Castlelake’s 650p easyJet Bid Faces Final Deadline Today

8 hrs ago

Foxconn just posted quarterly revenue of $78.71 billion. That figure landed nearly 6% above what analysts had already priced as a strong quarter, powered by AI server demand that management says is still accelerating into the second half of 2026.

This is more than a single company beating estimates. Foxconn occupies a position no other manufacturer holds: it is simultaneously NVIDIA’s largest server maker and Apple’s primary iPhone assembler. Its quarterly results function as a live composite reading on the two biggest hardware growth stories in technology right now, AI infrastructure and consumer electronics, delivered through one set of numbers.

Here is what drove the beat, what management is guiding for Q3, and where the genuine risks sit, so you can interpret what this result signals about the state of the AI hardware buildout and whether the momentum is sustainable.

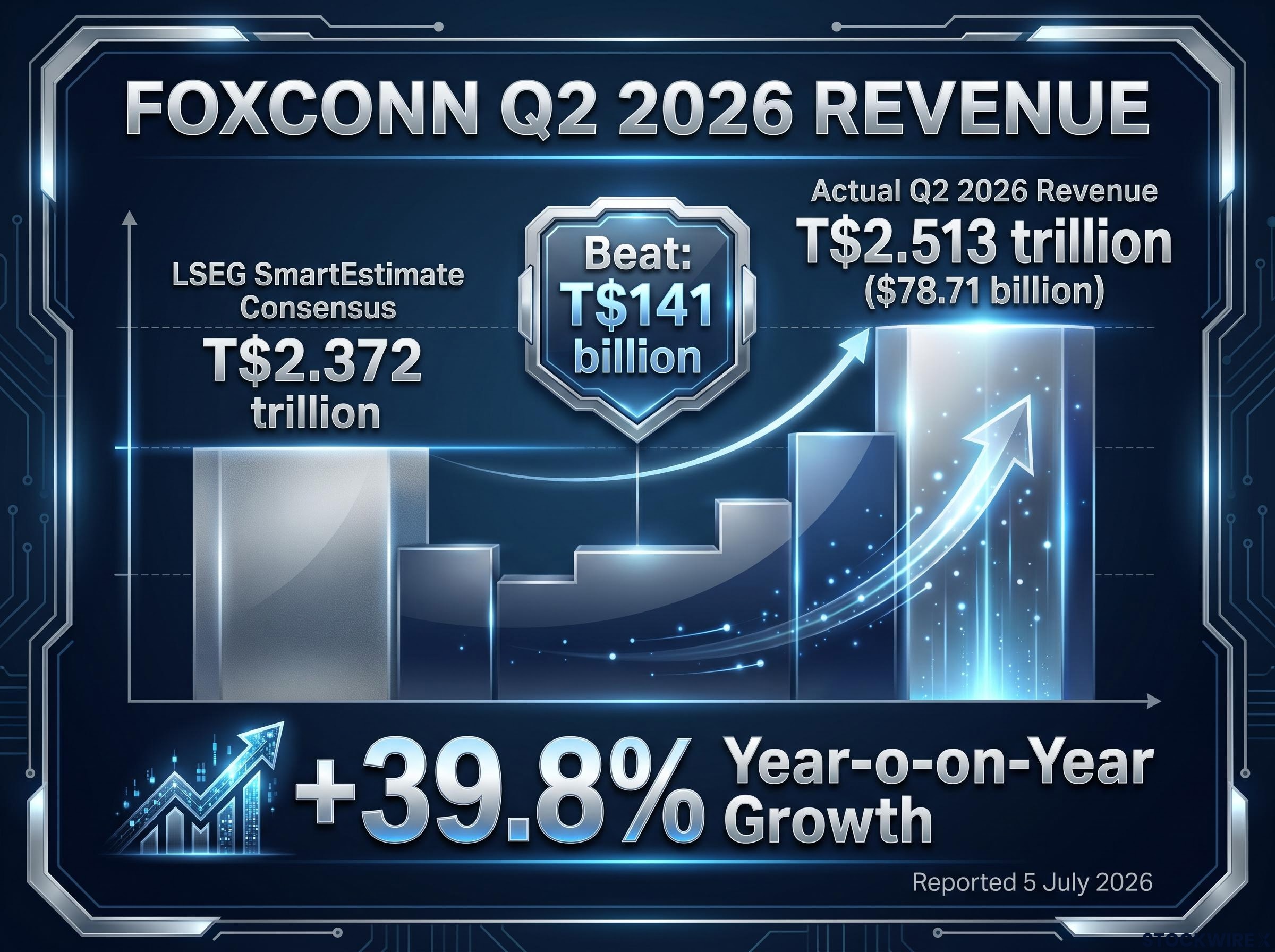

Foxconn reported its Q2 2026 results yesterday, 5 July 2026, and the numbers carried weight at every level. The April-June quarter came in at T$2.513 trillion (approximately $78.71 billion), representing a 39.8% year-on-year advance, a figure management rounded to “nearly 40%” growth in its statement.

The LSEG SmartEstimate consensus, a weighted forecast that gives greater influence to consistently accurate analysts, had projected T$2.372 trillion. Foxconn beat that by approximately T$141 billion. Analyst models were already pricing in a strong AI cycle. The company still exceeded them by a margin that signals genuine demand acceleration, not a routine beat on soft expectations.

The core figures:

June alone delivered T$821.8 billion in revenue, a 52.1% year-on-year surge that set a monthly record, suggesting the quarter finished on an accelerating trajectory rather than fading into quarter-end.

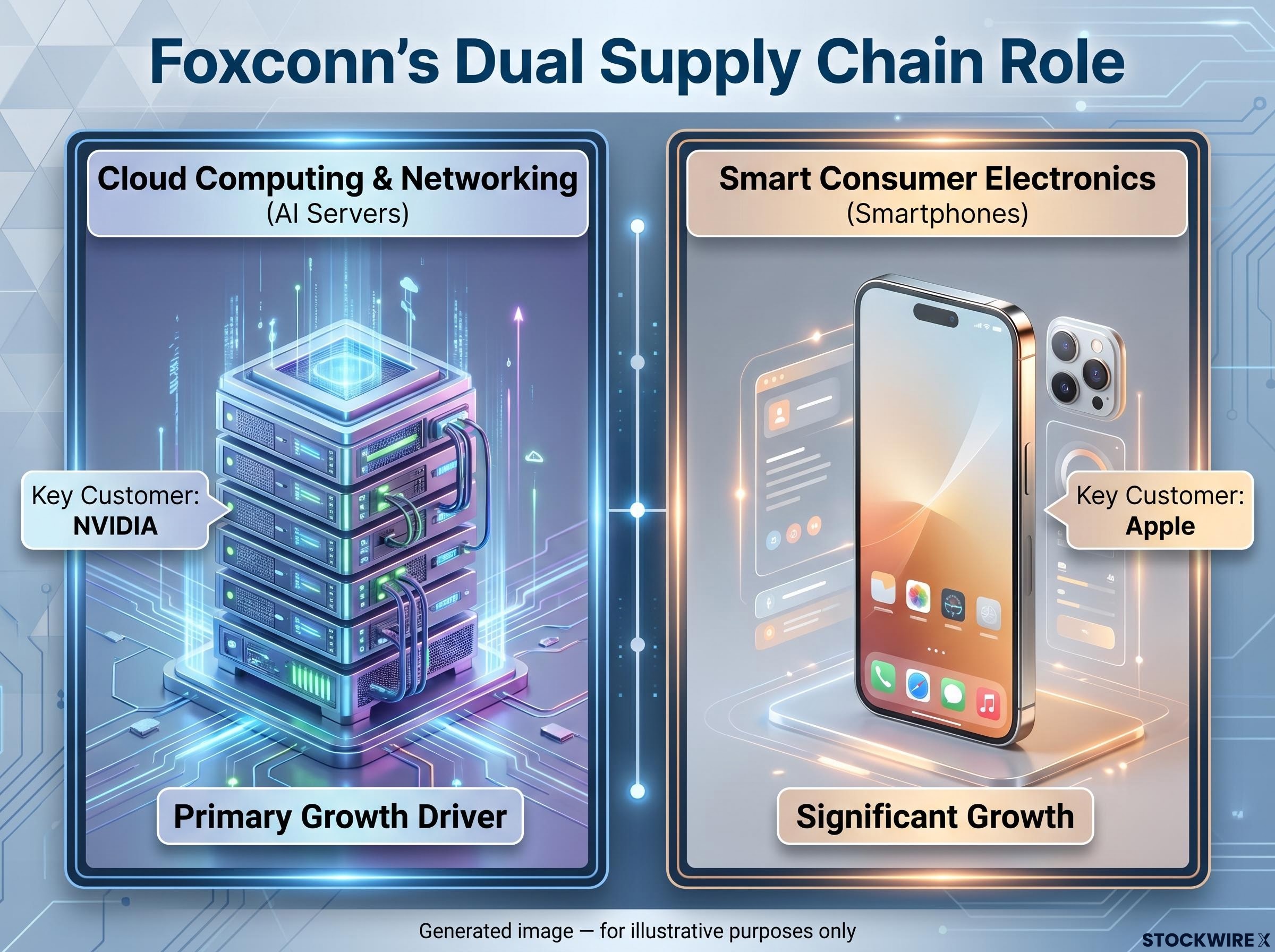

The top-line figure traces directly back to one business: cloud computing and networking products, the division that includes AI servers and related data-centre infrastructure. Management identified this segment as the primary Q2 growth driver, citing elevated demand as a direct consequence of accelerating AI deployment globally.

Foxconn is not a peripheral player in this supply chain. It is NVIDIA’s largest server manufacturer, meaning it assembles the GPU-based systems that power AI training and inference workloads at hyperscale and enterprise data centres worldwide. When hyperscalers commit capital to AI infrastructure, a significant share of that spend flows through Foxconn’s assembly lines.

Foxconn’s position as NVIDIA’s largest server manufacturer places it at the assembly layer of a tightly concentrated AI chip supply chain where four companies, NVIDIA, TSMC, ASML, and Broadcom, occupy distinct and non-interchangeable roles that no single quarterly result can fully capture.

That structural position is what makes the forward guidance particularly telling.

Management issued Q3 2026 guidance alongside the results, and the messaging on AI was unambiguous:

That forward visibility on AI rack volumes tells you something specific: hyperscaler capital expenditure is still in deployment mode, not consolidation mode. Foxconn’s order book supports continued outperformance, and management is willing to guide growth-on-growth without hedging on the demand side.

Hyperscaler capital expenditure commitments running at $630 to $725 billion for 2026 represent the upstream demand signal that ultimately flows into Foxconn’s order book, and the scale of that deployment explains why management felt confident guiding AI rack volumes higher on both a sequential and annual basis.

Foxconn holds three identities simultaneously: the world’s largest contract electronics manufacturer, NVIDIA’s lead server partner, and Apple’s primary iPhone assembler. No other company on earth offers that combination of exposure.

The analytical value of this dual position became clear in Q2 2026. Both segments, AI servers and consumer electronics, grew strongly. Neither was compensating for weakness in the other. That distinction matters: it points to broad-based hardware demand strength across two distinct end markets, not a lopsided result driven by a single customer or product cycle.

On the consumer side, Foxconn reported that “smart consumer electronics,” including iPhones, posted “significant” growth during the quarter. Detailed segment revenue figures were not disclosed, but favourable seasonal patterns are set to carry that performance into Q3: the back-to-school period and Apple’s annual iPhone production ramp ahead of new model launches typically push assembly volumes higher across the July-September window.

The consumer electronics momentum Foxconn is assembling against reflects a broader Apple outperformance story: iPhone market share reached record levels in Q1 2026 even as global smartphone shipments contracted roughly 6%, a divergence that makes the consumer segment’s contribution to Foxconn’s numbers structurally durable rather than cyclically opportunistic.

| Segment | Key customer(s) | Q2 2026 performance | Q3 2026 outlook |

|---|---|---|---|

| Cloud computing and networking products (AI servers, data-centre infrastructure) | NVIDIA, hyperscale data-centre operators | Primary growth driver; elevated demand from accelerating AI deployment | AI rack volumes growing quarter-on-quarter and year-on-year |

| Smart consumer electronics (smartphones, devices) | Apple | “Significant” growth reported (detailed figures not disclosed) | Seasonal tailwinds: back-to-school builds, iPhone production ramp |

The simultaneous strength across both segments is the detail that elevates this result beyond a narrow AI story. You cannot explain away the beat as one-dimensional when the consumer device cycle is also running hot.

Management paired the strong results with a cautionary note. Alongside the Q2 release on 5 July 2026, Foxconn raised concerns about “volatile” conditions in global politics and flagged broader geopolitical and macroeconomic turbulence as variables that could weigh on the business.

Management characterised the current operating environment as “volatile,” a direct signal that the company sees external political and economic conditions as a material variable for the second half of 2026.

The warning was broad. The company offered no detail on particular regions, events, or policy shifts it had in mind. But given Foxconn’s structural position as a globally distributed manufacturer with heavy concentration in Asia, the categories of risk are clear:

NVIDIA’s coordinated partnership agreements across South Korea’s memory, cloud, and energy sectors illustrate how actively the company is hardening its AI infrastructure supply chain across US-aligned manufacturing nodes, a strategy that also reduces the geopolitical concentration risk that Foxconn’s management flagged as a material variable for the second half of 2026.

The most important detail in this warning is what it did not include. Management raised no concerns about weakening orders, softening demand, or customer pullbacks. The caution is directed entirely at exogenous macro and political risks, not at the health of Foxconn’s own pipeline. That distinction tells you the company’s visibility into its order book remains strong, and that the principal uncertainty is about what happens around the business, not inside it.

Taken together, Foxconn’s Q2 2026 quarter delivers four distinct signals for anyone positioned in or around the AI hardware supply chain:

The beat magnitude, the forward guidance on AI rack volumes, and the nature of the risk warning collectively point to an AI hardware buildout that is structurally intact but politically exposed. For investors, that distinction shapes how you size risk: the threat is not that demand is cooling, but that the globally distributed supply chain delivering on that demand sits in the path of geopolitical uncertainty.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Foxconn’s Q2 2026 result confirms that the AI infrastructure investment cycle has reached a scale where it is materially moving results at one of the world’s largest manufacturers, not just in the financial statements of the hyperscalers placing the orders.

The combined AI server momentum and consumer electronics tailwinds heading into Q3 make near-term revenue direction relatively clear. The geopolitical risk warning is a reminder that Foxconn’s exposure to global trade dynamics is a persistent variable, not a one-quarter concern.

What to watch from here: Q3 2026 AI rack shipment volumes and any developments in trade or tariff policy affecting Asian manufacturing will be the most important follow-on signals from this result.

These statements are speculative and subject to change based on market developments and company performance.

Foxconn reported Q2 2026 revenue of T$2.513 trillion (approximately $78.71 billion), representing 39.8% year-on-year growth and beating the LSEG SmartEstimate consensus by approximately T$141 billion.

The beat was driven primarily by elevated demand in Foxconn's cloud computing and networking products segment, which covers AI servers and data-centre infrastructure assembled for customers including NVIDIA, reflecting accelerating global AI deployment that outpaced already-bullish analyst models.

Foxconn is NVIDIA's largest server manufacturer, meaning it assembles the GPU-based systems used for AI training and inference at hyperscale and enterprise data centres; when hyperscalers increase AI capital expenditure, a significant share of that spend flows through Foxconn's assembly lines.

Management guided for AI rack shipment volumes to grow on both a sequential and annual basis, with overall operations also expanding, and raised no concerns about demand softening, directing its caution entirely at geopolitical and macroeconomic externalities.

Foxconn management characterised the operating environment as volatile and cited geopolitical and macroeconomic turbulence as material risks, specifically around trade and tariff policy changes, currency movements, and regional political tensions in Asia, while noting no concerns about weakening orders or customer pullbacks.