Barclays: Q2 Earnings, Not Geopolitics, Will Set the Market Trend

1 hr ago

SK Hynix’s US listing drew more than seven times the demand available. Micron committed $250 billion to domestic manufacturing through 2035. Both announcements landed in the same week, and together they tell a single story: the largest pools of institutional capital on earth are now treating AI memory as infrastructure, not as a trade.

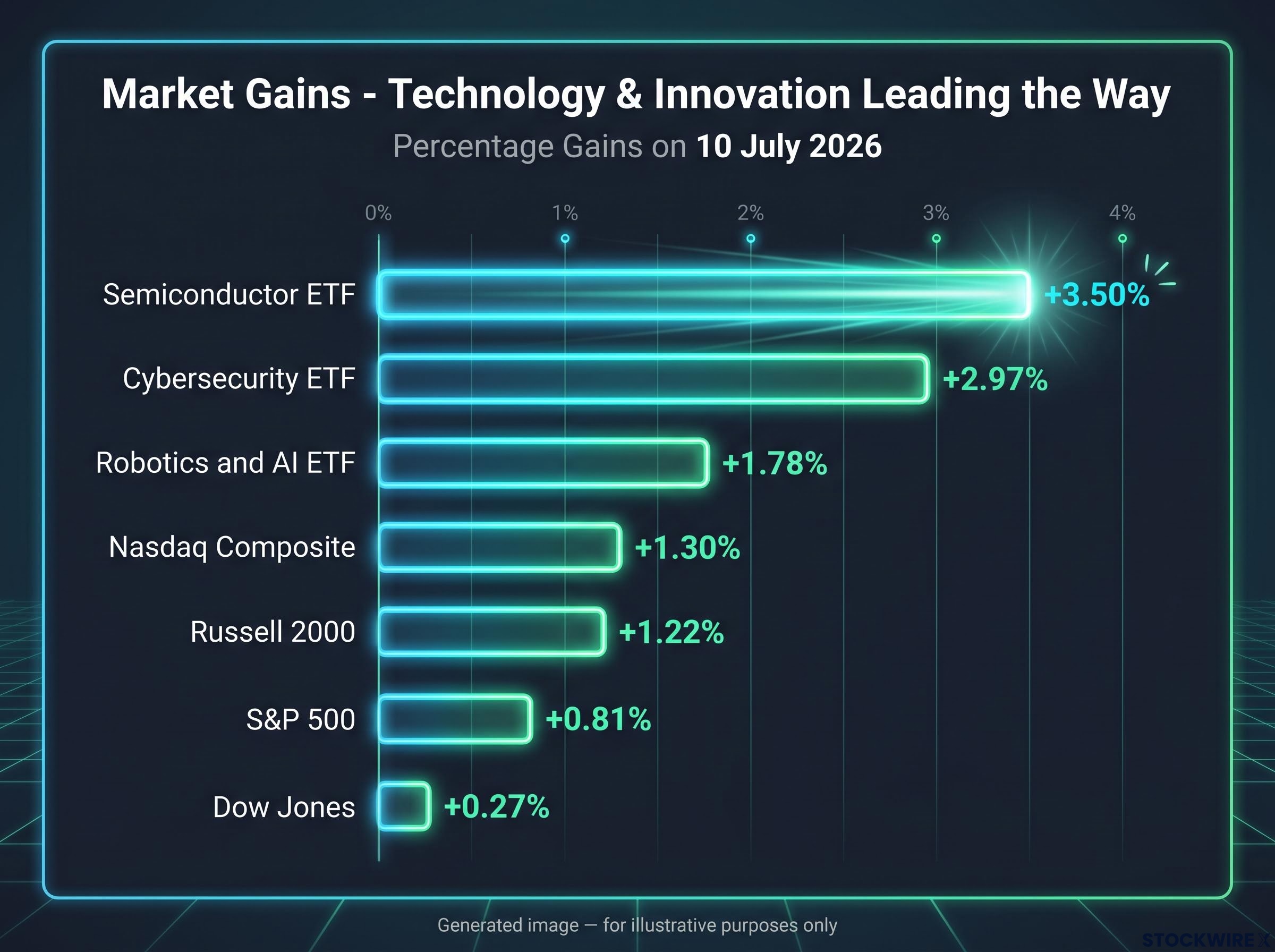

The timing sharpens the signal. The Philadelphia Semiconductor Index (SOX) surged 3.0% on 10 July 2026, but it remained roughly 11.5% below its 22 June peak. This rally arrived inside a correction. That distinction matters, because it separates a thematic re-rating from a trend reversal, and it is the lens that shapes everything that follows.

Here is what these two events actually reveal about the AI memory thesis, where the durable opportunity sits within the semiconductor stack, and which risks belong alongside any position you build around it.

The gains on 10 July were broad, but they were not even. The Nasdaq Composite climbed 1.30% to 26,207. The S&P 500 added 0.81% to 7,544. The Russell 2000 rose 1.22% to 2,993. The Dow Jones, weighted toward industrials and defensives, managed just 0.27% to reach 52,487.

Where the market leaned hard tells you more than the headline numbers. The Semiconductor ETF gained 3.50% to 581.7. The Cybersecurity ETF rose 2.97%. The Robotics and AI ETF added 1.78%. Inside the S&P 500, Information Technology led at +1.65%, while Consumer Staples fell 1.75% and Energy dropped 1.58%. The VIX fell 6.27% to 15.84, and the US 10-year Treasury yield eased 0.66% to 4.539%.

The SOX’s 3.0% surge was the headline. The context beneath it is what matters.

On 10 July 2026, the Philadelphia Semiconductor Index posted a 3.0% advance while still sitting roughly 11.5% beneath the high it had reached on 22 June. A strong thematic session and an ongoing correction are not mutually exclusive.

| Instrument | Move (%) | Level |

|---|---|---|

| Nasdaq Composite | +1.30% | 26,207 |

| S&P 500 | +0.81% | 7,544 |

| Dow Jones | +0.27% | 52,487 |

| Russell 2000 | +1.22% | 2,993 |

| Semiconductor ETF | +3.50% | 581.7 |

The gap between semiconductor infrastructure gains and hyperscaler underperformance on the same session tells you something specific. The market currently believes pricing power lives in physical constraints, not software monetisation. If you are allocating within the AI theme, that distinction should shape where your capital goes.

The market’s revealed preference on 10 July, with semiconductor infrastructure outpacing software and hyperscaler names, reflects a broader thesis about binding constraints on AI deployment: durable value concentrates where physical scarcity, not software monetisation, sets the ceiling on adoption speed.

SK Hynix priced its US ADRs at $149 per share, raising approximately $26.5 billion in what became one of the largest technology listings in US history. The offering was more than seven times oversubscribed. The ADRs now trade under ticker SKHY on Nasdaq, while the primary listing remains in Seoul.

The strategic rationale is straightforward: narrow the valuation gap with US peers like Micron by accessing dollar-based institutional mandates and ETF structures that could not previously hold the stock. This is not a capital-raising exercise born of necessity. It is a positioning decision designed to bring the world’s largest pool of equity buyers into the register.

The demand composition matters more than the headline ratio. According to Bloomberg, the book was driven by global long-only funds, technology-focused institutions, and sovereign wealth participants. That is not fast-money demand chasing a momentum window. It is long-duration capital underwriting a multi-year thesis on AI memory capacity.

SK Hynix has earmarked the proceeds for new factories, equipment, and EUV lithography scanners (the advanced tools required to manufacture next-generation memory), targeting HBM capacity for AI accelerators specifically, not general memory expansion.

A $26.5 billion raise at this demand quality is effectively a multi-year financing event for AI memory infrastructure. The oversubscription ratio tells you that institutional appetite for that capacity financing exceeded supply by a factor of seven, which is not a sentiment blip.

Two implications stand out for US-based investors:

The practical effect is that SK Hynix can now sit inside baskets and mandates that previously excluded it. That raises the probability of it becoming a core holding in AI and semiconductor portfolios rather than an Asia-specialist position.

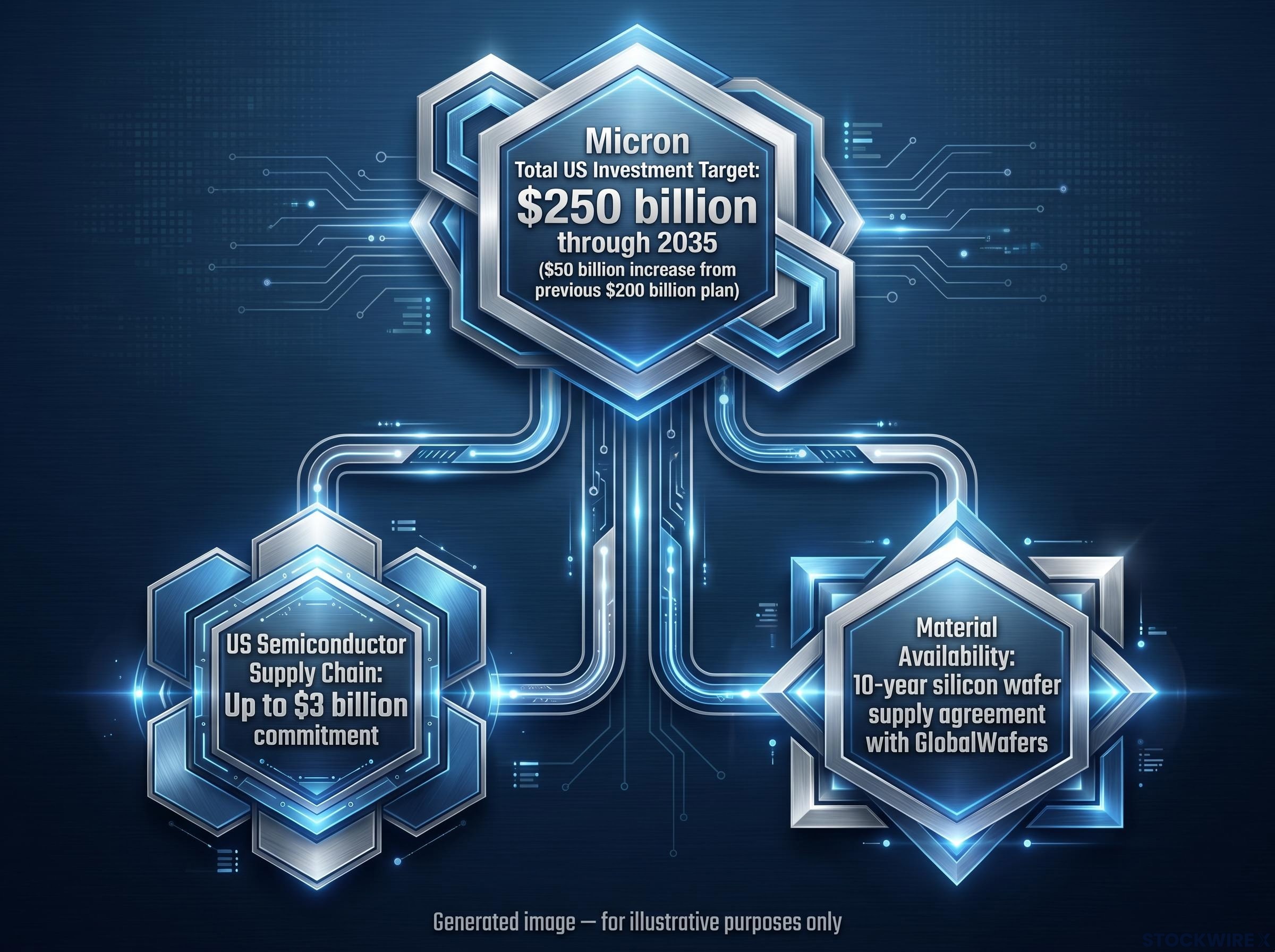

Micron raised its total US investment target to above $250 billion through 2035, a figure representing roughly $50 billion more than the company had previously committed under its $200 billion plan.

That figure deserves a moment on its own. A quarter-trillion-dollar domestic buildout, stretching across nearly a decade, is a management statement about demand duration. It says the leadership team believes AI-driven demand for advanced DRAM and high-bandwidth memory (HBM) will persist across multiple product cycles, not just the current one.

The near-term detail reinforces the conviction. Micron committed up to $3 billion toward strengthening the US semiconductor supply chain and entered a 10-year silicon wafer supply agreement with GlobalWafers, securing both input costs and material availability against a backdrop where geopolitical disruption is a live variable. Progress on the company’s New York campus is running ahead of the original construction timeline. Micron shares closed the session up 4.5% following the announcements.

That conviction is itself investable information. If management is committing at this scale, it implies a demand floor for advanced memory through at least the early 2030s.

The tension is real, though, and investors should hold it alongside the optimism:

CHIPS and Science Act incentives improve project returns and support the buildout case. But for equity holders, the posture means accepting capex-heavy balance sheets and earnings volatility as the cost of participating in a generational infrastructure theme.

The CHIPS for America program, administered through NIST, allocates federal funding across two offices covering manufacturing incentives and research and development, setting the policy architecture within which Micron’s domestic buildout qualifies for project return improvements.

The seven-times oversubscription for SK Hynix was not about generic memory. It was explicitly tied to the company’s position as a supplier of high-bandwidth memory for AI accelerators. That specificity is the correct investment lens to apply across the entire sector.

High-bandwidth memory (HBM) is memory designed to sit directly alongside AI processors, delivering data at speeds and bandwidths that standard server DRAM cannot match. It is a different product, sold to different customers, at different price points, with structurally different margin profiles. When you evaluate a memory company on DRAM market share alone, you may be measuring the wrong variable. The question that determines margin durability in this cycle is what fraction of output feeds AI accelerator demand at HBM pricing, not commodity server pricing.

HBM pricing power sits at the centre of the margin durability question: Bernstein projects a 2-2.5x HBM contract price increase for 2027, and the wafer economics gap between HBM and conventional DRAM means that substitution pressure from manufacturers seeking higher per-wafer returns is a structural risk the supply chain cannot simply absorb.

| Attribute | High-bandwidth memory (HBM) | Commodity DRAM |

|---|---|---|

| Primary end market | AI accelerators (GPUs, ASICs) | PCs, servers, mobile |

| Pricing dynamic | Supply-constrained, premium pricing | Commodity cycle, ASP pressure |

| Key customers | NVIDIA, AMD, hyperscaler ASICs | Broad OEM base |

| Investment evaluation focus | HBM3E/HBM4 roadmap, vendor depth | Cost leadership, utilisation rates |

The evaluation criteria for any AI memory name should start here: what share of revenue and capex is tied to HBM versus legacy products? How deep are the relationships with GPU and accelerator vendors? Where does the company sit on the HBM3E and HBM4 product roadmap? Investors who do not separate HBM from commodity DRAM when screening or sizing semiconductor positions risk treating meaningfully different risk and return profiles as equivalent.

Micron’s 10-year wafer agreement with GlobalWafers and SK Hynix’s use of IPO proceeds for EUV scanners express the same strategic logic: control over inputs and capacity is now a competitive moat, not a procurement function.

In a market where export controls and geopolitical disruption are live variables, companies that have locked in multi-year input supply and diversified their manufacturing geography carry a risk premium reduction. That should show up in how you think about both valuation multiples and margin stability. Multi-region manufacturing footprints aligned with CHIPS-style incentives matter precisely because the alternative, concentrated production exposed to policy shocks, carries costs that are no longer theoretical.

Micron has committed up to $3 billion in near-term US supply chain investment alongside its broader $250 billion buildout. SK Hynix is directing IPO proceeds toward EUV scanner procurement, the equipment layer that underpins next-generation HBM fabrication. Both companies are building the kind of input security that sustains pricing power and margin resilience through volatile periods.

If a semiconductor name cannot answer these three questions credibly, its supply-chain position is a vulnerability rather than a moat.

The SK Hynix listing and Micron commitment, taken together, offer a coherent framework for positioning within AI memory. The evidence supports four principles:

Given that pricing power currently resides in physical constraints, specifically memory, compute, and equipment, rather than software monetisation, overweighting infrastructure over applications is analytically defensible at this stage of the cycle.

The principle of infrastructure over applications was visible well before 10 July, with niche power and optical networking suppliers posting 90-130% revenue growth in the first five months of 2026 while hyperscalers absorbed the bulk of institutional attention, and the pattern reinforces the case for tilting toward physical constraint owners rather than software monetisation plays.

The SOX sitting 11.5% below its 22 June peak is a concrete reminder that structural themes do not eliminate drawdown risk. The investor who accepts that volatility as a feature of the thesis rather than evidence against it is better positioned to hold through the parts of the cycle that test conviction.

The $26.5 billion SK Hynix raise and Micron’s $250 billion commitment are not quarterly earnings momentum signals. They are long-duration capital commitments by both corporations and the institutions that financed them, underwriting a view that AI memory is generational infrastructure.

That does not eliminate uncertainty. Memory cycles have not been abolished. Multi-year execution risk across massive capex programmes is real. Seven-times oversubscription on a listing does not guarantee sustained equity appreciation any more than a strong IPO day guarantees a strong first year.

For investors wanting to build the cycle risk framework in more depth, our full explainer on semiconductor cycle timing covers the five-indicator sequence for identifying when the current supply-constrained environment begins to shift toward the 2027-2029 oversupply window, including the graduated de-risking sequence for memory positions specifically.

The two questions that determine whether this thesis belongs in your portfolio are specific. Can you differentiate which memory, which capacity, and which balance sheets are best positioned within the AI stack? And can you hold through the volatility that comes with capex-intensive, cycle-sensitive infrastructure names? If the answer to both is yes, the evidence assembled this week supports the structural case. If either answer is uncertain, position size and risk management matter more than directional conviction.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

AI memory stocks are shares in companies that manufacture high-bandwidth memory (HBM) and advanced DRAM designed specifically for AI accelerators and GPU clusters. Investor attention has intensified because SK Hynix's $26.5 billion US listing was seven times oversubscribed and Micron committed $250 billion to domestic manufacturing through 2035, signalling that large institutional pools of capital are treating AI memory as infrastructure rather than a cyclical trade.

HBM is memory engineered to sit directly alongside AI processors, delivering data at speeds and bandwidths that standard server DRAM cannot match. It commands premium, supply-constrained pricing and carries structurally higher margin profiles than commodity DRAM, which is sold across a broad OEM base at cycle-sensitive prices.

SK Hynix listed in the US to access dollar-based institutional mandates and ETF structures that could not previously hold the stock, narrowing its valuation gap with peers like Micron. The seven-times oversubscription was driven by global long-only funds, technology institutions, and sovereign wealth participants, indicating long-duration capital underwriting a multi-year AI memory capacity thesis rather than short-term momentum demand.

Micron's commitment represents roughly $50 billion more than its prior $200 billion plan and stretches through 2035, signalling management conviction that AI-driven demand for advanced DRAM and HBM will persist across multiple product cycles. It implies a demand floor for advanced memory into at least the early 2030s, though elevated capex will compress near-term free cash flow for equity holders.

The article identifies three key questions: whether the company holds long-term input agreements that reduce spot market exposure, whether it has a multi-region manufacturing footprint aligned with CHIPS Act incentives, and whether its capex plan is funded against a credible demand timeline with guardrails against overbuilding. Beyond supply chain, investors should assess what share of revenue and capex is tied to HBM versus legacy commodity DRAM, since the two carry meaningfully different risk and return profiles.