ASX 200 Enters June 2026 With Stretched Valuations and Upside Risk

11 hrs ago

Markets have priced in roughly 56 basis points of total European Central Bank (ECB) tightening through December 2026, but UBS economists warn that figure may be too low. With the ECB’s June 11, 2026 policy meeting days away, a 25 basis point rate hike is widely considered a foregone conclusion. UBS has shifted its analytical focus to the question that carries more weight for investors: what happens after June, and whether current market positioning adequately accounts for it.

UBS economists, led by Reinhard Cluse, have outlined a base case that includes a second hike in September, flagged upside risk for a potential July move, and identified a stagflationary revision pattern in the ECB’s forthcoming macroeconomic projections. For investors with European fixed income or rate-sensitive equity exposure, the gap between what is priced and what is plausible represents a material positioning risk heading into the second half of 2026.

The June 11 rate decision is, for practical purposes, already settled. UBS views a 25 basis point hike, bringing the deposit facility rate to 2.25%, as a near-certainty. ECB President Christine Lagarde’s remarks at the April 30 meeting, alongside subsequent statements from board members Isabel Schnabel and Philip Lane, cemented expectations weeks ago.

The ECB April 30 monetary policy statement confirmed the deposit facility rate held at 2.00%, providing the formal baseline from which the June 11 hike to 2.25% is expected to move, and anchoring the rate path projections that UBS is now warning markets have underpriced.

According to Reuters, citing ECB insider sources, the June hike was described as “nearly finalised” while a July move remained “entirely undecided.”

UBS explicitly ruled out a 50 basis point adjustment. The reasoning: inflation dynamics in the current cycle are less acute than those seen during the 2022-2023 tightening phase, and the risk of pro-inflationary secondary effects, particularly through wages, has substantially diminished.

That distinction matters. The June decision carries little new information for markets. Investors who treat it as the story risk missing the more consequential policy question already forming behind it: how many more hikes follow, and how quickly.

The ECB’s June 11 decision does not arrive in isolation: a compressed June policy window also delivers the Bank of Japan, Federal Reserve, and Bank of England within the same eight-day stretch, concentrating cross-asset repricing risk and reducing the sequential digestion time markets typically rely on after any single central bank move.

The core of UBS’s warning is not about June. It is about what comes after.

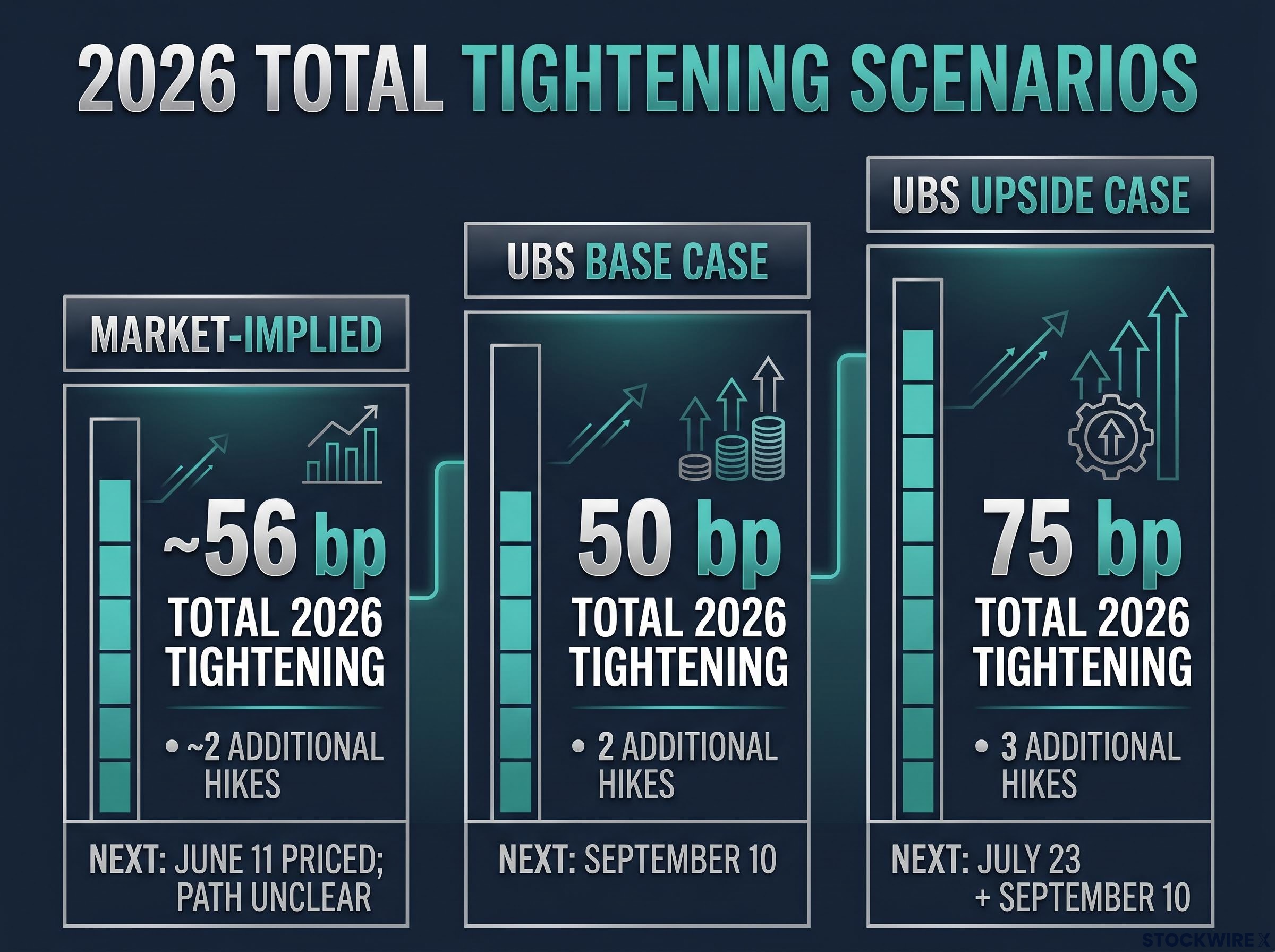

Market-implied pricing, as of publication, points to approximately 56 basis points of total ECB tightening through December 2026. UBS’s base case calls for two separate 25 basis point increases across the year, with the second hike arriving at the September 10 meeting rather than July 23. That base case alone accounts for 50 basis points, leaving the gap between market pricing and UBS’s floor expectation narrow.

The more significant risk sits above the base case. UBS acknowledged upside scenarios in which a July hike adds to, rather than substitutes for, the September move. Press reports citing ECB sources have suggested the central bank may need a minimum of two hikes across 2026, with a third-hike scenario partially incorporated in market pricing. If that third hike materialises, the total tightening path reaches 75 basis points, well above what markets have currently positioned for.

| Scenario | Additional Hikes | Next Expected Date | Total 2026 Tightening (bp) |

|---|---|---|---|

| Market-Implied | ~2 | June 11 priced; path unclear | ~56 |

| UBS Base Case | 2 | September 10 | 50 |

| UBS Upside Case | 3 | July 23 + September 10 | 75 |

For investors with European duration exposure, the gap between the 56 basis points currently priced and a potential 75 basis point outcome represents a meaningful asymmetry. The surprise risk is skewed hawkish, not dovish.

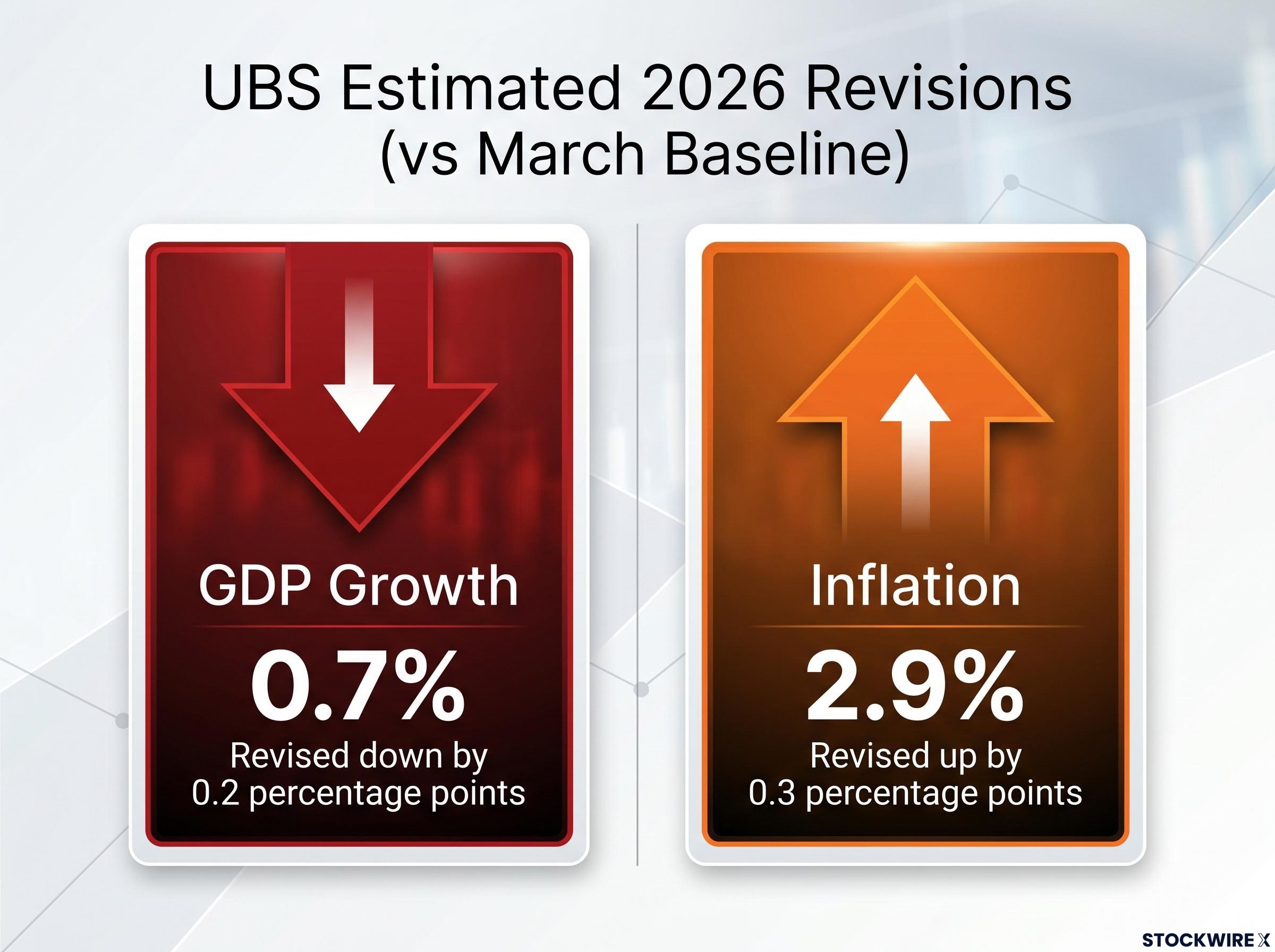

Alongside the rate decision, the June 11 meeting will deliver updated ECB staff macroeconomic projections. UBS expects the revisions to paint a difficult picture.

When a central bank simultaneously cuts its growth forecast while raising its inflation forecast, it faces a stagflationary bind: tightening policy to contain prices risks deepening a slowdown already underway. That is precisely the revision pattern UBS anticipates at the June meeting.

The March 2026 projections served as the ECB’s most recent formal economic assessment. UBS noted that the expected inflation revision, while worse than March’s central estimate, remains less severe than the ECB’s own adverse scenario published at the same meeting. Higher energy prices are the primary driver behind the upward inflation revision.

Energy prices are the primary driver behind UBS’s expected upward inflation revision, and the ECB rate repricing that followed Brent crude crossing $110 per barrel had already shifted market expectations toward 1-2 hikes before the June projections were published.

The practical consequence is straightforward. Slower growth combined with stickier inflation narrows the ECB’s room to pause its tightening cycle, reinforcing the case for further rate increases even as the economic backdrop softens.

Whether the next hike arrives in July or September depends on a specific set of economic variables. UBS identified five indicators that will serve as the ECB’s primary inputs for calibrating the post-June rate path.

UBS cited the diminished risk of a wage-price spiral, compared to the 2022-2023 cycle, as its stated reason for ruling out a 50 basis point hike. Any re-emergence of secondary inflationary effects through wages would materially alter the rate path.

These five indicators determine whether the July 23 meeting becomes a live policy event. Investors monitoring them will have advance visibility into the ECB’s thinking before the next decision lands.

The investment implications flow directly from the asymmetry in rate pricing. Markets have positioned for approximately 56 basis points of tightening. UBS’s base case sits at 50 basis points, and its upside scenario reaches 75 basis points. The gap means surprises are more likely to arrive on the hawkish side.

Rate-sensitive sectors are not the only channel through which additional ECB hikes transmit into European markets: private credit spillover risk, mapped by the ECB across approximately €425 billion in insurer, bank, and pension fund exposures, represents a secondary transmission mechanism where tighter monetary conditions could trigger second-round losses that exceed the initial direct credit hits.

Investors who treat the June hike as a closed chapter and shift attention elsewhere risk being caught offside by a faster-than-priced tightening cycle in the second half of 2026.

For investors with European fixed income exposure wanting to translate the rate path scenarios into specific portfolio adjustments, our comprehensive walkthrough of bond portfolio duration management covers how BlackRock, PIMCO, Vanguard, and J.P. Morgan Asset Management are positioning across the curve, with worked mechanics on how a 1 percentage point rate rise affects bonds at different duration levels.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements regarding ECB policy, including rate path projections and macroeconomic forecasts, are subject to change based on incoming economic data and policy developments.

The June hike is priced. What follows is not. UBS’s warning centres on a post-June tightening path that markets have not fully accounted for: stagflationary macro revisions that narrow the ECB’s room to pause, a potential July surprise that could add to rather than replace the September move, and a three-hike scenario that would push total 2026 tightening to 75 basis points.

The actionable focus from here: watch Lagarde’s June 11 press conference language for any shift toward July, monitor the five leading indicators UBS identified, and treat current rate pricing as a floor rather than a ceiling.

ECB rate hikes are increases to the European Central Bank's benchmark interest rates, most notably the deposit facility rate, which raise borrowing costs across the Eurozone. For investors, higher rates typically pressure bond prices, increase financing costs for rate-sensitive equities, and shift capital flows across European asset classes.

UBS economists expect at least two 25 basis point hikes in 2026, with a base case placing the second hike at the September 10 meeting. An upside scenario includes a third hike, potentially in July, which would bring total 2026 tightening to 75 basis points, above the roughly 56 basis points currently priced by markets.

The June 11 meeting is expected to deliver a near-certain 25 basis point hike to 2.25%, alongside updated staff macroeconomic projections. UBS anticipates those projections will show a stagflationary pattern, with growth revised down and inflation revised up, which would narrow the ECB's room to pause its tightening cycle after June.

UBS identified five key indicators: inflation expectations, wage growth, Eurozone GDP growth, employment and labour market data, and energy prices. A re-acceleration in any of these, particularly wages or energy costs, would increase the probability of the July 23 meeting becoming a live policy event.

European real estate and utilities are most exposed due to elevated debt loads and sensitivity to borrowing costs. Investors holding European fixed income duration are also at direct mark-to-market risk if the tightening cycle extends into September or accelerates with an earlier July hike.