Why the Fed Rate Cut That Never Came Is Now Your Base Case

21 mins ago

Equity markets are perched near their highs, and most of the financial press wants you watching the same things: U.S.-Iran sabre-rattling, Federal Reserve signalling, trade policy whiplash. Barclays thinks you are watching the wrong screen.

In a research note published 10 July 2026, the bank’s European equity strategist Emmanuel Cau made a direct claim: the variable that will determine whether this market holds its gains or reprices is not geopolitics. It is the Q2 2026 earnings season now actively underway. Cau’s argument sits inside a broader framework laid out in Barclays’ Q3 2026 Global Outlook from June 2026, which characterised fundamentals as solid but flagged a summer window where that thesis gets tested in real time.

Here is the analytical framework Barclays is using, what each component tells you about the market’s actual pressure points, and how it reshapes the way you should be reading the next several weeks of corporate results.

Cau’s core claim is not that geopolitical risk does not exist. It is that geopolitical risk is the wrong variable to trade on. Events like the U.S.-Iran conflict, shifting trade policy, and Fed uncertainty affect short-term volatility, but unless the shock is truly extreme, they do not alter the medium-term equity trend. That trend, in Barclays’ view, is set by something directly testable: whether companies report earnings and guidance that justify the prices investors are currently paying.

Barclays’ central thesis: Q2 2026 earnings are the decisive near-term catalyst for equity markets. The medium-term trend will be determined by whether reported results and forward guidance validate current valuations.

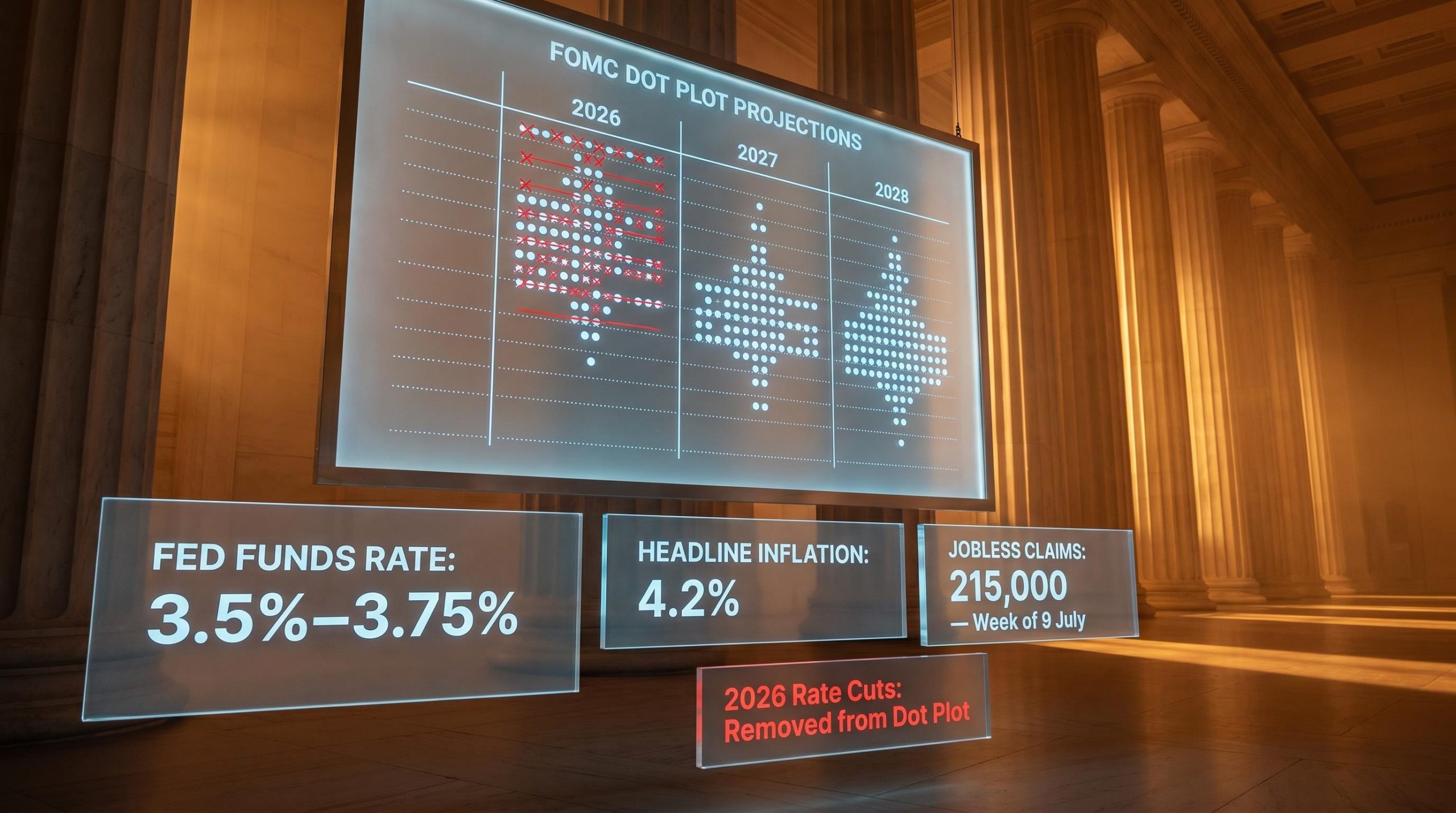

The distinction matters because it separates noise you cannot price from fundamentals you can measure. A geopolitical flare-up produces a gap down and a recovery. An earnings miss at stretched valuations produces a repricing that sticks. With the federal funds rate sitting at 3.50%-3.75% and inflation considerations still in play, the macro backdrop offers limited cushion if that repricing arrives.

The Federal Reserve June 2026 rate decision confirmed the federal funds target range at 3.50%-3.75%, leaving equity markets to absorb the full weight of earnings results rather than anticipating meaningful monetary cushion from a policy pivot.

What this tells you is straightforward: if you have been making positioning decisions based on headlines about Tehran or tariff threats, Barclays is arguing you are reacting to the wrong signal. The earnings reports hitting over the next several weeks are where the actual verdict gets delivered.

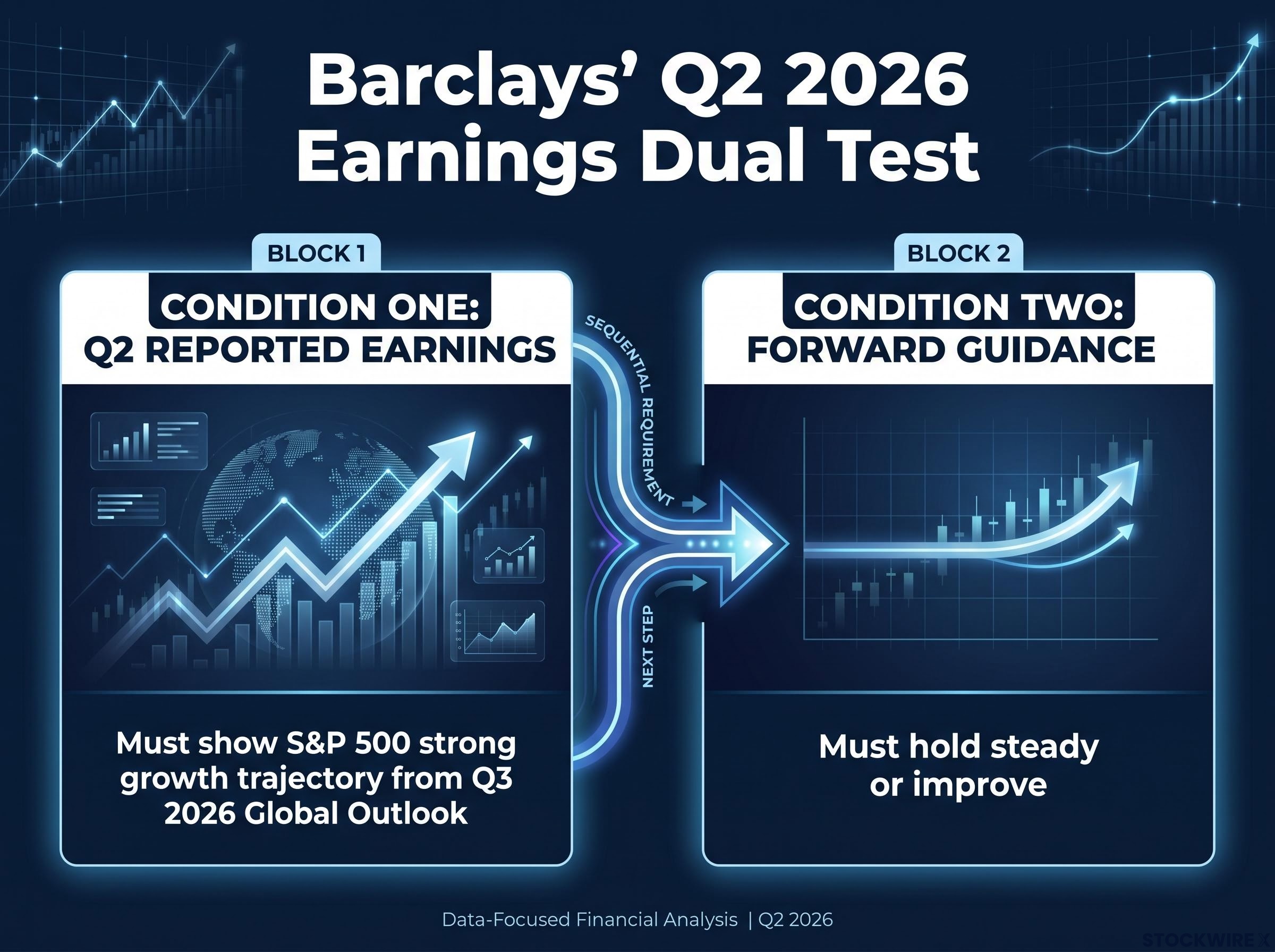

The strategic framing only matters if you understand what “holding up” looks like in practice. It is not as simple as beating consensus estimates. Barclays frames this earnings season as a dual test, and passing requires both conditions to be met:

That second condition is where the fragility sits. Tech and semiconductor stocks are trading well above historical valuation norms heading into this season. At those multiples, a solid quarter paired with cautious guidance is not a neutral outcome; it is a negative one. The market has already priced in continued strength. Anything less reopens the valuation question.

For you, this reframes how to read each individual earnings release. A headline “beat” that arrives alongside softer guidance is not bullish. In an elevated-valuation environment, sentiment is fragile to any forward-looking softness, and the market will treat guidance cuts as the dominant signal regardless of the backward-looking number.

Semiconductor and technology stocks pulled back before Q2 reporting even began. The natural read is bearish: if the market is selling these names ahead of results, something must be wrong.

Barclays sees it differently. Cau characterised the pullback as the result of hedge funds and momentum-driven vehicles reducing their positions ahead of reporting season, rather than any shift in the underlying fundamental view on the sector.

Barclays characterised the pre-earnings tech pullback as “froth removal,” implying stretched valuations correcting before earnings provide the real test, not a signal of structural damage.

Froth removal means the easy, positioning-driven gains got squeezed out. What remains is the fundamental question: are AI capital expenditure cycles translating into actual profit growth, or has the sector run ahead of what near-term earnings can support? That is precisely the question July reports will answer.

Barclays flags this as one of four concurrent risk factors for summer 2026, and the bank’s guidance here is notably nuanced. Not all tech and AI exposure carries the same risk:

AI valuation risk is compounded by what Goldman Sachs identified in May 2026 as a structural distributional problem: low index-level volatility masks large opposing moves by individual winners and losers that cancel out, leaving investors exposed to single-stock concentration risk that standard diversification metrics fail to capture.

The pullback itself is not your warning signal. The earnings reports from key AI and chip names this month are. They will tell you whether the CapEx-to-profit loop is real or whether pricing got ahead of the evidence.

If you check the S&P 500 each evening and see modest daily moves, you might conclude that volatility is contained. Barclays argues that conclusion is wrong, and the reason involves a concept called dispersion.

Dispersion measures the spread of individual stock returns around the index average. When dispersion is low, most stocks move in the same direction by similar amounts, and the index gives you an accurate read on what is happening. When dispersion is high, the index masks a much wider range of outcomes underneath.

Barclays observes that dispersion has risen materially in mid-2026, and that positioning dynamics have amplified individual stock moves. The practical consequence is that an index investor and a stock-level investor are experiencing two different markets right now. The index says calm. Individual holdings may say something quite different.

The CBOE S&P 500 Dispersion Index held near all-time highs through late June 2026, with dispersion at dot-com era levels driven by extreme concentration events such as two HBM memory chip stocks generating roughly 17% of ACWI total return in a single month, a historical anomaly that puts the index-versus-holdings gap Barclays describes in sharp relief.

For you, this is a direct challenge if you rely on index-level readings to gauge portfolio risk. Your actual exposure, at the individual position level, may be experiencing volatility the headline number does not reflect.

Barclays’ view is that the market is not structurally fragile, but it is operating with a thin margin for negative surprise. The bank maps four specific pressure points, each with a distinct probability profile and transmission channel.

| Risk Factor | Category | Primary Channel of Impact | Sectors Most Exposed |

|---|---|---|---|

| Stretched positioning | Base case | Crowded trades unwind sharply when sentiment shifts, producing disorderly moves | Technology, semiconductors, momentum-heavy names |

| U.S.-Iran conflict | Tail risk | Energy and commodity supply disruption, risk appetite withdrawal | Energy, defence, commodity-linked sectors |

| AI and semiconductor overvaluation | Base case | Earnings fail to validate elevated multiples, triggering sector repricing | AI infrastructure, chip designers, cloud CapEx beneficiaries |

| Fed policy and liquidity uncertainty | Base case | Surprise rate decisions in either direction at 3.50%-3.75% fed funds rate | Rate-sensitive equities, growth stocks, financials |

The distinction between base-case risks and tail risks matters for how you respond. Stretched positioning and valuation risk are things you should be actively managing around right now. The U.S.-Iran conflict, while serious, is not priced as a base-case outcome, and making large portfolio changes on a tail-risk scenario Barclays considers unlikely to materialise in its central forecast is a different kind of decision entirely.

Crowded positioning dynamics have been building throughout 2026, with June recording $150 billion in US equity inflows, the largest single-month figure in history, a signal that Barclays analyst Emmanuel Cau framed not as a confidence vote but as a FOMO culmination that caps upside while amplifying downside risk into earnings season.

The risk map tells you that the equity market’s summer is not a coin flip. It runs through four identifiable channels, and understanding which one fires first shapes what kind of volatility follows.

The framework translates directly into four actionable principles, each connecting back to the analytical layers already established:

For investors wanting a structured method to act on Barclays’ positioning guidance, our comprehensive walkthrough of beta-weighted position sizing covers how to convert each holding into market-risk equivalent dollars and apply volatility targeting to mechanically reduce exposure as dispersion conditions shift.

These are not generic prescriptions. Each one is the specific output of a framework that says earnings are the test and dispersion is the environment. The connective tissue between the analysis and the action is what makes this season navigable rather than reactive.

Barclays’ argument compresses to a single verdict: the medium-term equity trend will be set by whether Q2 2026 earnings and guidance justify current valuations. That is the test. Everything else, the Iran headlines, the Fed speculation, the positioning noise, is secondary unless it reaches a severity threshold that Barclays considers unlikely in its base case.

The Q3 2026 Global Outlook projected strong S&P 500 earnings growth. July’s reports are where that projection either gets confirmed or challenged, and Barclays has specifically flagged this summer as a period of elevated potential volatility around the outcome.

The question for you is not what the market will do. It is what the earnings and guidance from the companies you own are telling you, and whether those results justify the prices you are paying. That is the framework. The next several weeks will supply the answer.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. These statements are speculative and subject to change based on market developments and company performance.

—

Dispersion measures how widely individual stock returns diverge from the overall index return. When dispersion is high, as Barclays observes it is in mid-2026, the index looks calm while individual holdings experience large moves in opposite directions, meaning index-level readings can badly misrepresent your actual portfolio risk.

Barclays strategist Emmanuel Cau argues Q2 2026 earnings and forward guidance are the decisive near-term catalyst, not geopolitical events like U.S.-Iran tensions or Federal Reserve signalling, because an earnings miss at stretched valuations produces a repricing that sticks, whereas geopolitical shocks typically produce a gap down followed by recovery.

In an elevated-valuation environment, a company that beats Q2 numbers but cuts its second-half outlook does not pass Barclays' dual test, because the market has already priced in continued strength and will treat guidance cuts as the dominant signal regardless of the backward-looking result.

Barclays characterised the pre-earnings pullback in semiconductor and tech stocks as froth removal, meaning hedge funds and momentum vehicles reduced crowded positions ahead of reporting season rather than signalling any shift in the underlying fundamental view. The actual verdict on whether AI capital expenditure is translating into profit growth comes from July earnings reports, not the pullback itself.

Barclays draws a clear line between high-quality AI-earnings converters, companies demonstrably translating AI investment into durable profit growth, and valuation-driven momentum positions that rose on narrative rather than earnings evidence. The second category carries significantly more downside risk if Q2 results disappoint.