TSMC Posts Record US$39.6B Quarter Ahead of 16 July Earnings

45 mins ago

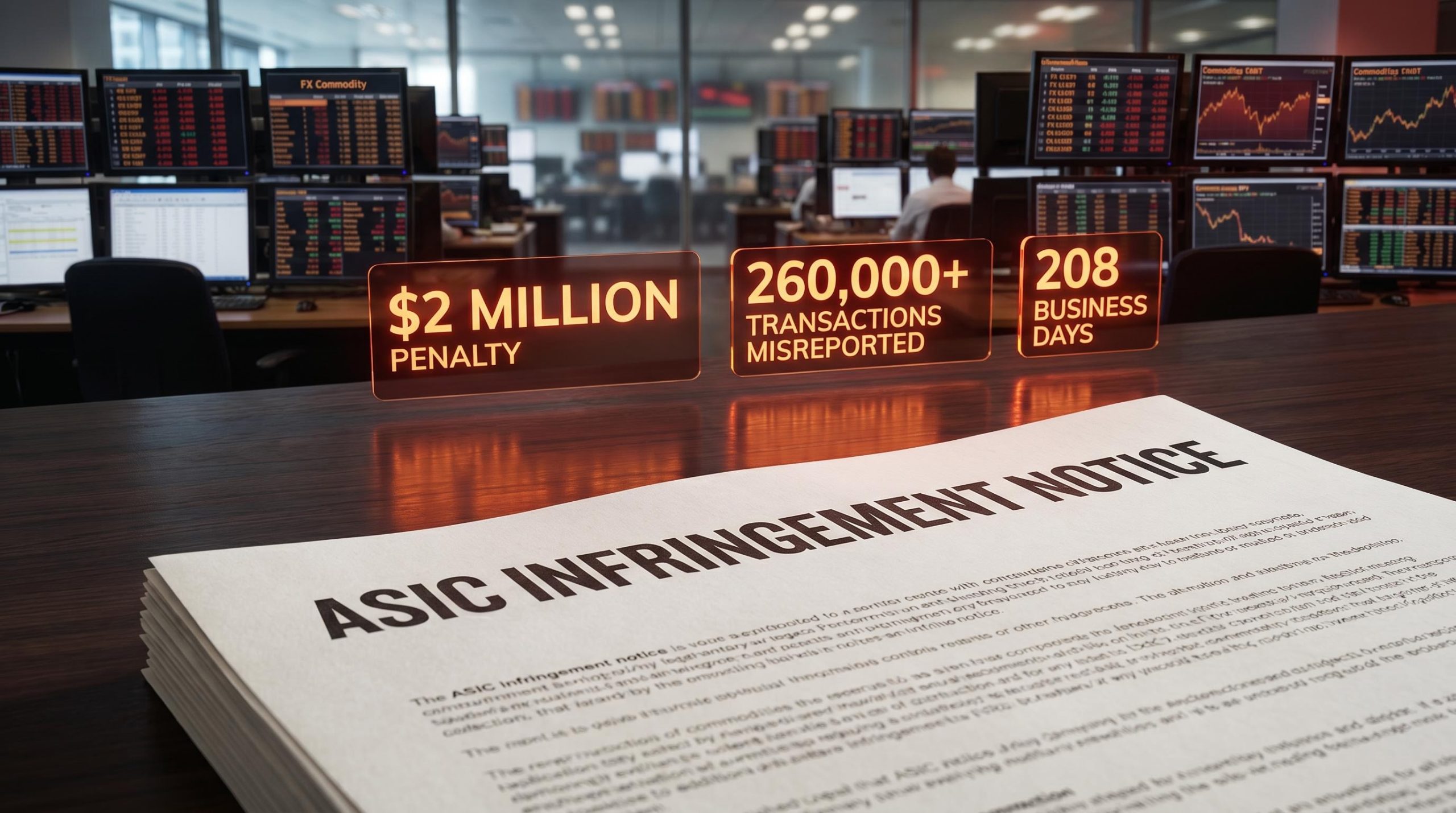

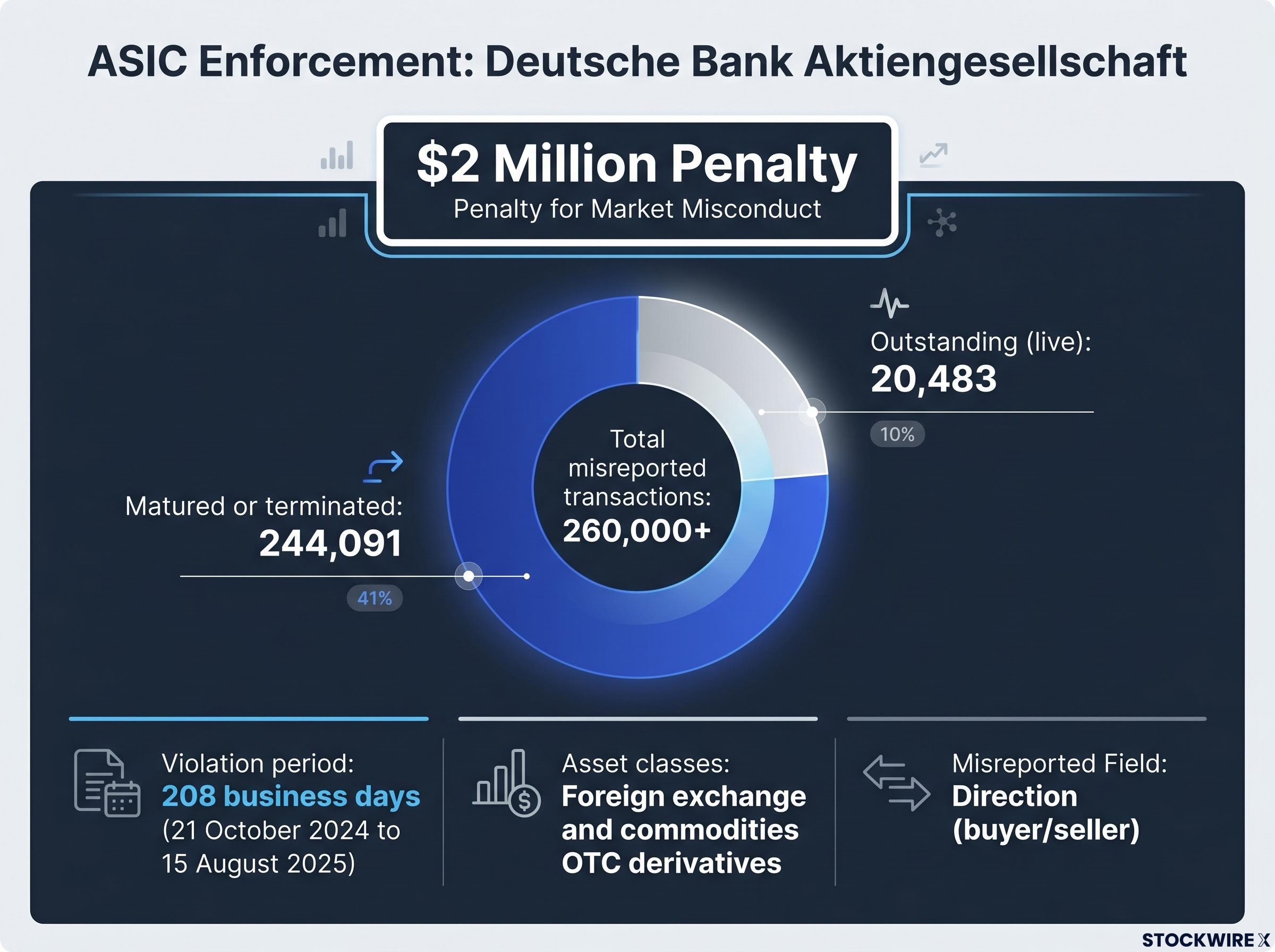

ASIC has issued a $2 million penalty against Deutsche Bank Aktiengesellschaft after the bank misreported in excess of 260,000 over-the-counter (OTC) derivative transactions spanning foreign exchange and commodities markets. The failures ran across 208 business days, from 21 October 2024 to 15 August 2025, making this one of the more significant data quality enforcement actions under the current reporting regime.

The regulator identified the errors as systemic, not incidental. These were not a handful of miskeyed entries caught in a routine audit. ASIC concluded that inaccurate mandatory data fields persisted across hundreds of thousands of transactions for close to a year, pointing to structural weaknesses in Deutsche Bank’s reporting framework rather than one-off mistakes.

Here is what the action reveals about ASIC’s current expectations: what specifically went wrong, why the regulator treated it as seriously as it did, and what this signals for every Australian market participant operating under the ASIC Derivative Transaction Rules (Reporting) 2024.

The penalty was issued under the ASIC Derivative Transaction Rules (Reporting) 2024, with the infringement notice announced on or around 13 July 2026. The transactions in question covered foreign exchange and commodities OTC derivatives, and the fields that were incorrectly populated were the mandatory “direction” indicators, the data elements that capture which side of a trade the reporting entity occupied, buyer or seller.

$2 million penalty. 208 business days of systemic misreporting.

The violation period ran from 21 October 2024 to 15 August 2025. One detail matters for how you read this outcome: settling an infringement notice by paying the penalty carries no formal acknowledgement of wrongdoing under the applicable regime. ASIC can impose a meaningful financial penalty and generate public accountability without requiring a court finding, which lowers the threshold for enforcement. For any firm managing derivative reporting obligations, that mechanism alone should elevate data quality from a secondary compliance concern to a primary one.

The total number of misreported OTC derivative transactions exceeded 260,000. Of that total, 244,091 had already been terminated or had reached maturity by the time ASIC identified the failures. A further 20,483 remained active, meaning they were live positions at the time of the finding.

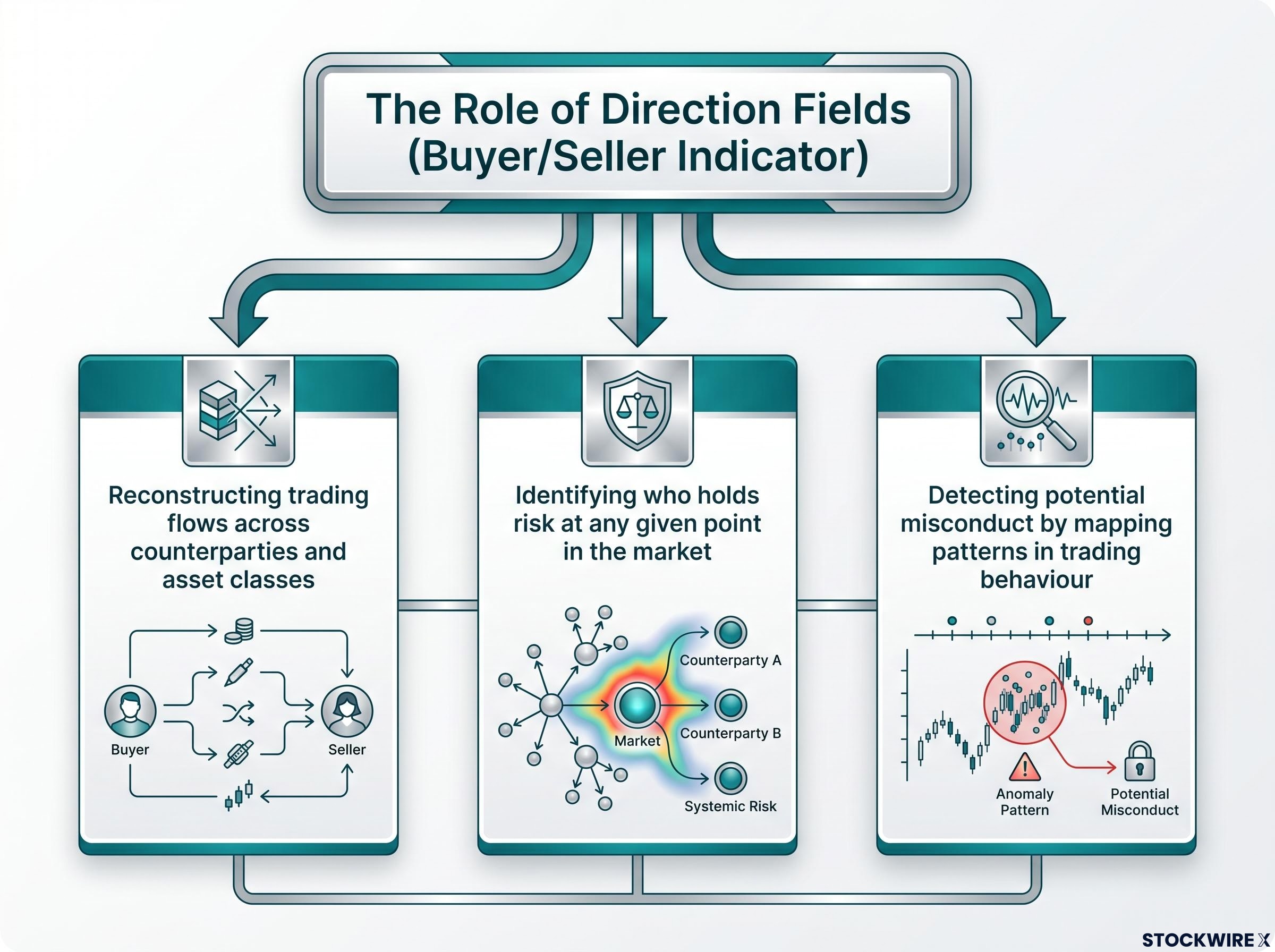

The misreported field, “direction,” is a key required data element under the 2024 rules. It serves a specific function:

That distinction is not administrative bookkeeping. It is the data regulators rely on to understand who holds risk in the market. When 20,483 live positions carried incorrect direction data, regulators were monitoring real market exposure using wrong information. That is the specific condition that elevates a reporting error from a record-keeping issue to a supervisory integrity problem.

| Item | Detail |

|---|---|

| Penalised entity | Deutsche Bank Aktiengesellschaft |

| Penalty amount | $2 million |

| Violation period | 21 October 2024 to 15 August 2025 (208 business days) |

| Total misreported transactions | 260,000+ |

| Matured or terminated | 244,091 |

| Outstanding (live) | 20,483 |

| Asset classes | Foreign exchange and commodities OTC derivatives |

| Field type misreported | Mandatory “direction” fields (buyer/seller indicator) |

In ASIC’s view, the failures were systemic in nature, attributable to underlying weaknesses in the bank’s broader reporting architecture rather than to individual errors.

OTC derivative markets are opaque by design. There is no centralised exchange displaying every trade. Regulators depend on reported data to see what is happening. Direction fields are one of the most important pieces of that picture because they answer a basic question: who is on which side of the trade?

That single data element supports three regulatory functions:

When direction data is inaccurate at the scale ASIC identified, the supervisory analytics and systemic risk assessments built on that data are materially distorted. Regulators cannot see the market clearly. For a compliance or risk professional at any Australian firm transacting OTC derivatives, that is why ASIC treats data quality as a substantive obligation rather than an administrative one.

ASIC’s 2026 ASX inquiry found that governance and risk management failures at the operator of Australia’s clearing and settlement system had been allowed to persist and compound over multiple years, a pattern that regulators have since made explicit they will not tolerate across any class of licensed market infrastructure participant.

The ASIC Derivative Transaction Rules (Reporting) 2024 introduced more granular and standardised data requirements compared to earlier frameworks. The approach is influenced by international standards set by the Committee on Payments and Market Infrastructures and the International Organization of Securities Commissions (CPMI-IOSCO). The direction field requirements reflect a global push toward data quality as a regulatory priority, not a local idiosyncrasy.

The CPMI-IOSCO guidance on OTC derivatives data harmonisation establishes the global framework for standardising critical data elements, including directional indicators, that national regulators like ASIC have embedded into their domestic reporting rules, making the 2024 Australian requirements part of a coordinated international data quality push rather than a unilateral national standard.

Deutsche Bank engaged constructively with ASIC throughout the investigation, settled the infringement notice, and is now putting in place remediation steps aimed at preventing further inaccuracies in its reporting systems. The bank is a global financial services group with operations in 55 countries, spanning investment banking, corporate banking, retail banking, and asset and wealth management. The entity penalised is the parent, Deutsche Bank Aktiengesellschaft.

Paying an infringement notice does not amount to an admission of guilt or liability, and the bank is not thereby treated as having contravened the ASIC Rules.

That legal distinction matters. It means there has been no court determination that Deutsche Bank breached the rules. However, public payment of an infringement notice still signals regulatory concern about a firm’s systems and governance. For compliance professionals assessing how their own firms would be expected to respond to a similar finding, the pattern here is straightforward: cooperate, pay, remediate, and accept that the public record will speak for itself regardless of the formal legal position.

The Deutsche Bank case converts a firm-specific penalty into a market-wide compliance signal. Four implications stand out, ordered by how directly they affect a compliance professional’s immediate priorities:

The Petra Capital case established that reporting system failures caused by a software update, rather than deliberate misconduct, still attracted formal penalty action from ASIC, confirming that the careless classification is sufficient to constitute a breach when firms fail to take reasonable precautionary steps.

ASIC’s approach reflects a global regulatory trend: treating systemic reporting weaknesses as serious compliance failures rather than technical errors. The 2024 rules framework has removed the ambiguity that may have previously allowed firms to treat reporting architecture as a lower-priority concern.

The $2 million penalty and the 260,000-transaction scale together define a concrete data point about ASIC’s current enforcement threshold. Systemic data quality failures under the 2024 rules will attract formal penalty action. The ambiguity is gone.

For compliance professionals at any Australian firm operating in OTC derivative markets, the relevant question is not whether their firm has had similar failures. It is whether they would know if it did.

For readers wanting to understand the wider pattern, our dedicated guide to ASIC’s enforcement escalation across financial markets traces how the regulator has moved from guidance to formal court penalties across asset classes, providing context for why the derivative reporting action against Deutsche Bank fits a broader institutional shift rather than representing an isolated case.

The Macquarie short sale reporting enforcement case, which produced a $35 million civil penalty following more than 14 years and up to 1.5 billion corrupted transactions, establishes the upper end of what systemic misreporting consequences can look like in Australian markets when failures are allowed to compound across a long horizon.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

ASIC issued a $2 million infringement notice against Deutsche Bank Aktiengesellschaft for misreporting more than 260,000 OTC derivative transactions across 208 business days from October 2024 to August 2025, with errors concentrated in mandatory direction fields that identify which party was the buyer and which was the seller.

Direction fields are mandatory data elements under the ASIC Derivative Transaction Rules (Reporting) 2024 that record which side of a trade each counterparty occupied; regulators use this data to reconstruct trading flows, identify who holds risk, and detect potential misconduct across opaque OTC markets.

No. Under the applicable regime, settling an infringement notice by paying the penalty carries no formal admission of guilt or liability, and Deutsche Bank is not treated as having contravened the ASIC Rules; however, the public record of payment still signals regulatory concern about the firm's systems and governance.

ASIC has made clear that submitting reports on time is not sufficient; the 2024 rules require the data itself to be accurate, and firms whose reporting infrastructure has not been updated to meet the more granular requirements now face heightened enforcement exposure for systemic accuracy failures.

Of the 260,000-plus misreported transactions, 244,091 had already matured or been terminated, while 20,483 were still live positions at the time of the finding, meaning regulators were monitoring active market exposure using inaccurate direction data.