JEPI.TO and JEPQ.TO: What’s Behind the Inflated Yields

27 mins ago

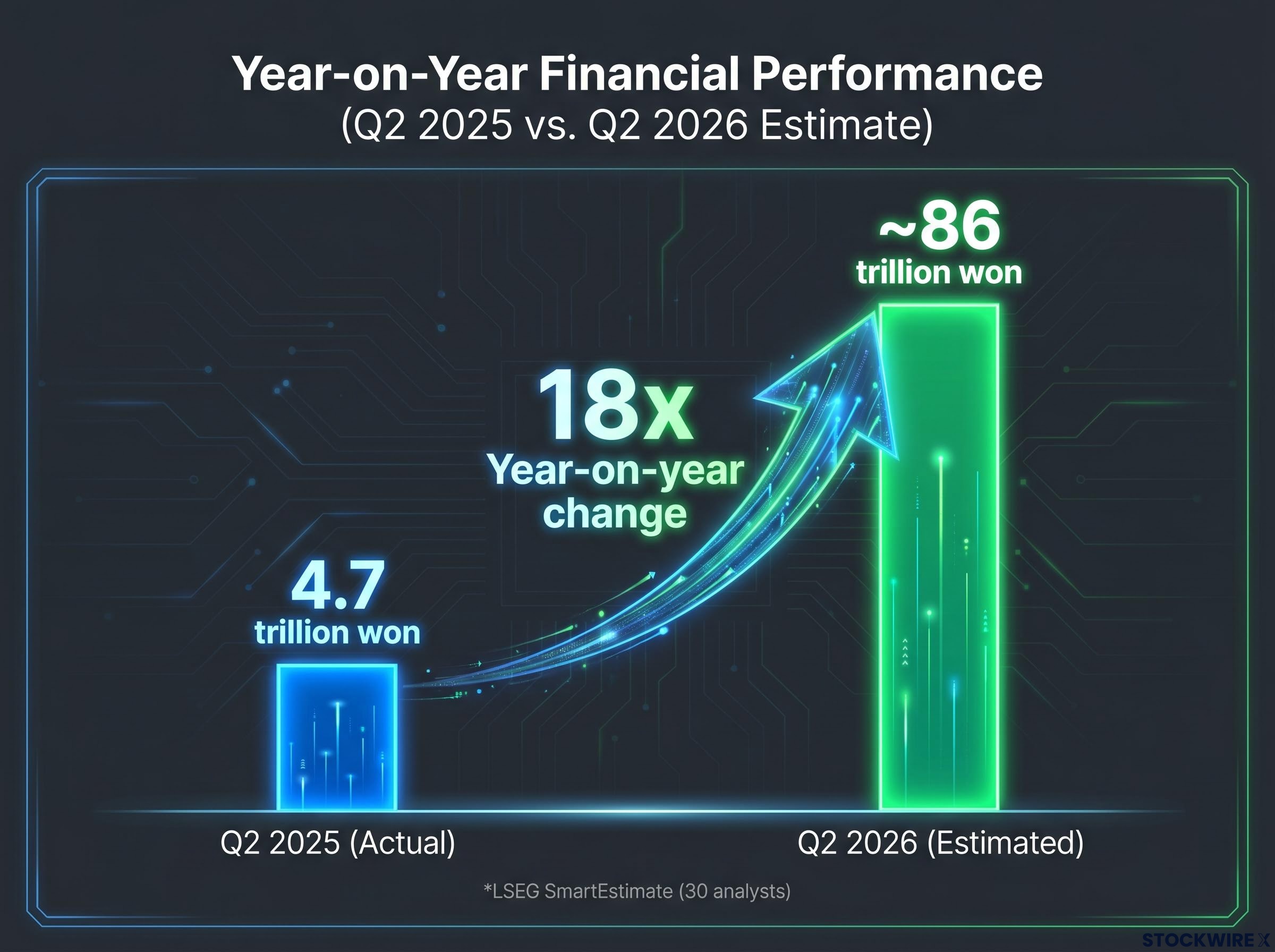

Samsung Electronics is forecast to post an operating profit of around 86 trillion won for Q2 2026, a figure that is approximately 18 times the profit recorded in the equivalent period a year earlier. For a company valued among the world’s largest chipmakers, that is one of the most dramatic year-on-year earnings swings in modern corporate history.

The outcome, which would represent a third straight quarter at record profit levels, reflects the collision of a prolonged global memory shortage with surging AI infrastructure investment on a scale the industry has not previously seen. But the headline number is only a partial picture: a wage settlement struck in May 2026 could push reported earnings below analyst consensus even if the underlying chip business performs exactly as expected.

Here is a clear framework for separating the signal from the accounting noise, understanding what is structurally different about this earnings cycle, and knowing exactly where to look when full results land later this month.

The scale of Samsung’s projected turnaround is best understood side by side.

| Metric | Q2 2025 (Actual) | Q2 2026 (Estimated) |

|---|---|---|

| Operating Profit (Won) | 4.7 trillion | ~86 trillion |

| Operating Profit (USD) | ~$3.08 billion | ~$56.35 billion |

The year-on-year change: approximately 18x.

The 86 trillion won projection is drawn from an LSEG SmartEstimate that aggregates forecasts from 30 analysts, weighted according to their historical forecasting accuracy rather than treated as equal inputs. Comprehensive results with full segment detail are due to be published by Samsung later in July 2026; every figure cited here represents analyst consensus projections, not confirmed actuals.

A move from 4.7 trillion won to 86 trillion won in twelve months is not a recovery from a bad year. It is a fundamental re-rating of what Samsung’s chip business can earn, and the question investors need to answer before drawing conclusions is whether that re-rating is already reflected in the share price.

The profit surge is not coming from a single product launch or a one-off pricing event. Three categories of demand are driving it simultaneously:

Samsung’s position as a supplier to Nvidia, Google, Apple, and other hyperscalers means its memory revenue functions as a leveraged bet on global AI infrastructure spending. When those customers accelerate capex, Samsung’s chip margins widen.

HBM4 supplier qualification for Nvidia’s Vera Rubin platform is the next demand catalyst visible on the horizon: Samsung qualified alongside SK Hynix and Micron in June 2026, though SK Hynix is estimated to hold 60-70% of initial volume allocations, with Samsung holding a secondary share of approximately 25-30%.

TrendForce DRAM pricing analysis covering the 2026 cycle identifies server and AI demand as the primary driver of DDR5 capacity displacement, with HBM3e price surges triggered by specification upgrades and accelerating order volumes from hyperscale customers.

On the supply side, the constraint is structural. New semiconductor fabrication plants require multi-year lead times and multi-billion dollar capital commitments before they produce a single chip. Rapid supply normalisation is not something the industry can deliver in the near term.

The evidence that customers recognise this: in April 2026, Samsung disclosed that it had entered into multi-year binding agreements with customers who wanted guaranteed access to chip supply going forward. Neither the names of those customers nor the specific terms of the contracts were made public. In commodity memory markets, multi-year binding agreements are unusual. Their existence tells you that this cycle has a different demand structure than previous consumer-led booms, which should raise the floor on what Samsung can earn through a full cycle.

Multi-year supply agreements between memory producers and hyperscalers represent a structural departure from prior commodity memory cycles, where spot pricing and short-term contracts defined customer relationships; SK Hynix has shifted to foundry-style agreements extending through 2028-2030, a regime change that reinforces rather than shortens the current cycle’s duration.

The same elevated memory prices that generate record chip profits create a problem in Samsung’s mobile division, which buys those components as inputs. Strong group profit does not mean all segments are strengthening.

| Attribute | Chip Division | Mobile Division |

|---|---|---|

| Price environment | Benefits from elevated memory pricing | Pays elevated memory pricing as input cost |

| Margin direction | Expanding to record levels | Under pressure, squeezed by component costs |

| H2 2026 outlook | Continued strength tied to AI demand | Additional handset price increases likely necessary |

Analyst commentary indicates that additional smartphone price rises are likely to be unavoidable in the latter part of 2026. The broader context: Apple moved to increase prices across its iPad and MacBook ranges in June 2026, a sign that component cost pressures are being felt across the industry rather than at Samsung alone.

The risk is consumer resistance. Price increases that protect margins can also suppress unit volumes, making the mobile recovery uncertain. Investors who apply a single earnings multiple to Samsung’s consolidated profit are effectively overpaying for the chip windfall and getting the mobile margin squeeze bundled in at the same valuation, when the two segments warrant very different treatments.

Operating profit measures what a company earns from running its business: total revenue minus direct costs of production and day-to-day overhead expenses, calculated before interest payments and tax. It strips out financing decisions and tax structures to show how well the core operations are performing.

Analysts use operating profit as the primary metric for assessing Samsung’s segment performance because it isolates how each division is actually performing before corporate-level financing and tax effects muddy the picture.

One-time accounting charges, including large provision bookings like Samsung’s accumulated bonus liability, are among the most consequential items excluded from non-GAAP earnings presentations, and the GAAP reconciliation table is where analysts locate the gap between reported and underlying performance.

The complication this quarter is that one-time accounting charges can move reported operating profit significantly without reflecting any change in the underlying business. A provision booked in Q2 for an obligation that accumulated over several quarters reduces the reported figure even if the chip business performed exactly as expected. For investors who primarily follow the headline beat or miss, this quarter’s Samsung report could be actively misleading if read at face value.

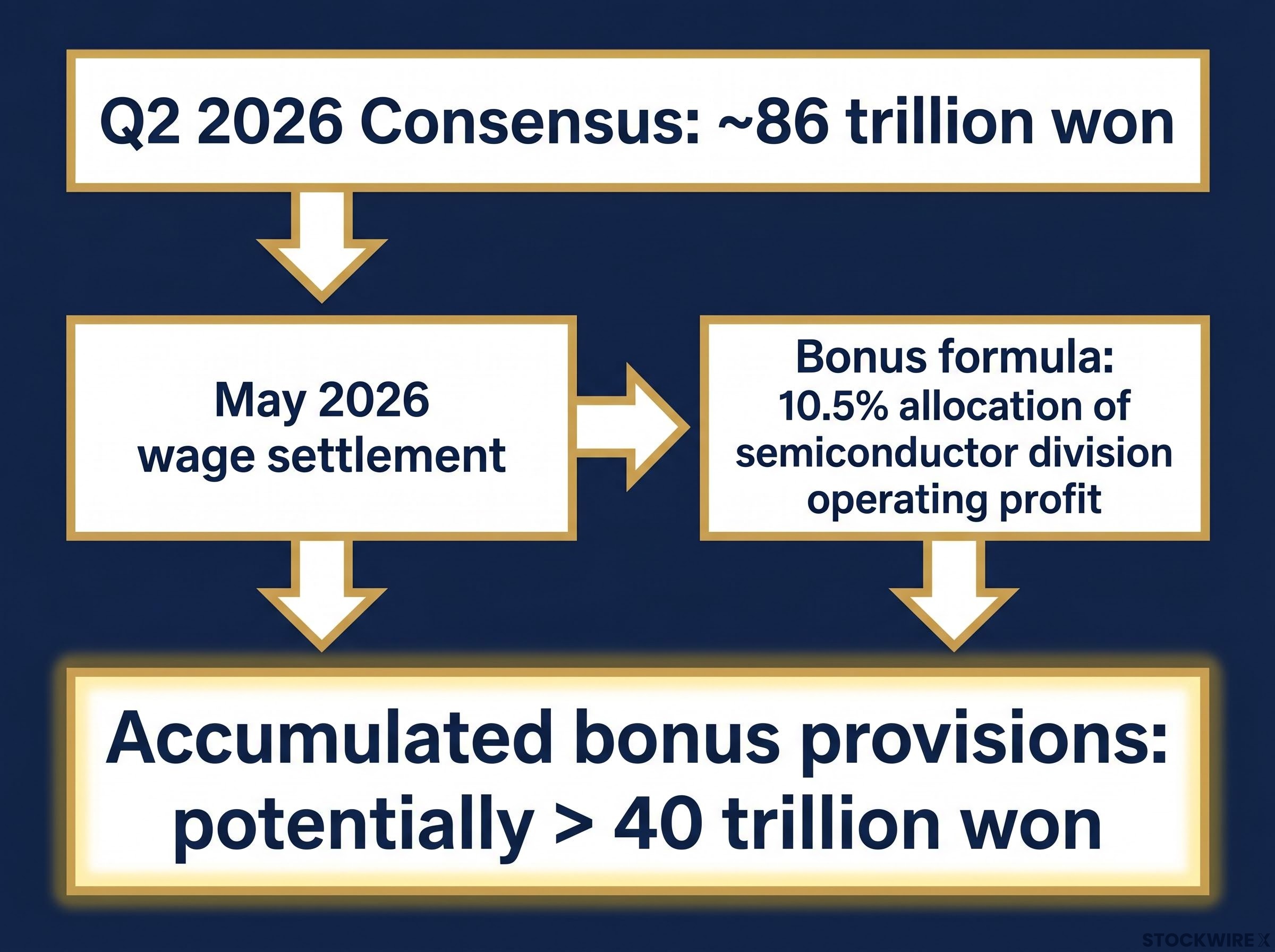

Towards the end of May 2026, Samsung headed off a threatened large-scale strike in its chip operations by concluding a wage agreement with employees. The settlement created a significant accounting variable.

The bonus formula: chip workers receive special bonuses funded by a 10.5% allocation of semiconductor division operating profit.

Several analysts place Samsung’s total accumulated bonus provisions at potentially more than 40 trillion won. The question is not whether the bonuses are owed; it is when Samsung formally recognises them in its financial statements.

If a large portion of those provisions is booked in Q2, reported operating profit could fall materially below the 86 trillion won consensus. A miss on that basis would not indicate any weakness in the chip business itself. Conversely, a clean beat above consensus could simply mean provision recognition was deferred to a later quarter.

When full results arrive, three areas will separate the signal from the noise:

If Samsung reports below 86 trillion won in July, the first question is not whether the chip cycle has turned. The first question is whether the delta is explained by provision timing.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Full detailed results are expected later in July 2026. Rather than reacting to the headline number, work through these five items in sequence:

Each item corresponds directly to a risk or uncertainty already covered in this article. Working through them in order will tell you far more than the headline profit figure alone.

The structural argument for a higher through-cycle earnings base is credible. HBM demand, multi-year supply contracts, and the sheer scale of AI infrastructure spending all support the view that Samsung’s memory business can earn materially more in an average year than it did in prior cycles.

But the 18x growth rate is, by definition, not repeatable. Memory remains capital-intensive and subject to downcycles as capacity eventually catches up. The key risk factors investors should monitor:

The central investor question: has the market already priced in AI-era profitability as Samsung’s new baseline? If it has, the upside from further earnings beats is more limited than the headline result suggests.

The most important number for a long-term investor is not 86 trillion won. It is what Samsung can earn through the next downcycle, because that figure determines whether today’s market price represents a margin of safety or a premium. One record quarter, however dramatic, cannot answer that question on its own.

For investors wanting to position around the downcycle risk Samsung’s own capital commitments are helping to create, our deep-dive into semiconductor cycle timing examines the five-indicator framework for identifying peak-cycle signals before earnings multiples compress.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Samsung is forecast to post operating profit of approximately 86 trillion won (around $56.35 billion USD) for Q2 2026, according to an LSEG SmartEstimate aggregating forecasts from 30 analysts weighted by historical accuracy. That figure is roughly 18 times the 4.7 trillion won Samsung reported in Q2 2025.

A May 2026 wage settlement with chip workers entitles them to bonuses funded by a 10.5% allocation of semiconductor division operating profit, and analysts estimate accumulated bonus provisions could exceed 40 trillion won. If a large portion is recognised in Q2, reported profit could fall materially below the 86 trillion won consensus despite the underlying chip business performing as expected.

High-bandwidth memory (HBM) is a specialised memory chip that sits inside AI accelerators and is essential for training and running large AI models at scale. Samsung's role as a supplier to Nvidia, Google, and Apple means its HBM revenue functions as a leveraged bet on global AI infrastructure spending, and surging demand for HBM is one of the three primary drivers behind the forecast 18x earnings jump.

The elevated memory prices generating record chip profits also raise Samsung's input costs in its mobile division, squeezing smartphone margins. Analysts expect additional handset price increases in the latter half of 2026, and the risk of consumer resistance means the mobile segment recovery remains uncertain even as the chip business hits record levels.

Investors should compare reported profit to the 86 trillion won consensus after adjusting for any bonus provisions recognised in the quarter, check semiconductor segment margins and average selling prices to assess whether memory pricing is still rising, and review management commentary on H2 2026 AI demand visibility from major hyperscaler customers. The headline beat or miss alone will be actively misleading if the bonus provision timing is not accounted for.