Why Oracle Gains as Adobe Falls: the AI Software Divide

6 hrs ago

BCA Research has issued a warning grounded in four decades of market data: a coming wave of AI-focused IPOs could quietly erode both broader equity returns and the premium valuations that have propelled AI leaders to historic highs. The warning, published on 8 June 2026 by BCA Chief Strategist Noah Weisberger, arrives as US IPO proceeds have surged 163.9% year-on-year despite fewer deals, signalling that large, market-moving listings are clustering. Anticipated candidates including xAI, Anthropic, and CoreWeave remain among the most frequently cited names in the queue.

What follows decodes the BCA Research thesis, explains the specific mechanisms by which new AI listings can pressure existing AI stocks, presents the strongest counter-arguments, and gives investors a framework for thinking about IPO cycle risk in their portfolios.

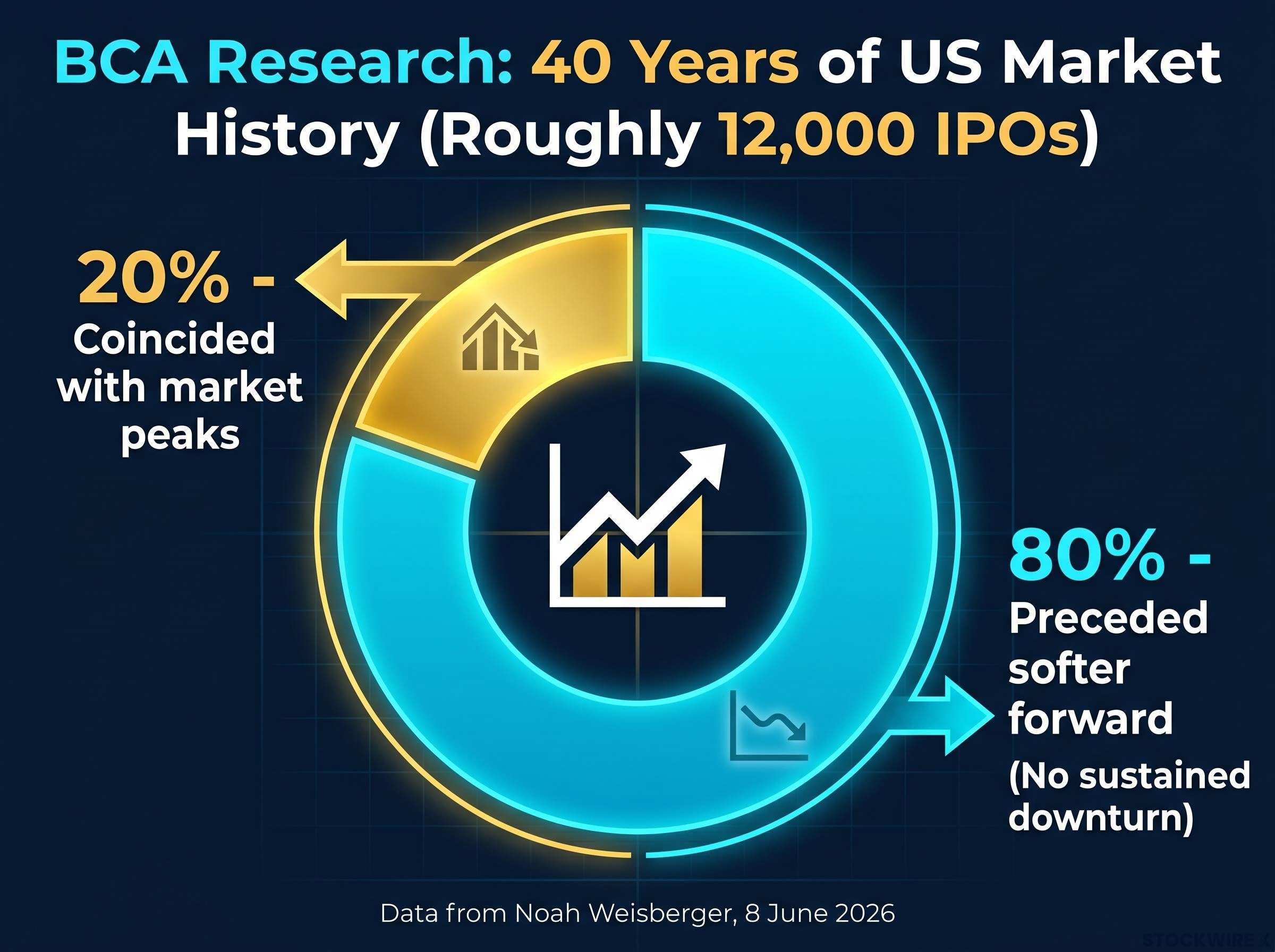

Weisberger’s analysis draws on a dataset spanning approximately 40 years and roughly 12,000 IPOs. The core finding is measured rather than alarmist: elevated IPO volumes have historically preceded weaker subsequent market performance and reduced valuation multiple expansion.

The critical nuance sits in the base rates. Only around 20% of large-scale IPO waves have historically coincided with market peaks. The remaining 80% saw softer forward returns without a sustained downturn.

Long-term IPO underperformance of approximately 3.3% per year over the first five years, drawn from data spanning 1980 to 2024, forms part of the empirical backdrop for BCA Research’s concern: elevated issuance volumes have not only pressured incumbent valuations in prior cycles but have also delivered weaker outcomes for investors who entered the new listings themselves.

Key parameters from the BCA Research dataset:

BCA Research characterises the elevated IPO environment as a cautionary indicator rather than a definitive signal to exit equity positions. A prolonged bear market is considered unlikely.

The current environment fits the pattern BCA Research identifies as worth monitoring. According to Renaissance Capital, 2026 year-to-date US IPO proceeds have reached $34.2 billion across 68 deals, a 163.9% increase in proceeds despite an 18.1% decline in deal count. Fewer offerings are raising far more capital, which means individual listings carry greater market weight.

The Renaissance Capital IPO market statistics for 2026 year-to-date record $34.2 billion in total proceeds across 68 priced deals, confirming that fewer but larger offerings are driving the surge in capital raised relative to the prior year.

The pressure on incumbents follows a sequence that institutional investors recognise and retail investors often miss.

The current deal-size environment amplifies this dynamic. PwC notes that the window for large issues remains open, with large tech offerings pricing successfully in Q1 2026. When individual deals are larger, the capital that must be raised or redirected to participate is correspondingly greater.

The numbers illustrate the shift in deal scale:

| Period | Deal count | Proceeds | Implied average deal size |

|---|---|---|---|

| Q1 2025 | 15 | ~$7.9 billion | ~$527 million |

| Q1 2026 | 22 | >$9.4 billion | ~$427 million |

| 2026 YTD (all) | 68 | $34.2 billion | ~$503 million |

SPAC issuance adds another dimension. PwC reports that Q1 2026 saw 62 SPACs raise over $11.8 billion, the highest level since 2021. SPACs historically serve as an alternative pathway for AI-adjacent and frontier-technology companies to reach public markets, broadening the supply pipeline further.

The conventional explanation for elevated AI valuations centres on the technology’s transformative potential. BCA Research’s argument is more precise: current AI leaders trade at exceptional multiples partly because investors wanting pure-play AI exposure have had almost nowhere else to go.

That scarcity has concentrated capital into a small number of names. When the only way to express an AI bet in public markets is through a handful of mega-cap incumbents, those incumbents absorb disproportionate flows. Their valuations reflect not only their earnings power but also the absence of alternatives.

New AI listings break that dynamic. Each fresh listing gives institutional and retail investors another vehicle for AI exposure, diluting the exclusivity that has supported incumbent pricing. PwC’s Q1 2026 analysis observed that investor demand is “becoming more selective,” with differentiation by business model rather than blanket AI enthusiasm, a shift that raises the bar for incumbents once direct comparables begin trading.

The most frequently cited IPO candidates remain private or pre-filing as of June 2026:

Marquee AI listings carry a compounding problem: prediction markets and retail sentiment routinely embed best-case valuations before a single public share trades, meaning the expectations gap is widest precisely when enthusiasm is highest, and the named candidates in the current pipeline, including xAI and Anthropic, are entering an environment where that dynamic is already well documented.

Capital reallocation toward newly listed AI names can disadvantage existing incumbents even if overall AI sector demand remains strong. BCA Research identifies this leadership rotation as a likely second-order effect: earlier AI winners may underperform broader sector indices as capital disperses into new entrants.

The cloud-software IPO wave of the 2010s offers a precedent. Early leaders enjoyed strong scarcity premia. Subsequent waves of listings provided investors with more targeted options, leading to relative multiple compression of incumbents even when the sector’s long-term growth story remained intact. The sector did not collapse; leadership simply shifted.

The strongest counter-argument is structural: the 2022-2023 IPO drought created a substantial backlog of quality issuers. Some portion of the current surge reflects catch-up issuance rather than speculative exuberance.

EY’s Q1 2026 global report states there “really isn’t evidence that these deals overwhelm market capacity since they’re well telegraphed,” giving investors time to adjust portfolios without forced selling.

PwC reinforces this reading. IPOs in 2026 were, on average, trading down approximately 1% through 31 March 2026, compared with the S&P 500 declining roughly 5% over the same period. Modest outperformance by new issues is not the profile of a speculative blowout. PwC described 2025 as “the strongest IPO year since 2021,” framing 2026 as a continuation of a selective, fundamentals-focused recovery rather than a bubble.

The two most-cited historical analogues for the market-top interpretation carry their own caveats:

Both episodes involved a measurable deterioration in deal quality that preceded the downturn. Whether the current AI IPO pipeline replicates that deterioration or maintains the selectivity PwC and EY describe will determine which historical analogue proves more relevant.

An IPO cycle describes the recurring pattern in which the volume of new public listings rises and falls with broader market conditions. Companies time listings to coincide with high valuations and strong investor demand, which means IPO surges tend to cluster during periods of elevated risk appetite.

The mechanism by which high IPO volumes can dampen forward returns is straightforward: new supply competes for institutional capital. When the market absorbs a large volume of new listings, money that would otherwise flow into existing stocks is redirected toward new offerings. The very conditions that enable IPO surges, stretched valuations and abundant liquidity, are also the conditions that historically precede periods of weaker performance.

Dealogic commentary notes that mega-deals (over $1 billion) tend to dominate volume late in the cycle, concentrating the capital-absorption effect into a smaller number of high-impact listings.

BCA Research’s thesis contains two separable risks that portfolio holders face simultaneously:

An investor who is long the broader market and concentrated in AI leaders faces both risks at once. Recognising them as distinct allows for more targeted portfolio assessment.

Index-level concentration risk compounds the scarcity premium problem: the top five companies control roughly 30% of total US market capitalisation, meaning passive investors who believe they are diversified are in practice carrying outsized exposure to the same names whose valuations BCA Research identifies as most vulnerable to new supply.

BCA Research’s warning is probabilistic, not binary. The 20% historical peak-coincidence rate means the base case is weaker forward returns, not a market collapse. Weisberger’s own framing suggests a prolonged bear market is considered unlikely.

Three portfolio questions are worth asking this week:

Specific indicators worth tracking:

PwC observes that investor demand is becoming more selective and fundamentals-focused. Renaissance Capital pipeline commentary notes crypto and frontier-tech names (including Kraken, Ripple, and Gemini) as part of a broader new-technology issuance wave, suggesting the capital-absorption effect may extend beyond AI into adjacent sectors.

For investors who have identified meaningful exposure to scarcity-premium AI names and want a step-by-step execution framework, our dedicated guide to portfolio rebalancing after an equity rally covers the threshold triggers, tax-efficient ordering of trades, and alternative capital destinations including private credit and market-neutral funds that are most relevant in the current rate environment.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Past performance does not guarantee future results. Financial projections and historical patterns are subject to market conditions and various risk factors. Forward-looking statements regarding IPO pipeline candidates and their potential market impact are speculative and subject to change.

BCA Research’s four-decade dataset establishes a genuine pattern: elevated IPO volumes have historically softened forward returns and pressured scarcity premia. The 20% peak-coincidence rate means this is not an exit signal, but neither is it background noise.

The tension between the market-top interpretation and the mid-cycle broadening view remains genuinely unresolved. EY and PwC see a selective, quality-driven recovery absorbing new supply without systemic stress. BCA Research sees the conditions for scarcity erosion and leadership rotation assembling in real time.

The resolution depends on what happens next: whether a cluster of large AI-focused listings, deals on the scale of xAI, Anthropic, or CoreWeave, prices within a condensed window. That concentration would most closely replicate the historical conditions BCA Research identifies as consequential. Until those filings materialise, the warning is credible, the timing is uncertain, and the monitoring framework matters more than any single positioning call.

—

BCA Research warns that a wave of large AI-focused IPOs, including anticipated listings from xAI, Anthropic, and CoreWeave, could weaken broader equity returns and compress the premium valuations currently held by AI market leaders. The warning is based on approximately 40 years of US market data covering roughly 12,000 IPOs.

When large IPOs enter the market, institutional investors often trim existing holdings, including incumbent AI leaders, to free up capital for participation in new listings. This reallocation of capital reduces the scarcity premium that concentrated AI stocks have historically benefited from, putting downward pressure on their relative valuations.

BCA Research's dataset shows that only around 20% of large-scale IPO waves have historically coincided with market peaks; the remaining 80% preceded weaker forward returns without a sustained downturn. This means an IPO surge is a cautionary indicator, not a definitive signal to exit equity positions.

The most frequently cited AI IPO candidates as of June 2026 include xAI, Anthropic, CoreWeave, and Databricks, all of which remain private or pre-filing. Their eventual listings are expected to provide investors with new pure-play AI exposure, potentially diluting the scarcity premium currently held by incumbent AI leaders.

Investors should track the pace of large AI IPO filings such as S-1 submissions from xAI or Anthropic, institutional commentary on portfolio rebalancing ahead of major listings, and the relative performance of established AI leaders versus newly listed AI companies in the weeks following significant IPOs.