The a2 Milk Company FY26 Revenue Tops Guidance as China Supply Clears

a2 Milk resolves China supply chain disruption as FY26 revenue beats guidance

The a2 Milk Company has confirmed that the China label infant milk formula (IMF) supply chain issues that hit its fourth quarter of FY26 have now been substantially resolved, while preliminary FY26 results have landed in line with or slightly ahead of April guidance.

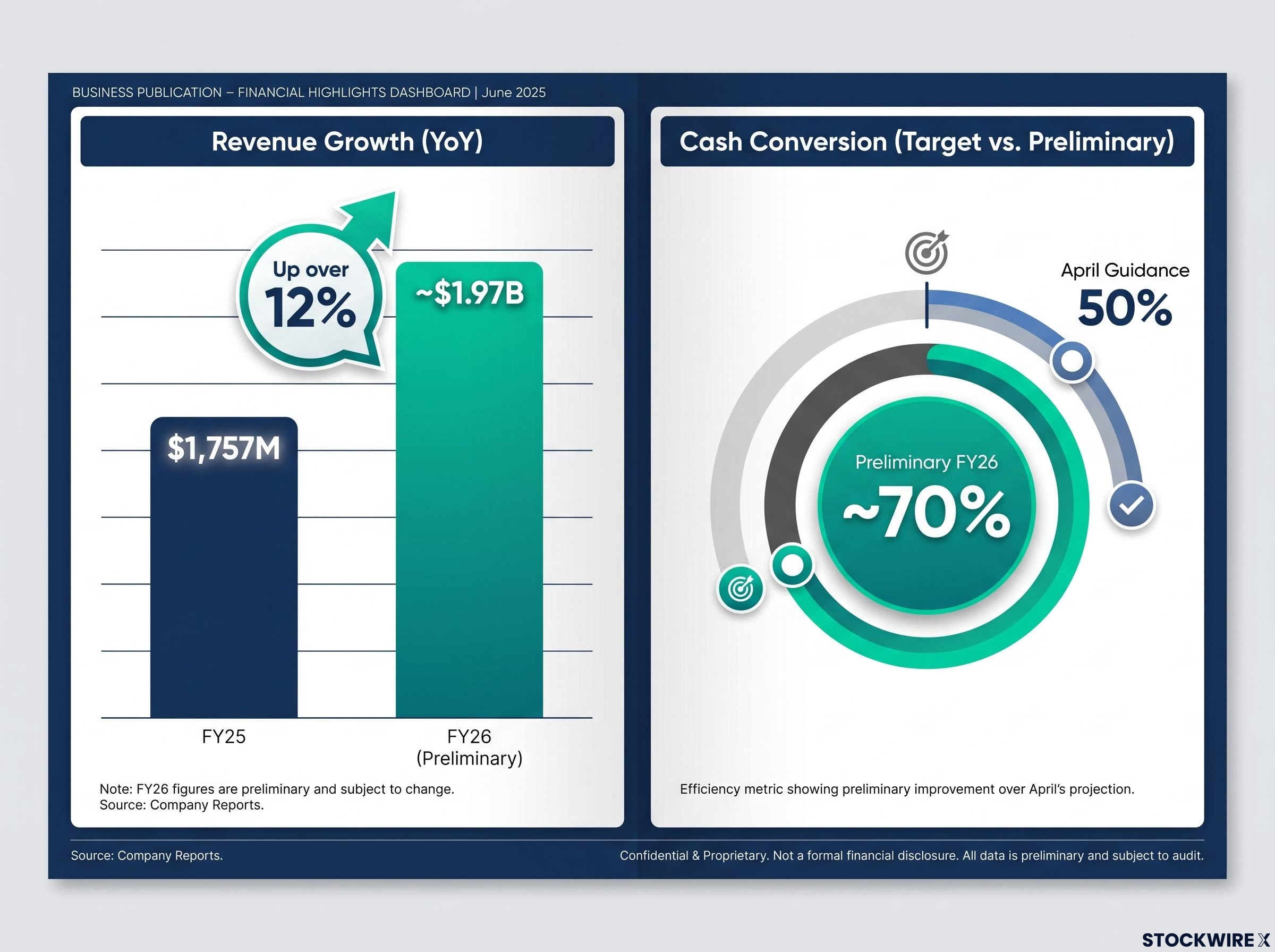

The dairy nutrition group expects revenue of approximately $1.97 billion, up over 12% on FY25. This preliminary, unaudited update, released on 7 July 2026, precedes the audited FY26 results due on 17 August 2026.

For investors, the message is twofold. A short-term operational disruption in the China channel is resolving, while the broader business delivered results above expectations across multiple financial metrics.

When big ASX news breaks, our subscribers know first

FY26 revenue climbs over 12% despite China headwinds

The Company expects to deliver FY26 results in line with, or slightly ahead of, the guidance range announced on 13 April 2026, expressed on a continuing operations basis. The preliminary figures point to a beat across several key measures.

China label IMF sales were down approximately 14% on FY25, reflecting the supply issues that materially impacted product availability in the final quarter. All other product categories, including English label IMF, Other Nutritionals and Liquid Milk, performed strongly and are significantly up on FY25.

The result compares favourably against the April Guidance on revenue growth, EBITDA margin, NPAT and cash conversion. Notably, cash conversion is expected to reach approximately 70%, well ahead of the 50% previously guided.

| Metric | April Guidance | Preliminary FY26 | vs FY25 |

|---|---|---|---|

| Revenue | Low to mid double-digit growth | ~$1.97 billion | Up over 12% |

| EBITDA % margin | 14.0%–14.5% | High end of range | — |

| NPAT | Similar to down | Slightly up on FY25 reported | Underlying NPAT expected up |

| Cash conversion | 50% | ~70% | — |

By way of comparison, FY25 continuing operations revenue was $1,757 million and FY25 reported NPAT was $203 million. The preliminary figures suggest the company absorbed a significant channel disruption while still expanding its top line by double digits.

What caused the China label IMF supply disruption, and how it was resolved

The shortfalls that hit 4Q26 stemmed from a combination of factors:

The FY26 guidance downgrade issued in April flagged five converging supply constraints, including Synlait manufacturing backlogs, enhanced cereulide testing requirements, and elevated Chinese customs inspection rates, which collectively pushed revenue recognition into FY27.

-

Strong demand in the preceding quarter

-

Freight challenges

-

Synlait production backlog

-

Extended product release times

-

Additional customs clearance requirements and testing measures

The availability impact necessitated a large proportion of existing users to switch to alternative brands, with some switching to a2™ English label products. The impact on English label IMF was limited and largely concentrated on a2 Genesis™, which was affected by planned production downtime at a2 Pokeno and a change in China importation requirements.

The Company has confirmed that the contributing factors have now substantially been resolved. Product flows to distributors and retailers have materially improved across China label and English label products, with stock levels returning to target levels.

Winning back users: the road to recovery

With supply constraints easing, the Company is now focused on sales and marketing initiatives to encourage previous China label IMF users to return. It is also accelerating new user recruitment with its retail and distribution partners.

The contributing factors to the product availability issues have now substantially been resolved, and the Company is now focused on various sales and marketing initiatives to encourage previous China label IMF users to return while accelerating new user recruitment with its retail and distribution partners.

The next major ASX story will hit our subscribers first

What’s next for a2 Milk investors

The near-term catalysts and watch-points for shareholders are as follows:

-

17 August 2026 — audited FY26 results and FY27 outlook commentary to be released

-

Preliminary figures remain subject to finalisation and external audit

-

Watch for the pace of China label user return and new user recruitment

-

Note the a2 Platinum™ transition in 1H27, referenced in the underlying results footnote, with a2 Pokeno production volumes temporarily low ahead of this transition

The preliminary update points to a resilient FY26 result delivered above guidance, despite a contained and now-resolved supply disruption. Attention now shifts to the company’s recovery efforts and its a2 Platinum™ transition heading into FY27, with the audited results in August set to provide fuller detail on the outlook.

Don’t Miss the Next Consumer Staples Winner

Big News Blast delivers FREE breaking ASX news straight to your inbox within minutes of release, complete with in-depth analysis already done for you. Join 20,000+ subscribers staying ahead of the market on Consumer Staples and beyond. Click the “Free Alerts” button at StockWire X to start receiving alerts the moment news breaks.