On 21 May 2026, the Department of Commerce announced it would take direct equity ownership in nine quantum computing companies as part of a $2.013 billion initiative under the CHIPS and Science Act. The announcement triggered immediate, sector-wide repricing: quantum computing stocks posted double-digit single-day gains broadly across the category, including names that received no funding at all. Government equity stakes in private technology firms are historically rare outside crisis-era bailouts, and the structural novelty of this programme, proactive ownership in a frontier sector framed around national security and taxpayer upside, is precisely what investors need to understand before interpreting the price movements that followed. This article examines why the ownership structure matters, what is actually driving the stock gains, and how investors should think about positioning across the different tiers of quantum equity exposure.

Why the government is buying equity stakes in quantum computing companies, not just writing cheques

The $2.013 billion CHIPS quantum programme does not operate like a conventional grant. Each of the nine recipients is required to grant the U.S. government a minority, non-controlling equity stake as a condition of funding, a structure explicitly designed to “enhance the return for the U.S. taxpayer.”

Department of Commerce language: Equity stakes are structured to “enhance the return for the U.S. taxpayer,” creating ongoing financial alignment between the government and funded companies.

That distinction is not cosmetic. It changes the nature of the relationship between the state and the companies it backs. Three structural dimensions separate this programme from both standard grants and the crisis-era equity injections of 2008:

- Ownership interest: Grants confer no ownership. Crisis-era bailouts created equity positions the government intended to exit as rapidly as possible. CHIPS quantum stakes are designed for sustained participation.

- Duration of relationship: A grant is transactional; once disbursed, the financial relationship ends. An equity stake ties the government’s financial outcome to the company’s long-term trajectory.

- Government incentive alignment: Under a grant, the government has no direct financial stake in the company’s commercial success. Under equity, the government benefits when the company appreciates and loses when it does not.

The programme operates under the CHIPS and Science Act, which is congressionally authorised legislation. This is not a novel executive action or a unilateral policy experiment. The legislative foundation matters: it signals that the equity mechanism has institutional backing beyond a single administration’s priorities.

NIST’s official announcement of the quantum funding letters of intent confirms the Department of Commerce will receive a minority, non-controlling equity stake in each of the nine recipient companies, with the programme explicitly framed around returning financial value to U.S. taxpayers rather than functioning as a conventional subsidy.

When big ASX news breaks, our subscribers know first

The nine companies receiving funds, and what the allocations reveal about priorities

The allocation structure is not a diversified spread of equal bets. It is a deliberately tiered programme that reveals where the government sees foundational infrastructure and where it sees speculative frontier.

| Recipient | Proposed Amount | Strategic Role |

|---|---|---|

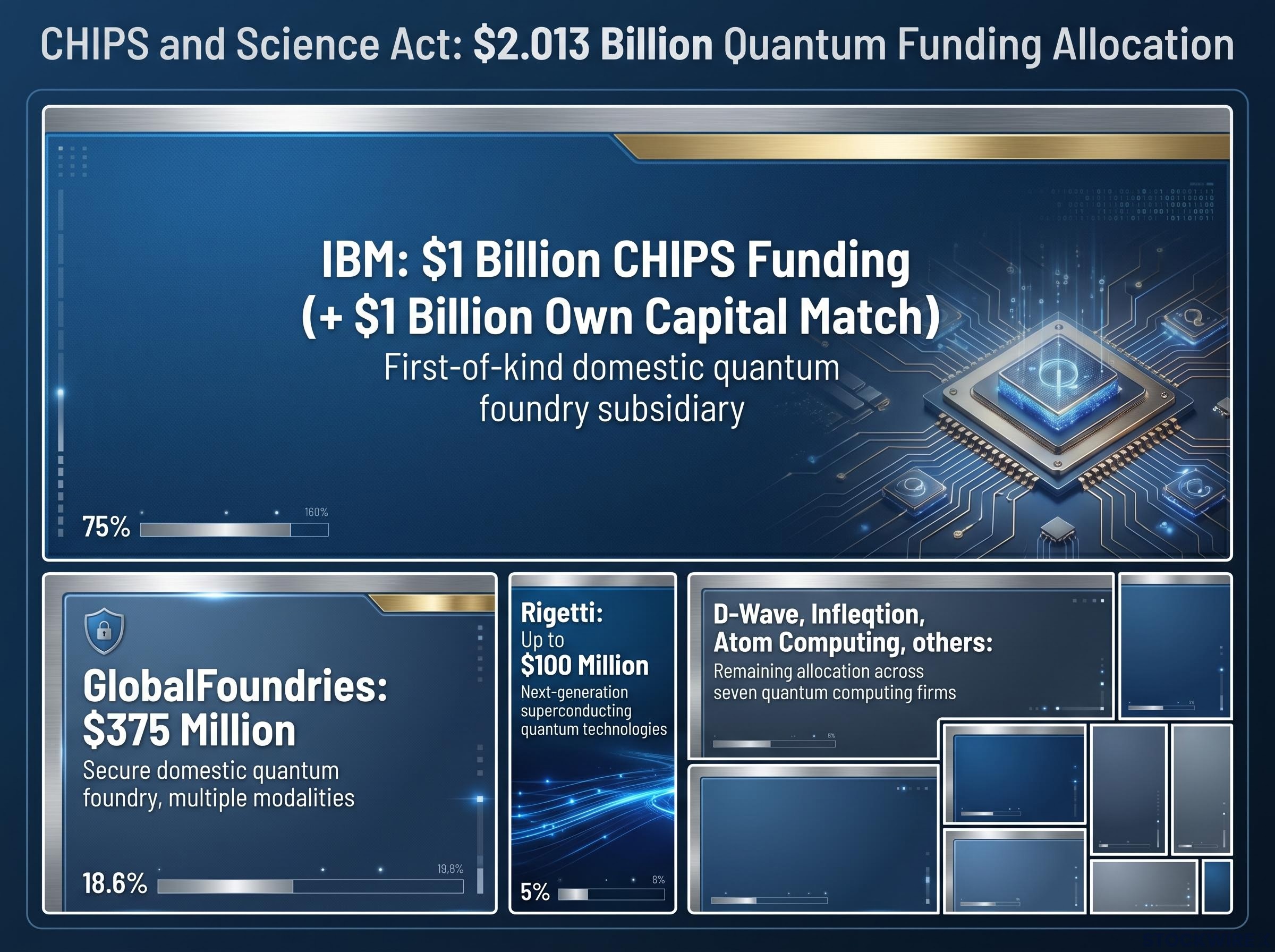

| IBM | $1 billion | First-of-kind domestic quantum foundry subsidiary |

| GlobalFoundries | $375 million | Secure domestic quantum foundry, multiple modalities |

| Rigetti | Up to $100 million | Next-generation superconducting quantum technologies |

| D-Wave, Infleqtion, Atom Computing, others | Remaining allocation across seven quantum computing firms | Various quantum development areas across competing modalities |

IBM alone accounts for nearly half the total programme. Its $1 billion in CHIPS funding is matched by $1 billion of IBM’s own capital, bringing the total quantum foundry investment to approximately $2 billion. That matching commitment signals internal conviction, not grant-seeking behaviour.

The five smaller recipients beyond Rigetti, D-Wave, Infleqtion, and Atom Computing have not all been fully identified in official materials. Rather than speculate, the allocation pattern itself tells the story: foundry infrastructure first, speculative modality bets second.

What “quantum foundry” means and why the supply chain framing matters

A quantum foundry produces the specialised hardware, such as quantum-grade superconducting wafers, that multiple quantum computing approaches depend on. It sits at the infrastructure layer, not the application layer. The government’s framing around domestic manufacturing and reduced foreign supplier dependence ties these investments directly to the broader U.S. national security and export control architecture. The funded foundries are designed to support superconducting, trapped ion, photonic, topological, and silicon spin modalities, meaning the supply chain investment is modality-agnostic even as the smaller allocations are not.

The foundry model is already being pursued outside the CHIPS programme: wafer-scale qubit manufacturing using semiconductor industry-standard processes is the approach Archer Materials is scaling toward its 2026 working qubit demonstration, a pathway that reduces capital intensity by routing production through existing foundry infrastructure rather than building bespoke fabrication capacity.

What the stock market reaction actually shows about how investors are reading the signal

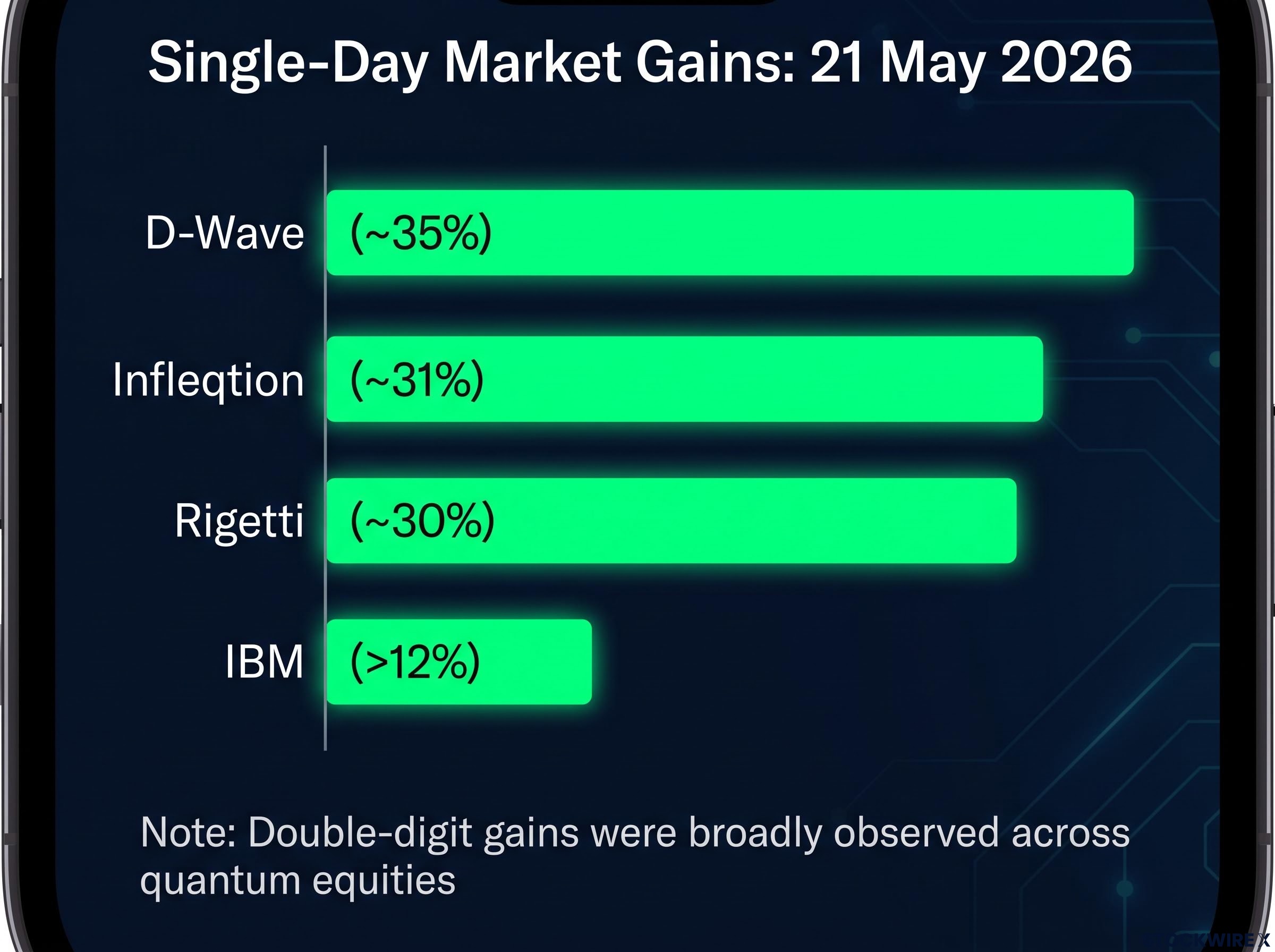

The headline numbers were striking. Reported single-day gains on 21 May included approximately 35% for D-Wave, approximately 31% for Infleqtion, approximately 30% for Rigetti, and more than 12% for IBM. Double-digit gains were broadly observed across quantum equities as a category.

Data confidence note: The specific percentage figures above are drawn from source reporting and should be treated as approximate rather than definitively sourced. The broader characterisation of double-digit gains across quantum names is confirmed in contemporaneous market reporting.

The analytically revealing detail, however, is not the funded names. It is the companies that rallied without receiving a single dollar of CHIPS funding. Their balance sheets did not change. Their technology roadmaps did not change. Their share prices moved anyway.

That pattern is consistent with a category or basket trade, where capital flows hit the entire theme rather than specific beneficiaries. Three distinct populations of movers were visible on the day:

- Direct funding recipients (IBM, Rigetti, D-Wave, Infleqtion, Atom Computing): price driven by direct capital access, government equity validation, and strategic endorsement.

- Sector adjacents (quantum-related firms without CHIPS funding): price driven by thematic association and inferred policy tailwinds for the broader sector.

- Thematic ETFs and momentum vehicles: price driven by algorithmic and screen-based rebalancing in response to the sector catalyst.

The distinction matters. For funded recipients, the price move reflects a genuine change in their capital structure and strategic positioning. For non-recipients, it reflects sentiment, and sentiment is reversible.

How government equity positions drive market sentiment: the copycat investor hypothesis and what it means for quantum price action

When a high-profile capital allocator discloses a new position, other investors often follow. The structural logic is straightforward: if an entity with superior information access or analytical resources is buying, the position itself becomes a signal.

The most established version of this pattern is the Buffett effect. When Berkshire Hathaway’s new positions become public through SEC filings, copycat buying has historically pushed prices higher in the days that follow. Berkshire has previously sought confidential treatment from the SEC to delay disclosure of new positions, precisely to prevent front-running during accumulation.

Three mechanisms that make government equity positions potentially market-moving

The government equity stakes in quantum computing companies carry a version of this dynamic, amplified by the political and strategic framing. Three mechanisms are analytically defensible:

- Perceived downside protection: Investors may infer greater political will to prevent catastrophic failure in a company where the government holds a direct equity stake. This is a behavioural inference about investor psychology, not a formal guarantee.

- Validation of strategic importance: Government selection implies a higher probability of future contracts, preferred procurement relationships, and favourable regulatory treatment.

- Momentum and category trading reflexivity: Once a catalyst re-rates a theme, capital flows hit the entire category. ETFs, momentum strategies, and thematic screens pile in regardless of whether any given name received direct funding.

A framework sometimes referred to informally as the “Trump effect” attempts to capture the dynamic where awareness of government or presidentially associated equity positions drives rapid share price appreciation. This is an emerging interpretive heuristic that some market participants appear to be applying, not an officially named or academically established phenomenon. The term does not appear in Department of Commerce language. It is useful as a working lens, not a settled law, and investors should apply it with appropriate scepticism.

What government ownership of quantum stocks actually changes for investors, and what it does not

The equity structure genuinely changes several things. It creates alignment of interests between the government and funded companies that extends beyond a single budget cycle. It signals a durability of policy commitment that a one-off grant cannot match. And government ownership may function as a de facto barrier to foreign acquisition, as any attempt to acquire a company with a U.S. government equity stake would face heightened scrutiny under the Committee on Foreign Investment in the United States (CFIUS) framework. That last point is an informed structural inference, not a stated Department of Commerce objective.

What changes:

- Alignment of financial interests between government and company

- Durable policy commitment beyond a single budget cycle

- Heightened CFIUS scrutiny as a likely barrier to foreign acquisition

- Companies retain operational independence (stakes are explicitly minority, non-controlling)

What does not change:

- Technology and engineering execution risk remain fully intact

- All nine letters of intent are proposed incentives subject to negotiation and final agreement

- The informational advantage of the announcement has already dissipated for liquid names

- Commercial readiness timelines for quantum computing have not compressed

Department of Commerce language: Funded work addresses “the most consequential, unresolved engineering problems in quantum computing.”

That phrasing is not boilerplate. It is a direct acknowledgement that these are frontier research and development efforts, not finished products. Investors who anchor to “government backing equals safety” are misreading the signal. Government backing here means strategic endorsement and supply chain commitment, not a guarantee against technology failure or valuation correction.

The gap between government enthusiasm and commercial arrival is visible in the application layer: quantum machine learning applications in finance, including fraud detection systems being benchmarked against 280,000 real bank transaction records, are still in the simulation and prototype phase, with full working systems targeted for late 2026 at the earliest.

Positioning across the quantum equity landscape: funded names, sector adjacents, and what each category demands

The quantum equity space now sorts into three distinct tiers, each demanding a different analytical standard.

| Category | Representative Names | Primary Driver | Key Risk | Analytical Standard |

|---|---|---|---|---|

| Policy-anchored large cap | IBM | Largest CHIPS recipient, $1B own-capital match, foundry mandate | Quantum remains a growth vector within a diversified business | Foundry infrastructure thesis |

| Funded high-beta | Rigetti, D-Wave, Infleqtion, Atom Computing | Government equity validation, direct capital access | Full technology and commercial timing risk; post-announcement pricing | Modality-specific technology thesis |

| Non-recipient sentiment beta | Other quantum-related equities | Thematic association, category trading | No fundamental change; vulnerable to sharp reversal | Independent fundamental thesis required |

IBM represents the most clearly documented policy-anchored quantum exposure: the largest single recipient, a meaningful own-capital match, a first-of-kind foundry mandate, and large-cap diversification across existing revenue streams.

The smaller funded names carry genuine government validation but remain high-risk investments dependent on both the commercial timing of quantum utility and the competitive viability of their specific technical approaches. Investors entering after the post-announcement repricing are buying at prices that already incorporate the policy signal.

Non-recipient quantum names appreciated on pure sentiment. Their balance sheets and technology roadmaps were not directly affected by the announcement. These positions are vulnerable to sharp reversal if enthusiasm cools or follow-on government actions concentrate resources on a narrower set of funded names. A separate, independent fundamental thesis is required to hold these names with conviction.

Investors exploring the technology risk dimension of quantum positions will find our deep-dive into competing quantum modalities and prototype timelines useful: it examines how room-temperature graphene-based qubit approaches, cryogenic superconducting systems, and ecosystem partnership structures each carry distinct risk profiles and commercial readiness horizons, with sensing applications potentially reaching commercial traction before general-purpose quantum computing.

What a $2 billion government equity stake in quantum tells us about the next phase of U.S. technology policy

The CHIPS quantum programme represents a deliberate expansion of the government’s industrial policy toolkit. The shift from procurement and subsidies to direct co-ownership in strategic technology sectors is a structural evolution, not a one-off. The CHIPS and Science Act provides the congressional authorisation, making this a replicable programme model rather than a unilateral experiment.

If equity stakes in quantum prove politically successful and financially defensible, the model is applicable to other frontier sectors. Plausible areas of extension include:

- Advanced semiconductor manufacturing beyond current CHIPS commitments

- AI infrastructure and domestic compute capacity

- Biotechnology and pharmaceutical supply chain resilience

- Clean energy and battery technology manufacturing

The broader policy architecture supports this reading. CFIUS scrutiny, export controls on quantum technology to China, and the domestic manufacturing resilience framing all point toward a government increasingly willing to use financial instruments, not just regulatory ones, to compete for technological leadership. The Department of Commerce has framed quantum as relevant to defence, materials science, finance, and energy systems.

The quantum sector sits inside the same export control architecture that governs semiconductors and AI hardware: AI chip export controls, Taiwan policy, and semiconductor supply chain restrictions were all left unresolved at the May 2026 US-China trade summit, meaning the competitive technology landscape that makes domestic quantum foundry capacity strategically valuable has not materially changed.

For investors, the structural signal is durable. The technology risk timeline is not. Quantum computing’s commercial readiness has not compressed because of a government equity stake, and investors who conflate government enthusiasm with commercial arrival will be running ahead of the fundamentals. The investor who understands the structural expansion of government industrial policy holds a longer-range analytical frame than the investor who reads only the 21 May headline.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. These statements regarding future government policy applications are speculative and subject to change based on market developments and legislative priorities.