Dow Hits 53,000 as Six S&P 500 Sectors Finish in the Red

11 hrs ago

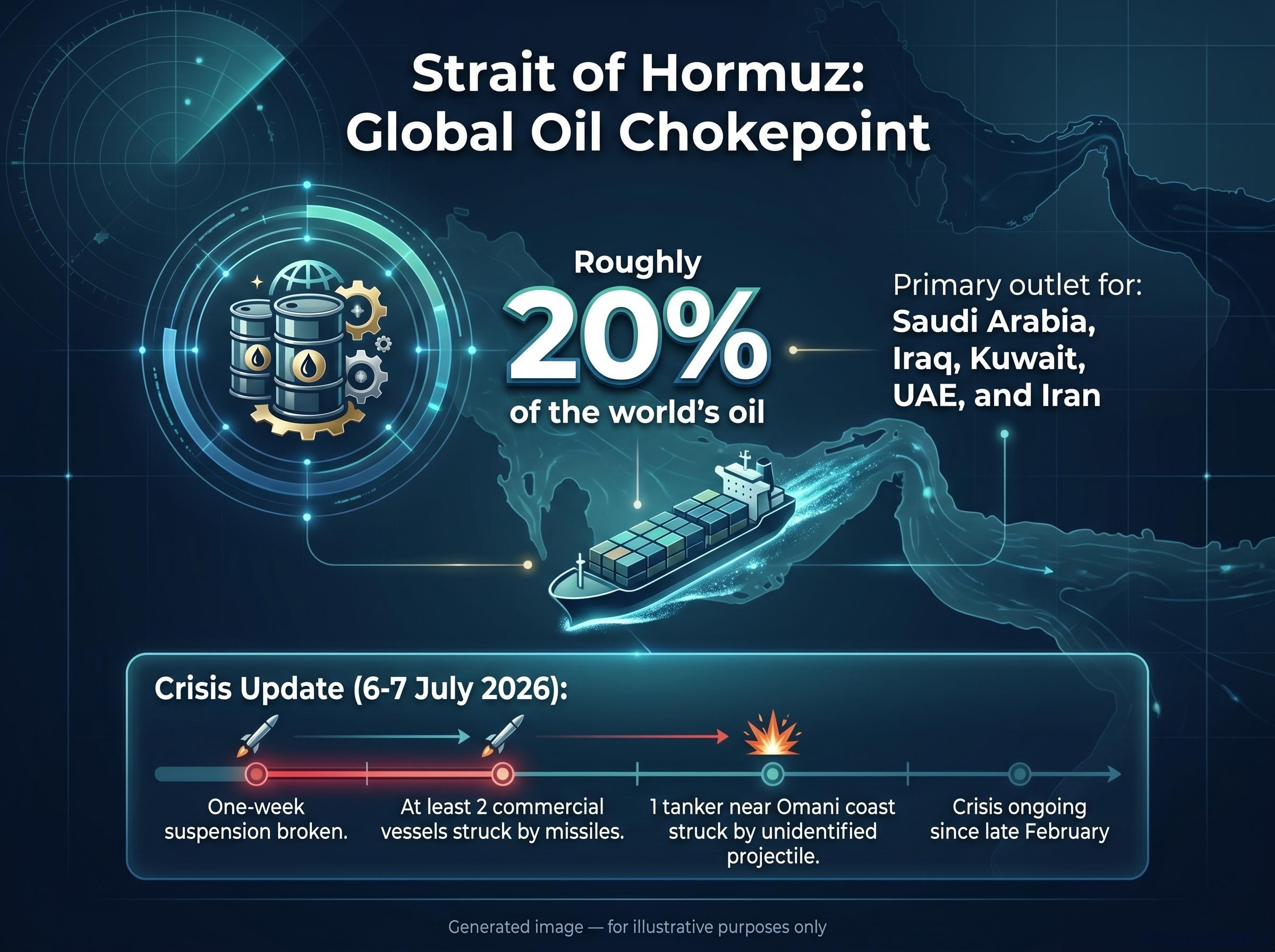

Iranian forces launched missiles against at least two commercial vessels passing through the Strait of Hormuz overnight, bringing a one-week cessation of attacks to an end and placing a fragile U.S.-Iran memorandum of understanding in serious jeopardy. The attack, confirmed by U.S. officials cited by Reuters via Axios, marks the resumption of a stop-start cycle of maritime harassment that has defined the 2026 Strait of Hormuz crisis since the U.S.-Israeli air campaign began in late February.

The strikes arrived on the same day Federal Reserve Governor Christopher Waller publicly declared the 2% inflation target “non-negotiable” and described U.S. inflation as entering an accelerating phase. That collision, a fresh energy supply shock landing on a central bank already in defensive posture, is the story underneath the headline.

Here is the chain of causation that connects a missile fired in the Persian Gulf to the interest rate environment shaping your borrowing costs, mortgage rates, and portfolio returns. The transmission mechanism matters more than the headline, and this article walks through each link.

At least two missiles were launched by Iranian forces at commercial vessels passing through the Strait of Hormuz on the night of 6-7 July 2026, with both ships sustaining significant damage and no casualties among those aboard. The U.K. Maritime Trade Operations agency also issued a separate report that a tanker heading south along the Omani coast had been struck by a projectile of unidentified origin, setting off a fire with no resulting injuries or environmental damage.

The Doha diplomatic framework that had underpinned the one-week pause was structured around a 60-day memorandum of understanding, and last week’s talks failed to produce any binding commitment on strait access before the overnight strikes resumed.

The confirmed facts:

This is not a first strike. It is the resumption of a pattern. Since late February, the strait has seen repeated cycles of escalation, pause, and re-escalation. That pattern is what markets are pricing: not a one-time spike, but a chronic harassment scenario. The distinction changes the duration and severity of the economic impact, because traders cannot fade a risk that keeps returning on a fortnightly schedule.

Roughly 20% of the world’s oil passes through the Strait of Hormuz under normal conditions.

That single statistic explains why this chokepoint has no peer. The strait is the primary maritime outlet for Saudi Arabia, Iraq, Kuwait, the UAE, and Iran, five of the largest oil exporters on the planet. When credible threats emerge against this route, the consequences cascade within hours.

War-risk insurance premiums jump first. Freight rates follow as shipowners demand compensation for the danger. Some operators reroute around Africa, adding weeks to voyage times and raising delivered costs. Effective global supply tightens even when no barrels are physically destroyed, because the market prices the risk of destruction, not just the destruction itself.

Alternative pipeline routes exist, but they carry limited capacity and cannot quickly replace seaborne volumes for most exporters. Earlier episodes in the 2026 crisis have already produced near-blockage conditions, meaning the strait’s vulnerability is not theoretical; it is established fact within this conflict cycle.

Pipeline bypass routes, including the Fujairah oil infrastructure that served as one of the few alternatives to seaborne Hormuz transit, have themselves been struck during this conflict cycle, compounding the bottleneck that alternative capacity was meant to relieve.

The absence of a credible alternative at scale means any sustained threat translates directly into higher delivered oil costs globally. That is why this is an inflation story, not just a shipping story.

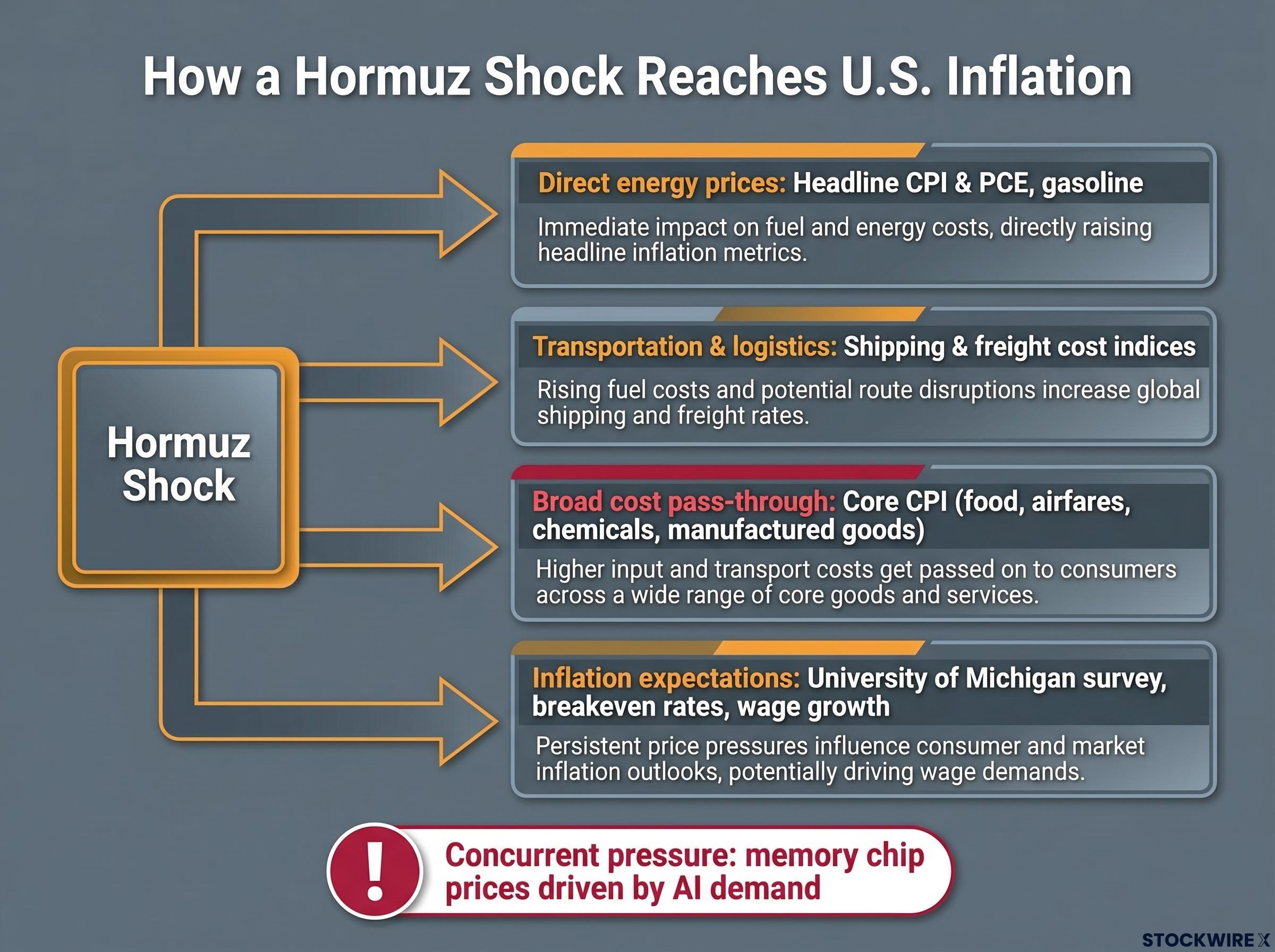

The link between a missile in the Persian Gulf and the price on a U.S. petrol pump runs through four distinct channels, each operating on a different timeline:

| Transmission Channel | Where It Shows Up in Inflation Data |

|---|---|

| Direct energy prices | Headline CPI and PCE energy components; gasoline prices within weeks |

| Transportation and logistics | Goods inflation via shipping and freight cost indices |

| Broad cost pass-through | Core CPI categories: food, airfares, chemicals, manufactured goods |

| Inflation expectations | University of Michigan survey, breakeven inflation rates, wage growth data |

A short-lived oil spike has a modest and temporary inflation impact. The risk materialises if the conflict proves durable. And the Hormuz shock does not arrive in isolation: concurrent inflationary pressure from memory chip prices driven by AI demand means energy is not the only supply-side force the Fed is already monitoring.

The first three channels operate mechanically. Expectations are different. Once workers and firms adjust their behaviour based on anticipated inflation, the Fed must work harder and longer to bring it back down. Rate rises that would otherwise cool demand take longer to bite when both sides of every negotiation, wages and prices, have already priced in higher inflation as a baseline.

This is the specific mechanism behind Waller’s characterisation of inflation as entering an accelerating phase. It is not merely elevated; it risks becoming embedded.

Waller spoke on 6 July 2026, the same day the strikes occurred. His remarks define the policy environment into which this shock landed.

Waller described the 2% inflation target as both credible and “non-negotiable.”

He characterised U.S. inflation as running materially above target and entering an accelerating phase. Where the Fed’s attention had previously been directed toward softness in the jobs market, employment conditions have since steadied and receded as the central bank’s primary concern; price stability has taken its place as the dominant risk.

The FOMC dissent recorded at the April 2026 rate decision, where hawks outnumbered the lone dovish dissenter three to one, illustrated that the committee was already tilting toward a more restrictive stance before the Hormuz crisis resumed its current phase.

The policy implications are direct. The likelihood of near-term rate cuts has fallen, even if easing had been on the table for later in 2026. An energy-driven inflation bump provides a clear reason to wait. The bar for “looking through” the shock is higher than usual, because inflation is already above target and accelerating. And if the conflict proves durable and CPI or PCE surprises to the upside, the risk tilts toward renewed tightening rather than patience.

There is a secondary effect worth noting: hawkish Fed expectations tend to support the U.S. dollar, which partly offsets imported inflation (oil is dollar-priced) but tightens financial conditions globally.

For the reader, “non-negotiable” is not rhetorical. It means the Fed will accept slower growth and higher unemployment before it tolerates a second inflation overshoot. A Hormuz-driven energy shock that bleeds into core inflation puts that tradeoff directly in play.

The overnight strikes do not tell you the outcome. They tell you the range. Here are the three paths the conflict can take, and the market and policy consequences of each.

| Scenario | Disruption Type | Inflation Impact | Fed Policy Implication |

|---|---|---|---|

| 1. Contained flare-up | Short spike, diplomacy resumes | Modest, temporary | Fed looks through it; rate path unchanged |

| 2. Chronic harassment | Missiles or drones every few days | Meaningful, persistent | Rate-cut window closes; higher for longer locks in |

| 3. Major disruption or blockade | Large share of flows cut off | Stagflation risk | Fed forced to choose between fighting inflation and cushioning a downturn |

Markets are currently pricing whether the resumed attacks represent a return to chronic Scenario 2 harassment after a brief pause, or the beginning of something closer to Scenario 3. The shape of the oil futures curve will be one of the clearest signals. Backwardation (near-term contracts trading above longer-dated ones) indicates traders expect scarcity to persist. Contango (the reverse) suggests they see the disruption as temporary.

A cost pass-through threshold of around $85-$90 per barrel sustained through Q3 2026 is where analysts estimate inventory buffers thin and the corporate calculus between margin erosion and volume protection shifts, meaning Scenario 2 chronic harassment carries a materially different inflation trajectory than Scenario 1.

Your task is not to predict which scenario unfolds. It is to recognise the signals that distinguish them. A persistent backwardated futures curve, rising war-risk insurance premia, and upward drift in core CPI are the early indicators that Scenario 2 is cementing, and that is when the Fed’s posture shifts from wait-and-see to actively hawkish.

The events of 6-7 July are a starting point, not a conclusion. These are the five indicator categories that will tell you where this is heading:

Tracking these five categories in the coming weeks gives you a materially better basis for positioning than reacting to individual headlines, because together they reveal whether the conflict is moving toward a chronic state or toward resolution.

The through-line is direct: a geopolitical flashpoint in the Persian Gulf is now a live input into U.S. inflation mechanics and, through the Fed’s reaction function, into interest rates, borrowing costs, and asset prices. The Hormuz shock is dangerous not primarily because of the initial oil spike, but because it arrives when the Fed has declared it has no tolerance for a second inflation overshoot.

Monitor the five signal categories identified above. Watch the Fed’s language for any shift from “looking through” the shock to “acting on” it. Position accordingly rather than reacting to each news cycle.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. These statements are speculative and subject to change based on market developments and geopolitical conditions.

The Strait of Hormuz is the world's most critical oil shipping chokepoint, through which roughly 20% of global oil supply passes under normal conditions. It is the primary maritime outlet for Saudi Arabia, Iraq, Kuwait, the UAE, and Iran, meaning any credible threat to the strait drives up war-risk insurance, freight rates, and ultimately delivered oil costs worldwide.

Iranian forces launched missiles at at least two commercial vessels transiting the Strait of Hormuz overnight on 6-7 July 2026, with both ships sustaining significant damage. A separate tanker near the Omani coast was also struck by a projectile of unidentified origin, triggering an onboard fire, according to U.K. Maritime Trade Operations.

A Hormuz attack transmits into U.S. inflation through four channels: direct energy price increases in headline CPI and PCE, higher shipping and logistics costs that reignite goods inflation, broad cost pass-through into trucking, agriculture, and manufacturing, and a shift in inflation expectations that can make price pressures self-reinforcing.

Fed Governor Christopher Waller declared the 2% inflation target non-negotiable on the same day as the attacks and described inflation as entering an accelerating phase, meaning the likelihood of near-term rate cuts has fallen sharply. If the conflict proves durable and CPI or PCE surprises to the upside, the risk tilts toward renewed tightening rather than patience.

The five key indicator categories are: the shape of the oil futures curve (backwardation signals persistent scarcity), war-risk insurance premia and shipping rerouting patterns, U.S.-Iran diplomatic and military developments, upcoming CPI and PCE inflation prints, and Fed communication from Waller and other FOMC members about whether they view the shock as temporary or structural.