Record U.S. Equity Inflows Signal Fragility, Barclays Warns

3 mins ago

For the better part of a year, the consensus on Wall Street was not whether the Federal Reserve would cut rates, but when. That consensus is now gone.

Markets have moved to pricing in something no one was forecasting at the start of 2026: a rate hike. Jerome Powell’s address on 30 June 2026 arrived against a backdrop where two structurally different inflation forces have combined to strand the easing cycle entirely. An oil shock tied to Middle East conflict lit the first fuse; AI-driven semiconductor inflation is now doing something potentially more durable.

Together, those forces have pushed several Federal Open Market Committee (FOMC) members toward advocating for at least one hike before year-end, with CME FedWatch pricing roughly two-thirds odds on that outcome. Here is what those two forces actually are, why one is fading while the other is building, and what the resulting policy environment means for rate-sensitive assets heading into the second half of 2026. If you have been positioning for a rate-cut environment, this is the read that explains precisely what changed and why.

Entering 2026, the debate among macro forecasters was about timing, not direction. Most Wall Street desks assumed a gradual Fed easing path. The question was whether cuts started in Q1 or Q2, not whether they would happen at all.

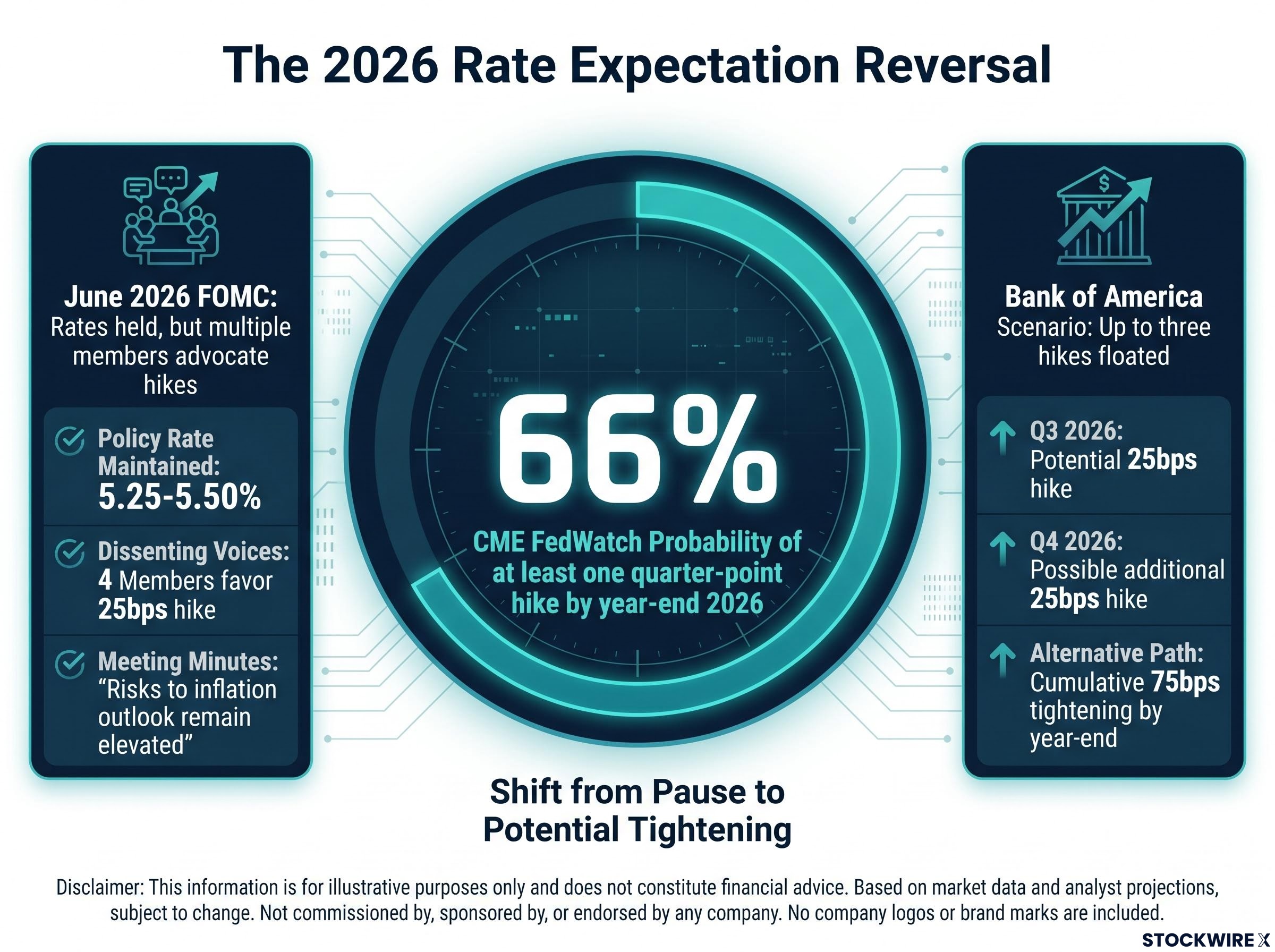

The June 2026 FOMC meeting shattered that framing. The committee held rates unchanged, but the signal underneath was striking: several committee members put forward the case for raising rates at least once before the year is out.

The June 2026 FOMC regime shift went beyond the rate decision itself: new Chair Kevin Warsh stripped forward guidance from the policy statement entirely, recentring the Fed’s communication architecture on strict data-dependency at the precise moment inflation sits 130 basis points above target.

The market mechanism that quantifies how completely a narrative has flipped is the CME FedWatch tool, and its current reading leaves little room for ambiguity.

CME FedWatch now assigns roughly two-thirds probability to at least one quarter-point hike by year-end 2026, with rate cuts effectively priced out entirely.

The key data points that define the reversal:

The speed and completeness of this reversal matters directly for positioning. Any portfolio built on a falling-rate assumption in early 2026 is now operating in the wrong regime, and this is not a minor recalibration. It is a directional change with compounding effects across bonds, equities, and consumer credit.

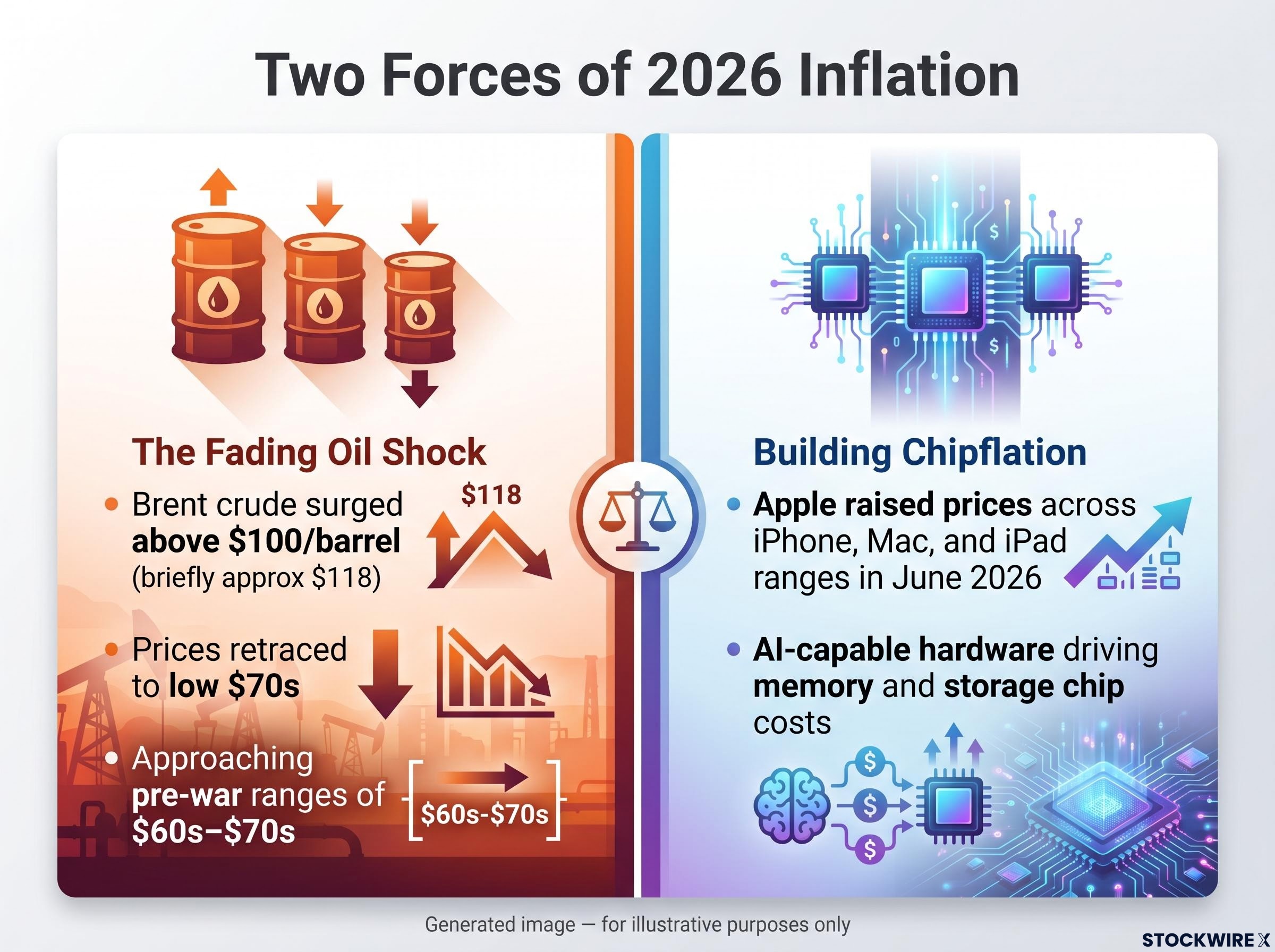

The Iran conflict-linked crude spike was the first and most visible inflation catalyst of 2026. Benchmarks surged above $100 per barrel, with reports of prices briefly reaching approximately $118 (not independently confirmed). Energy costs fed through into transportation, manufacturing, and broader goods prices with speed that reminded markets how quickly an oil shock can move headline inflation.

For a stretch of early 2026, crude was the inflation story. Then the geopolitics shifted.

After the U.S.-Iran agreement came through, Brent crude fell back sharply. Prices dipped into the low $70s, approaching pre-war ranges in the $60s-$70s. The speed of the retracement matched the severity of the initial spike.

But here is the signal that matters: even as oil normalised, overall inflation remained elevated. Energy’s contribution to headline Consumer Price Index (CPI) began fading, yet the Fed’s hawkish posture did not soften. That gap between oil normalisation and persistent inflation is what told markets another source was at work.

The oil price trajectory moved through three distinct stages:

For investors watching headline CPI, the fading oil premium is genuinely good news on energy. But it also removes the comforting argument that inflation will resolve itself naturally as crude normalises, because a second and more persistent source is still building.

The term “chipflation” has emerged from institutional research to describe a force that has no recent precedent in monetary policy: AI-driven price increases in advanced semiconductors and memory chips. A related term, “memflation,” captures the specific pressure on memory and storage components. Both describe sharp rises in integrated circuit and memory prices, which according to several research houses could drive another bout of global goods price inflation in 2026 and push semiconductor revenues to multi-decade highs (not independently confirmed).

When Apple, a company historically willing to absorb cost pressures to protect market positioning, raises visible retail prices, the underlying cost signal is credible and material.

During June 2026, Apple raised prices across its iPhone, Mac, and iPad ranges, pointing directly to surging memory and storage chip costs driven by the demands of AI-capable hardware as the reason for the move. When a company with Apple’s pricing discipline decides absorption is no longer tenable, every other device maker in the industry faces the same cost pressure or worse.

The memory chip price dynamics driving Apple’s June price hikes trace back to a structural supply squeeze: Samsung, SK Hynix, and Micron have collectively redirected capacity toward high-margin HBM for AI data centres, tightening commodity DRAM availability at precisely the moment consumer device demand is rising.

The structural difference between this force and the oil shock is what makes chipflation harder for the Fed to dismiss.

| Attribute | Oil Shock | Chipflation | Why it matters |

|---|---|---|---|

| Origin | Geopolitical conflict | AI infrastructure demand boom | One can be resolved diplomatically; the other is tied to a multi-year adoption cycle |

| Timeline to resolution | Weeks to months (diplomacy) | Years (fab capacity expansion) | Advanced node capacity cannot be scaled in quarters |

| Policy treatment | Traditionally “looked through” as transitory | No historical precedent for Fed to cite as transitory | The Fed lacks a playbook for AI-linked goods inflation |

| Investor implication | Energy hedges and commodity rotation | Technology thesis and inflation thesis in direct tension | The AI growth story and the inflation story are the same story |

Chipflation introduces an inflation dynamic directly linked to the AI adoption boom. That means the technology investment thesis and the inflation thesis now point in opposite directions for the same set of assets. You need to hold both views simultaneously.

The Fed is not managing a single inflation shock. It is managing two simultaneous and structurally distinct sources of price pressure, and that dual-track structure creates analytical complexity that a pure energy shock or a pure demand surge would not.

The policy logic works like this: the receding force (oil) reduces the argument for multiple aggressive hikes. But the building force (chipflation) is structural and multi-year. When those two dynamics operate at the same time, the rational central bank response is not to ease but to hold or tighten modestly, because easing into a building structural force risks losing credibility on inflation expectations entirely.

The June 2026 FOMC meeting reflected exactly this calculus. Rates held, but the committee saw several members push for tightening before year-end. The “higher for longer” characterisation now describes the baseline, not a tail risk.

The embedded-inflation risk runs through three channels:

Central banks in a dual-force inflation environment tend to lean hawkish to protect inflation-expectation anchoring, even when headline growth and employment remain stable. This is especially true when one of the forces, AI chipflation, is novel and lacks a historical precedent the Fed can cite as definitively transitory.

The reader should understand that the Fed’s caution is not about any single data point. It is about the risk that two inflation sources arriving together will anchor expectations in a way that forces more aggressive action later if not addressed now. That distinction is what separates correct interpretation of Fed communications in the second half of 2026 from the common error of treating a drop in oil prices as a dovish signal.

The macro argument translates into concrete portfolio consequences across three asset classes, and the effects are arriving simultaneously.

Fixed income and duration face the most direct pressure. The new baseline of “higher for longer plus one hike probability” pushes implied yields higher and increases refinancing risk for rate-sensitive sectors such as real estate and utilities. With FedWatch showing high odds of at least one hike and effectively no cuts priced into late 2026, the duration risk is not speculative. It is embedded in market pricing today.

The irony is acute: the very AI and semiconductor ecosystems driving structural goods inflation are also the ones most sensitive to an upward shift in discount rates.

AI and technology equities sit at the centre of a feedback loop. Strategists warn that as hike probability rises, price-to-earnings (P/E) multiples on major AI stocks face compression, even as those companies are generating the chipflation that sustains the hawkish rate environment. The growth thesis and the valuation headwind originate from the same source.

Discount-rate compression is the mechanism that transmits a rate-hike environment into equity valuations even when corporate earnings are growing: rising yields reduce the present value of future cash flows and shrink P/E multiples, with high-duration sectors such as technology suffering the largest mark-to-market losses.

Consumer credit and housing complete the picture. Mortgage, auto loan, and credit card borrowing costs face upward pressure through late 2026. Households are already absorbing higher prices for AI-enabled devices and residual energy costs, compressing real purchasing power at the margin.

| Asset class | Direct rate mechanism | Specific risk in H2 2026 | Investor action to consider |

|---|---|---|---|

| Fixed income | Higher implied yields, wider credit spreads | Refinancing risk in real estate and utilities | Review duration exposure and sector concentration |

| AI and tech equities | Rising discount rates compress P/E multiples | Multiple compression in the sector generating chipflation | Stress-test AI holdings against a one-hike scenario |

| Consumer credit | Upward pressure on mortgage and borrowing rates | Reduced household spending capacity | Monitor consumer-discretionary exposure for demand softening |

For an investor holding a standard 60/40 or tech-heavy portfolio built on the 2025 rate-cut assumption, this repricing creates simultaneous headwinds across bonds, equities, and household demand. Recognising all three at once is what separates coherent 2026 positioning from reactive adjustments.

The analytical argument above becomes testable through four observable signals. Each one carries a directional test that maps to a specific policy outcome.

For investors wanting to stress-test AI equity holdings against the hike scenario the article outlines, our deep-dive into AI capex and equity valuations examines the 18-24 month lag between hyperscaler spending commitments and revenue realisation, quantifying the valuation risk already embedded in the semiconductor sector before rate pressure is applied.

The key question in every FOMC statement and press conference for the rest of 2026 is whether policymakers describe AI-linked goods inflation as transitory or structural. That single word choice governs the number of hikes.

If the Fed characterises chipflation as a one-off adjustment tied to a specific investment cycle, one hike or none is the likely outcome. If policymakers begin framing it as persistent and embedded, the door opens to additional tightening. Powell’s 30 June address is the most recent data point; follow-up communications in July and August will be the next scheduled opportunities to clarify this framing.

These four signals give you a personal watchlist you can track in real time, rather than waiting for the next FOMC announcement to find out whether the rate environment has shifted underneath your positions.

The expected rate-cut tailwind has not arrived, and the probability of a rate-hike headwind is now non-trivial. CME FedWatch’s roughly two-thirds probability of at least one hike is the market’s current best estimate, and it reflects a regime change, not a temporary recalibration.

The two forces driving this environment have different durability profiles. Oil normalisation is reducing near-term headline pressure. AI chipflation, tied to multi-year fab investment timelines, ensures structural goods inflation persists into 2027. The net inflation trend is not clearly downward.

Three positioning implications follow:

This is not a macro environment where waiting for the Fed to pivot dovish is a viable positioning strategy. The structural inflation source has a multi-year timeline that the Fed will increasingly treat as requiring a policy response rather than patient observation. The old assumptions no longer hold, and the sooner your portfolio reflects the new regime, the better positioned you are for what the second half of 2026 delivers.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

—

Chipflation refers to AI-driven price increases in advanced semiconductors and memory chips, caused by manufacturers redirecting capacity toward high-margin AI data centre components, which tightens supply for consumer devices. Apple's June 2026 price hikes across iPhone, Mac, and iPad lines, attributed directly to surging memory and storage chip costs, confirm the pressure is real and spreading.

Two simultaneous inflation forces have reversed the rate-cut consensus: an oil shock tied to Middle East conflict pushed crude above $100 per barrel, and AI-driven semiconductor inflation is now driving structural goods price increases that the Fed cannot easily dismiss as transitory. CME FedWatch assigns approximately 66% probability to at least one quarter-point hike before year-end 2026.

The U.S.-Iran agreement triggered a sharp crude retracement, with Brent falling to the low $70s from above $100, reducing energy's contribution to headline CPI. However, overall inflation remained elevated after oil normalised, confirming that chipflation, not energy, is now the more persistent and policy-relevant inflation driver.

Rising hike probability compresses price-to-earnings multiples on AI and technology equities by increasing discount rates, which reduces the present value of future cash flows. The feedback loop is self-reinforcing: the same AI infrastructure boom generating chipflation is also the source of the valuation headwind now facing the sector.

The four key signals are: Brent crude relative to the $60s-$70s pre-war range, semiconductor and electronics producer price data beyond Apple's initial hikes, AI data-centre capex and power cost trends, and FOMC language on whether chipflation is framed as transitory or structural, with Powell's July and August communications being the next scheduled clarification points.