What Chip Earnings and the Oil Spike Mean for Your Portfolio

47 mins ago

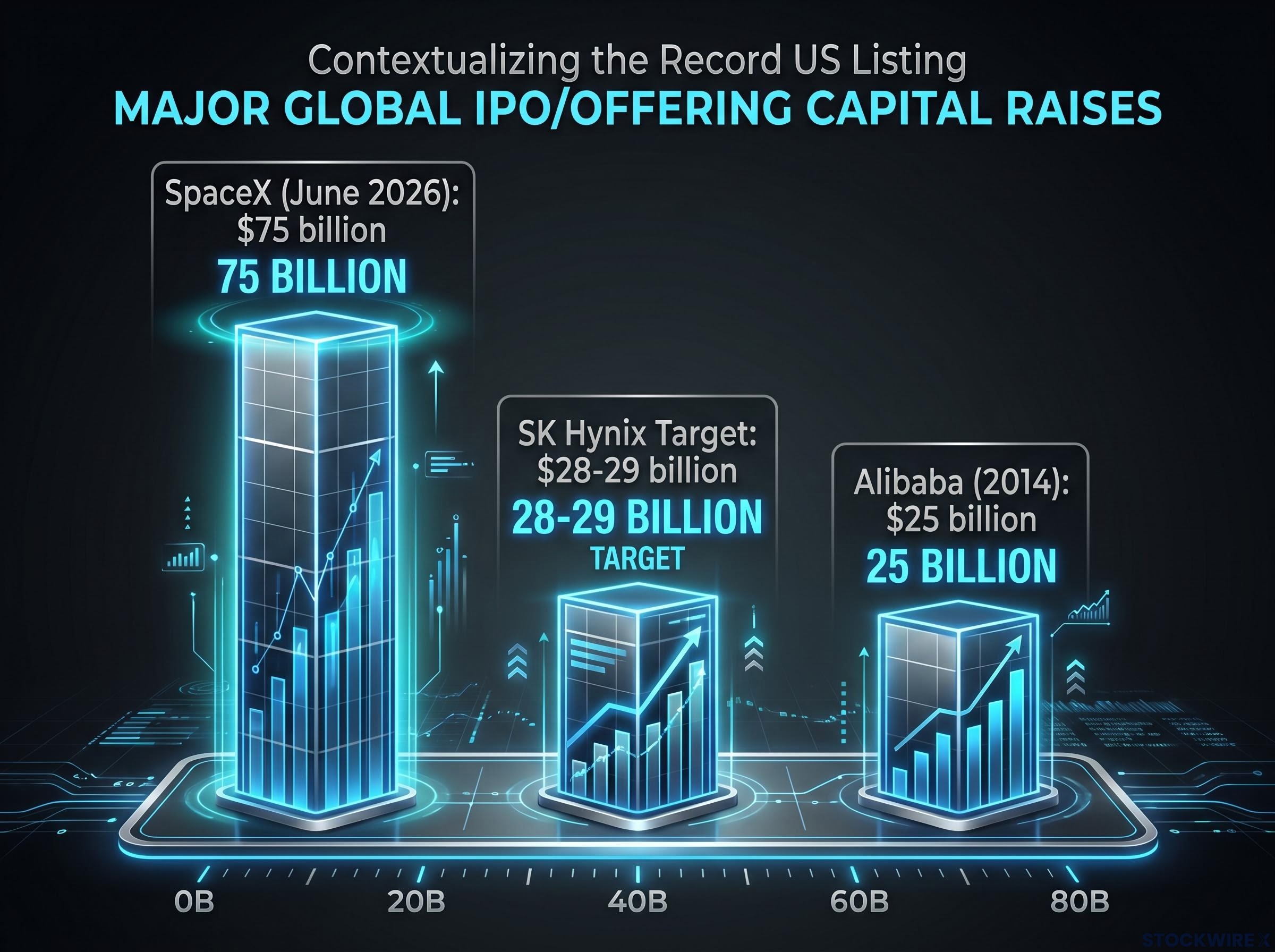

SK Hynix is listing on Nasdaq this week, targeting approximately $28 billion in gross proceeds. If the deal prices as expected, it will be the largest-ever US listing by a foreign company, surpassing Alibaba’s 2014 record of $25 billion.

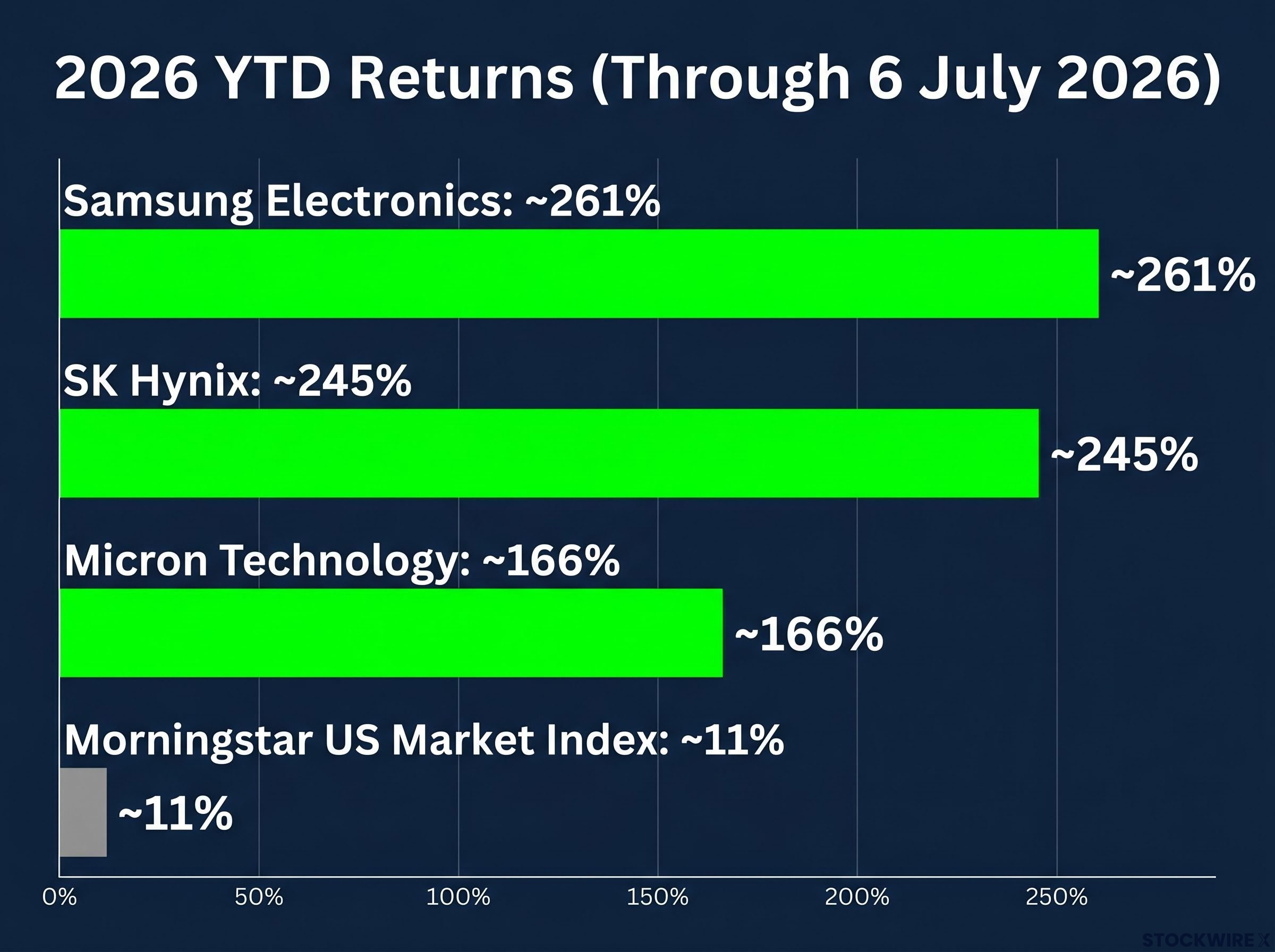

The timing is not accidental. SK Hynix is the dominant supplier of high-bandwidth memory (HBM), the chip that keeps AI data centres running at full capacity. Nvidia, Google, and Microsoft all depend on it. The company’s Korean-listed shares are up roughly 245% year-to-date through 6 July 2026, and it is capitalising on the AI trade at peak visibility.

Here is a clear framework for evaluating whether SKHY is worth buying at the IPO price, covering the deal structure, the business fundamentals, the valuation signal, and the risks that could make a strong company a poor investment at the wrong entry point.

The SK Hynix IPO is not a standard equity offering, and the structural details matter more than usual for US investors.

The company is offering 17.79 million new common shares via American Depositary Shares (ADSs), meaning this is a primary offering raising fresh capital rather than existing shareholders cashing out. Each ADS represents one-tenth of a common share, so 10 ADSs equal one common share listed in Seoul. Trading under the ticker SKHY on Nasdaq is scheduled to begin 10 July 2026, following pricing around 9 July.

Here are the core deal facts:

Renaissance Capital’s Nick Einhorn, who serves as the firm’s Director of Research, places the deal as the second-biggest IPO of 2026 by overall size, with only SpaceX’s $75 billion June offering having raised more capital.

The ADS structure means US investors are not buying the same instrument as Korean investors. The 10-to-1 ratio will influence how the share price reads relative to the Seoul-listed stock, a detail that matters when assessing whether post-IPO price movements reflect genuine fundamental shifts or structural arbitrage between two exchanges.

The US listing is not a routine capital raise. It is a deliberate attempt to close a structural valuation gap.

Korean semiconductor companies have historically traded at lower valuation multiples than comparable US-listed peers. Morningstar equity analyst Jing Jie Yu identifies the offering as explicitly intended to narrow this gap, often referred to as the “Korea discount.” By listing alongside Micron Technology on Nasdaq, SK Hynix positions itself for direct peer comparison by US institutional investors, rather than being valued solely against domestic benchmarks.

The Korea discount is a persistent structural feature of Korean equity markets, rooted in chaebol governance structures, historically weak payout culture, and the geopolitical risk premium attached to the peninsula, and it is precisely this gap that SK Hynix’s Nasdaq listing is designed to close by giving US institutional funds direct access to a stock many cannot hold through the Seoul exchange.

The valuation re-rating thesis: SK Hynix is betting that a Nasdaq listing will unlock higher valuation multiples by giving US institutional funds, many of which cannot or do not buy Korean-listed shares, a way to own the stock directly.

That access point matters. Many large institutional allocators are structurally unable to invest in Korean equities. The ADS listing unlocks a substantially larger pool of global capital at the precise moment AI demand gives SK Hynix its strongest pitch.

If the re-rating thesis works, SKHY could sustain a premium to its Korean-listed shares over time. If it does not, the IPO premium fades, and early US buyers absorb the gap. Understanding which outcome you are betting on shapes whether the IPO price looks attractive or aggressive.

High-bandwidth memory is the component that feeds data fast enough to keep GPUs and AI accelerators fully utilised. Without sufficient HBM, the most powerful AI chips in a data centre sit idle, waiting for data. It is not a peripheral component; it is the bottleneck that determines how much of an AI system’s theoretical performance actually translates into real-world output.

SK Hynix owns the bottleneck.

Q1 2026 revenue surged 198% year-over-year to a record 52.6 trillion won, according to the company’s SEC filing, reflecting tight HBM supply and strong pricing power.

The company’s position in the HBM market is specific and dominant:

The company’s market capitalisation exceeded $1 trillion in May 2026 and stood at approximately $1.03 trillion as of early July 2026.

A 198% revenue surge is not a normal business cycle outcome. It reflects a supply-demand imbalance that favours SK Hynix right now, and the question for investors is how long that imbalance persists before competitors and capacity expansions erode it. That question is what the next two sections answer.

HBM contract pricing for 2027 is already the subject of detailed structural analysis, with Bernstein projecting a 2-2.5x increase driven by a wafer economics gap that makes conventional DRAM materially more profitable per wafer, a substitution threat that amplifies fourfold at the hyperscaler purchase level once Nvidia applies margin preservation.

The business story is strong. The question is whether the price already reflects it.

Morningstar equity analyst Jing Jie Yu assigns SK Hynix a 3-star rating as of 8 July 2026. Under Morningstar’s rating system, a three-star designation indicates the stock is priced close to its estimated fair value, leaving buyers with little cushion for error or disappointment.

Morningstar’s 3-star rating signals that investors buying SKHY at the IPO are not getting a discount. They are paying approximately what the business is worth on current fundamentals, meaning future returns depend almost entirely on the AI cycle continuing to outperform expectations.

The performance numbers make that valuation context sharper. Here is how SK Hynix stacks up against its peers for 2026 year-to-date:

| Company / Index | 2026 YTD Return |

|---|---|

| SK Hynix | ~245% |

| Samsung Electronics | ~261% |

| Micron Technology | ~166% |

| Morningstar US Market Index | ~11% |

Over three years, SK Hynix shares have gained approximately 1,951% in Korean won. That is an extraordinary return, and it complicates the entry-point calculation for new buyers. Adding to the timing uncertainty, Korean-listed shares have already declined approximately 25% from their late-June 2026 peak.

For investors evaluating whether to buy SKHY on the open, this is the most actionable data point: the valuation reflects limited margin of safety, and the entry price assumes the AI cycle extends rather than normalises.

Memory markets have a pattern, and it runs on a cycle that has never broken permanently. Tight supply triggers industry-wide capacity builds. Those builds take 18-24 months to produce chips at scale. Then supply catches up with demand, prices compress, and margins contract. It has happened with DRAM. It has happened with NAND. There is no structural reason HBM is exempt.

Here are the five risk categories to weigh against the business case:

This is where the cycle risk becomes specific. According to Morningstar equity analyst Jing Jie Yu, the base case assumes that Samsung, Micron, and Chinese producers will all bring meaningful new HBM capacity to market over the next two years, with those investment commitments translating into chip output at scale around 2028.

A structured semiconductor cycle framework matters here because memory — including DRAM, NAND, and HBM — is identified as the highest-risk segment in the coming supply wave, with a realistic oversupply scenario in 2028-2029 as wafer capacity expands beyond AI-driven demand growth, the precise timeline the article’s near-term supply risk section flags.

That timeline is not a distant threat. It means investors buying SKHY at the IPO may be entering near the top of the current HBM pricing cycle. If Samsung and Chinese producers close the gap faster than the market currently assumes, the pricing power that drove that 198% revenue surge begins to erode, and the valuation built on its continuation compresses with it.

The investment case comes down to what kind of investor you are and how long you plan to hold.

| Dimension | Assessment |

|---|---|

| Business quality | Very high: HBM technology leader, tier-one AI customers, explosive growth |

| Current cycle | Extremely favourable: tight HBM supply, high prices, ~198% YoY revenue growth |

| Valuation and timing | Aggressive: ~245% YTD, >$1T market cap, 3-star Morningstar rating |

| Industry structure | Cyclical and competitive: history shows today’s tightness gives way to oversupply |

| Near-term supply risk | Elevated: significant competitive capacity additions projected within two years |

The $28 billion in fresh proceeds will be deployed into South Korean capacity expansion, including the Yongin fabrication plant (expected online H1 2027) and EUV lithography scanner acquisitions. That signals a company reinvesting for growth rather than harvesting, the right structure for a long-horizon bet but one that offers no near-term yield cushion if sentiment shifts.

For high-conviction investors who believe AI-driven HBM demand will remain structurally tight for years: a measured position with a willingness to average in on pullbacks and hold through a full memory cycle is the more defensible posture. For most retail investors, the risk-reward at IPO appears balanced rather than asymmetric. The AI and HBM story is substantially priced in.

Three signals to monitor after the dust settles on IPO week:

Buying a record-breaking IPO at full valuation after a 245% run means you are paying for a future that must outperform current expectations. That can work. But waiting for post-IPO volatility to settle and monitoring how the market values SKHY relative to Micron is, for most investors, the more defensible path.

For investors exploring alternatives to single-cycle chip exposure, our deep-dive into AI infrastructure bottlenecks examines why power availability and cooling density, rather than memory supply, may represent the most durable value positions in the AI buildout across 2026 and beyond.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

—

SK Hynix is listing on Nasdaq under the ticker SKHY via American Depositary Shares, with trading scheduled to begin on 10 July 2026 following pricing around 9 July. The offering targets approximately $28-29 billion in gross proceeds, which would make it the largest-ever US listing by a foreign company, surpassing Alibaba's $25 billion record set in 2014.

High-bandwidth memory is the chip that feeds data fast enough to keep GPUs and AI accelerators fully utilised; without it, the most powerful AI chips sit idle waiting for data. SK Hynix controls an estimated 56-62% of global HBM production, making it the dominant supplier to Nvidia, Google, and Microsoft, and the primary reason its Q1 2026 revenue surged 198% year-over-year to a record 52.6 trillion won.

Each SKHY ADS represents one-tenth of a common share listed in Seoul, meaning 10 ADSs equal one Korean-listed share. US investors are not buying the same instrument as Korean investors, and price movements in SKHY relative to the Seoul-listed stock can reflect structural arbitrage between the two exchanges rather than pure fundamental shifts.

The Korea discount refers to the persistently lower valuation multiples that Korean-listed stocks trade at compared to US peers, driven by chaebol governance structures, weak payout culture, and geopolitical risk premiums. By listing on Nasdaq alongside Micron Technology, SK Hynix aims to unlock access for US institutional funds that cannot hold Korean-listed shares and close this valuation gap through a re-rating to US peer multiples.

The core risks include memory market cyclicality, with Samsung, Micron, and Chinese producers all expanding HBM capacity that Morningstar projects could reach scale around 2028 and compress pricing; a Morningstar 3-star rating signalling the stock is priced near fair value after a 245% year-to-date run; and IPO-specific volatility from order imbalances and hedge fund ADS arbitrage in the weeks following listing.