Why Memory Chip Stocks Face a $39 Billion Cycle Reversal

22 mins ago

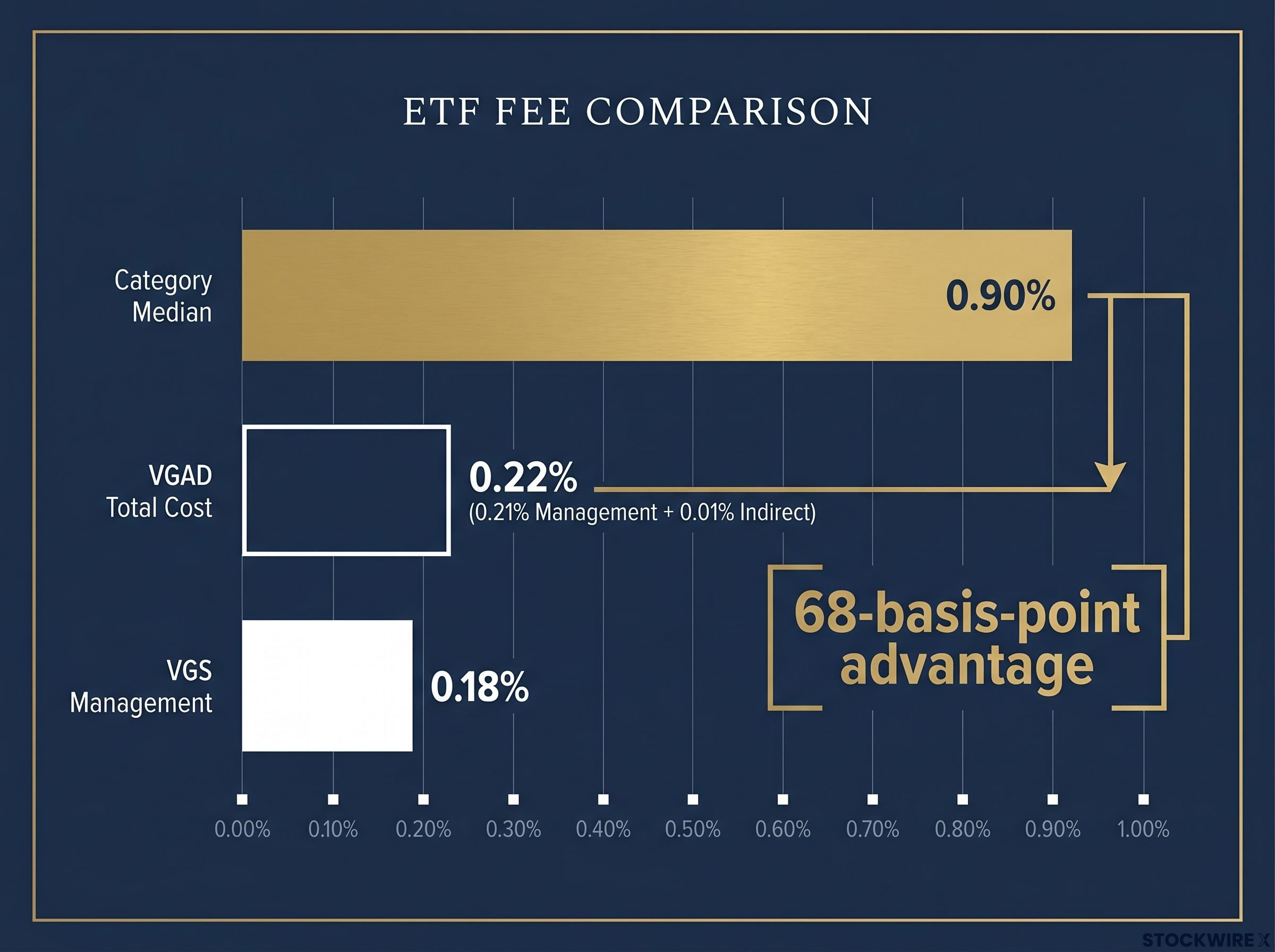

At 0.22% per year, VGAD charges less than a quarter of what the typical fund in its category costs. The median fee for currency-hedged international equity funds sits at 0.90%, a gap of 68 basis points that compounds every year an investor holds the position. That spread is not a rounding error. It is the single biggest reason Morningstar upgraded VGAD to its highest conviction rating.

The upgrade, from Silver to Gold, landed in April 2026. It marks a categorical shift in how Morningstar’s research team views this fund relative to its peers: not just competitive, but structurally advantaged. For Australian investors weighing their options in developed-market international equity exposure, it is a signal worth examining on its own terms rather than taking at face value.

Here is the data and the framework to decide whether VGAD belongs in your portfolio, or whether its hedged structure and US-heavy composition make it the wrong fit for your specific situation.

Morningstar’s Medalist Rating is a forward-looking assessment of whether a fund is likely to outperform its category peers over a full market cycle. It is not a buy recommendation. Five tiers capture the spectrum:

For passive index-tracking funds specifically, Morningstar assigns a 40% weighting to its Price Score within the overall Medalist Rating. That weighting is higher than for active funds, because index ETFs replicate the same benchmark. The underlying exposure is effectively identical across providers. What differs is what you pay for it.

Morningstar’s Price Score methodology, introduced in the April 2026 update, weights fee competitiveness at 40% for passive funds and 30% for active funds, a structural shift that directly explains why low-cost index ETFs are gaining ground on higher-fee active strategies across the ratings table.

VGAD received a Price Score of 2.06, placing it in the least expensive quintile of its Morningstar category. That score, weighted at 40% of the total rating, is what tipped the fund from Silver to Gold. For index ETFs, fees are not a secondary detail; they are structurally the most controllable performance driver.

Morningstar characterised VGAD as offering “structural advantages, including passive global market management, cost-efficient accessibility, and broad diversification.”

The upgrade was attributed by Morningstar research analysts, with Simonelle Mody, Associate Investment Specialist at Morningstar Australia, contributing to the assessment. Understanding what drove the rating, rather than treating Gold as a marketing badge, equips you to apply the same evaluative logic to any fund you compare.

VGAD’s fee structure breaks down into two components: a 0.21% management fee and 0.01% in indirect costs, producing a total cost ratio of 0.22% per annum. The category median sits at 0.90%.

That is a 68-basis-point annual advantage before any performance is measured.

| Fund | Structure | Management Fee |

|---|---|---|

| VGAD | Hedged | 0.21% p.a. |

| VGS | Unhedged | 0.18% p.a. |

| Category median | Various | 0.90% p.a. |

The 3-basis-point gap between VGAD and its unhedged sibling VGS reflects the operational cost of maintaining currency forwards. That premium is typical across hedged and unhedged pairs from all major providers and is not a VGAD-specific penalty.

Morningstar’s view is that in index-replicating strategies, what a fund charges is among the most dependable indicators of how it will perform against its peers over time. The underlying index exposure is effectively identical across low-cost and high-cost providers. What varies is the drag each fund imposes on the return stream. Over a ten-year horizon, that 68-basis-point annual advantage compounds into a material performance edge, and it requires no forecasting ability to capture.

The headline statistics suggest breadth:

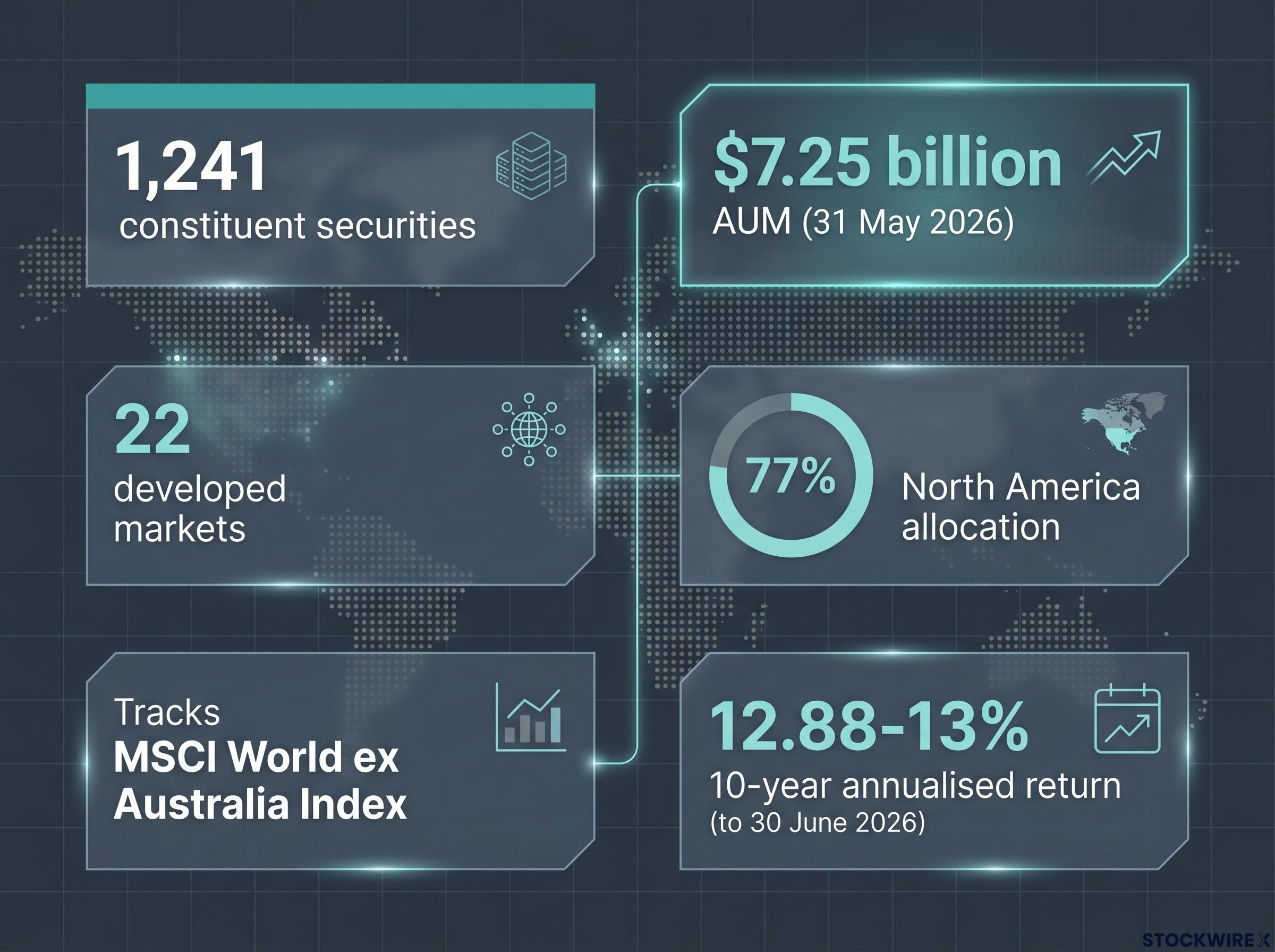

That last figure is where the breadth narrative needs qualifying. VGAD tracks the MSCI World ex Australia Index, a cap-weighted benchmark constructed to capture the largest listed companies across developed markets, accounting for approximately 85% of each market’s investable universe. The fund has delivered an annualised total return of approximately 12.88-13% over ten years to 30 June 2026, a track record shaped heavily by the dominance of US mega-cap technology names.

If you already hold significant US equity exposure through another fund or through direct shareholdings, VGAD amplifies rather than diversifies that concentration. That is the portfolio overlap question you need to answer before the rating matters.

The concentration is not a VGAD design choice. It is how global developed-market indices are constructed across all major index providers. US companies represent the largest share of global developed-market capitalisation, and cap-weighting reflects that reality. Morningstar Australia and Simonelle Mody note that many index constituents operate across multiple geographies and business lines, meaning their fortunes are not tied to any single product or market. Still, if your existing portfolio already carries heavy US or technology weighting, adding VGAD stacks that exposure rather than offsetting it.

US mega-cap concentration has reached levels with no modern historical precedent: five companies now control roughly 30% of total US equity market capitalisation, a structural reality that cap-weighted indices like the MSCI World ex Australia simply reflect rather than manage.

Currency hedging removes exchange rate movements from returns. When you hold VGAD, the performance you see reflects the underlying equity market in Australian dollar terms, stripped of AUD/foreign currency fluctuations.

The trade-off is symmetrical:

The cost of the insurance is knowable and fixed: a 3-basis-point management fee premium over VGS (0.21% versus 0.18%). Long-run MSCI World ex Australia data shows the hedged version delivered slightly higher returns in some periods but with higher volatility compared to the unhedged version, confirming that hedging reshapes the risk-return profile rather than improving it outright.

The practical magnitude of this trade-off becomes clearer when examining hedged vs unhedged ETF returns across a full currency cycle: the HNDQ and NDQ pair diverged by 13 percentage points over the year to May 2026, a gap produced entirely by AUD/USD appreciation rather than any difference in the underlying equity holdings.

Hedging changes the pattern of risk and return rather than eliminating risk. It is a specific tool for a specific portfolio objective, not a default enhancement.

Hedging is most defensible if your spending and liabilities are in Australian dollars and you want international equity returns without currency noise. It is not something to adopt because “hedging sounds safer.”

VGAD suits investors who:

VGAD may not suit investors who:

The Gold Medalist Rating is a within-category relative assessment. It tells you VGAD is one of the strongest vehicles in its category. It does not tell you whether that category belongs in your portfolio. That distinction is the most important one.

For most Australian investors evaluating this fund, the real decision is VGAD versus VGS. Same provider, same underlying equity universe, same index family, different currency treatment. The 3-basis-point fee premium for hedging is relatively small. The more material question is whether you want AUD currency exposure removed or retained, and that depends on your portfolio context, not on the rating.

VGS performance and concentration data from the same period reinforces the point: despite tracking more than 3,500 securities, the fund carries over 72% in US equities, meaning investors comparing VGAD and VGS are largely evaluating two vehicles with near-identical underlying composition but different currency structures.

The analysis comes down to two questions:

If the answer to the first question is yes and the second is no, VGAD’s case is exceptionally strong. A total cost ratio of 0.22% against a 0.90% category median, $7.25 billion in assets providing deep liquidity, and a ten-year annualised return of approximately 12.88-13% combine to make this a fund that is very difficult to displace within its category.

The Gold rating reflects genuine structural quality: low fees, broad diversification across 1,241 securities, and strong implementation by one of the largest global asset managers. That quality is real. Whether it fits your portfolio is a separate question only you can answer.

If the hedged structure does not match your objectives, or if the US concentration amplifies risk you already hold, treat VGAD as a benchmark for what cost-efficiency looks like in the category rather than a default choice.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results.

VGAD is the Vanguard MSCI Index International Shares (Hedged) ETF, tracking the MSCI World ex Australia Index across 1,241 securities in 22 developed markets, with currency hedging applied to remove AUD/foreign currency fluctuations from returns.

Morningstar's April 2026 upgrade was driven primarily by VGAD's fee competitiveness: a total cost ratio of 0.22% versus a category median of 0.90%, giving the fund a Price Score of 2.06 in the least expensive quintile, with fees weighted at 40% of the Medalist Rating for passive funds.

VGAD and VGS track the same underlying equity universe using the same index family, but VGAD applies currency hedging to remove AUD exchange rate movements from returns, while VGS leaves that exposure intact; the hedging costs 3 basis points more per year (0.21% versus 0.18%).

When the AUD rises against foreign currencies, VGAD outperforms unhedged equivalents by avoiding the translation drag; when the AUD falls, unhedged funds gain a tailwind that VGAD does not capture, meaning hedging reshapes the risk-return profile rather than improving it outright.

Approximately 77% of VGAD is allocated to North America, reflecting the cap-weighted construction of the MSCI World ex Australia Index, which means investors with existing US equity holdings will increase that concentration rather than diversify it by adding VGAD.