The Structural Case for a Generation of Persistent Inflation

31 mins ago

Eurozone headline inflation hit 3.2% in May 2026, its highest reading since September 2023, and markets are pricing a 98-99% probability that the European Central Bank will raise interest rates on 11 June. The anticipated 25 basis point increase would be the ECB’s first rate hike in approximately three years. Yet one influential investment manager is arguing the move will do essentially nothing to fix the problem it claims to address.

The trigger is an energy price surge of 10.9% year-over-year, geopolitical in origin rather than demand-driven. That distinction matters. It shapes whether rate hikes can actually cool the inflation showing up in the data, or whether they risk tightening financial conditions into a supply shock the ECB cannot control.

This analysis breaks down why the type of inflation driving the eurozone’s current surge matters more than the headline number, what the hawkish case for action genuinely rests on, and why long-term investors should be watching the yield curve rather than the 11 June decision itself.

The ECB Governing Council meets on Wednesday, 11 June 2026, and the outcome is as close to a foregone conclusion as monetary policy gets. Market-implied probability of a 25 basis point hike stands at 98-99%, according to ECB Watch tool pricing. That would lift the deposit facility rate from 2.00% to 2.25%, the first increase since the ECB held rates steady in June 2025.

Market-implied probability of a June 2026 hike: 98-99%. The last time the ECB raised rates was approximately three years ago.

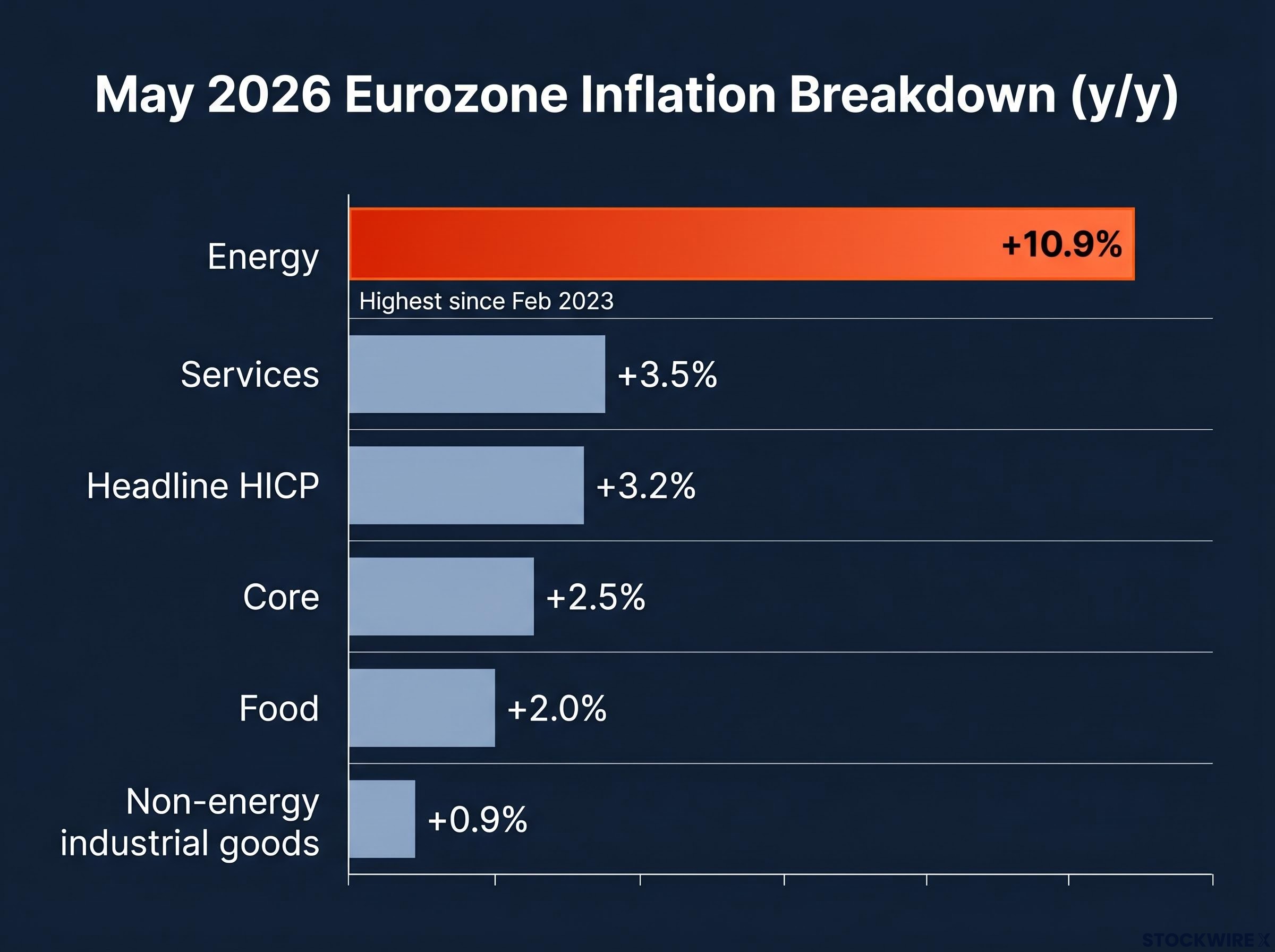

The data that cemented this consensus arrived in the May 2026 Harmonised Index of Consumer Prices (HICP) flash estimate. Headline inflation rose to 3.2% year-over-year, the fourth consecutive monthly increase and the highest since September 2023. The prior rate decision on 30 April 2026 kept rates unchanged, but the inflation trajectory since then closed the debate for most market participants.

The June 11 decision is, in that sense, a communication event as much as a policy event; ECB forward guidance on September tightening, and specifically whether Lagarde signals a conditional pause or an active hiking cycle, will carry more weight for EUR/USD and euro rate markets than the 25 basis points themselves.

The component breakdown, however, tells a less uniform story than the headline suggests.

| HICP Component | May 2026 (y/y) |

|---|---|

| Headline HICP | +3.2% |

| Energy | +10.9% |

| Services | +3.5% |

| Core (ex-energy and food) | +2.5% |

| Non-energy industrial goods | +0.9% |

| Food, alcohol and tobacco | +2.0% |

One component stands apart from the rest. Energy at +10.9% is running at more than three times the rate of any other category.

Start with the number doing the most work. Energy prices rose 10.9% year-over-year in May 2026, the highest since February 2023, and contributed the bulk of the 0.2 percentage point increase from April’s headline reading. Non-energy industrial goods, by contrast, rose just 0.9%. Food inflation sat at 2.0%, close to the ECB’s target.

The energy surge is not a story about European consumers spending too freely. It is a supply-side disruption, driven by geopolitical pressures including the Middle East conflict. Markets are already responding through adaptation mechanisms:

For context, the eurozone’s last major energy-driven inflation episode, following Russia’s 2022 invasion of Ukraine, peaked at 10.6% year-over-year. The current headline of 3.2% is nowhere near that level, but the energy component’s acceleration is what has markets on edge.

Core inflation (excluding energy and food) rose to 2.5% in May, up from 2.2% in April. Services inflation held at 3.5%. Both readings sit above the ECB’s 2% target, and both reflect wage and demand dynamics rather than energy pass-through.

This is where the hawkish case finds its strongest footing within the data itself. Core broadening above target suggests some degree of underlying price pressure that cannot be dismissed as a pure energy story. Sceptics counter that 2.5% core is elevated but not alarming, and that tightening into an energy shock risks compounding rather than resolving the problem.

The ECB is not acting carelessly. Four arguments underpin the consensus for a June hike, and each carries genuine weight:

The institutional memory of 2022 reinforces all four arguments. The ECB was criticised for starting its hiking cycle too late, which forced a steeper and more disruptive tightening path. Officials calibrated by that experience are predisposed to act early rather than risk a repeat. Whether the current episode resembles 2022 closely enough to justify that instinct is the central question.

Demand-driven inflation occurs when aggregate demand outstrips supply. Consumers and businesses are spending more than the economy can produce. Rate hikes work directly against this: raising the cost of borrowing restrains credit, dampens investment, and cools consumption. The mechanism is well understood, and the ECB has deployed it effectively in past cycles.

Energy-driven inflation works differently. When gas and oil prices spike because of geopolitical disruptions, the problem is insufficient supply rather than excessive demand. Rate hikes cannot produce more gas. They cannot reopen shipping lanes or reverse pipeline damage.

Both the ECB and the Federal Reserve operate a formal look-through framework for oil shocks driven by geopolitical supply disruption, treating them differently from demand-side price pressures on the basis that market adaptation, not rate hikes, is the primary correction mechanism for supply-constrained commodity spikes.

Fisher Investments characterises the anticipated June hike as misguided on precisely these grounds, arguing the ECB is applying the wrong tool to the wrong problem.

According to Fisher Investments, rate hikes “cannot address the underlying causes” of energy-driven inflation, and higher energy costs in the absence of a comparable money supply surge are more likely to trigger household and business adaptation than broad-based inflation.

ECB officials are psychologically anchored to the 2022 inflation episode, when eurozone CPI peaked at 10.6% year-over-year following Russia’s invasion of Ukraine. That episode involved a comparable money supply expansion alongside the energy shock, which is why inflation became broad-based and persistent.

Fisher Investments argues the current episode differs on this specific point. There is no comparable money supply surge accompanying the 2026 energy disruption. Markets are already adapting through rerouted shipping, alternative pipelines, and eased restrictions.

This distinction, between a supply shock accompanied by monetary expansion and one without it, is where the entire policy debate lives. If the ECB has diagnosed the current inflation as structurally similar to 2022, it will hike. If the diagnosis is wrong, the rate increase addresses a problem that does not exist while creating new risks that do.

If the June hike were a one-off, the debate would be largely academic. A single 25 basis point increase from 2.00% to 2.25% is unlikely to materially alter the growth trajectory. The more consequential question is what happens if the ECB continues hiking because energy prices remain elevated.

The eurozone growth constraints that make the ECB’s position uniquely difficult are visible in the GDP data: Q1 2026 expansion of just 0.1% quarter-on-quarter means the ECB is contemplating a hiking cycle against an economy growing at near-stall speed, a combination that amplifies the overtightening risk Fisher Investments is flagging.

Fisher Investments flags yield curve inversion as the specific risk long-term investors should monitor.

Fisher Investments characterises yield curve inversion from potential ECB over-tightening as “the more significant risk for long-term investors,” though notes it has not yet materialised.

Yield curve inversion occurs when short-term interest rates rise above long-term rates, compressing the difference between them. It is a signal that bond markets expect weaker future growth and eventual rate cuts. When a central bank pushes policy rates well above the neutral rate, it compresses term premia and effectively tells markets it is willing to sacrifice growth to fight inflation.

The ECB’s own Bank Lending Survey shows that higher policy rates translate into stricter lending standards, with small and medium enterprises and households most exposed to tighter credit conditions. Continuing to hike into already restrictive lending conditions risks amplifying drag on investment and housing.

The ECB Bank Lending Survey for Q1 2026 recorded tightening credit standards across loans to firms and households, with SMEs and consumer credit segments showing the sharpest deterioration, adding empirical weight to concerns that further rate increases would amplify existing drag rather than address a demand problem.

Monetary policy also transmits with significant lags. If energy prices normalise through market adaptation before hikes fully affect the economy, the ECB may have over-tightened relative to where inflation actually settles. The cumulative effect of multiple rate increases could prove excessive in retrospect.

Hawkish counterarguments attempt to pre-empt precisely this concern by arguing that acting early and forcefully reduces the total tightening required, keeping the cumulative overshoot risk manageable. The tension between acting early enough and acting too much is not new, but it is sharpened when the dominant inflation driver sits outside the reach of monetary policy.

The June 11 decision is effectively priced in. Whether the hike is the right call depends on a diagnosis that reasonable economists disagree on: is the eurozone facing a demand problem that rate hikes can cool, or a supply problem that rate hikes cannot fix?

Fisher Investments characterises the single hike as misguided but notes that bond markets are currently pricing the rate outlook appropriately. The immediate risk is not the 25 basis points themselves. It is the signal the decision sends about how the ECB reads the inflation data, and whether a hiking cycle follows.

Yield curve inversion has not materialised. If it does, it will tell investors that markets believe the ECB has overtightened. Until then, the energy-driven versus demand-driven inflation distinction remains the decisive analytical frame for evaluating every ECB communication that follows.

Central banks calibrated to fight demand-driven inflation with rate hikes face a structural limitation when the dominant driver is geopolitical and supply-side. The 11 June meeting will reveal which diagnosis the ECB has made. What matters more is what comes after.

For investors wanting to understand how persistent above-target inflation historically affects equity valuations, our full explainer on energy-driven inflation and equity returns examines cross-border CPI data across four major economies and the evidence on equities as a long-run store of purchasing power through inflationary cycles.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results, and financial projections are subject to market conditions and various risk factors.

A supply-side inflation shock occurs when prices rise due to constrained supply rather than excessive consumer demand, as is the case with the current eurozone energy surge driven by geopolitical disruption. This matters because rate hikes are designed to cool demand, meaning they cannot directly resolve a supply problem and risk slowing an already fragile economy without fixing the underlying cause.

Yield curve inversion occurs when short-term interest rates rise above long-term rates, signalling that bond markets expect weaker future growth and eventual rate cuts. Fisher Investments has identified potential ECB over-tightening as the primary risk that could trigger inversion, making it the key indicator for long-term investors monitoring the consequences of the June 2026 ECB rate hike cycle.

Core inflation excludes volatile energy and food prices to measure underlying price pressures from wages and demand, whereas headline inflation includes all components. In May 2026, eurozone headline inflation was 3.2% driven heavily by a 10.9% energy surge, while core inflation stood at 2.5%, reflecting more moderate but still above-target demand-side pressure.

The ECB is widely expected to raise its deposit facility rate by 25 basis points from 2.00% to 2.25% at its 11 June 2026 meeting, which would be the first rate increase in approximately three years. Market-implied probability of this move stands at 98-99% following the May 2026 HICP flash estimate showing headline inflation at a 33-month high of 3.2%.

During the 2022 episode, a comparable money supply expansion accompanied the energy shock, which helped inflation become broad-based and persistent, with eurozone CPI peaking at 10.6% year-over-year. Fisher Investments argues the 2026 episode differs because there is no comparable money supply surge alongside the energy disruption, making broad-based persistent inflation less likely and rate hikes a potentially mismatched policy response.