Why AI Makes Markets Safer Daily but Riskier in a Crisis

34 mins ago

Two analyst calls landed in the same week targeting the same sector thesis from opposite directions. Bernstein stripped its Outperform rating from Salesforce and removed its price target entirely, while Stifel raised Shopify to Buy and lifted its target from $110 to $150.

The coincidence is not cosmetic. It reflects a structural fracture forming across enterprise software between AI as a story and AI as a measurable operating outcome. The week of 10 July 2026 produced a live experiment in how sophisticated institutional analysts are now separating AI winners from AI storylines, and both actions are grounded in the same bottom-up methodology: customer conversations, proprietary survey work, CIO budget data, and reported operating metrics.

That methodological overlap makes the divergence in conclusions significant. Here is a framework for reading AI monetisation claims across enterprise software, grounded in exactly the evidence that moved two experienced analysts in opposite directions in the same week.

Jackson Ader at Bernstein did not downgrade Salesforce on valuation or macro concerns. He downgraded it on evidence, or more precisely, on what the evidence failed to show. Bernstein’s prior rating was Outperform; the new rating is Sector Weight, a neutral equivalent, with the price target removed entirely. The action was announced during the week of 10 July 2026.

The Bernstein action sits on top of a pre-existing analyst split: a Salesforce valuation stress-test published in May 2026 found Morgan Stanley and Bank of America at Buy, JPMorgan at Neutral, and Bernstein already at Market Perform, reflecting unresolved uncertainty about whether Agentforce ARR and Data Cloud trajectory can sustain a premium multiple.

The analyst’s channel checks and customer conversations surfaced three distinct diagnostic issues:

CIO budget signal: The Bernstein CIO survey returned a result in which the proportion of chief information officers intending to cut Salesforce’s share of their IT budget over the coming 12 months exceeded the proportion planning to raise it. That is the most actionable data point in the downgrade.

When more buyers are planning to shrink a vendor’s wallet share than grow it, the AI narrative has not yet changed the purchasing decision. That gap between narrative and behaviour is precisely what Bernstein is pricing in. Understanding why a sophisticated analyst withdrew conviction matters more than the rating change itself; the methodology Ader used, tracking customer budget behaviour rather than accepting management guidance at face value, is a template for independent due diligence on any AI software name.

Salesforce responded to the evidence gap directly. Around May 2026, the company began publishing a set of Agentforce-specific metrics that are more concrete than anything previously available, and they deserve to be taken seriously as indicators of usage-level activity.

| Metric | Value |

|---|---|

| Agentforce ARR | ~$1.2B |

| Combined AI and data ARR (Agentforce + Data Cloud + related products incl. Informatica Cloud) | $3.4B |

| Tokens processed | ~28.6 trillion |

| Cumulative Agentic Work Units delivered | 3.8 billion (strong QoQ growth) |

These are real numbers. $1.2 billion in Agentforce annual recurring revenue (ARR), meaning the annualised value of active, recurring subscriptions, is not trivial. 3.8 billion Agentic Work Units, each representing a discrete task completed by an AI agent, signals genuine platform activity.

The unresolved question is whether those metrics change the financial trajectory that matters at the consolidated level. For a company of Salesforce’s total revenue base, the key question is whether that $1.2B in Agentforce ARR is displacing existing internal budget or expanding it, and whether its growth rate is fast enough to move the needle on consolidated revenue and margin. That is the analytical gap the market has not yet closed, and it is why the share price has not re-rated on these disclosures.

Start with the operating numbers. In Q1 2026, Shopify recorded gross merchandise volume (GMV), the total dollar value of orders processed through its platform, of $101 billion, a 35% year-over-year increase at a time when the broader U.S. e-commerce market expanded by just 9.8%. That is not a rising-tide story. It is documented share capture across multiple segments simultaneously.

The U.S. Census Bureau e-commerce estimates for Q1 2026 place overall U.S. retail e-commerce growth at 9.8% year over year, the official benchmark against which Shopify’s 35% GMV expansion represents a share-capture differential that is not easily explained by macro tailwinds.

| Segment | Q1 2026 Growth Rate | Context |

|---|---|---|

| Total GMV | 35% YoY | vs. 9.8% U.S. e-commerce growth |

| B2B GMV | 80% YoY | New segment expansion |

| International GMV | 45% YoY | Geographic diversification |

| Enterprise merchants (>$100M GMV) | ~Doubled over 2 years | Upmarket migration |

Analyst J. Parker Lane at Stifel raised Shopify to Buy and lifted the price target to $150 from $110 during the week of 10 July 2026. The upgrade rests on this operating data, not on an AI feature announcement.

Stifel described Shopify as concurrently taking share across legacy platform migration, enterprise customers, B2B, international expansion, and payments, a simultaneous advance across that many fronts being unusual among software platforms operating at comparable scale.

The geographic concentration reframe is important. Shopify generated 63% of its 2025 revenue from the U.S. market, despite the U.S. representing roughly 40% of global e-commerce activity outside China, suggesting a substantial untapped international opportunity. Stifel reads that gap not as concentration risk but as evidence of a latent international growth runway.

The agentic commerce framing enters as the forward thesis layer, not the foundation. Shopify’s AI is embedded at the transactional layer of commerce: inventory, payments, logistics, and customer interactions. Its impact registers directly in GMV and merchant behaviour rather than as a separately sold product line requiring additional customer spend. Based on its survey work and industry conversations, Stifel sees a credible path to revenue growth exceeding 30% in 2026 and continuing at mid-20s percentage rates thereafter; the timing of the upgrade also reflects an improved risk-reward profile following a year-to-date decline in the share price.

A 35% GMV growth rate against a 9.8% market benchmark is the kind of compounding mechanism that justifies a durability premium, and it is already visible in the reported numbers.

What the Bernstein downgrade and the Stifel upgrade share is a methodological foundation that investors can apply across any enterprise software position carrying an AI premium. Two tests emerge directly from the evidence.

Enterprise AI pilot failure rates, estimated at 70-80% across the industry with poor data integration as the primary cause, provide the structural backdrop for why Bernstein’s data readiness finding at Salesforce is not an isolated customer-specific problem but a sector-wide bottleneck that vendors cannot resolve through product investment alone.

The data readiness constraint surfaced in Bernstein’s channel checks is not a temporary integration delay. It is a structural dependency. Agentforce requires unified, trusted internal data to function reliably, and many enterprises have not achieved that state.

Salesforce’s own messaging acknowledges this explicitly, positioning Data Cloud as the prerequisite layer and warning against what it calls “automation theatre,” the deployment of AI agents that perform tasks without reliable data inputs and produce unreliable outputs.

“Automation theatre” is Salesforce’s own framing for AI deployments that lack the trusted data foundation to deliver reliable results. The phrase captures the failure mode efficiently: activity without accuracy.

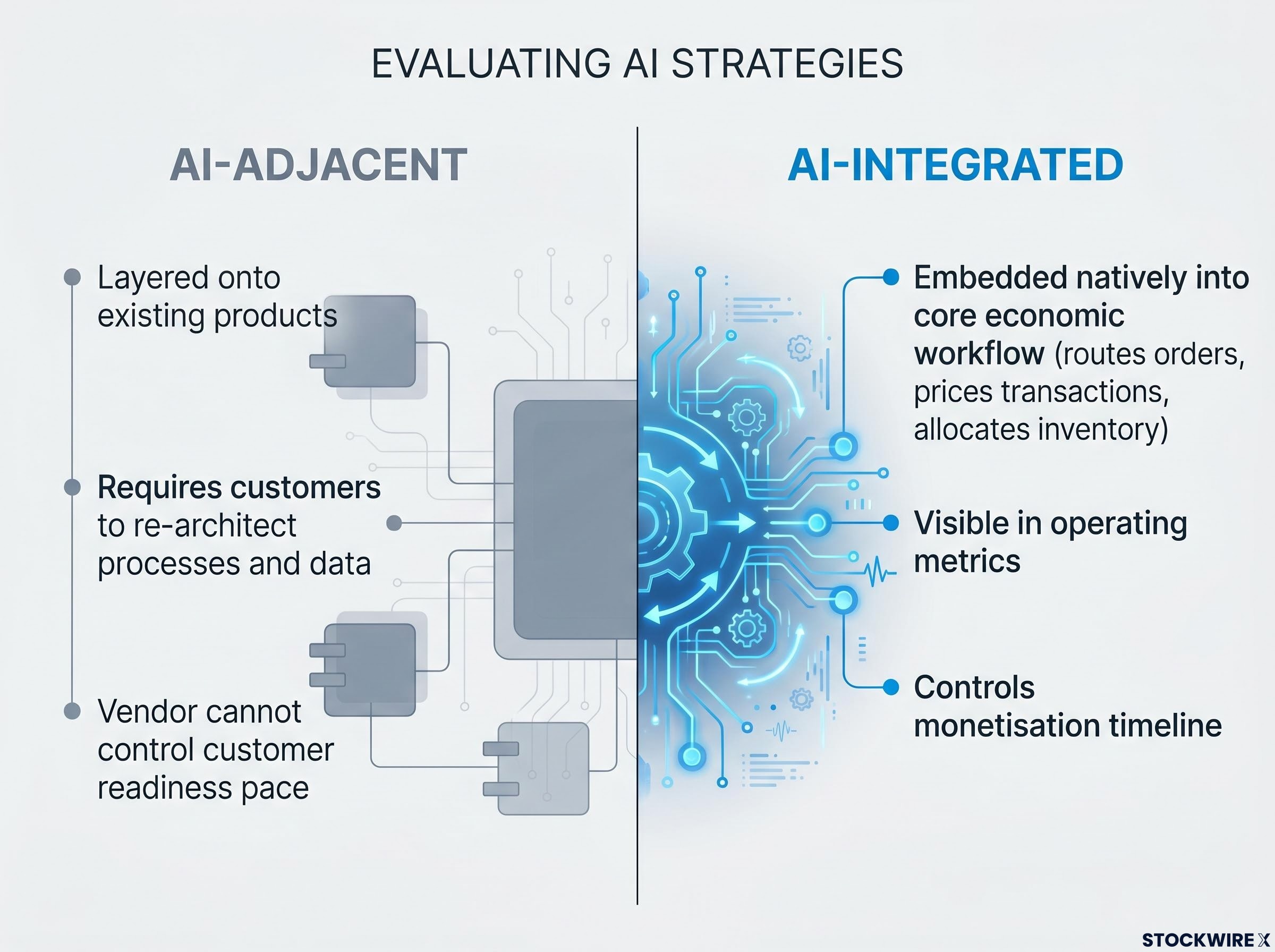

For you as an investor, the implication is direct: vendors whose AI value proposition is gated on customer data maturity inherit a timeline they cannot fully accelerate through product investment alone. Whether a company’s AI story passes the integration test or the adjacent test is the single most practically useful question you can ask before attributing a valuation premium to an AI growth thesis, because it determines whether the monetisation timeline is in the vendor’s control or the customer’s.

These two analyst actions are not anomalies. They are early markers of a directional shift in how enterprise software valuations are being calibrated for AI.

The premium that was previously granted on promise is now being conditioned on auditable, recurring, and diversified revenue streams. Bernstein’s conclusion was specific: agentic AI acceleration is further away than previously anticipated at the scale the valuation implied. That is a valuation recalibration, not a fundamental impairment thesis. Stifel’s upgrade contained a dual-lever structure: a fundamental thesis grounded in GMV and segment mix, plus a timing argument that the year-to-date share price decline improved risk-reward.

The broader SaaS pricing regime shift underway means the question of whether AI monetisation is adjacent or integrated also determines which pricing model is durable: per-seat structures that depend on human licence counts face compression from AI-native entrants benchmarking at $500,000-$700,000 in ARR per employee, a benchmark that reframes what healthy unit economics look like for the next generation of enterprise software.

The characteristics separating these two categories are becoming increasingly visible:

The cost of being wrong about AI monetisation timing is higher in software than in earlier technology cycles because software multiples are more sensitive to growth rate expectations than hardware or semiconductor names. The asymmetry is real.

The market is now imposing three questions on new AI software growth theses: where in the P&L does AI live, how does it change customer behaviour, and how quickly do those changes compound into durable growth?

These questions are not theoretical. They are the precise diagnostic Bernstein applied to Salesforce and that Stifel confirmed Shopify passes on the current evidence. For you, reviewing a software portfolio today, the right question is not whether each holding has an AI strategy (essentially all of them do) but whether that strategy has yet produced any signal in the operating metrics that are already being reported, because that distinction is now where multiple premium or discount is being assigned.

The core distinction this analysis has built is between thesis quality (is the AI story structurally sound?) and near-term valuation appropriateness (is that story priced correctly for what the evidence currently supports?). These are two questions that must be answered separately.

The Salesforce downgrade does not close the Agentforce story. It resets the evidence bar. If Agentforce ARR continues to scale beyond $1.2 billion and begins to show up in consolidated growth acceleration, the bull case reopens. Stifel’s projection of mid-20s percentage revenue growth for Shopify continuing past 2026 is the kind of forward-looking metric that reflects demonstrated rather than promised AI integration.

The specific metrics to monitor across any enterprise software position carrying an AI premium are already published each quarter:

The analytical discipline is simply applying the same evidentiary standard to AI claims that you would apply to any other growth thesis. Investors who internalise the distinction between thesis quality and current valuation appropriateness are positioned to hold AI software names with more confidence when the evidence supports it, and to demand recalibration when it does not, without being whipsawed by every headline analyst action.

For investors wanting to extend this evidentiary framework beyond the software tier, our deep-dive into AI ecosystem switching costs examines why the durable variable across hardware and software positions is ecosystem ownership, not product category, with a four-step diagnostic covering stack layer, moat durability, and token deflation stress-testing.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

AI monetization in enterprise software refers to the measurable revenue and operating impact generated by AI products, tracked through metrics like AI-specific ARR, GMV growth, and CIO budget share allocation rather than through product announcements or management guidance alone.

Bernstein downgraded Salesforce to Sector Weight and removed its price target because channel checks and CIO survey data showed more buyers planning to cut Salesforce's IT budget share than grow it, while customer conversations surfaced data readiness constraints and product maturity concerns that Agentforce's financial disclosures did not corroborate.

AI-adjacent strategies layer AI onto existing products as add-ons, making monetization dependent on customers first restructuring their data environments; AI-integrated strategies embed AI natively into core economic workflows, meaning their impact registers directly in reported operating metrics like GMV or transaction volume without requiring additional customer spend.

Stifel pointed to Shopify's Q1 2026 GMV of $101 billion, a 35% year-over-year increase against a 9.8% broader U.S. e-commerce growth rate, alongside 80% B2B GMV growth, 45% international GMV growth, and a near-doubling of enterprise merchants over two years.

The two most reliable signals are CIO budget share direction (whether buyers are allocating more wallet share to the vendor, not just expressing positive AI sentiment) and whether AI-driven activity is visible in consolidated financial results such as revenue growth acceleration, GMV, or identifiable AI segment revenue, rather than only in supplementary disclosures.