3 ASX Short Positions That Challenge the Price Chart

3 hrs ago

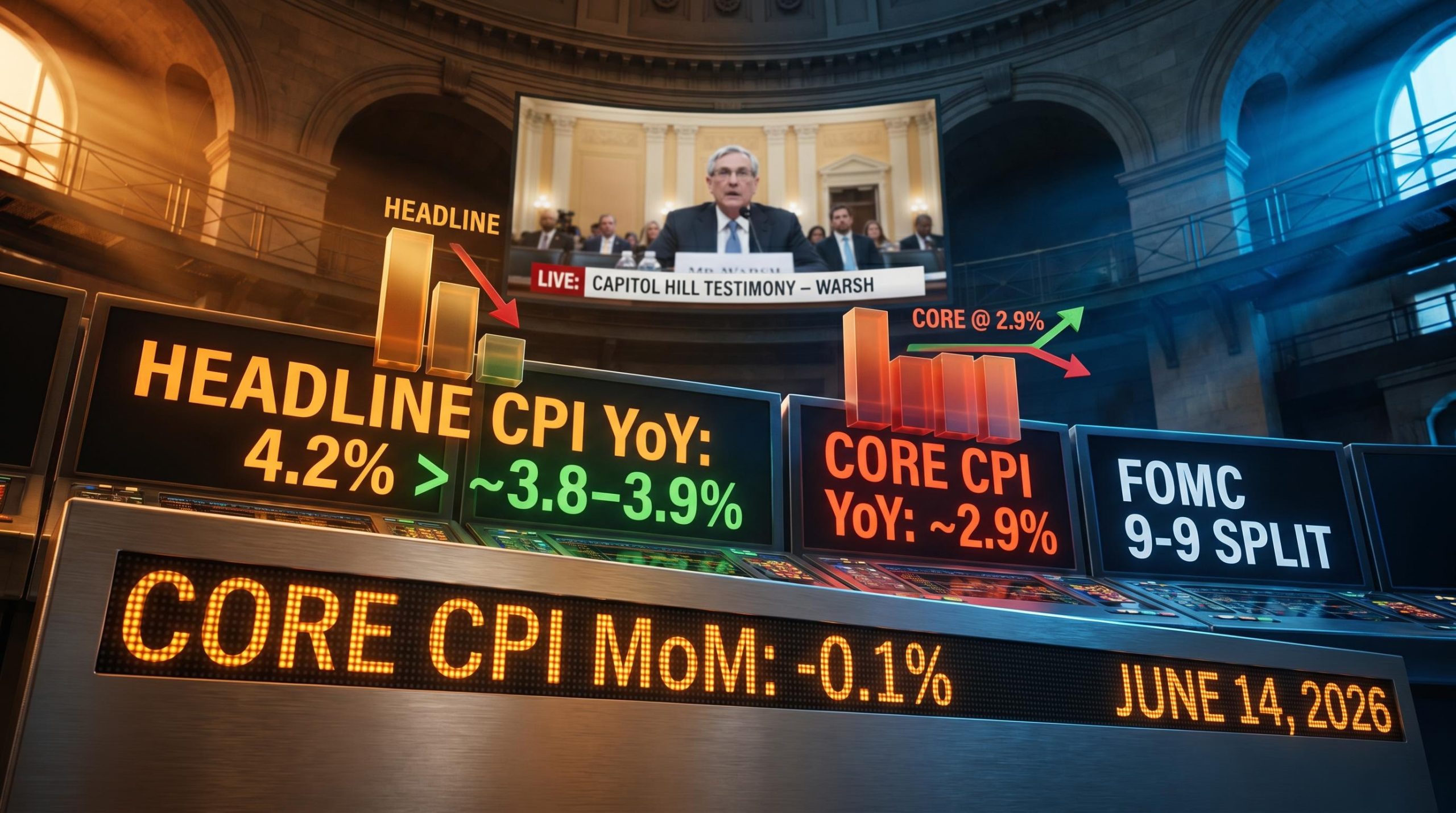

The June Consumer Price Index report lands on Tuesday, 14 July 2026, the same morning Federal Reserve Chair Kevin Warsh sits before Congress. With the committee split evenly between those content to hold rates and those pushing for at least one further increase, a single data release does not usually settle a debate. This one might move the needle.

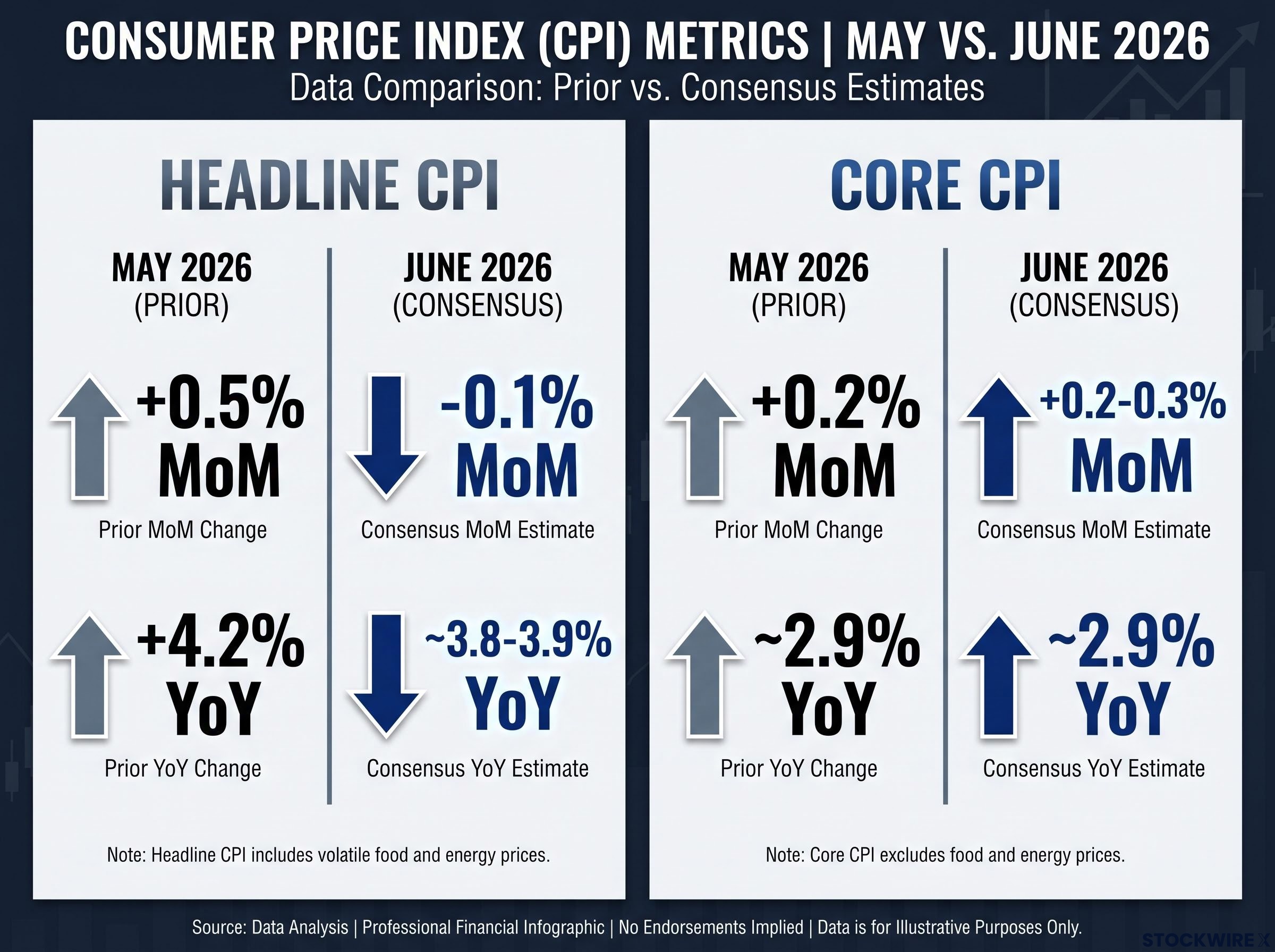

The May headline reading of 4.2% year-on-year is expected to ease noticeably as petrol prices retreat, while the core measure is forecast to remain around 2.9%, barely shifted from twelve months prior. That gap between a softening headline and a sticky core is precisely what makes this US inflation report consequential. The Fed already removed cut-leaning language at its June meeting and acknowledged the possibility of additional hikes. A single print now lands inside a policy environment with no margin for surprise in either direction.

Here is what the numbers are expected to show, what Warsh is likely to say in response, and what each scenario means for the rate path and the assets most sensitive to it, all before markets open and before the testimony begins.

For June, the consensus points to a -0.1% month-on-month headline print, a meaningful turnaround from the +0.5% recorded in May. Lower petrol prices are doing almost all of the heavy lifting, dragging the year-on-year rate toward the 3.8-3.9% range.

The May CPI report established the baseline from which Tuesday’s June release is measured: headline inflation at 4.2% year-on-year driven almost entirely by a 40.5% gasoline surge, while core held at a softer-than-expected 2.9%, confirming that the energy shock and underlying price pressure were running on separate tracks.

The complication sits underneath. Core CPI, which excludes food and energy from its calculation, is expected to come in somewhere between +0.2% and +0.3% month-on-month, leaving the year-on-year rate near 2.9%. That is essentially unchanged from a year earlier and roughly a full percentage point above the Fed’s 2% target.

| Measure | May (prior) | June consensus |

|---|---|---|

| Headline CPI (MoM) | +0.5% | -0.1% |

| Headline CPI (YoY) | +4.2% | ~3.8-3.9% |

| Core CPI (MoM) | +0.2% | +0.2-0.3% |

| Core CPI (YoY) | ~2.9% | ~2.9% |

Prediction markets still price a high probability that year-on-year CPI remains above 3.6%, signalling that markets expect only modest deceleration, not a collapse in inflation.

The gap between a falling headline and a sticky core tells you the disinflation story is real but incomplete. Investors treating a soft headline as a policy pivot signal are reading only half the data.

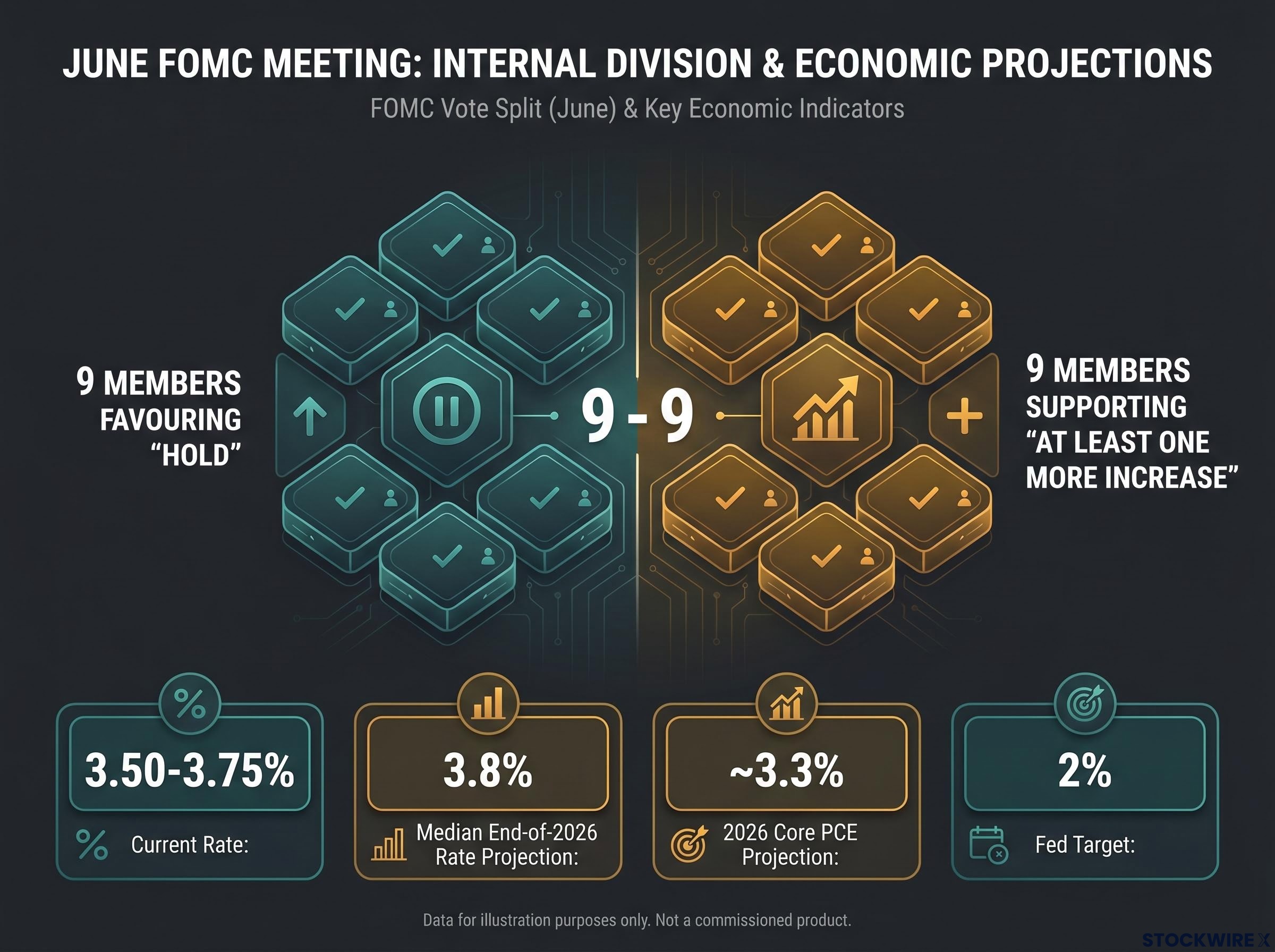

The June FOMC meeting produced a unanimous hold at 3.50-3.75%, but unanimity on the rate itself masked deep division on what comes next. Key outcomes from that meeting:

That 9-9 divide is unusually stark, even by the standards of a committee accustomed to disagreement.

Warsh’s confirmation in May 2026 placed him at the head of a committee already showing four dissenting votes, inheriting a credibility gap created when three hawkish dissenters publicly opposed the guidance language that the prior chair had defended.

The Fed’s 2% target has gone unmet for the better part of five years running, a prolonged stretch that has made committee members increasingly reluctant to call victory on the back of any single data point or short-lived favourable trend.

The dot plot shift toward 3.8% reflects this caution. The committee has revised its own confidence in a smooth glide back to 2%, and the median projection now bakes in the possibility that further tightening will be necessary to finish the job.

A 9-9 committee means Tuesday’s CPI print is not just an input into a unified policy framework. It is a swing vote in an ongoing internal argument, and that raises the stakes of any upside or downside surprise significantly.

When you see a CPI release, two numbers compete for the headline. The first is headline CPI, which measures the price change across the entire consumer basket, including food and energy. The second is core CPI, which excludes those two categories.

The Fed places greater weight on core because food and energy prices are volatile. Gasoline can swing 10% in a month on supply disruptions without reflecting anything about the broader economy. Core captures the stickier components: services, shelter, and wages, which move slowly and are harder to reverse once they accelerate.

The Fed’s own core PCE projection for 2026 sits at approximately 3.3%, a concrete measure of where its internal models expect underlying inflation to land.

When you see the headline fall but core stay near 2.9%, the Fed sees a disinflation process that is intact but unfinished. That is why this report is likely to validate a pause rather than trigger a pivot. A one-month soft headline driven by petrol prices does not change the core-focused assessment; sustained core disinflation across several consecutive months is what would be required to shift policy meaningfully.

Long and variable lags in monetary policy transmission mean that rate decisions already made are still working their way through mortgage markets, business lending, and consumer credit, which is one reason why the Fed remains cautious about declaring victory on core inflation after a single month of softer data.

Before markets open on Tuesday, it is worth mapping the three paths the data could take, because identifying which scenario has materialised in the first hour after release is worth more than any post-hoc commentary.

| Scenario | CPI print characteristics | Expected policy outcome |

|---|---|---|

| Baseline | Headline -0.1% MoM; core +0.2-0.3% MoM | Watchful pause confirmed; zero to one hike priced for remainder of 2026 |

| Upside surprise | Core at +0.4% or above MoM | Hawkish bloc validated; higher odds of a 25-basis-point hike by late 2026 |

| Downside surprise | Core at +0.1% MoM with YoY clearly declining | Dovish bloc gains influence; cuts return as a longer-term possibility pending further data |

The baseline is the scenario most forecasters expect. A soft headline eases immediate hike fears, but core running near 2.9% keeps the Fed on hold rather than prompting a turn. An upside surprise in core would reinforce the hawkish nine and likely push explicit hike language into Warsh’s testimony that same morning. A downside surprise would be the first genuinely convincing sign that underlying inflation pressure is receding, though even then, the Fed would want several consecutive soft prints before committing to cuts.

Pre-mapping these paths means you interpret the number against a framework, rather than reacting to a single data point in either direction.

Several structural forces are working in favour of lower inflation. Together, they explain why the broad disinflation story has genuine legs, even if the pace has frustrated the Fed.

The 2026 FIFA World Cup is generating a short-lived, geographically concentrated upward pressure on core services prices. Elevated charges for accommodation, dining, and travel in tournament host cities are estimated to contribute around +0.03 percentage points to headline CPI and roughly +0.04 percentage points to core over the summer months, with the effect unwinding once the tournament concludes.

The combination of fading energy costs, moderating rents, and eventual tariff completion gives the disinflation trend real support. But the World Cup effect means June’s core print could read slightly hotter than the underlying trend warrants, which is a distinction worth keeping in mind before drawing conclusions from a single month’s data.

Warsh’s Congressional appearance on the same morning as the CPI release turns Tuesday into a dual event. The CPI gives investors the number; Warsh provides the interpretive filter that tells them how the Fed intends to weight it.

Under the baseline scenario of a soft headline and steady core, Warsh is likely to frame the data as progress that falls short of mission accomplished, stressing that core remains above target and that policy will stay data-dependent. Three scenarios for his tone and the corresponding market reactions:

Prior to the release, the DXY dollar index had been holding in the vicinity of its 100-week simple moving average while remaining above the March 2026 high of 100.43, a positioning that makes the currency particularly sensitive to any shift in Warsh’s tone.

For you, Warsh’s tone is often more market-moving than the CPI number itself, because it signals how the Fed intends to weight the data. On a split committee, the tone could shift meaningfully in either direction depending on the print.

Retail sales data for June drops two days later on 16 July 2026 (headline +0.3%, ex-autos 0.0%, control group +0.5%), which will either reinforce or complicate the soft-landing narrative that Tuesday’s CPI begins to shape.

A baseline soft headline will reduce near-term hike fears. It will not trigger cuts. It will not resolve the committee’s 9-9 internal division. And it will not, on its own, change the most probable rate path: an extended plateau around 3.50-3.75%, with a single hike later in 2026 conditional on core re-acceleration or a stall in disinflation.

Meaningful rate cuts would require several consecutive months of core clearly trending toward 2%, with temporary World Cup and tariff effects fully washed out. The forward indicators that matter most from here:

Retail sales land on 16 July, and the control group figure of +0.5% consensus will serve as an early test of whether the soft-landing picture sketched by Tuesday’s CPI holds up under scrutiny from a second data point.

For investors wanting to extend their macro framework beyond Tuesday’s CPI, our full explainer on the June jobs report covers how the removal of Fed forward guidance makes payrolls more market-moving than usual and examines the World Cup hiring distortions that complicate the headline read.

The honest read for investors is that one CPI print rarely changes the rate trajectory in a divided-committee environment. Position for the plateau as the base case, and keep the hike scenario as a live tail risk.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements regarding Fed policy, inflation trajectories, and market outcomes are speculative and subject to change based on incoming data and economic developments.

Core CPI excludes food and energy prices from its calculation because those categories are highly volatile and can swing dramatically on supply disruptions without reflecting broader economic conditions. The Fed focuses on core because it captures stickier components like services, shelter, and wages, which are harder to reverse once they accelerate.

The June 2026 consensus expects headline CPI to fall 0.1% month-on-month, bringing the year-on-year rate toward 3.8-3.9%, driven largely by falling petrol prices. Core CPI is forecast to come in at 0.2-0.3% month-on-month, leaving the year-on-year rate near 2.9%, essentially unchanged from a year earlier.

If core CPI prints at 0.4% or above month-on-month, the hawkish bloc of the 9-9 split FOMC committee would be validated, increasing the probability of a 25-basis-point rate hike before the end of 2026. Fed Chair Kevin Warsh, testifying before Congress the same morning, would likely introduce explicitly hawkish language in response.

The 2026 FIFA World Cup is pushing up accommodation, dining, and travel costs in host cities, estimated to add around 0.03 percentage points to headline CPI and 0.04 percentage points to core for the summer months. The effect is temporary and geographically concentrated, and it unwinds once the tournament ends, meaning June's core print may read slightly hotter than the underlying inflation trend actually warrants.

A baseline soft headline will reduce near-term hike fears but will not trigger rate cuts or resolve the committee's 9-9 internal division. The most probable rate path remains an extended plateau around 3.50-3.75%, with a single hike later in 2026 conditional on core re-acceleration; meaningful cuts would require several consecutive months of core clearly trending toward 2%.