Intel Has Quadrupled: Does the Bull Case Still Hold?

54 mins ago

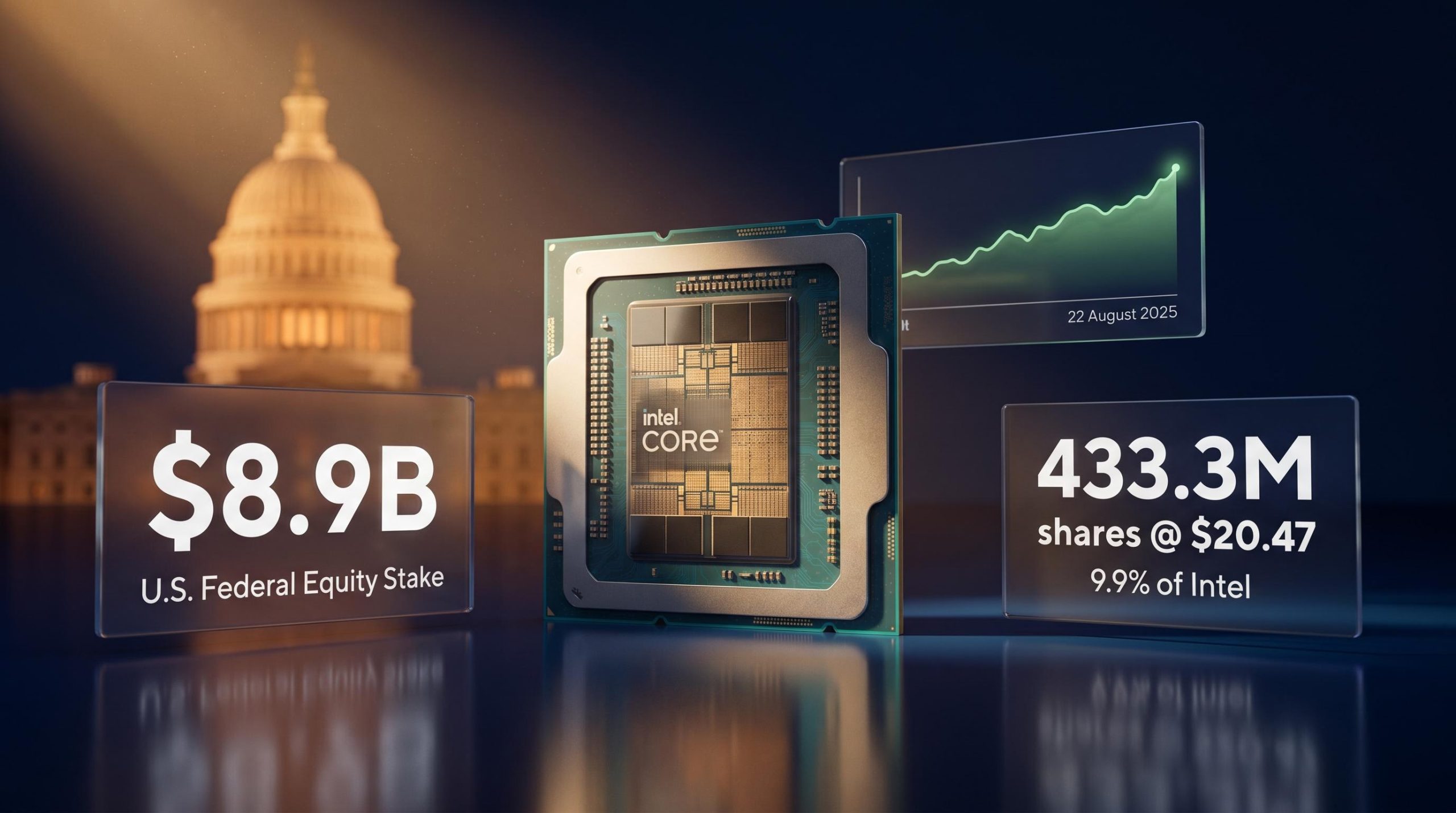

The United States federal government is now Intel’s single largest shareholder. Not because Intel was collapsing, not because a financial crisis forced Washington’s hand, but because the administration decided, deliberately, to convert $8.9 billion in unspent federal funds into 433.3 million shares of a publicly traded semiconductor company.

That fact alone is strange enough to sit with for a moment. The last time Washington held equity stakes of this size in American corporations, General Motors was weeks from bankruptcy and the global financial system was in freefall. Intel is not failing. It is struggling competitively, but it is solvent, operational, and listed on the Nasdaq.

What makes this analytically significant is not just the equity position. It is the combination: a direct financial stake in Intel’s stock price, paired with an active campaign in which administration officials personally lobbied Apple, Nvidia, and SpaceX to become Intel customers. The government is simultaneously investor and deal broker. Here is what that means for anyone tracking semiconductor stocks, industrial policy, or the increasingly blurred line between Washington and Wall Street.

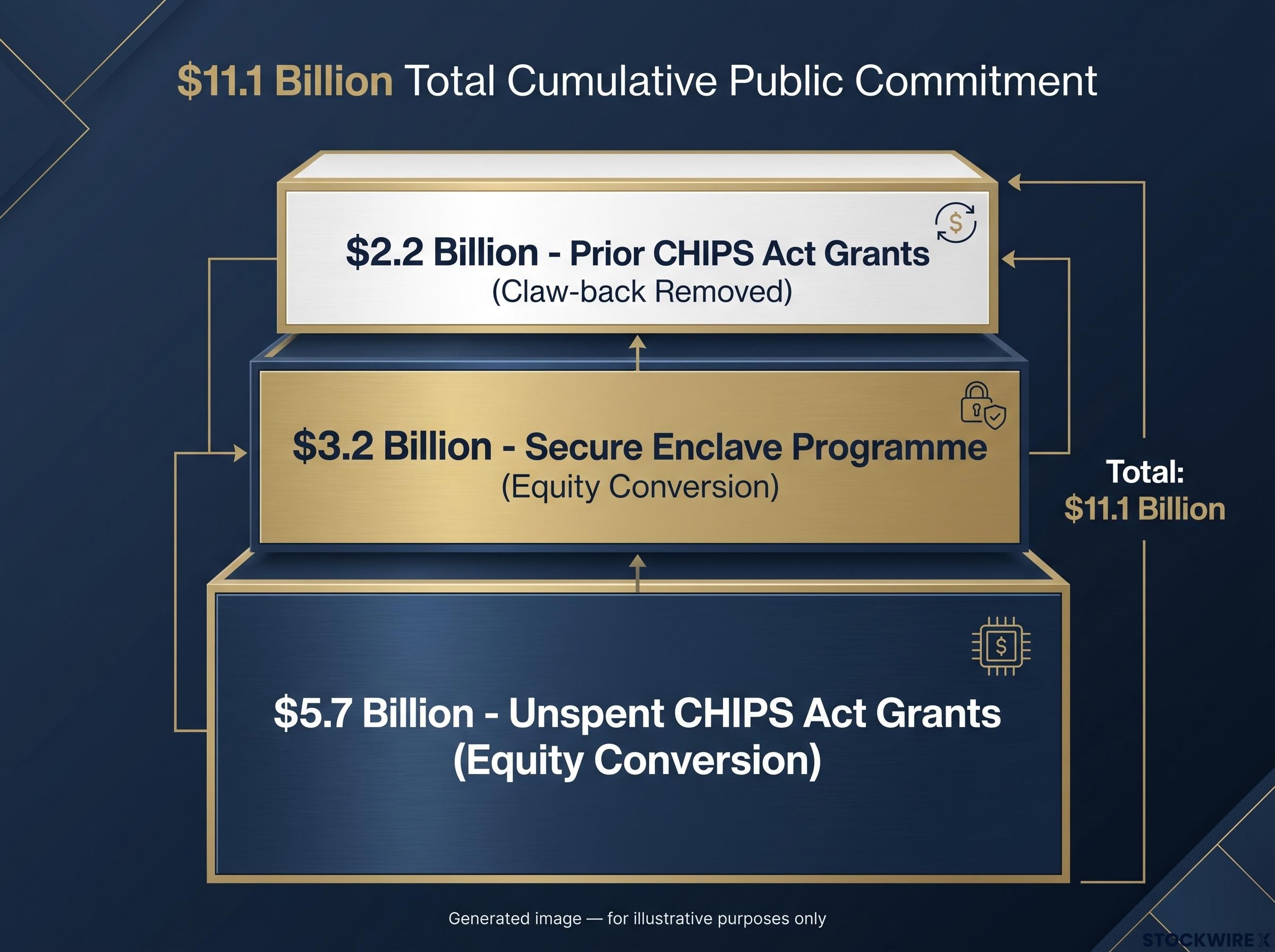

The funding came from two sources. $5.7 billion in unspent CHIPS Act grants previously earmarked for Intel was redirected from its original subsidy structure into a direct share purchase. A further $3.2 billion from the Secure Enclave programme, a separate federal initiative focused on secure chip production, was folded in alongside it.

The government bought 433.3 million primary shares at $20.47 per share, acquiring approximately 9.9% of Intel’s outstanding common stock. The deal was announced on 22 August 2025.

Intel’s August 2025 8-K filing with the SEC formally documents the Warrant and Common Stock Agreement with the Department of Commerce, confirming the conversion of $5.695 billion in CHIPS Act disbursements and $3.174 billion from the Secure Enclave programme into common stock, along with the removal of prior project milestone requirements.

What “redirected” means here is worth understanding precisely. The government did not claw back money already paid to Intel. It took grant allocations that had been approved but not yet disbursed and converted them into equity. The distinction matters: instead of conditional subsidies with performance requirements attached, the government now holds a direct financial stake whose value rises and falls with Intel’s share price.

Intel had already received $2.2 billion in prior CHIPS Act grants before this deal. As part of the new arrangement, the claw-back provisions on those earlier grants were eliminated, described in deal documentation as creating “permanency of capital.” Total cumulative public commitment now sits at $11.1 billion.

| Funding source | Amount | Mechanism |

|---|---|---|

| Unspent CHIPS Act grants | $5.7 billion | Grant-to-equity conversion (share purchase) |

| Secure Enclave programme | $3.2 billion | Grant-to-equity conversion (share purchase) |

| Prior CHIPS Act grants (already disbursed) | $2.2 billion | Prior disbursement; claw-back provisions removed |

“Permanency of capital” — the language used in Intel’s press release to describe the removal of claw-back provisions on the $2.2 billion in previously disbursed grants, converting conditional government support into unconditional commitment.

The shift from conditional grants to unconditional equity ownership is not administrative housekeeping. It means the government’s financial return now depends on Intel’s stock performing, which changes the political calculus around every future policy decision that touches Intel’s competitive environment.

Per Intel’s press release, the government’s 9.9% stake comes with no board representation, no special governance rights, no special information rights, and a voting arrangement aligned with Intel’s board of directors on matters requiring shareholder approval, subject to limited exceptions. The structure is passive by design.

That design creates a tension worth understanding. The government’s exposure to Intel operates across three distinct categories:

One unverified provision is worth noting with appropriate caution. Some reporting has described a five-year warrant allowing the government to acquire an additional 5% of Intel’s common shares at $20 per share, exercisable only if Intel ceases to own at least 51% of its foundry business. This specific feature has not been independently confirmed in primary deal documentation and should be treated as unverified.

Policy analysts interviewed by PBS and NPR flagged a structural conflict of interest: the same government that sets export controls, tariffs, and defence procurement rules now holds a large financial position in Intel. Even without formal governance rights, that overlap creates real second-order risk.

The absence of formal governance rights does not reduce the government’s practical influence. It simply means that influence operates through policy levers, tariffs, export controls, procurement decisions, rather than boardroom votes. For investors accustomed to analysing government stakes through a governance lens, this requires a different analytical frame. The risk sits in the policy channel, not the shareholder one.

According to the Wall Street Journal, President Trump and Commerce Secretary Howard Lutnick engaged directly with Apple CEO Tim Cook, pressing him to route chip production through Intel’s fabrication facilities during talks concerning proposed tariffs on semiconductor imports. Apple subsequently secured a tariff exemption on semiconductor imports, and the Wall Street Journal, citing a person familiar with the negotiations, reported that Apple is now expected to have Intel manufacture chips for certain Mac and iPhone product lines.

The precise mechanism matters here. The Apple-Intel foundry engagement is documented. The specific question of whether tariffs were used as explicit contractual leverage to steer Apple toward Intel fabrication is interpretive analysis built on partial reporting rather than fully disclosed contractual terms. What is confirmed is that the lobbying happened, the tariff exemption was granted, and Apple is expected to use Intel’s foundry services.

The Apple-Intel foundry agreement, confirmed by the president rather than through standard investor relations channels, covers entry-level silicon on Intel’s 18A process node with volume production targeted for 2027, while TSMC retains Apple’s flagship chip production, a split that defines the commercial ceiling of the arrangement.

For investors tracking Intel Foundry Services, the Apple arrangement is not just a customer win. It is a government-brokered demand signal that would not have materialised through ordinary commercial competition, and that distinction matters when forecasting foundry revenue sustainability.

Administration officials also promoted Intel partnership opportunities to two other companies:

Reporting by the Wall Street Journal indicated that administration officials actively encouraged both Nvidia and SpaceX to pursue Intel partnerships, using tools such as defence contracting, launch licences, and broader regulatory leverage to encourage domestic sourcing. What remains undocumented is whether those conversations produced formal agreements, specific mandates, or binding commitments. The strategic logic is coherent for both companies. The absence of public deal specifics does not mean nothing is happening; it means investors are working with partial information, which is itself a material fact about the risk profile.

The administration has publicly cited paper gains on the Intel position as evidence that “America First” industrial strategy works. That public commitment to Intel’s stock performance creates what analysts have described as a de facto “policy put,” a term for an implicit price support that exists not because of any formal guarantee but because the political cost of visible stock price deterioration would be high.

The asymmetry is real without being a guarantee. Intel can still underperform if foundry execution falters, if the Apple arrangement delivers less revenue than expected, or if advanced process nodes remain uncompetitive with TSMC. No policy intervention eliminates commercial delivery risk. But the policy support is likely stronger and more persistent than for a comparable firm without a government equity overhang, at least during the current administration’s term.

The administration has claimed the government’s Intel stake has appreciated from approximately $11 billion to over $50 billion. These figures are cited in administration communications and market reporting but have not been independently confirmed.

What makes this intervention unusual is its proactive character. PBS and NPR both emphasise that Intel is not in crisis. This is not a GM-style rescue or a TARP-era emergency. Experts describe it as the government signalling that large federal grant programmes will now be expected to produce equity returns rather than simply catalyse private investment.

The second-order risks flagged by policy analysts are worth tracking:

The policy put is not a trading signal. It is a structural feature of the current environment that changes the probability distribution of Intel’s downside scenarios in ways that standard valuation models do not capture.

The equity stake and associated customer steering effectively designate Intel as Washington’s chosen national champion in advanced semiconductor fabrication. PBS explicitly noted the deal “raises vital questions” about how this partnership might influence other companies and market dynamics. Those questions have specific names attached.

TSMC’s Arizona operations were already strongly encouraged by Washington as a supply-chain security measure. The Intel stake and government-brokered customer steering now risk crowding out some of the commercial upside TSMC expected from its U.S. presence, even as the U.S. still relies on TSMC globally for the most advanced process nodes. TSMC is simultaneously a policy beneficiary and a potential commercial competitor to a government-backed rival.

For other domestic foundry players, the government’s clear designation of Intel as the primary partner may affect:

NPR framed the Intel stake as part of a broader contest with China and concern about advanced chip concentration in East Asia. The framework at work is what might be called directed industrial coordination: the government moving beyond tariffs and subsidies into active shaping of business-to-business relationships, with Intel at the centre.

Whether this model gets replicated depends substantially on Intel’s performance. If the turnaround sustains and stock appreciation holds, the political incentive to apply the equity co-investment model in other strategic sectors (batteries, rare earths, defence electronics, advanced materials) will be high. If Intel disappoints, the episode may become a cautionary tale about state equity stakes in competitive technology markets where commercial execution risk is real.

Either way, government as co-investor and deal intermediary is now a live variable in U.S. industrial policy, not a theoretical possibility. Investors in adjacent strategic industries should treat this as a structural feature of the current environment, not a one-off transaction.

CHIPS Act equity stakes in quantum computing companies followed an identical structural logic in May 2026, with the Department of Commerce taking minority positions in nine firms rather than issuing conventional grants, producing the same government-as-co-investor dynamic and triggering sector-wide repricing that included companies which received no funding at all.

The Intel stake combines three distinct departures from prior U.S. industrial policy: direct equity ownership at scale, active commercial lobbying of the government’s portfolio company’s potential customers, and political integration of a company’s stock performance into administration narratives. Each layer compounds the others.

What has changed structurally is that government as co-investor and deal intermediary is no longer theoretical. What has not changed is that Intel’s execution risk in foundry is still real, and no policy intervention eliminates the commercial delivery risk that ultimately determines whether the government’s bet pays off.

That leaves investors with a decision-point. Those who treat Intel as a normal equity story using standard peer comparisons are missing the policy layer entirely. Those who treat it as purely a policy story are ignoring the commercial execution risk that still determines long-term value. The analytical challenge is holding both simultaneously, because neither alone gives you an accurate read on what Intel is worth in a world where Washington is both shareholder and salesman.

For investors wanting to stress-test the commercial execution assumptions behind the policy narrative, our full explainer on BofA’s Intel upgrade thesis walks through the 2030 EPS modelling, the foundry revenue sizing, and the specific process-node assumptions that underpin the Street-high price target.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements about Intel’s commercial arrangements, stock performance, and government policy direction are subject to change based on market developments, policy shifts, and company performance.

The U.S. government converted $8.9 billion in unspent federal funds into 433.3 million Intel shares at $20.47 per share on 22 August 2025, acquiring approximately 9.9% of Intel's outstanding common stock. The funds came from $5.7 billion in redirected CHIPS Act grants and $3.2 billion from the Secure Enclave programme.

The federal government owns approximately 9.9% of Intel's outstanding common stock, making it Intel's single largest shareholder, with a total cumulative public commitment of $11.1 billion when prior disbursements are included.

No. The government's stake comes with no board representation, no special governance rights, and no special information rights; voting is aligned with Intel's board of directors on shareholder matters, making the position passive by design.

The policy put refers to an implicit price support created by the administration's political stake in Intel's stock performance: because officials have publicly cited paper gains as proof that 'America First' industrial strategy works, the political cost of visible stock price deterioration is high, making sustained policy support more likely than for a comparable firm without government ownership.

President Trump and Commerce Secretary Howard Lutnick lobbied Apple CEO Tim Cook to route chip production through Intel's fabrication facilities during tariff negotiations; Apple subsequently received a semiconductor tariff exemption and is expected to have Intel manufacture chips for certain Mac and iPhone lines, while administration officials also promoted Intel partnership opportunities to Nvidia and SpaceX.