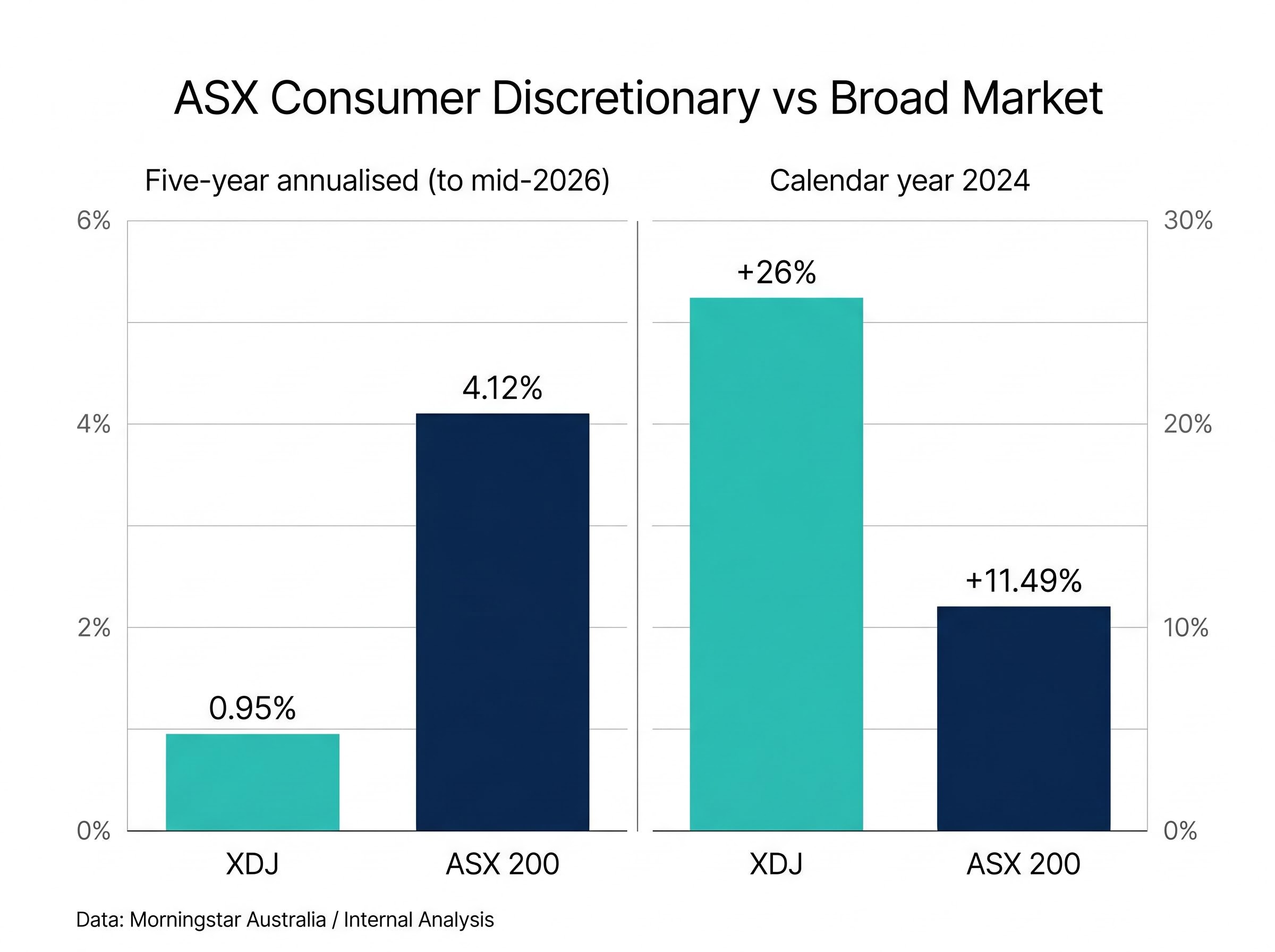

The ASX consumer discretionary sector delivered annualised returns of roughly 0.95% over the five years to mid-2026. The S&P/ASX 200 returned approximately 4.12% per year over the same period. A sector built on products Australians recognise, shop for, and interact with daily has materially underdelivered for investors who held it.

The gap is not a single bad year or a stretch of poor luck. It reflects structural dynamics tied to interest rate sensitivity, consumer balance sheets, and the way cyclical earnings compress when household budgets tighten. Those dynamics are increasingly relevant now, as the Reserve Bank of Australia (RBA) moves into an easing cycle and retail investor attention returns to the sector. What follows is an examination of why the underperformance occurred, what mechanisms drove it, and what investors need to evaluate carefully before concluding that familiarity with these businesses translates into investment edge.

Five years of trailing the market: what the numbers actually show

The core gap: Over five years to mid-2026, the S&P/ASX Consumer Discretionary Index (XDJ) returned approximately 0.95% annualised, against the ASX 200’s 4.12% per year (internal analysis, consistent with available sector commentary).

That gap, compounded over half a decade, represents a material divergence in investor outcomes. A dollar allocated to the broader index meaningfully outgrew one allocated to the discretionary sector.

Then 2024 complicated the picture. In calendar year 2024, the XDJ delivered approximately +26% in price returns, against the ASX 200’s +11.49% total return, according to Morningstar Australia. Consumer discretionary was not merely keeping pace; it was among the stronger-performing sectors on the ASX that year.

| Timeframe | XDJ Return | ASX 200 Return |

|---|---|---|

| Five-year annualised (to mid-2026) | ~0.95% | ~4.12% |

| Calendar year 2024 | ~+26% | ~+11.49% |

A single strong year does not erase a multi-year structural shortfall. What it does is raise the question of what conditions produced each outcome, and whether the forces behind the longer underperformance have genuinely shifted or merely paused.

When big ASX news breaks, our subscribers know first

What consumer discretionary actually means as an investment category

The label “consumer discretionary” describes spending that households cut first when budgets tighten. These are goods and services that people want but do not need in the same way they need groceries, utilities, or healthcare. That distinction from consumer staples is the sector’s defining economic characteristic, and it is the reason performance is so sensitive to the household income cycle.

The consumer staples drawdown profile on the ASX tells a different story from discretionary: the XSJ recorded a maximum drawdown of approximately -9% in 2025 against roughly -15% for the ASX 200, illustrating how the same household budget pressure that compresses discretionary earnings provides a relative floor for non-essential spending categories.

On the ASX, the sector spans a broader range of businesses than many retail investors appreciate:

- Big-ticket retail: Harvey Norman (ASX: HVN), covering furniture, appliances, and home goods

- Electronics: JB Hi-Fi (ASX: JBH), a value-positioned consumer electronics retailer

- Apparel and leisure: Super Retail Group (ASX: SUL) and Premier Investments (ASX: PMV), spanning auto accessories, outdoor, and specialty fashion brands

- Diversified retail: Wesfarmers (ASX: WES), operating Bunnings, Kmart, and Target, a portfolio that straddles discretionary and staples-adjacent formats

- Gaming: Aristocrat Leisure (ASX: ALL), a technology-driven business with a less visible connection to household consumption cycles

That breadth matters. Wesfarmers does not behave like Harvey Norman in a downturn, and Aristocrat Leisure responds to different demand drivers than an apparel retailer. The sector’s apparent accessibility, because consumers recognise these brands, can create a false sense of analytical clarity about what drives their share prices.

Interest rate sensitivity and why this sector feels the squeeze first

The transmission mechanism from the RBA cash rate to consumer discretionary earnings is direct and well-documented. When rates rise, mortgage repayments increase for the majority of Australian homeowners on variable or short-fixed rate loans. That compression arrives in household budgets before consumers make any active choice to cut spending. The discretionary budget shrinks mechanically.

Data from the Australian Bureau of Statistics (ABS) confirms how this played out. The Australian National Accounts for the December quarter 2024, released in March 2025, showed weak volume growth in household final consumption expenditure across discretionary categories including furnishings, recreation and culture, and hotels, cafes, and restaurants. ABS Monthly Retail Trade data through March to May 2025 reinforced the pattern: modest headline turnover growth alongside ongoing consumer caution in discretionary categories.

The RBA’s Statements on Monetary Policy throughout 2025 consistently highlighted that higher interest rates and cost-of-living pressures had produced below-trend growth in household consumption, particularly in non-essential spending.

Once this mechanism is understood, the five-year performance gap stops looking like a puzzle. Consumer discretionary earnings were being compressed by the same rate cycle that was supporting bank margins and resource sector cash flows elsewhere on the ASX.

Household cost-of-living pressures in 2026 extended well beyond the direct mortgage channel, with electricity costs rising 25.4% annually and fuel prices surging 32.8% in a single month, meaning discretionary budgets faced compression from multiple directions simultaneously rather than from rate rises alone.

What the RBA easing cycle means for discretionary stocks from here

The consensus view across Australian financial media and economics teams treats consumer discretionary as a cyclical beneficiary of falling rates. As AMP Chief Economist Shane Oliver has noted, discretionary retailers sit at the rate-sensitive end of the market, and sectors leveraged to household consumption are positioned to benefit as the RBA eases. Rate cuts ease mortgage burdens and gradually restore the household discretionary budget.

The qualification matters, though. The initial phase of rate cuts may coincide with a still-softening labour market, which could limit the speed of any consumer recovery. The pace at which rate relief translates into actual spending depends on employment conditions remaining broadly stable.

Dividends in a cyclical sector: reliability is not guaranteed

Consumer discretionary is broadly characterised as a low-yield, capital-growth-oriented sector, a profile that contrasts with the ASX’s higher-yielding financials and materials sectors. For income-seeking investors, this distinction carries real portfolio consequences.

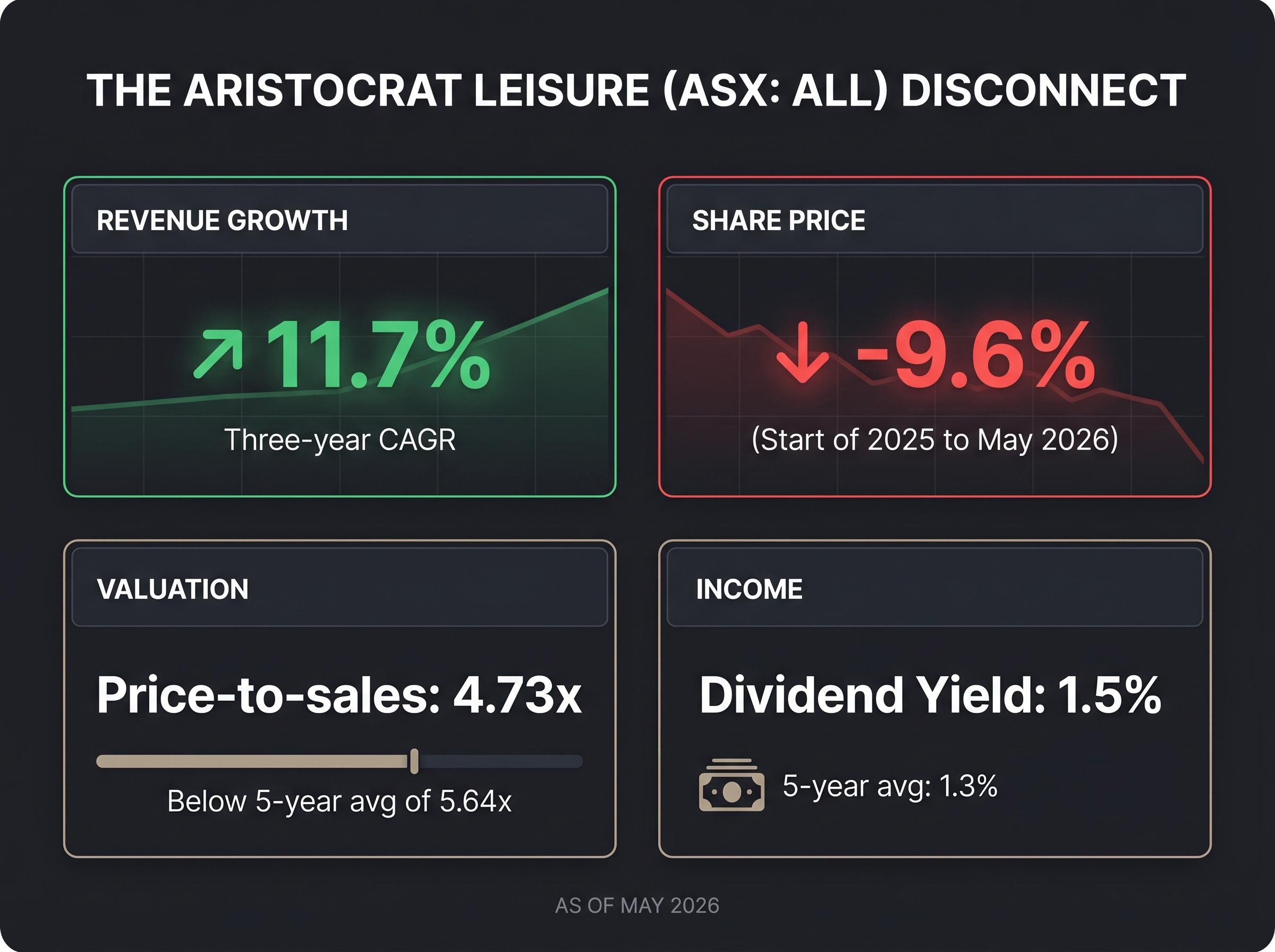

Aristocrat Leisure’s current dividend yield sits at 1.5% as of May 2026, with a five-year average of approximately 1.3% (Rask Media). That is well below what income-focused investors typically expect from ASX-listed companies.

Aristocrat is not an outlier in the sense of being misclassified. It is a growth-oriented discretionary business, and its yield reflects that orientation. The company reinvests earnings rather than distributing them, a rational capital allocation choice for a business growing revenue at double-digit rates.

The broader issue extends beyond any single name. Cyclical earnings compression in a high-rate environment creates real payout risk across the sector. When revenue softens, companies prioritise balance sheet preservation over distribution maintenance. Investors who approach consumer discretionary expecting dividend reliability comparable to banks or infrastructure names are likely to find the income profile inconsistent and, at times, disappointing.

The familiarity trap: why knowing the brand does not mean knowing the stock

Retail investors can describe what Harvey Norman sells. They can explain how JB Hi-Fi positions on price. That operational familiarity, however, does not translate into insight about earnings quality, balance sheet risk, valuation multiples, or cyclical positioning. The gap between knowing a business and understanding its investment case is where returns are most commonly eroded.

Aristocrat Leisure provides a concrete illustration. As of May 2026, the company’s shares traded at 4.73x price-to-sales, approximately 16% below a five-year average of 5.64x, according to Rask Media. Revenue growth has been strong: an annualised 11.7% compound rate over three years. Yet the share price declined 9.6% from the start of 2025 through May 2026.

| Metric | Current (May 2026) | Five-Year Average |

|---|---|---|

| Price-to-sales | 4.73x | 5.64x |

| Three-year revenue CAGR | 11.7% | |

| Share price change (start of 2025 to May 2026) | -9.6% | |

A business growing revenue at double digits, trading below its historical valuation average, and still losing ground for shareholders. That disconnect is not a contradiction; it reflects the complexity of valuation in a cyclical sector where forward earnings expectations, not trailing revenue, drive pricing. Brand recognition cannot resolve that complexity. Only rigorous analysis of earnings trajectory, multiple compression risk, and macro positioning can.

Multiple compression risk is not unique to the consumer discretionary sector, but it operates with particular force in cyclical businesses where earnings forecasts are themselves uncertain; WiseTech Global’s forward P/E contracted from approximately 86x to 34x between October 2025 and April 2026 even as EPS estimates rose, demonstrating that a falling share price and improving fundamentals can coexist when valuation multiples are resetting.

What a rate-cutting environment actually changes for the sector outlook

The anticipated RBA easing cycle provides a plausible tailwind for consumer discretionary. It does not, however, guarantee investment returns.

The distinction matters. A macroeconomic recovery in consumer spending and an investment return in consumer discretionary stocks are not the same thing. Markets frequently price anticipated recoveries before they materialise in company earnings. An investor who buys into the sector because rate cuts are coming may find that the share prices have already moved.

AMP commentary has noted that restrictive conditions may persist through much of 2025 before materialising as meaningful consumer tailwinds. Recovery may also arrive unevenly across sub-categories, with electronics and big-ticket durables potentially responding faster to rate relief than apparel, restaurants, or leisure spending.

The three signals worth watching as the consumer cycle turns

Rather than a buy or sell signal, investors benefit from a monitoring framework. Three data sources provide the clearest forward reads on whether rate cuts are translating into the kind of spending recovery that supports sector earnings:

- ABS Monthly Retail Trade: Track discretionary category turnover month-on-month for evidence of consumer budget recovery in household goods, clothing, and hospitality.

- ABS Household Final Consumption Expenditure (quarterly): Watch volume growth in furnishings, recreation and culture, and hotels and cafes as leading indicators for sector-level earnings improvement.

- Labour market conditions: Unemployment and underemployment trends determine whether rate cuts translate to sustained consumer confidence or are absorbed by a weakening employment backdrop.

These indicators, taken together, offer a more grounded basis for sector positioning than headline rate-cut expectations alone.

Sector familiarity is a starting point, not an investment edge

The five-year underperformance of the ASX consumer discretionary sector reflects real structural forces: interest rate sensitivity, cyclical earnings compression, and a low-dividend-yield profile that rewards capital growth rather than income. Brand recognition does not help investors navigate any of those dynamics.

The current moment offers a plausible catalyst. An RBA easing cycle could gradually restore household discretionary budgets and support sector earnings. The timing, pace, and distribution of that recovery across sub-categories, however, remains uncertain.

Investors evaluating any consumer discretionary stock should test their thesis against three questions: how sensitive is this business to the rate cycle, how reliable is its dividend in a downturn, and does the current valuation already reflect the recovery being priced in? Those questions require analytical work, not product familiarity.

For investors wanting to understand how the relative valuation gap between discretionary and defensive sectors has opened up portfolio opportunities, our dedicated guide to contrarian positioning in beaten-down consumer defensives examines the historical precedents from the dot-com bust and GFC, the institutional managers currently rotating into the trade, and the genuine risks that could prevent the thesis from paying off.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results.