Why AI Needs Enterprise SaaS More Than It Threatens It

24 mins ago

The most-discussed question in AI investing right now, whether to back hardware or software, is actually the wrong question. It frames the decision as a binary when the real differentiator is something both hardware and software companies can either have or lack entirely: ecosystem ownership and switching costs.

The question is live because the AI buildout is generating enormous revenue for chipmakers and GPU vendors, numbers that are difficult to argue with. But historical technology cycles suggest that hardware booms rarely translate into durable investor compounding. Meanwhile, the companies that were supposed to be the clear software winners are facing a structural challenge from open-source models and cheap local compute that was not priced in at the start of the cycle.

Here is the analytical framework that cuts through both the hardware hype and the reflexive “software always wins” assumption, so you can evaluate any AI company on the variable that actually drives long-term returns.

The PC era generated enormous revenue for hardware manufacturers. Dell and Hewlett-Packard shipped millions of units, scaled globally, and reported headline growth that looked, for a while, indistinguishable from structural compounding. Then the cycle turned. Hardware margins compressed as competition caught up, and the lasting value concentrated in Microsoft, the company selling software that replicated at near-zero marginal cost into every machine those hardware firms shipped.

The canonical comparison is owning Microsoft versus owning Dell or HP during the 1990s. Software captured the majority of value created; hardware manufacturers, despite the unit-volume boom, did not.

The structural economics that drove that divergence still apply. Software businesses carry three advantages that compound over time:

The lesson is not that hardware companies fail. It is that hardware companies tend to experience boom-and-bust cycles while software firms compound. For AI, the question is whether anything fundamental has changed that breaks this pattern.

The hardware bull case is not speculative. The numbers are genuine and large.

The scale of the current AI investment boom puts this cycle in historically unprecedented territory: US IT spending reached 4.9% of GDP in Q1 2026, surpassing both the dot-com era peak and the cloud buildout peak, with combined hyperscaler CapEx commitments for 2026 sitting in the $600-$805 billion range.

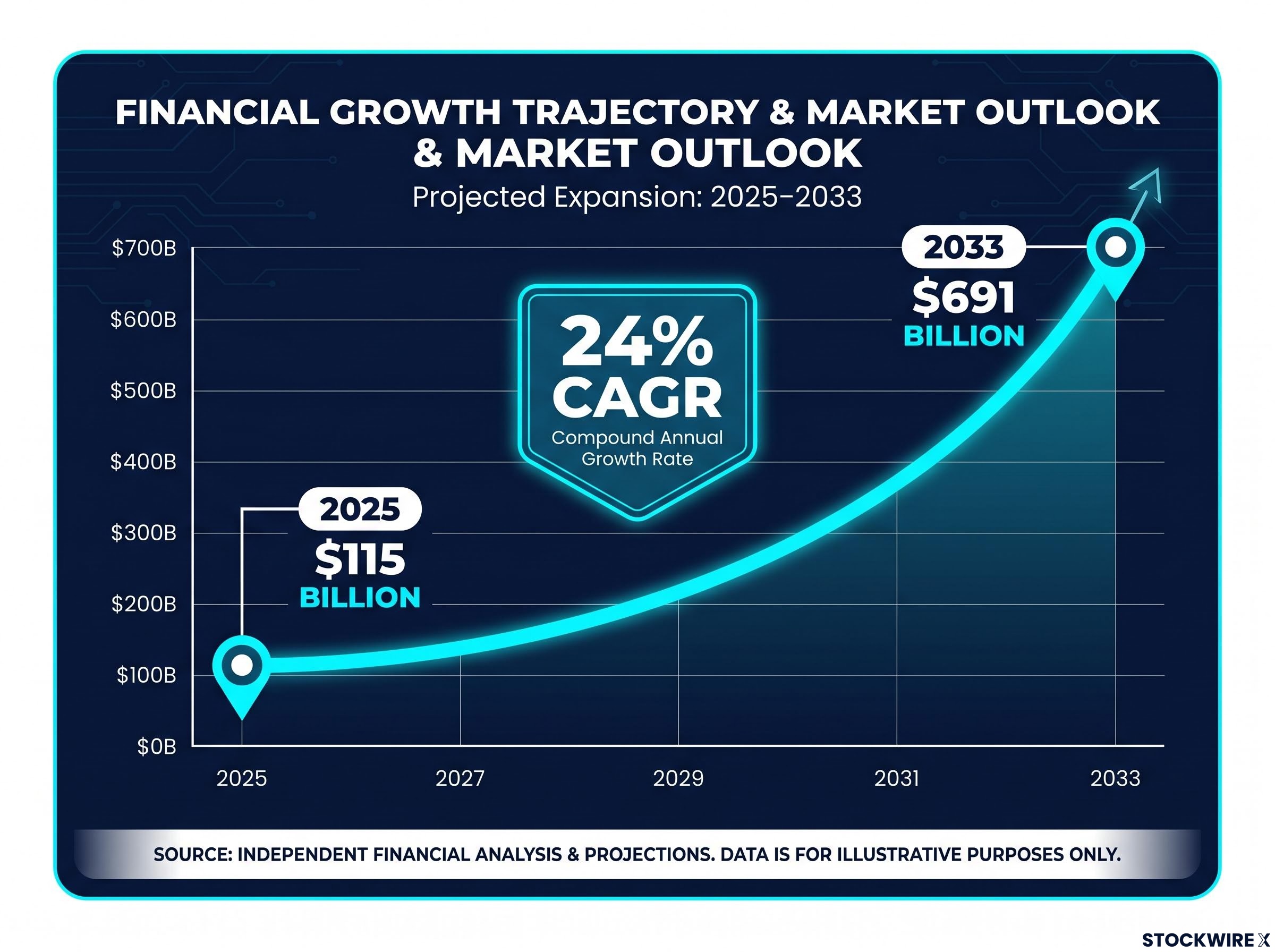

The global AI hardware market was approximately $115 billion in 2025 and is projected to reach approximately $691 billion by 2033, growing at a compound annual growth rate of roughly 24%. Data centre expansion, generative AI, and edge computing are all driving demand for high-performance GPUs, AI accelerators, and specialised processors.

That growth trajectory validates the buildout. But growth and durability are different claims, and the volatility data makes cycle risk feel immediate rather than theoretical.

| Company | Event | Share Price Move | Timeframe |

|---|---|---|---|

| SanDisk | AI-driven memory demand surge | Approximately +4,000%, followed by a material overnight decline | One-year trailing period |

| Micron | Earnings-related sell-off during the boom | Approximately -10% overnight | Single session |

The mechanism behind this cyclicality is structural. Hardware manufacturers must forecast demand, manage inventory, and compete on process and capacity. When demand plateaus or competition catches up, corrections are sharp. Some firms are attempting to stabilise revenue by securing multi-year supply contracts with large technology buyers, importing recurring-revenue characteristics, but this remains the exception rather than the norm.

The volatility data is not a reason to avoid hardware entirely. It is a signal that hardware positions require a different mental model from software positions. Cycle awareness and timing matter in ways that they do not for platform businesses with embedded switching costs. If you hold hardware names, you need to know whether you are in a cyclical momentum trade or a structural compounder, because the correct holding period, position size, and exit criteria are completely different for each.

Software’s structural advantages, scalability, switching costs, recurring revenue, are genuine and historically well-supported. The instinct that software captures more durable value than hardware is grounded in decades of evidence. The problem is that applying it automatically to every AI software company is where the logic breaks.

Open-source AI models and cheap local hardware introduce a substitution risk that most standard software-as-a-service (SaaS) businesses have never faced at this scale. Stock of the Apple Mac Mini was exhausted across Australian retailers as consumers raced to run AI models on local devices rather than through cloud subscriptions. The same dynamic played out at the level of small organisations: one podcast host recounted building a local AI agent on a home iMac, wiring it into a team group chat, and setting it to handle assigned tasks around the clock, effectively replacing per-token cloud spend with a one-time hardware purchase.

Linux Foundation research on open model economics quantifies the cost gap between open and closed AI models, finding that comparable performance is increasingly available at materially lower cost, a dynamic that directly pressures the recurring revenue assumptions underpinning most cloud AI subscription valuations.

Three conditions make a cloud AI subscription business vulnerable to this substitution:

The parallel to the streaming industry is instructive. Early broad adoption later stratified into a smaller pool willing to pay for multiple premium services and a larger pool content with cheaper or free options. Cloud AI subscriptions may follow the same path.

Moore’s Law suggests that cost per token of AI model usage should, over time, decline. As that cost falls, AI providers must grow volume faster than price declines to sustain revenue. If a meaningful portion of future volume migrates to open-source or local solutions, the addressable volume pool shrinks precisely as per-unit pricing compresses. That double pressure is the specific risk that should be modelled before buying any cloud AI subscription business, not after.

Not all hardware companies fit the commodity supplier model. A specific class of hardware business behaves more like a platform, combining high-performance compute, networking and memory bandwidth, and a developer software ecosystem into a unified stack that customers standardise on.

The mechanism is straightforward: once a developer builds on a particular GPU ecosystem’s libraries, tools, and software environment, re-platforming involves significant cost, risk, and retraining. That creates the same switching costs that traditionally belong to software.

Nvidia exemplifies this concretely. Rather than relying solely on cloud intermediaries, the company has moved to sell purpose-built AI computing systems straight to end users. Its DGX Spark device carries a retail price of approximately $9,000 and ships with 128 GB RAM and a 4 TB SSD. At the higher end, the RTX 5090 is priced at roughly $6,000 and the RTX Pro 6000 at roughly $20,000. By spanning both consumer and enterprise segments directly, Nvidia embeds its ecosystem across a wider base than cloud-only distribution would allow. Apple is pursuing a similar logic through unified memory architecture and on-device AI processing, another hardware-software integration play aimed at creating ecosystem stickiness.

Three diagnostic criteria separate these businesses from commodity chip suppliers:

Venture capital investment in robotics and physical AI rose from approximately $4.2 billion in 2019 to $26 billion in 2025, reflecting institutional recognition that some physical AI infrastructure plays carry durable moats that justify long-cycle capital allocation.

AI infrastructure constraints on deployment, particularly power availability and grid interconnection timelines, function as a separate moat layer that neither chip suppliers nor model providers fully control, and companies positioned at those physical bottlenecks have historically built compounding franchises comparable to the railroad enablers of earlier industrial revolutions.

The investor takeaway is not “Nvidia is a buy.” It is a diagnostic question: does this hardware company own a developer ecosystem and create real re-platforming costs, or is it selling commoditised performance at a price that will compress as more suppliers enter?

The complexity above collapses into a four-step diagnostic sequence you can apply to any AI holding or prospective investment.

| Stack Layer | Key Diagnostic Question | Holding Posture |

|---|---|---|

| Raw components and chips | Is competitive advantage transient or ecosystem-embedded? | Cyclical; timing and exit criteria matter |

| Data centre and cloud infrastructure | Does the company control standards or sell capacity? | Depends on switching costs; evaluate individually |

| Model providers | How exposed is the pricing model to open-source substitution? | High conviction required; stress-test recurring revenue |

| Applications and vertical SaaS | Are there workflow-embedded switching costs and data lock-in? | Compounder if moats verified; position for patience |

An additional risk for hardware businesses worth noting: hyperscalers are building custom silicon, and Apple has reportedly sought regulatory approval to procure memory from Chinese manufacturers, a move that signals large buyers are willing to pursue lower-cost supply chains even when doing so involves geopolitical complexity. Incumbent suppliers face sustained pricing pressure as a result.

Mapping where profit concentrates across the AI supply chain reveals a striking valuation divergence: legacy application software multiples compressed approximately 41% over the trailing twelve months, while AI-native firms trade at a median of roughly 21x EV/revenue, a split that mirrors the hardware-versus-platform distinction this framework identifies at the moat level.

Working through this framework on a position you currently hold will, in many cases, reveal that you are treating a cyclical position as if it were a structural compounder, or vice versa. Both errors are common, and both lead to suboptimal entry and exit decisions.

The “hardware or software” frame most investors arrive with is a shortcut, and it produces shortcut conclusions. The durable variable is not which layer of the stack a company occupies. It is whether the company owns the customer relationship, the workflow dependence, or the developer ecosystem in a way that makes switching costly.

This produces a counterintuitive portfolio implication: some hardware companies belong in the “compounder” category and some software companies belong in the “cyclical or vulnerable” category. Layer alone is an unreliable signal.

Portfolio managers in public markets have already begun trimming semiconductor holdings after sharp run-ups, applying cycle awareness even as the buildout continues. The “good enough” threshold concept suggests the AI investment landscape will ultimately stratify in the same way other technology markets have, with a small premium tier for genuinely indispensable platforms and a larger commoditised tier where margins compress.

For readers wanting to apply the compounder-versus-cyclical framework to a concrete position, our full explainer on Microsoft’s AI risks examines how OpenAI compute diversification, agentic bundle erosion, and duration sensitivity interact beneath 15-18% revenue growth, providing a worked example of how structural pressures can build before they appear in reported metrics.

Three portfolio implications flow from this framework:

The AI cycle is still in early stages. The distinction between cyclical beneficiary and structural compounder is not yet fully priced in. For your portfolio, that gap is where the framework pays off: identify which of your positions have clear switching costs embedded in customer workflows, and which are riding the buildout wave without them. Those two categories deserve fundamentally different position sizing and exit logic.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

—

A cyclical AI company generates strong returns during a buildout phase but remains tied to boom-and-bust demand cycles, while a structural compounder grows and defends margins over time because customers face real costs when switching away from its platform.

During the 1990s PC cycle, hardware manufacturers like Dell and HP delivered impressive unit volume but ultimately saw margins compress, while Microsoft captured the majority of value created because its software replicated at near-zero cost with embedded switching costs; the same structural economics apply to AI.

Token deflation refers to the long-run decline in the cost per unit of AI model usage as compute improves; if pricing compresses while open-source and local alternatives absorb volume, cloud AI subscription businesses face a double pressure on revenue that needs to be stress-tested before investing.

Open-source models increasingly match the performance of proprietary cloud AI at materially lower cost, and cheap local hardware like Apple's Mac Mini lets individuals and small organisations replace recurring subscription spend with a one-time purchase, creating a substitution risk that most SaaS businesses have never faced at this scale.

Nvidia sells an integrated full stack combining high-performance compute, networking, and a developer software ecosystem, meaning developers who build on its libraries and tools face significant re-platforming costs, which creates the kind of switching costs that traditionally belong to software businesses rather than hardware vendors.