What Chip Earnings and the Oil Spike Mean for Your Portfolio

46 mins ago

SK Hynix is raising nearly $29 billion in one of the largest technology listings in years. Its closest peers are falling apart. Samsung dropped 7% in a single session after flagging decelerating price increases. Micron, SanDisk, and Western Digital have each shed double-digit percentages in recent weeks. The juxtaposition is not coincidental; it is the same cycle producing both outcomes simultaneously.

The memory chip industry has a documented structural pattern. Demand shocks create supply bottlenecks, margins explode, capital floods in to build new capacity, and that capacity eventually crashes the pricing that justified the investment. The AI cycle has been the most powerful demand catalyst in a generation, and SK Hynix’s IPO, designed to fund a 60% capacity expansion by 2030, is itself the mechanism that has historically ended these booms.

Here is a framework for reading the late-cycle signals already visible in memory chip stocks and assessing how much risk is priced in versus still ahead. The data points are specific, the risk channels are named, and the analytical actions are concrete enough to apply this week.

DRAM, NAND, and HBM (high-bandwidth memory, the advanced chips powering AI server infrastructure) are largely commoditised products. Pricing is set by the balance of supply and demand, not by brand loyalty, switching costs, or proprietary intellectual property. That makes memory manufacturers structurally different from logic chipmakers (companies like NVIDIA or Broadcom that design unique architectures) or analog specialists (like Texas Instruments) that compete on design rather than volume.

The distinction matters because it determines how profits behave:

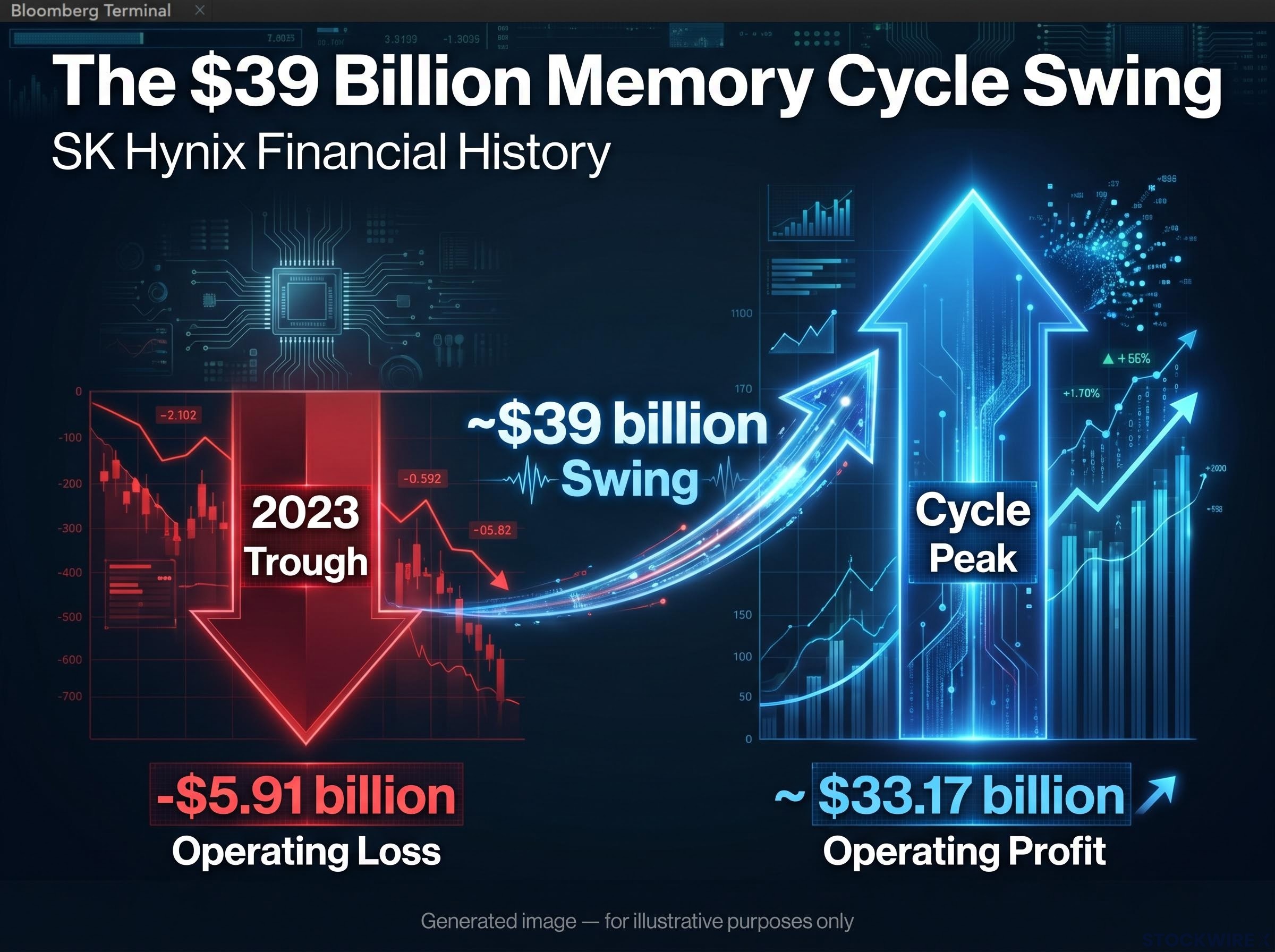

SK Hynix’s own financial history makes this concrete. In 2023, the company posted an operating loss of approximately $5.91 billion, according to PitchBook data as of 7 July 2026. Its peak annual operating profit reached approximately $33.17 billion.

That is a swing of nearly $39 billion from trough to peak across roughly two years, not because SK Hynix is an unusually volatile company, but because the memory industry’s structure produces these outcomes routinely.

If you hold memory chip stocks today, you are implicitly holding a position on where in that cycle the industry currently sits.

Generative AI and large language model infrastructure created the demand catalyst. Starting in earnest in 2024-2025, the buildout of AI server capacity produced acute supply bottlenecks for HBM and advanced DRAM, the memory types most critical to training and inference workloads. SK Hynix, as the leading HBM supplier, captured a disproportionate share of that demand surge.

HBM supply constraints operate on a fundamentally different timeline than capital investment: HBM inventory sits at just 3-4 weeks industry-wide, all three major producers are fully sold out through 2026, and demand grew 130% year-on-year in 2025 against a wafer start growth rate of only 6-8%, a structural rather than cyclical gap that explains why Google’s Sundar Pichai identified memory availability rather than capital as the binding AI infrastructure constraint.

The catalyst behind the memory chip stocks surge that preceded current valuations was itself a convergence of structural constraints: sold-out HBM capacity across SK Hynix and Micron through 2026-2027, a looming Samsung labour strike threatening to remove 3-4% of DRAM supply, and U.S.-China trade signals reducing the likelihood of Chinese producers filling the gap.

The numbers tell the story of what an AI-driven memory peak looks like. SK Hynix’s Q1 2026 results showed revenue of 52.5763 trillion won, up 198% year-over-year. Operating margin hit 72%. Net margin reached 77%. Its Korean-listed shares had gained close to 770% over the prior year before surrendering around 20% from their June 2026 highs, with the company’s market capitalisation surpassing $1 trillion.

| Metric | 2023 Trough | Q1 2026 Peak |

|---|---|---|

| Operating Profit/Loss | -$5.91 billion | ~$33.17 billion (annualised) |

| Operating Margin | Negative | 72% |

| Net Margin | Negative | 77% |

| Stock Performance | Cycle low | ~770% 12-month rally |

Nick Einhorn, director of research at Renaissance Capital, characterised revenue doubling since Q3 2025 as AI-driven peak-cycle conditions. Morningstar analyst Jing Jie Yu argued that investors are treating memory companies as if their strong profitability is both permanent and structurally anchored, a premise Morningstar rejects.

The memory supercycle thesis argues this upcycle is structurally different: hyperscaler capex projected at $725 billion in 2026, a supply vacuum that cannot be filled before 2027, and SK Hynix’s shift to foundry-style multi-year supply agreements through 2028-2030 are each cited as reasons the standard commodity-cycle playbook understates how durable current margins may prove.

A 72% operating margin in a commodity-pricing industry is a signal that supply is acutely constrained relative to demand. Historically, margins like these are the ceiling of the cycle, not a new normal. Micron’s recent earnings confirmed near-term demand remains strong, but that is consistent with late-cycle conditions where supply constraint is still resolving, not evidence that the constraint is permanent.

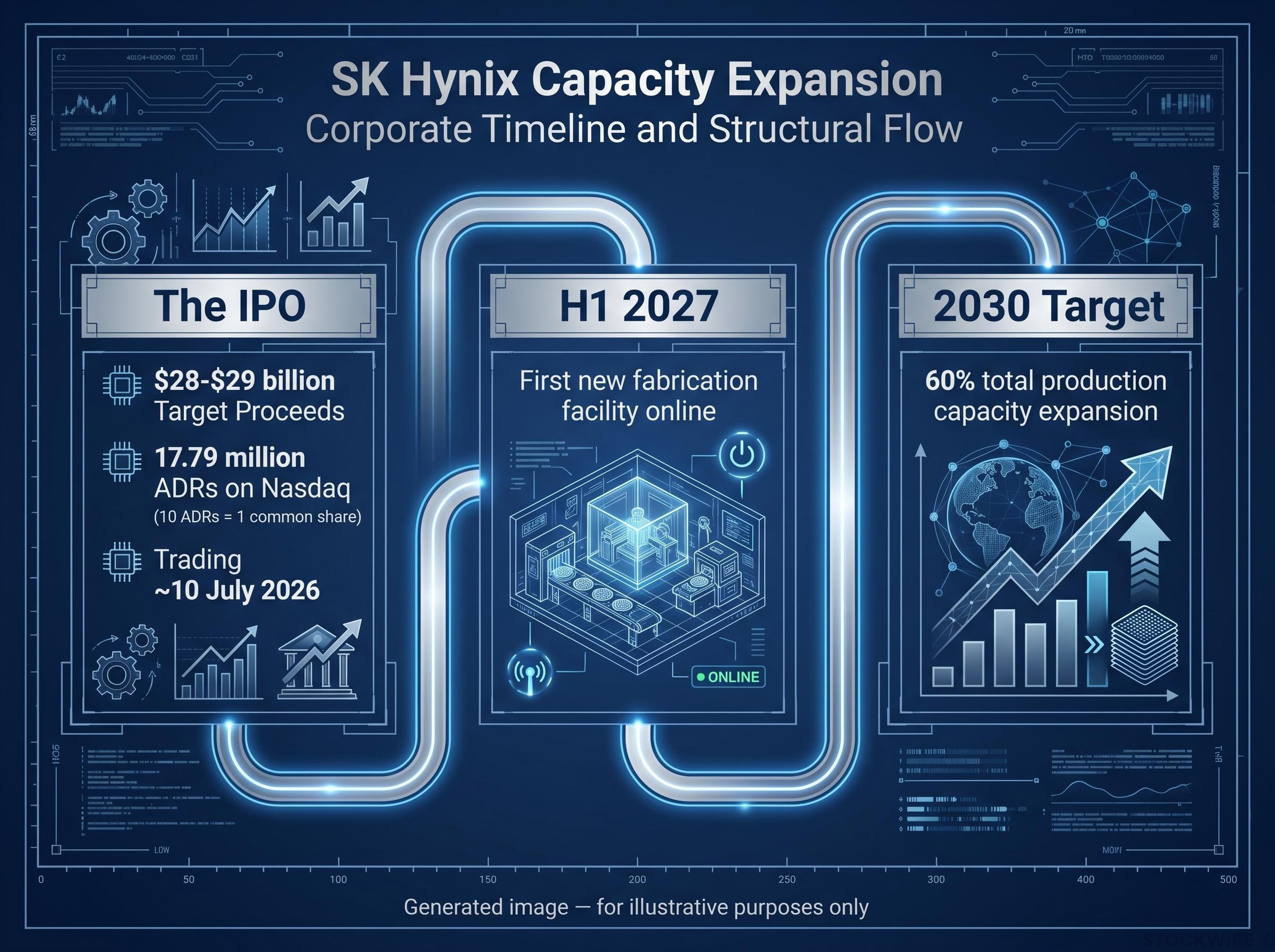

The IPO’s scale and explicit purpose are worth reading as a cyclical indicator, not just a corporate finance event. A commodity-like industry raising nearly $29 billion at peak margins, specifically to build capacity that will increase supply by 60% by 2030, is a late-cycle hallmark. It is the supply response that high prices incentivise, and it is the same mechanism that has ended previous memory upcycles.

The deal structure is straightforward: approximately 17.79 million ADRs (American Depositary Receipts, U.S.-listed securities that represent ownership in foreign shares) on Nasdaq, with 10 ADRs equalling one common share, targeting gross proceeds of $28-$29 billion. Trading is expected to commence around 10 July 2026. Morningstar analyst Jing Jie Yu has indicated that the raised capital will be directed toward expanding total production capacity by 60% before 2030, with the first of two fabrication facilities set to come online during the first half of 2027.

How the deal prices and trades is itself a real-time sentiment gauge. Three scenarios, and what each signals:

Bank of America has warned that speculation in high-multiple stocks has reached “extreme levels” and historically precedes a valuation “snapback.”

That warning matters here. According to Renaissance Capital’s Einhorn, the Renaissance IPO Index had advanced roughly 28% through the first half of 2026, outpacing the broader U.S. equity market’s gain of approximately 11% over the same period. The listing environment is rich. The question is whether institutional capital treats the SK Hynix IPO as confirmation that AI memory justifies these valuations, or as the moment it begins pricing for a permanent plateau that commodity economics will not deliver.

Samsung Electronics published its Q2 2026 preliminary results in early July 2026, which showed that price increases across its memory product range were losing momentum. The stock fell around 7% on the day and has since retreated roughly 18% from its peak in the prior month. The critical detail: this was not a collapse in prices. It was a slowdown in their rate of increase. The market’s reaction tells you how sensitively these stocks are priced to continued acceleration, and how little deterioration is required to trigger significant drawdowns.

The pattern extends beyond Samsung:

Steve Sosnick, chief strategist at Interactive Brokers, noted that a weak IPO result or further deterioration in memory stocks had the potential to send shockwaves through the wider market well beyond what a standard sector rotation would produce.

These are not isolated signals. They are the market’s early grading of the cycle thesis in real time. Investors who can read them before they fully develop have a positioning advantage over those waiting for quarterly earnings confirmation.

The risk is not simply that memory chip stocks might decline. It operates through four distinct mechanisms, and the dangerous scenario is all four operating simultaneously, which is precisely what happened during the 2023 trough.

The simultaneous compression of earnings and multiples, the Bank of America snapback scenario, is what produced the most severe peak-to-trough drawdowns in previous memory cycles. If you hold memory exposure, stress-test your position sizing against that combined scenario, not just one channel at a time.

None of these analytical moves requires forecasting the cycle turn precisely. They require building a position that survives the turn if it comes, which is a different and more achievable task than timing.

For investors wanting to apply a structured de-risking sequence across their semiconductor exposure, our dedicated guide to semiconductor cycle investing details a five-indicator framework and a graduated exit sequence that prioritises pure-play memory and thin-moat AI plays first, as the supply wave from locked-in 2026 capital budgets arrives across 2027-2029.

This is not a call to exit memory positions wholesale. It is a framework for holding them with appropriate cycle awareness and position sizing that accounts for the structural reality that $39 billion swings in a single company’s operating profit are not anomalies in this industry. They are the product.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Memory chip stocks are shares in companies like SK Hynix, Samsung, and Micron that manufacture DRAM, NAND, and HBM chips. Unlike logic chipmakers with pricing power and proprietary designs, memory manufacturers compete in a commodity-like market where profits are almost entirely driven by whether industry supply is above or below current demand, producing swings of tens of billions of dollars in operating profit within a single cycle.

Samsung dropped roughly 7% after its Q2 2026 preliminary results showed that price increases across its memory product range were losing momentum. The severity of the reaction reflects how sensitively memory chip stocks are priced to continued acceleration in pricing, not just positive absolute prices.

A commodity-like industry raising nearly $29 billion at peak margins specifically to expand production capacity by 60% before 2030 is a textbook late-cycle signal: high prices are incentivising the very supply response that historically ends memory upcycles, with the first new fabrication facility scheduled to come online in H1 2027.

The article recommends building models on normalised mid-cycle margins rather than peak figures, using SK Hynix's 2023 operating loss of $5.91 billion as the stress-test reference rather than its current 72% operating margin, and stress-testing valuation multiples against scenarios where earnings and price-to-earnings ratios fall simultaneously.

The Roundhill Memory ETF (ticker: DRAM), launched 2 April 2026, holds approximately 75% of its assets in SK Hynix, Samsung, and Micron, meaning redemptions or de-risking from the fund can amplify sell-offs in individual memory chip stocks well beyond what company fundamentals alone would produce.