Lululemon Plunges 12% on CEO Pick Amid Activist Investor Battle

1 hr ago

On 29 April 2026, Etsy shares surged 6.3% following the release of the company’s first-quarter financial results. This positive market reaction to the latest Etsy earnings report reflects a significant milestone for the United States e-commerce platform. Investors responded favourably to the company achieving its first quarter-over-quarter expansion in active purchasers in 24 months, a metric that had previously pressured the stock valuation.

This article unpacks the underlying metrics driving the morning stock pop and the mechanics of the platform turnaround. It also analyses what the recent Depop divestiture means for the company’s standalone valuation moving forward.

The market reaction on Wednesday morning highlighted a clear investor preference for top-line growth over minor profitability shortfalls. According to company data, first-quarter revenue reached $631.3 million, exceeding the pre-earnings Wall Street consensus estimate of $617 million by 1.6%. This revenue beat provided the foundation for the stock valuation increase, successfully anchoring investor confidence in the platform’s core commercial engine.

Conversely, the company recorded a slight earnings per share miss to provide a balanced picture of quarterly profitability. According to company data, adjusted earnings per share landed at $0.60, falling narrowly short of the $0.62 forecast, while pre-earnings Zacks Consensus Estimates had projected slightly different benchmarks. However, according to company data, the company achieved $185 million in adjusted EBITDA, representing a healthy 29.3% margin.

The pre-earnings Zacks Investment Research consensus estimates established the strict baseline expectations for the marketplace, making the ultimate revenue outperformance a clear catalyst for the morning share price rally.

Retail and institutional investors are currently prioritising revenue generation and user acquisition metrics across the broader consumer technology sector. The combination of strong top-line growth and healthy profit margins overshadowed the marginal earnings miss, explaining why the market ultimately rewarded the stock. These figures establish a solid financial baseline for the first quarter.

| Metric | Q1 2026 Actual | Wall Street Estimate |

|---|---|---|

| Revenue | $631.3 million | $617 million |

| Adjusted EPS | $0.60 | $0.62 |

| Adjusted EBITDA Margin | 29.3% | N/A |

To understand the positive market reaction, investors must look beyond abstract financial figures to the actual customer base. E-commerce platforms rely heavily on Gross Merchandise Sales, which represents the total dollar value of items sold across the marketplace within a specific period. This metric functions as the clearest indicator of overall marketplace health, capturing exactly how much money is flowing through the ecosystem before platform fees are applied.

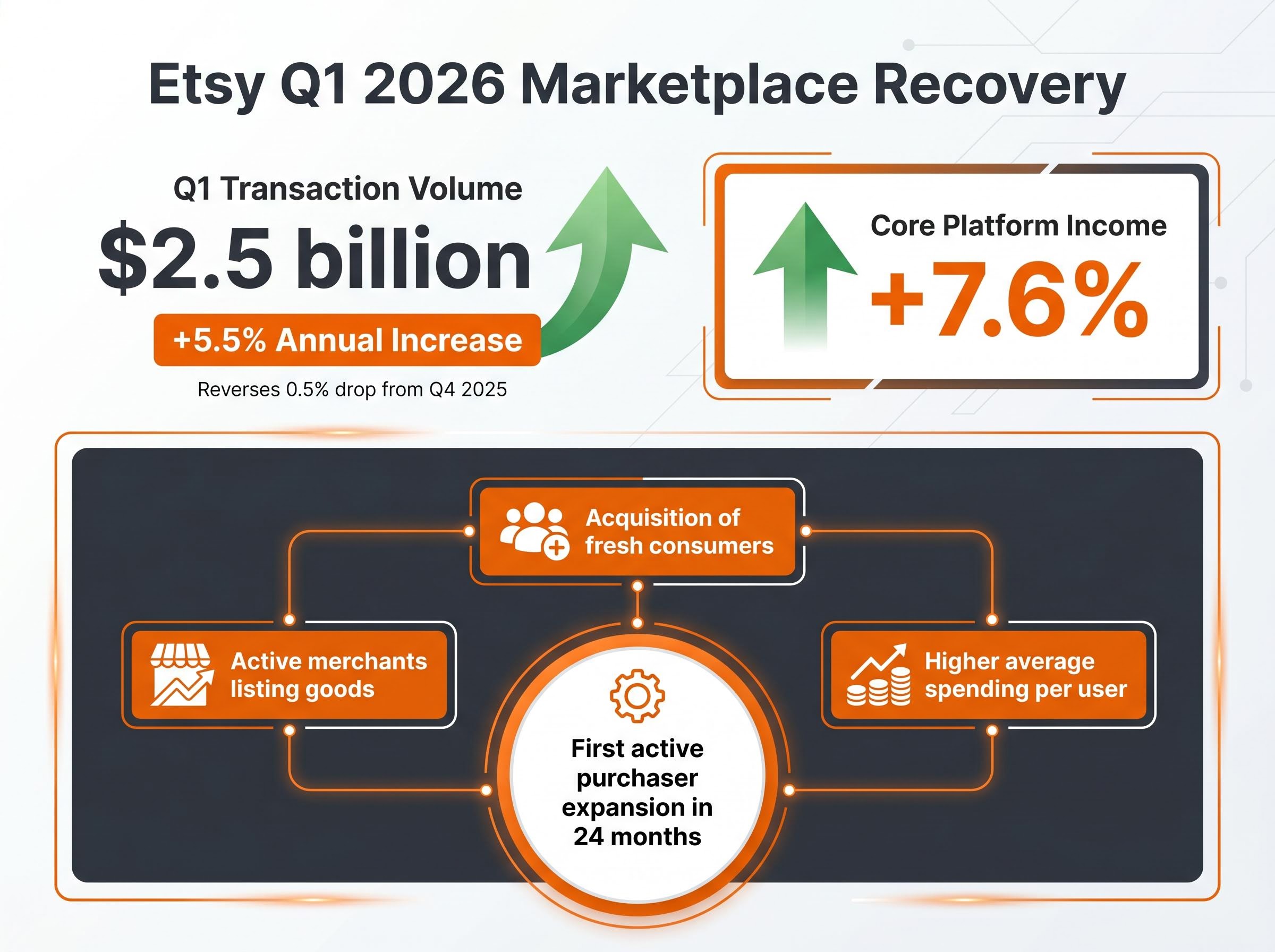

According to company data, first-quarter transaction volume hit $2.5 billion, a 5.5% annual increase that successfully reversed the 0.5% drop from the final quarter of 2025. Furthermore, core platform income expanded by 7.6% compared to the same period last year. The most important signal of platform health was the quarter-over-quarter active purchaser expansion, which finally broke a sustained two-year period of contraction.

The official SEC Form 8-K filing details this transaction volume recovery, providing the regulatory documentation that confirmed the marketplace’s return to active buyer expansion.

“The reversal of a 24-month decline in active purchasers provides the first concrete evidence that the marketplace is successfully retaining users in a highly competitive retail environment.”

The company reported simultaneous growth across multiple user engagement categories to show this is a broad recovery rather than an isolated metric. This broad expansion includes three specific areas:

A sustained annual increase in active merchants listing goods Consistent acquisition of fresh consumers onto the platform * An upward trend in average spending per individual user

The combination of higher average spending and new consumer acquisition creates a compounding effect on total transaction volume. When more users join the platform and simultaneously spend more money per visit, the overall marketplace generates exponentially higher baseline revenue. Wall Street analysts look for this specific combination of metrics to confirm a sustainable turnaround, as it proves the company can scale its transaction volume without relying purely on seasonal discounting.

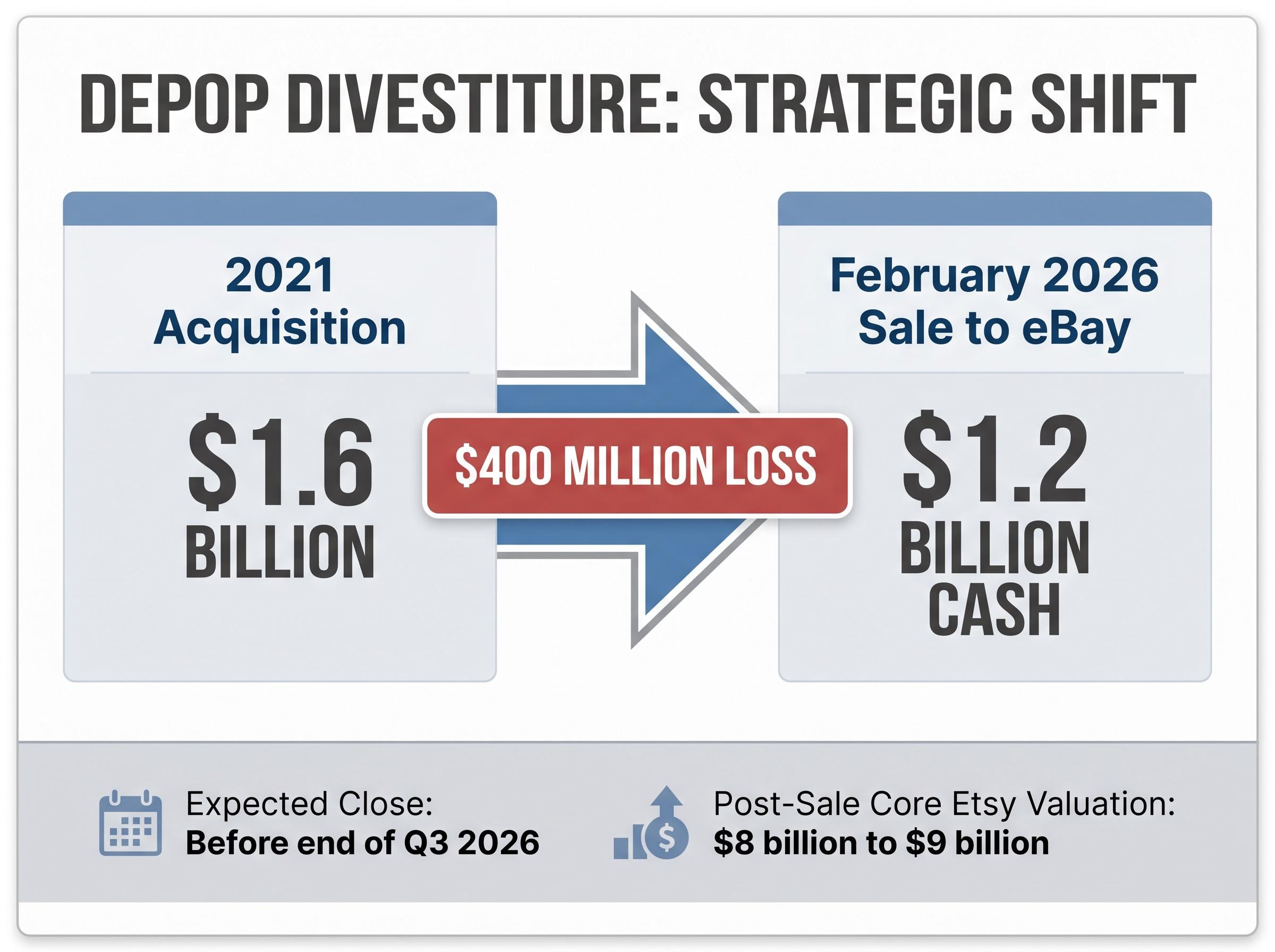

The earnings report arrives within a larger structural shift for the company, following a calculated move to streamline operations. In February 2026, management announced an agreement to sell the fashion resale app Depop to eBay in a $1.2 billion cash transaction. Because of this pending divestiture, Depop’s operational data is omitted from the core financial results reported in this quarter.

This divestiture represents a strategic decision to focus entirely on the core handmade goods marketplace and emerging artificial intelligence commerce tools. The cash sale represents a $400 million loss against the original $1.6 billion acquisition price paid in 2021. However, shedding a sprawling portfolio for a leaner operation allows the company to direct capital toward higher-margin initiatives like agentic commerce features.

The transaction remains subject to customary closing conditions and regulatory approvals, but it is expected to close before the end of the third quarter of 2026. Post-sale standalone valuation for the core business is estimated between $8 billion and $9 billion. This structural adjustment helps explain the market’s willingness to reward the stock, as investors anticipate a more focused, efficient enterprise.

For investors evaluating the competitive implications of this transaction, our detailed coverage of the Etsy Depop sale explores how shedding the asset allows the platform to defend its artisanal moat while eBay consolidates the apparel resale market.

Markets function as forward-looking mechanisms, and management provided clear benchmarks to maintain the current stock momentum. The forward guidance outlined specific projections for the second quarter to show immediate near-term confidence in the ongoing recovery. Profit margins are expected to remain stable through the remainder of the year, providing a reliable floor for institutional investors concerned about escalating operational costs.

Management expects sustained, albeit lower single-digit, expansion across the full calendar year. These projections give retail and institutional stakeholders exact benchmarks that the company must hit in the coming quarters to justify its current valuation.

Achieving this projected baseline relies heavily on upcoming quarterly performance, making the annual margin assessment a critical catalyst for institutional shareholders evaluating the stock trajectory.

The company’s immediate and full-year forward guidance includes:

Second-quarter transaction volumes projected between $2.48 billion and $2.53 billion, indicating a 3% to 5% annual expansion rate Second-quarter fee capture rate estimated near 25.7%, with adjusted EBITDA profitability ranging from 27% to 29% * Full-year adjusted EBITDA margins projected to settle between 28% and 30%

Strong top-line revenue and a critical reversal in user metrics successfully overshadowed the minor first-quarter profit miss. The pending Depop sale leaves the company structurally leaner and solely reliant on its core marketplace, removing distraction from management’s operational focus. This structural shift positions the platform to capitalise on its recent active purchaser expansion while developing targeted artificial intelligence shopping tools.

The primary challenge for management is maintaining this newly recovered transaction volume momentum through the vital holiday quarters of 2026. If the current combination of new consumer acquisition and higher average spending persists, the core marketplace will enter the second half of the year from a highly strengthened position.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results, and forward-looking statements regarding platform growth or acquisitions are subject to market conditions and regulatory approvals.

Etsy's stock surged because the company reported strong first-quarter revenue that beat Wall Street estimates and, critically, achieved its first quarter-over-quarter expansion in active purchasers in two years. This turnaround in user metrics overshadowed a minor profit miss.

The sale of Depop allows Etsy to streamline its operations and focus entirely on its higher-margin core handmade goods marketplace and emerging artificial intelligence commerce tools. This strategic move aims to enhance efficiency and capital allocation for the standalone business.

Etsy's first-quarter revenue of $631.3 million exceeded Wall Street's $617 million consensus estimate, while adjusted earnings per share of $0.60 narrowly missed the $0.62 forecast. Despite the slight EPS miss, the revenue beat and healthy adjusted EBITDA margin pleased investors.

Gross Merchandise Sales (GMS) represents the total dollar value of items sold across a marketplace. Etsy's Q1 2026 GMS increased by 5.5% annually to $2.5 billion, successfully reversing a previous decline and indicating a healthy recovery in marketplace activity.

Etsy's forward guidance for 2026 signals cautious optimism, projecting sustained, lower single-digit expansion across the full calendar year. Management expects stable profit margins, with full-year adjusted EBITDA margins settling between 28% and 30%.