Uber’s $1B European Expansion Shrinks to Two Markets

3 hrs ago

Castlelake has until the close of business today, 5 July 2026, to either table a formal offer for easyJet or walk away. That deadline is not a formality. It is the moment that determines whether the airline’s shareholders receive a bid premium or absorb a sharp reversal in a share price that has already priced in meaningful deal probability.

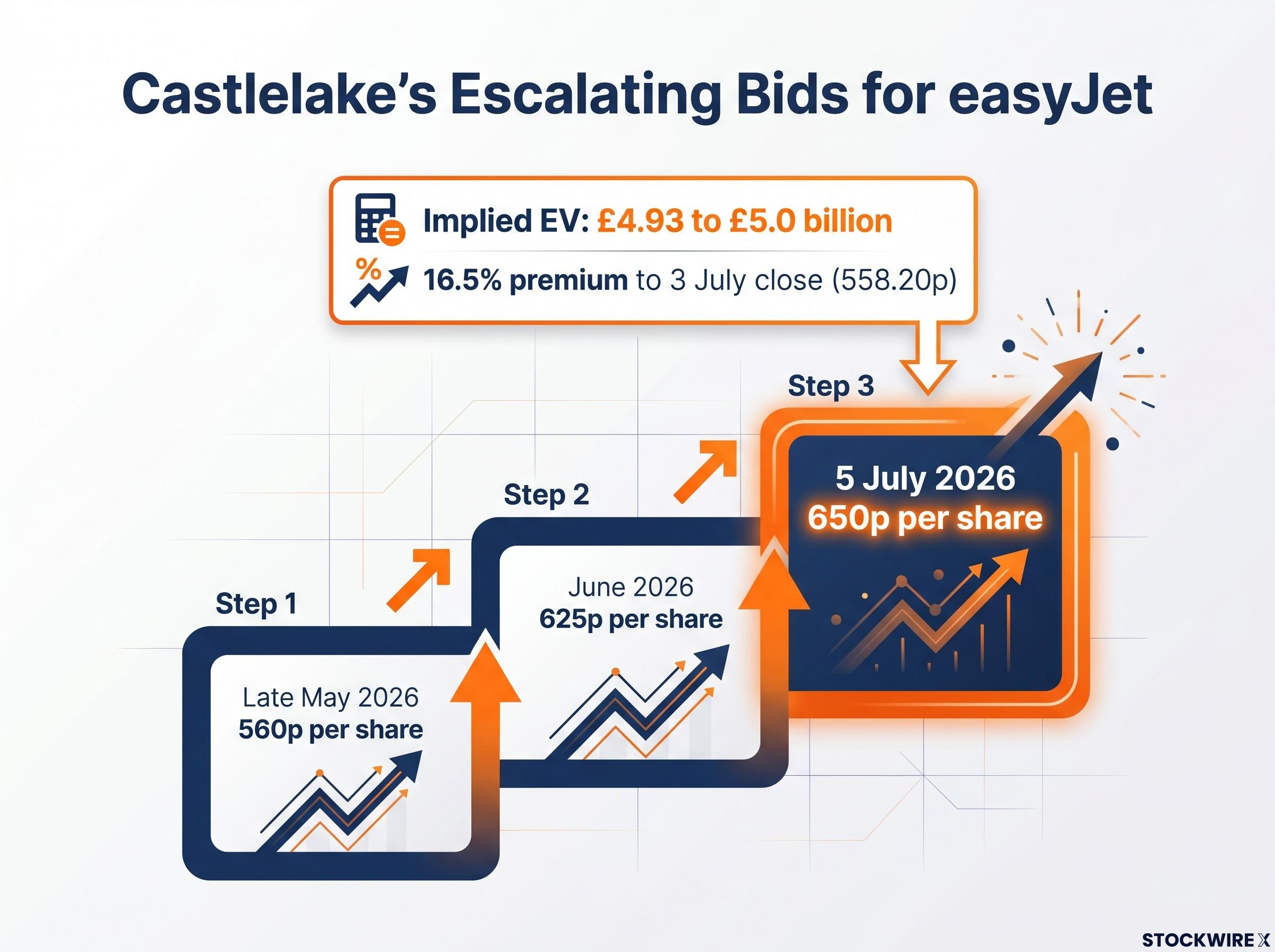

The Minneapolis-based alternative asset manager has escalated its indicative approach three times, from 560p to 625p and most recently to 650p per share, each rejected by the easyJet board. At 650p, the implied enterprise value sits at roughly £4.93 to £5.0 billion, a premium of approximately 16.5% to the 3 July closing price of 558.20p. What makes this unusual is the acquirer: Castlelake is an aviation asset specialist, not an airline operator. That distinction tells you something specific about what it is actually buying.

This piece maps what has happened, why Castlelake wants easyJet’s assets specifically, what the Haji-Ioannou family’s 15.3% stake means for the outcome, and what each scenario from today’s deadline looks like if you hold the stock.

Castlelake first approached easyJet in late May 2026. What followed was not a single proposal but a negotiating arc, three bids, three rejections, and multiple deadline extensions that brought the process to today’s resolution point.

At 650p, the implied enterprise value is approximately £4.93 to £5.0 billion, representing a 16.5% premium to the 3 July close of 558.20p.

The bid is supported by Peter Bellew, a former easyJet COO who left the airline suddenly in 2022, alongside Mark Breen. Bellew’s involvement adds operational credibility to what would otherwise read as a pure financial play. Three escalations and repeated Panel extensions tell you Castlelake has not been bluffing. And the board’s rejections look more like a valuation dispute than a categorical refusal of the deal itself.

The PUSU rule, short for Put Up or Shut Up, is the mechanism the UK Takeover Panel uses to prevent indefinite bid speculation from distorting a company’s share price. Once a potential bidder is publicly identified, the Panel sets a deadline by which the bidder must either announce a firm intention to make an offer or confirm it will not proceed. The Panel had already granted multiple extensions in this case, a signal that substantive engagement was ongoing.

Takeover Panel intervention can reshape a bid’s trajectory in ways that extend well beyond the initial deadline, as the Humm Group case demonstrated when the Panel ordered corrective disclosure after finding the board had privately rejected a proposal while publicly signalling willingness to engage.

Today, 5 July 2026, is that deadline. The two outcomes carry structurally different consequences:

For investors holding easyJet shares today, the specific language in any RNS (Regulatory News Service) announcement is the single most important variable. “Firm intention” and “does not intend” have price implications that will play out within minutes of publication.

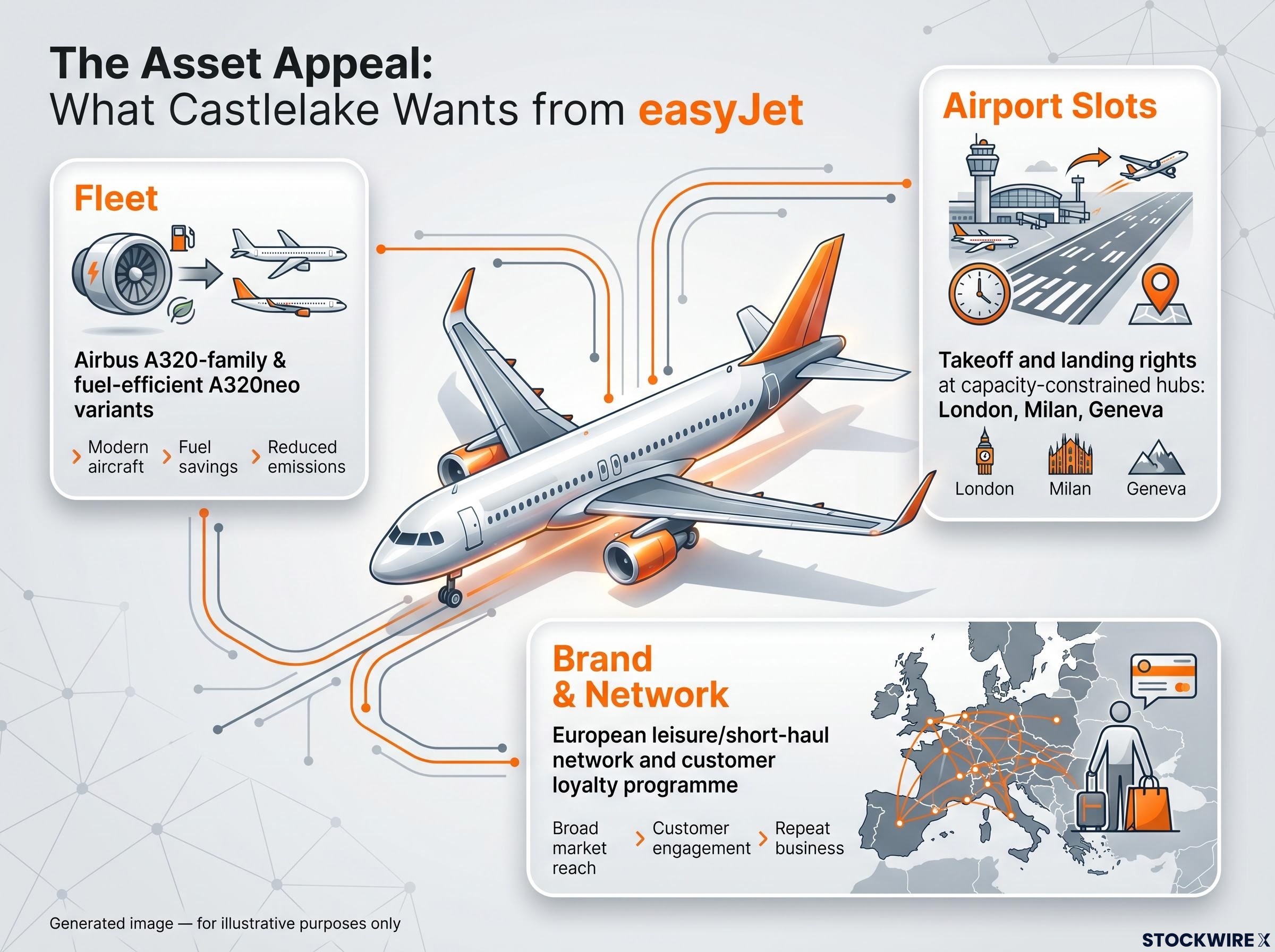

Castlelake is not an airline operator looking for European scale. It is an aviation asset specialist. That distinction reshapes the entire acquisition thesis.

The interest centres on three asset categories:

Airport slots at capacity-constrained hubs are the crown jewels of this deal: hard to replicate, valuable to operate, and potentially worth more than the market currently prices into easyJet’s equity.

An asset-specialist acquirer pricing slots and fleet collateral means the bid valuation is partly anchored to assets that do not appear clearly on easyJet’s income statement. That is why the board’s resistance on price may be more justified than the headline premium of 16.5% suggests.

The timing of Castlelake’s approach was not accidental. A specific set of financial conditions opened the window.

| Metric | Actual / reported | Consensus / expectation | Variance |

|---|---|---|---|

| H1 FY2026 EPS | -£0.501 | -£0.4345 | ~15.3% miss |

| Jet fuel costs | Rising, geopolitical pressure | Moderation expected | Negative surprise |

| Summer bookings | Weaker than forecast | Seasonal recovery | Demand shortfall |

The H1 earnings miss was the primary vulnerability signal. Reported EPS of -£0.501 fell short of the analyst consensus of -£0.4345 by roughly 15.3%, with the gap attributable to accelerating jet fuel costs (elevated in part by geopolitical tensions surrounding the Iran conflict) and summer booking volumes that came in below expectations.

That earnings pressure, combined with the 558.20p close on 3 July, created a depressed valuation relative to underlying asset quality. This is precisely the condition that makes a premium bid attractive to frustrated shareholders while the board argues the stock is worth more on a normalised basis. It is also what makes the shareholder vote, if a formal offer arrives, genuinely contested.

The broader UK equity de-rating has compounded the stock-specific pressure on easyJet: domestic institutional ownership of UK equities has fallen from around 80% in the early 1990s to roughly 42% today, reducing the stabilising bid that would otherwise limit how far individual stocks overshoot to the downside on earnings misses.

The bid’s fate may hinge less on institutional fund managers than on one family.

With a shareholding of approximately 15.3% linked to founder Stelios Haji-Ioannou, the Haji-Ioannou family ranks as easyJet’s single largest shareholder, placing them in the role of decisive swing factor in any bid outcome.

At standard UK takeover acceptance thresholds (typically 50% plus one share for a recommended offer), a 15.3% bloc that votes or accepts collectively can either clear the path or block the deal without needing to move other major shareholders. The family has historically been vocal and interventionist on strategic matters affecting the company.

Blocking position dynamics operate similarly across major takeover regimes: in the Accent Group bid, Frasers entered the process already holding 22.9% of the target, a stake large enough to deter competing bidders and shape the board’s negotiating posture before any formal offer document was issued.

The two directions carry markedly different market consequences:

For investors watching today’s announcement, the Haji-Ioannou family’s first public statement on any formal offer will be a more important price signal than the board’s recommendation. Their 15.3% gives them effective veto or acceleration power over the outcome.

The PUSU deadline creates a clean decision tree. Each branch carries distinct implications depending on what price you hold easyJet at.

What to watch on the RNS feed: The phrases “firm intention to make an offer” and “does not intend to make an offer” are the two specific formulations that carry immediate price consequences. Monitor the London Stock Exchange’s Regulatory News Service for any statement from easyJet’s board or Castlelake before the close of business today.

The scenario that matters most for your position depends on your entry price. Buyers near current levels face asymmetric risk if the bid collapses. Those who entered below 558p need to weigh whether 650p reflects full value or whether a rival approach could push the price higher.

Today’s PUSU deadline resolves the question of Castlelake’s immediate intent. It does not resolve the question of easyJet’s underlying value, or the competing assessments of a board that has rejected three offers and shareholders absorbing an earnings miss.

Two monitoring priorities remain active regardless of what the RNS carries this evening. The first is the Haji-Ioannou family’s public stance, which will shape completion probability more directly than the board’s recommendation. The second is whether easyJet enters a formal offer process or a standalone recovery period against the same cost and demand pressures that opened this window in the first place.

Director equity alignment shapes how boards assess and communicate bid adequacy: directors whose personal wealth is closely tied to share price tend to evaluate premium offers differently from those collecting fixed fees against a minimum equity threshold, a distinction that becomes structurally significant when a board is advising shareholders to reject an approach at three successive offer levels.

Watch for two specific phrases on the RNS: “firm intention to make an offer” or “does not intend to make an offer.” The distinction between them is the difference between a formal takeover timetable and a cooling-off period with no bid on the table.

Parse the language, stress-test your position against both outcomes, and let the announcement dictate the next decision rather than the speculation preceding it.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements regarding bid outcomes and share price scenarios are speculative and subject to change based on market developments and regulatory processes.

The PUSU (Put Up or Shut Up) rule is a UK Takeover Panel mechanism requiring a named bidder to either announce a firm intention to make an offer or confirm it will not proceed by a set deadline. For the easyJet takeover, that deadline is 5 July 2026, and Castlelake must commit to a formal offer or enter a cooling-off period that prevents it from returning without Panel dispensation.

Castlelake has made three escalating indicative proposals: 560p, 625p, and most recently 650p per share. At 650p, the implied enterprise value is approximately 4.93 to 5.0 billion pounds, representing a 16.5% premium to easyJet's 3 July closing price of 558.20p.

The board has maintained that each offer undervalues the business, a position strengthened by the argument that easyJet's airport slots at capacity-constrained hubs like London, Milan, and Geneva carry asset value that does not show clearly on the income statement and is not fully reflected in the 650p offer price.

If Castlelake confirms it does not intend to make an offer, any takeover premium embedded in the current share price would unwind, with the 558.20p close on 3 July acting as the reversion anchor. The stock could trade below that level if the market had been pricing meaningful completion probability, given ongoing earnings pressure and fuel cost headwinds.

The Haji-Ioannou family holds approximately 15.3% of easyJet, making them the single largest shareholder. At standard UK takeover acceptance thresholds of 50% plus one share, that bloc alone can either clear the path to deal completion or block Castlelake from reaching the necessary acceptance threshold without needing to move any other major shareholder.