the accelerated commercial timeline.

The first quarter of 2026 marks a definitive and structural transition for the entire business model. By successfully pivoting toward commercial data centre power solutions, the company has effectively insulated its balance sheet against the current sales stagnation occurring in the residential consumer market.

The substantial 45-cent earnings beat serves as clear, quantifiable market validation of this new corporate strategy. However, the recently upgraded financial guidance dictates that management must now accelerate their operational execution across all newly acquired subsidiaries. The primary challenge moving forward will involve scaling manufacturing capacity quickly enough to meet the surging infrastructure demands of the rapidly growing artificial intelligence sector.

For investors wanting to understand the broader macroeconomic forces driving this demand, our deep-dive into hyperscaler AI infrastructure spending breaks down the historic capital outlays fueling the semiconductor supercycle and the potential structural risks emerging across the US economy.

This article is for informational purposes only and should not be considered financial advice. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Generac reported a significant Q1 2026 earnings beat, with consolidated revenue reaching $1.059 billion and adjusted earnings per share of $1.80, exceeding analyst estimates.

Generac is actively transitioning from a primary reliance on residential home generators to becoming a critical infrastructure provider for the global technology sector, particularly focusing on commercial data center power solutions.

The commercial division's revenue grew by a substantial 28% to $510.1 million, while the consumer division's sales saw a minimal 1% increase, underscoring the success of the strategic pivot.

Generac upgraded its 2026 outlook due to the strong Q1 performance and successful commercial expansion, raising annual revenue growth projections to the mid-to-upper teens and elevating Modified EBITDA ratios.

Recent acquisitions of Allmand and Enercon in early 2026 provided Generac with immediate manufacturing capacity and specialized engineering talent, directly accelerating operational growth within the data center backup power market.