TSMC just reported what may be its most profitable quarter in history, with net profit surging as AI chip demand breaks records. The same week, the Philadelphia Semiconductor Index shed over 2% of its value.

That is not a contradiction. It is the story.

The semiconductor sector has entered a phase where the strength of actual business results is no longer sufficient to move stocks higher. After a powerful AI-fuelled rally in early 2026, chipmakers now face a more demanding market, one that is actively interrogating whether future earnings can justify the prices already embedded in valuations. Understanding this shift matters for anyone watching AI infrastructure spending, technology sector allocations, or the broader trajectory of the AI trade.

Here is the specific mechanics driving the disconnect, using TSMC and ASML as the primary case studies, and the forward indicators that will determine whether this is a healthy consolidation or the beginning of a more sustained de-rating.

TSMC’s record quarter, in the numbers that matter

Start with the scale of what TSMC actually delivered, because the gap between these results and the market’s reaction is the fact that frames everything else.

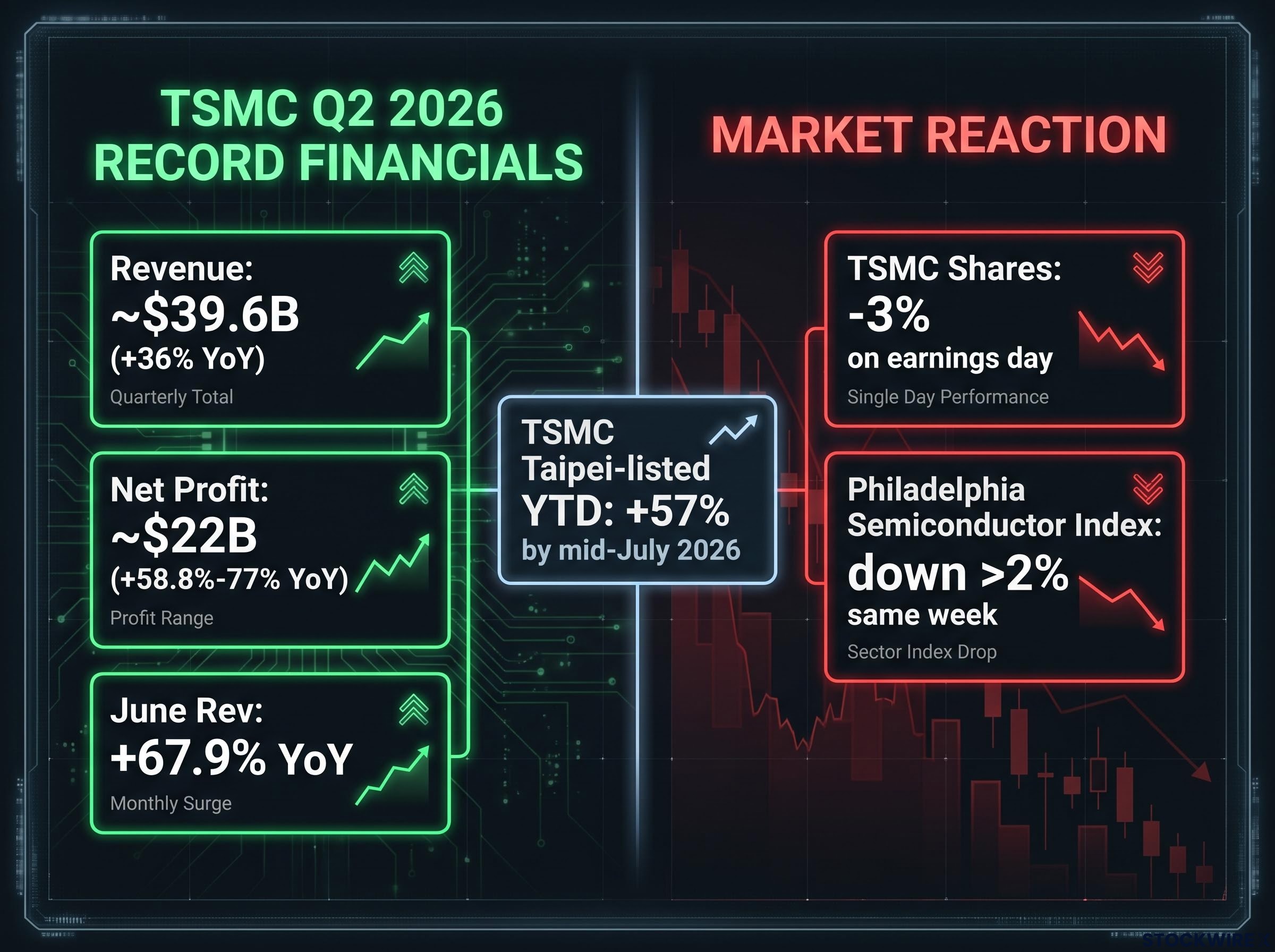

Q2 2026 revenue came in at approximately T$1.27 trillion (roughly $39.6 billion), up 36% year-over-year and above the top end of TSMC’s own guidance range of $39-$40.2 billion. Net profit hit T$706.6 billion (approximately $22 billion), with year-on-year growth between roughly 58.8% and 77% depending on methodology and timing of final conference call data released 16 July 2026. June monthly revenue alone surged 67.9% year-over-year. First-half revenue reached T$2.4 trillion (approximately $75 billion), up 35.6% on the prior year.

These are not modest beats. They are historically exceptional.

TechPowerUp’s reporting on TSMC’s Q2 2026 results confirms consolidated revenue of $40.20 billion and strong diluted EPS growth, with leading-edge process technology demand from AI customers cited as the primary driver of the outperformance.

| Metric | Q2 2026 Result | Market Reaction |

|---|---|---|

| Revenue | ~$39.6B (up 36% YoY) | Beat top of guidance range |

| Net Profit Growth | ~58.8%-77% YoY | TSMC shares fell ~3% on earnings day |

| June Monthly Revenue | Up 67.9% YoY | Philadelphia Semiconductor Index down >2% |

| H1 2026 Revenue | ~$75B (up 35.6% YoY) | Sector-wide profit-taking continued |

The gap between what TSMC reported and how its stock moved is the signal to hold in mind for everything that follows. It reframes what the market is actually pricing right now: not the present, but the sustainability of the future.

ASML’s parallel experience reinforces the pattern

ASML, which manufactures the extreme ultraviolet (EUV) lithography tools required for the most advanced chips, delivered a parallel experience. Its results came in ahead of expectations, it lifted its forward guidance, and management pointed to AI as a durable structural source of chip demand.

The stock dropped as much as 6% intraday, closed approximately 2.5% lower, and slid further the following day.

This is not a TSMC-specific anomaly. It is a sector-wide pattern: record results, falling stocks.

When big ASX news breaks, our subscribers know first

What record earnings look like when the market has already moved on

The instinct is to call this irrational. It is not. It is the predictable output of a market that priced in these results months earlier.

TSMC’s Taipei-listed shares were up approximately 57% year-to-date by mid-July 2026. That run-up did not happen in a vacuum. It happened because the market spent the first half of the year embedding the AI growth story into the price before the earnings arrived.

By the time TSMC reported, the record quarter was not new information. It was confirmation of what the stock had already paid for. The earnings release functioned less as a catalyst and more as a liquidity event, a moment for investors who had captured the pre-earnings gain to lock in profits.

Three specific factors transformed record earnings into a sell-the-news event:

Valuation dispersion across chip names is wider than sector-level indices suggest: Micron trades below 9x forward earnings while Intel sits at roughly 101x, meaning the valuation discipline the market is currently applying to TSMC and ASML is not uniform across the sector and requires name-by-name analysis rather than index-level conclusions.

- Pre-positioned valuations: A 57% year-to-date gain means the stock had already borrowed from its own future returns. A record quarter could justify the price already paid, but not add meaningfully to it.

- ASML EUV shipment commentary: ASML referenced approximately 80 low-NA EUV systems targeted for 2027, which fell short of some analyst hopes for closer to 90 systems, introducing a subtle disappointment into the forward outlook.

- No meaningful guidance surprise: TSMC’s full-year outlook, initially set at slightly above 30% revenue growth, contained nothing beyond what was already modelled into consensus estimates.

A similar pattern played out in 2025. TSMC posted a historic AI-driven profit surge that year, and semiconductor stocks retreated in the same manner, with questions about whether the pace of growth could be sustained dominating the post-earnings conversation. This is repeating market behaviour, not an anomaly.

What the AI chip supercycle actually is, and where the market now sits within it

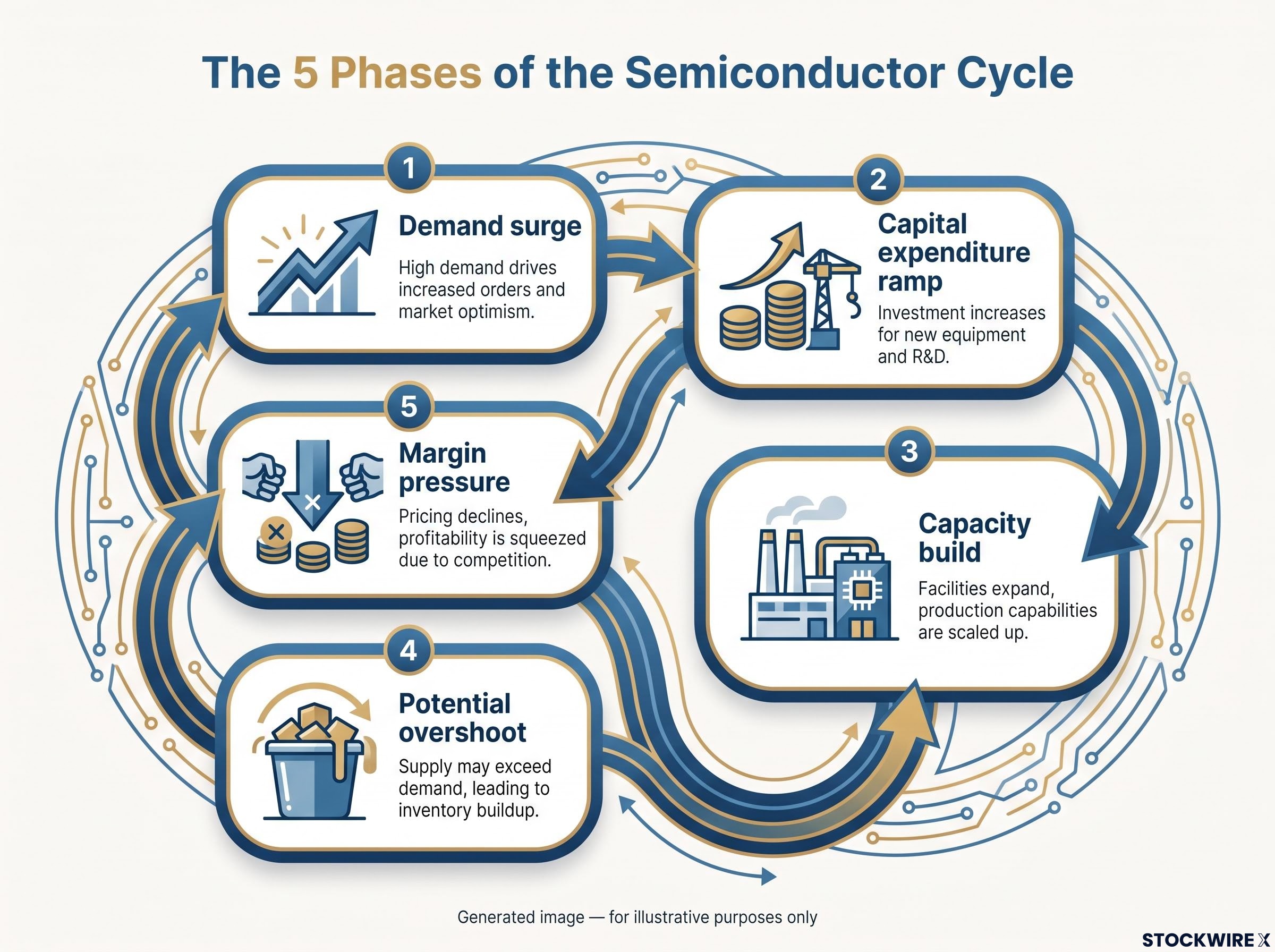

To understand why investors can be anxious about a sector posting record profits, you need to understand how semiconductor cycles work.

Semiconductor cycles, the recurring patterns of boom and correction in the chip industry, follow a predictable structural sequence:

- Demand surge: A new application (in this case, AI) creates a step-change in chip consumption.

- Capital expenditure ramp: Chipmakers and their equipment suppliers invest heavily to expand capacity.

- Capacity build: New fabrication plants come online, increasing the industry’s total output.

- Potential overshoot: If investment runs ahead of demand growth, the industry builds more capacity than it needs.

- Margin pressure: Overcapacity compresses pricing power, and margins fall even if revenue stays elevated.

ASML’s equipment order data functions as a 12-18 month forward indicator of fab expansion. That is the time it takes for an order placed today to translate into operational capacity. When order trends moderate, the market treats it as an early warning sign for a later slowdown, regardless of how strong current earnings look.

Why AI demand does not automatically break the cycle

AI represents a genuine structural demand driver. TSMC described chip demand as “insatiable” earlier in 2026 and raised its full-year revenue outlook accordingly.

But structural demand does not eliminate the risk of over-investment. Market participants have begun questioning whether sector growth can sustain its rapid pace in the quarters ahead, even with AI orders remaining solid. Commentary in 2025 already flagged sustainability concerns and over-building risk while profits were hitting records.

The shift is subtle but important: the market has moved from price discovery (how big could AI be?) to valuation discipline (is the growth large enough, for long enough, to justify what has already been paid?). For anyone holding semiconductor exposure, the relevant question is not whether TSMC will keep selling chips. It is whether the earnings growth rate will remain high enough to justify the price paid today.

The policy and geopolitical ceiling on semiconductor valuations

Even if AI demand continues to exceed expectations, external risk factors cap how high investors are willing to take semiconductor multiples. These are not tail risks. They are structural valuation constraints permanently in the background.

Three primary external factors are compressing the upside case:

- Export controls on China: ASML faces ongoing pressure from U.S. restrictions and European regulatory alignment limiting its most advanced tool shipments to China. This creates a persistent revenue ceiling that analysts must model, compressing the upside case even in strong demand environments.

- Taiwan geopolitical exposure: TSMC’s geographic concentration in Taiwan leaves it exposed to geopolitical risk that resurfaces as a valuation discount whenever multiples look stretched or macro conditions shift.

- Tariff and trade policy uncertainty: Equipment makers including ASML have flagged tariff and policy risks as potential 2026 headwinds in management commentary, creating the possibility that revenue growth moderates even if AI orders remain solid.

The risk picture is asymmetric. AI upside is capped by policy; downside is not. Policy risk does not need to materialise into actual revenue losses to affect stock multiples. The mere possibility of a revenue ceiling is enough to limit how much investors will pay for earnings that have not yet arrived. That dynamic helps explain why strong fundamentals and falling stocks can coexist without the market being wrong.

Export control durability is a structural feature of the AI chip supply chain rather than a cyclical policy risk: US restrictions on advanced semiconductors are grounded in bipartisan national-security law, placing them outside the reach of trade negotiators and making them a permanent valuation ceiling regardless of diplomatic progress.

How this plays beyond the chip sector

TSMC and ASML sit at the core of the AI hardware stack, and the market reads their post-earnings behaviour as a signal for the broader AI trade.

When the two most important companies in AI chip manufacturing report record results and their stocks fall, it feeds concern that extends well beyond semiconductors. In 2025, weakness in chip names following TSMC’s strong results weighed directly on wider semiconductor and technology indices, even when the underlying fundamental story remained positive. The transmission mechanism is well-established.

The market is no longer asking whether AI chips will sell. It is asking whether they will sell enough, for long enough, to justify the prices already paid.

That question is the defining feature of the current phase. The AI trade has moved from momentum-driven price discovery to valuation discipline. In practical terms, this means investors with exposure not just to chip stocks but to AI infrastructure plays, cloud names, and technology indices broadly should understand that this valuation reckoning in semiconductors functions as an early-warning system. If TSMC’s record quarter cannot move the Philadelphia Semiconductor Index higher, the implication for broader technology sector positioning is that the market’s tolerance for AI-story valuations has become meaningfully more demanding.

The next major ASX story will hit our subscribers first

The forward indicators that will settle this question

Rather than reacting to each headline, four specific indicators will tell you whether this is a consolidation within a durable trend or the beginning of a more sustained de-rating:

- Hyperscaler and cloud capital expenditure guidance for H2 2026 and into 2027. This is the primary leading demand signal for AI chip orders. Whether spending commitments continue to step up, hold flat, or show signs of plateauing will reveal whether the demand intent behind AI investment is still accelerating.

- Order and backlog commentary from Nvidia, AMD, and major cloud custom-chip programmes. Pay particular attention to lead times and any signs of double-ordering or inventory build. These would signal demand pull-forward rather than durable growth, a distinction that matters enormously for sustainability.

- ASML EUV order trends and shipment plans. As the 12-18 month forward indicator for cutting-edge capacity additions, ASML’s order book reveals how aggressively the industry will continue expanding. Any moderation here is treated as an early warning for a later slowdown.

- Policy and export control developments. Export restrictions, tariffs, and China exposure can compress valuation multiples even when earnings remain strong. Watch for any tightening of U.S. or European restrictions on advanced semiconductor equipment.

Each indicator reveals something different. Capital expenditure guidance reveals demand intent. Order backlog reveals whether that demand is durable or front-loaded. ASML orders reveal the supply-side response. Policy signals reveal the ceiling on what the market will pay. Positive surprises across these indicators could allow earnings growth to “grow into” current valuations. Negative surprises or faster normalisation would extend the de-rating even as companies report solid numbers.

What the sell-off tells you, and what it does not

The AI demand story, as evidenced by TSMC’s record quarter and ASML’s raised guidance, remains fundamentally intact. Nothing in the Q2 2026 data suggests a deceleration in the appetite for advanced AI processors. TSMC described demand as “insatiable” earlier this year, and these results are consistent with that characterisation.

What has changed is what kind of evidence investors now require to maintain or add to semiconductor positions. The market’s reaction does not reflect a loss of confidence in AI itself. It reflects a transition from momentum-driven to fundamentals-disciplined investing in the sector, a phase that tends to produce more selective, volatile price action even in a structurally strong industry.

Semiconductor positioning data from Bank of America shows active long-only overweights at approximately 20%, half the 2017 cycle peak of 40%, which complicates the narrative that the current sell-the-news dynamic reflects speculative excess rather than valuation discipline in a fundamentally supported sector.

The sell-off is not the market saying AI is over. It is the market saying the price of believing in AI has to be earned quarter by quarter from here, not discounted years into the future in a single re-rating event.

The distinction that matters: AI’s structural reality is not in question. Whether that reality is already in the price is.

This pattern played out in 2025 and is repeating now: strong fundamental results, soft stock reactions, with valuation and sustainability questions dominating the post-earnings narrative. Investors who understand this distinction will make better-informed decisions about semiconductor sector positioning, separating the AI fundamental story from the separate, and currently more demanding, question of whether current prices already reflect it.

For readers wanting to place the current valuation reckoning in longer historical context, our deep-dive into the supercycle versus dot-com comparison examines how the $3.8 trillion rally in semiconductor market cap compares structurally to the 2000 cycle, including the role of agentic AI in converting episodic chip demand into permanent baseline consumption.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.