Why a Rising AUD Is Quietly Eroding Your International ETF Returns

Jul 3, 2026

A company worth more broken apart than whole sounds like a contradiction. It is not. It is a documented market pattern with a name, a formula, and a set of corporate responses that have created real investment opportunities across U.S. equities for decades.

The pattern has a live example right now. On 29 June 2026, Comcast announced it will spin off NBCUniversal and Sky into a separate public company, retaining up to 19.9% of the new entity for approximately one year before monetising the stake. The precision of that ownership figure is not incidental, and the reasoning behind it tells you something important about how major corporate transactions are actually structured.

Here is the framework for understanding why conglomerate discounts form, how spinoffs close them, what separates a genuine value-unlock from a corporate shell game, and how to read the structural signals (like an ownership percentage calibrated to exactly 19.9%) that professionals use to evaluate whether a breakup will create value for shareholders.

Consider a cable infrastructure business and a streaming media business. They have different growth rates, different risk profiles, and attract entirely different investor bases. Bundle them inside one corporate structure, and the market is forced to apply a single blended valuation multiple that satisfies neither side.

That blended penalty is the conglomerate discount: the gap between a diversified company’s actual market capitalisation and the aggregate value its individual businesses would command if each traded on its own.

Four forces drive the discount:

Empirical research across developed markets typically finds conglomerate discounts in the mid-single to mid-teens percent range. That is not a rounding error on a balance sheet. It represents a recurring, measurable inefficiency that has historically been correctable through the right corporate action.

Disney offers a useful illustration. Disney+ sits inside a large conglomerate alongside theme parks, broadcast networks, and studios, yet Netflix trades as a focused, pure-play streamer in the same content industry. Despite competing for the same subscribers and operating under the same content economics, Netflix commands a significantly higher valuation multiple than the Disney+ business implies within the parent structure. The gap between those two multiples is precisely what the conglomerate discount looks like in practice.

A spinoff distributes shares of a subsidiary to existing shareholders, creating a new independent public company without selling anything to an outside buyer. You end up owning stock in both the parent and the new entity, and no cash changes hands.

Once you understand why the discount forms, the spinoff mechanism feels almost obvious. It attacks every driver of the penalty simultaneously through four channels:

The self-selection point matters directly to you. A spinoff is not just a corporate event to observe. It is an active decision point: you will need to choose which post-separation entity, if either, fits your own investment objectives.

Historically, breakup and sum-of-the-parts (SOTP) situations have been recurring targets for activist investors and have often led to outperformance when the underlying businesses were solid and the transaction was well designed.

Activist investors play a central role in forcing these separations into motion: the Elliott Investment Management intervention at Norwegian Cruise Line Holdings, where a 10%-plus stake preceded a full boardroom overhaul, illustrates how accumulating a position and publicly pressing for a structural change converts a documented discount into a catalyst.

A new ticker symbol does not fix a bad business. Before celebrating the value-unlock thesis on any announced separation, check whether the conditions for failure are present.

Four red flags should trigger scepticism:

Each of these flags translates into a specific question you can ask when Comcast or any other conglomerate announces a breakup. They are the difference between identifying a genuine opportunity and misreading a corporate distress signal.

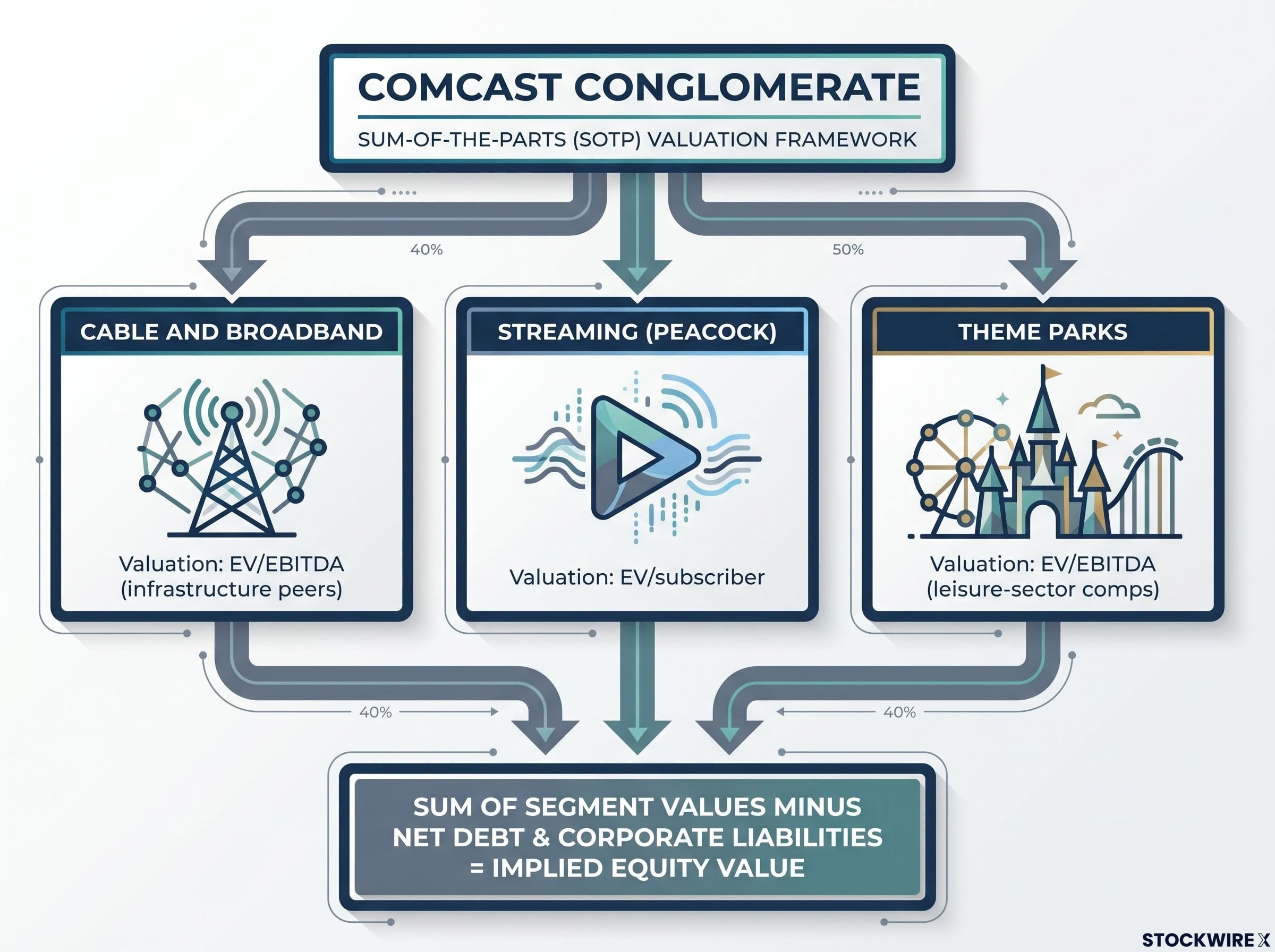

Sum-of-the-parts (SOTP) valuation is the framework that converts the conglomerate discount from an abstract observation into a number you can measure. It is the primary analytical tool activists use to build the case for a breakup, and it is what professional analysts run post-announcement to assess whether the value release is already priced in.

The process follows five steps:

The formula: Conglomerate Discount = (SOTP Value minus Current Market Cap) ÷ SOTP Value × 100%

Applied to Comcast, the exercise looks like this: the cable and broadband segment would use infrastructure-peer multiples, while NBCUniversal/Sky would use media and streaming comparables. Running both through SOTP reveals what the market was not pricing into the combined entity.

Sum-of-parts valuation is not limited to traditional conglomerates: Piper Sandler’s 17-segment Tesla framework applies the same segment-by-segment logic to a company whose automotive, software, and robotics divisions carry entirely different growth profiles and appropriate multiples, demonstrating how the method transfers across sectors beyond cable and media.

| Business Segment | Suggested Valuation Method | Rationale |

|---|---|---|

| Cable and broadband | EV/EBITDA (infrastructure peers) | Capital-intensive, stable-cashflow business benchmarked against cable and connectivity comps |

| Streaming (Peacock) | EV/subscriber | Subscriber-growth-stage business best compared to pure-play streaming peers |

| Theme parks | EV/EBITDA (leisure-sector comps) | Cyclical, asset-heavy operations valued against entertainment and leisure peers |

The formula and these five steps give you a screen you can apply to any conglomerate announcement. If the SOTP value is materially above the market cap and a credible catalyst is present, you have the analytical foundation to evaluate whether an opportunity exists.

Intrinsic value estimation sits beneath every SOTP exercise: the segment-level multiples and DCF inputs used to calculate each division’s standalone worth are the same tools value investors apply to individual stocks, and the terminal value assumption alone typically drives 60-80% of a DCF model’s total implied output.

Comcast bundles a capital-intensive broadband infrastructure business with cyclical media, streaming, and theme-park assets. That combination produces the exact blended-multiple problem the previous sections described: two very different businesses forcing investors to accept a single valuation that underprices both.

Under the plan announced 29 June 2026, Comcast will spin off NBCUniversal (including Sky) as an independent public company. Comcast will retain up to 19.9% of the new entity for approximately one year before monetising the stake. The transaction is expected to close around mid-2027, subject to board approval, regulatory clearances, and financing.

The Comcast SOTP valuation figures that have emerged since the 29 June announcement point to a gross implied value of approximately $190 billion, with a debt-adjusted per-share range of $29-$33 against a pre-announcement price of around $24, representing the 18-25% upside gap that the discount framework predicts.

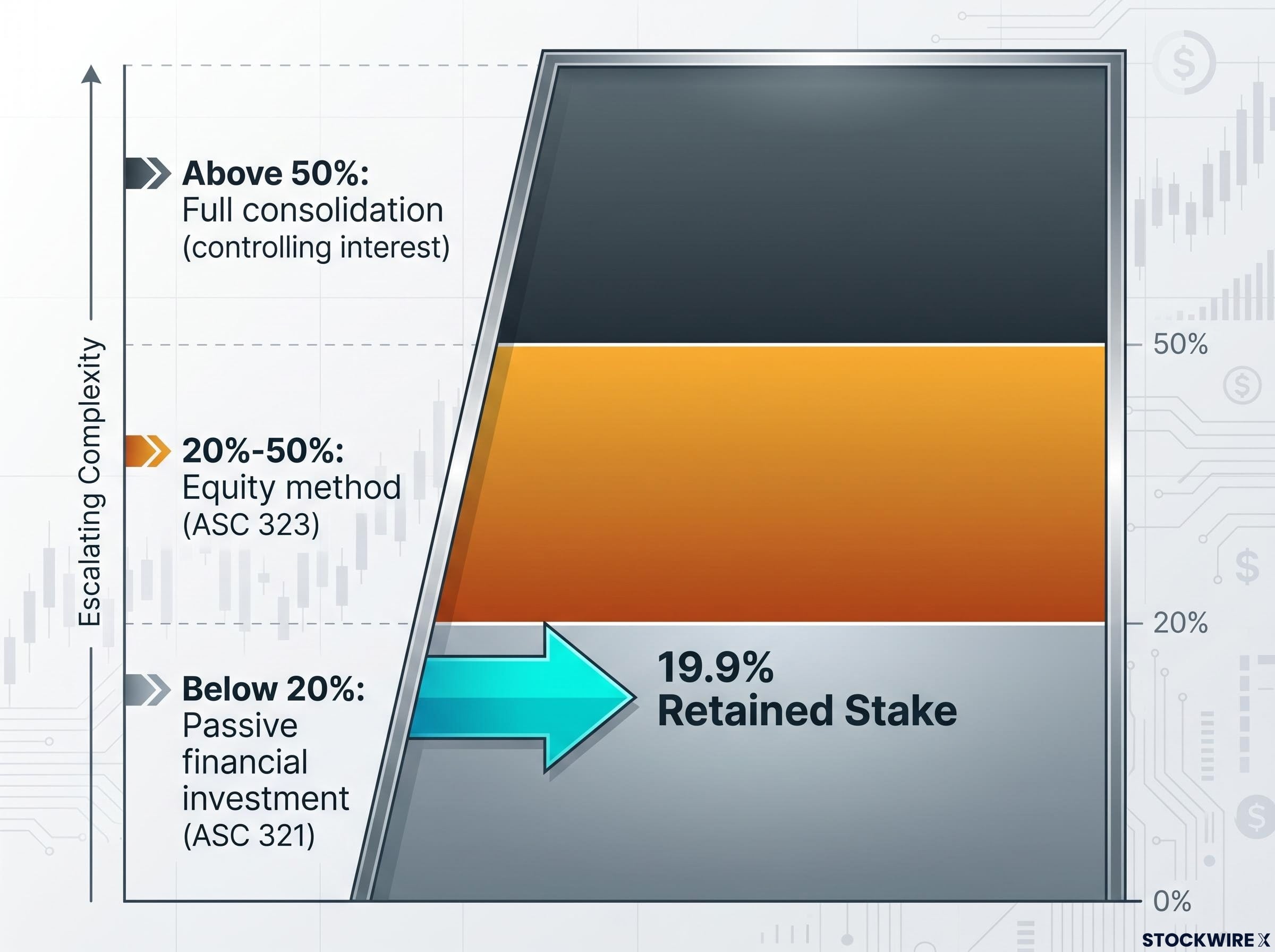

The precision of that 19.9% figure deserves attention. It is calibrated to keep Comcast just below a specific accounting threshold, and understanding the three-tier ownership framework tells you exactly why.

| Ownership Level | Accounting Treatment | Effect on Comcast’s Reported Earnings |

|---|---|---|

| Above 50% | Full consolidation (controlling interest) | Revenue and profits fully consolidated; minority interest deducted |

| 20%-50% | Equity method (ASC 323) | Comcast’s proportional share of NBCUniversal’s gains or losses flows through its income statement each quarter |

| Below 20% | Passive financial investment (ASC 321) | Holding sits on the balance sheet; changes in value appear as unrealised gains or losses without direct income statement entanglement |

At 20% or above, the equity method under ASC 323 would require Comcast to recognise its proportional share of NBCUniversal’s earnings or losses through its own income statement every quarter. Below 20%, the stake is treated as a passive financial investment under ASC 321. NBCUniversal’s operational results stay off Comcast’s income statement entirely, keeping the “new Comcast” broadband story clean and undiluted by media-sector volatility.

No public statement from Comcast spelled out this accounting rationale, but the ownership figure itself is a strong signal. The 20% threshold is a well-established cut-off in accounting standards, marking the boundary between passive investment treatment and the equity method. Stopping at 19.9% keeps the retained stake on the balance sheet without entangling Comcast’s income statement in NBCUniversal’s quarterly results. That is a consequential difference, and a figure chosen at that exact level points to the accounting and legal teams rather than any other consideration.

This detail changes how you should read any future corporate separation that features a precisely calibrated retained stake. The number is never incidental.

Everything covered so far (SOTP analysis, the four value-unlock channels, the red flags, and the accounting thresholds) converges into a five-point checklist you can apply to any announced corporate separation.

Corporate separations are announced regularly across U.S. markets. Having this repeatable framework converts each announcement from noise into a structured analytical exercise where you can form your own initial view before relying on headline commentary.

Conglomerate discounts are structural, recurring, and correctable through the right separation, but only when the underlying businesses are genuinely strong and the transaction is designed to let both entities stand independently. The mid-single to mid-teens percent discount range documented in developed markets means you will encounter this dynamic across multiple sectors over the course of your investing timeline, not just in media and broadband.

The Comcast case is instructive beyond its own facts. The 19.9% accounting detail, the pure-play divergence between broadband infrastructure and media, and the SOTP logic are all patterns that will appear again in future corporate separations. Recognising them in advance is what separates a reactive response to a headline from a structured analytical assessment.

The frameworks introduced here, SOTP valuation, pure-play benchmarking, accounting-tier awareness, and the five-point checklist, are transferable tools. They work on the next conglomerate breakup announcement just as they work on this one.

With the Comcast transaction expected to close around mid-2027, you have a live situation to track over the coming year that will test every concept covered in this article. It is a real-time case study in whether the conglomerate discount closes as the theory predicts.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

These statements are speculative and subject to change based on market developments and company performance. Past performance does not guarantee future results.

A conglomerate discount is the gap between a diversified company's actual market capitalisation and the aggregate value its individual businesses would command if each traded independently. It is calculated using sum-of-the-parts (SOTP) analysis: subtract the current market cap from the implied SOTP value, divide by the SOTP value, and multiply by 100 to get the percentage discount.

The 19.9% figure keeps Comcast just below the 20% threshold that triggers equity method accounting under ASC 323. Above 20%, Comcast would be required to recognise its proportional share of NBCUniversal's earnings or losses through its own income statement every quarter; below 20%, the stake is treated as a passive financial investment under ASC 321, keeping Comcast's broadband financials clean and undiluted by media-sector volatility.

A spinoff attacks every driver of the discount simultaneously: each separated company earns pure-play status and is valued with multiples appropriate for its specific industry, management focus improves, each entity attracts the investor base that suits its risk profile, and cleaner standalone financials remove the valuation fog that consolidated reporting creates.

Four red flags signal a value-destructive spinoff: the transaction shunts a genuinely weak or declining business into the spun entity, the new company receives a disproportionate share of the combined debt, top management stays with the parent rather than leading the spin, or the low valuation multiple reflects real business deterioration rather than structural complexity.

SOTP analysis applied to Comcast following the 29 June 2026 announcement points to a gross implied value of approximately $190 billion, with a debt-adjusted per-share range of $29-$33 against a pre-announcement price of around $24, representing an 18-25% upside gap consistent with what the conglomerate discount framework predicts.