McPherson’s Ltd Flags FY26 Revenue and EBITDA Pullback Ahead of Audited Results

McPherson’s flags FY26 revenue and earnings pullback ahead of audited results

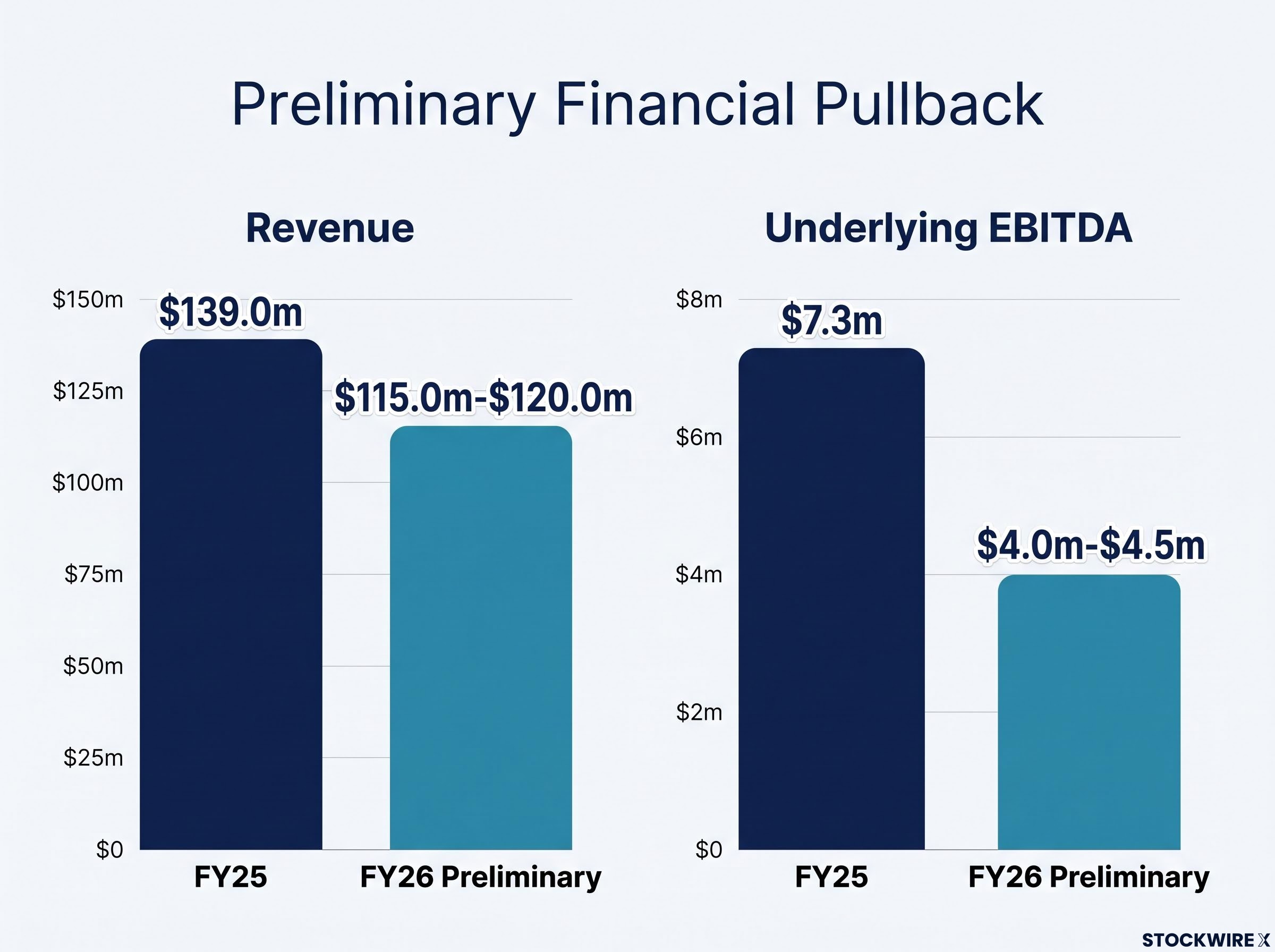

McPherson’s Limited (ASX:MCP) has released preliminary unaudited results for the full year ended 30 June 2026 (FY26), flagging lower revenue and underlying earnings compared with FY25, alongside anticipated non-cash intangible asset impairments.

The health and beauty products supplier expects FY26 revenue from continuing operations of $115.0m to $120.0m, down from $139.0m in FY25, with underlying EBITDA of $4.0m to $4.5m versus $7.3m a year earlier. Audited results are scheduled for release on Thursday 27 August 2026.

These figures are preliminary, unaudited management estimates and remain subject to audit adjustment.

When big ASX news breaks, our subscribers know first

FY26 preliminary results at a glance

The table below summarises the headline metrics disclosed in the trading update against the prior comparable period.

| Metric | FY26 (preliminary) | FY25 | Change / Note |

|---|---|---|---|

| Revenue from continuing operations | $115.0m–$120.0m | $139.0m | Lower year-on-year |

| Underlying EBITDA | $4.0m–$4.5m | $7.3m | Lower year-on-year |

| 2H26 underlying EBITDA | $1.8m–$2.3m | n/a | Half-on-half vs $2.2m in 1H26 |

| Net cash | $4.5m (30 June 2026) | $8.8m (30 June 2025) | Lower year-on-year |

| Non-cash intangible impairments | $15.0m–$20.0m | n/a | Preliminary, unaudited |

Notably, second-half underlying EBITDA of $1.8m to $2.3m held broadly in line with the $2.2m recorded in the first half, despite the full-year decline against FY25.

What drove the softer FY26 performance

As foreshadowed in the Company’s announcement dated 23 April 2026, the anticipated result reflects challenges relating to the transition to its new operating model, which affected sales performance during the year. Management identified several contributing factors tied to this transition:

The April 2026 guidance revision had already flagged that sales were tracking below expectations during the operating model transition, with external supplier surcharges compounding the earnings pressure at that point in the year.

-

Forecast variability as the business adapted to new ordering patterns

-

Reduced in-store availability from range rationalisation

-

Delayed impacts of out-of-stocks, which, although resolved early in 2H26, constrained participation in customer promotional activity

Since the April 2026 update, a number of McPherson’s customers have reduced inventory cover days, adjusted stock levels and tightened ranging in response to broader macro-economic conditions and competitive dynamics within channels.

The Company noted that while ordering patterns from customers have “largely stabilised”, a level of variability remains. This, coupled with the decision to increase inventory levels, impacted closing cash balances.

Several of the identified problems, such as out-of-stocks, were already resolved early in the second half.

Cost discipline and balance sheet strength

Offsetting the softer top line, the new operating model continues to deliver cost benefits, while the Company retained a net-cash position at year end. Management highlighted the following points:

-

The new operating model is delivering materially lower distribution costs, improved efficiency and tighter overhead control, partly mitigating the impact of lower sales revenues

-

A&P (advertising and promotion) spend was reduced in 2H26 in a disciplined manner

-

Net cash stood at $4.5m as at 30 June 2026, with debt facilities undrawn

Under the on-market share buy-back announced on 25 February 2026, the Company acquired 4,995,130 shares for a consideration of $0.8m.

The combination of an undrawn debt facility and a net-cash balance sheet underpins financial flexibility as the business works through the operating-model transition.

Understanding non-cash impairments

The trading update flagged preliminary non-cash intangible asset impairments in the order of $15.0m to $20.0m. For readers less familiar with the term, an impairment is an accounting write-down that reduces the carrying value of an asset on the balance sheet when its recoverable value falls below what is recorded.

Crucially, these impairments do not involve any cash outflow. They reflect trading performance relative to plan and will be classified as material items in the FY26 accounts, meaning they will not impact underlying earnings.

The announcement also preserved an important nuance on reversibility:

From the ASX announcement

“To the extent impairments relate to McPherson’s brands, these may be reversed upon an improvement in the performance of the brands.”

The next major ASX story will hit our subscribers first

What comes next for McPherson’s

The Company expects to release its audited FY26 results on Thursday 27 August 2026, and the preliminary figures may be subject to audit adjustment before then.

Management indicated that ordering patterns have largely stabilised, that out-of-stock issues were resolved early in 2H26, and that cost savings from the new operating model continue to embed. These factors form the basis of the stabilisation narrative underpinning the update.

The Company’s portfolio remains anchored in iconic health and beauty brands, including Manicare, Swisspers, Lady Jayne, Maseur, Glam, Dr. LeWinn’s and Fusion Health, sold through pharmacy, grocery, health food and e-commerce channels. Backed by a net-cash balance sheet, McPherson’s awaits the release of its audited FY26 results on Thursday 27 August 2026.

Don’t Miss the Next Consumer Sector Move

Big News Blast delivers FREE breaking ASX consumer sector news directly to your inbox within minutes of release, complete with in-depth analysis already done for you. Join 20,000+ investors staying ahead of the market. Click the “Free Alerts” button at StockWire X to start receiving alerts the moment news breaks.