Hormuz Prices Have Normalised. Geopolitical Inflation Risk Has Not.

9 mins ago

For years, Comcast traded at a price that implied the market was assigning something close to zero value to NBCUniversal. Not a discount. Not a haircut. Something closer to erasure. The Comcast split, announced yesterday, is management’s formal concession that this valuation gap was real, structural, and unlikely to close on its own.

The restructuring, disclosed on 29 June 2026, will take roughly 12 months to complete. That means the window for positioning around the initial mispricing is open but finite. Shares jumped sharply on announcement day, which tells you a portion of the estimated upside has already been captured by investors who moved first.

Here is the analytical framework for deciding whether the remaining gap is still worth owning, and which of the two resulting companies you may want to hold versus exit once the split completes.

When dissimilar businesses share a corporate umbrella, the combined valuation multiple tends to gravitate toward the lowest-valued segment. That gravitational pull suppresses the implied worth of faster-growing or higher-multiple divisions. This is what the market calls a conglomerate discount, and Comcast had one of the most visible examples in US large-cap equities.

The numbers make the problem concrete:

Because connectivity dominated earnings so heavily, the entire company traded on a telecom multiple. Every dollar of NBCUniversal’s earnings was being valued as if it were broadband revenue rather than streaming, studio, or theme park revenue. Consider Disney’s streaming arm: it commands a far lower earnings multiple than Netflix even though the two compete for the same audiences, because it is priced as part of a diversified entertainment conglomerate rather than as a standalone growth business. Peacock, Universal Studios, and Sky were subject to the same compression inside Comcast’s corporate umbrella.

The split is not a strategic choice in the usual sense. It is the mathematical conclusion the market had already reached: these businesses do not belong in the same valuation wrapper.

For investors wanting to situate the NBCUniversal re-rating within the broader market context, our deep-dive into growth stock valuation compression examines why entertainment and streaming names are trading at a 21% discount to fair value, the widest gap since 2022.

On the day the spin-off completes, you will hold shares in two separate listed companies, each with a different risk profile, a different growth trajectory, and a different natural investor base.

| Entity | Core Assets | CEO | Investor Profile | Expected Multiple |

|---|---|---|---|---|

| New Comcast (Connectivity) | Xfinity broadband, Xfinity Wireless, Comcast Business | Michael Angelakis | Value/income; stable cash flows, elevated debt | ~7.4x earnings |

| NBCUniversal/Sky (Media) | NBC, Telemundo, Peacock, Universal Studios, theme parks, Sky Europe | Mike Cavanagh | Growth; streaming, entertainment, parks exposure | ~20x earnings |

Brian Roberts retains an overarching leadership role across both entities. NBCUniversal will maintain a dual-class share structure post-separation.

One detail that most coverage has glossed over: the Versant Media Group carve-out, completed in January 2026, already removed USA Network, Oxygen, E!, SYFY, Golf Channel, CNBC, MSNBC, and several other cable networks from the media segment. Those assets are not part of the NBCUniversal/Sky entity going forward. Any sum-of-the-parts analysis that includes them is double-counting.

You will need to make a separate hold or sell decision on each resulting stock. That decision requires knowing exactly what each entity contains, and the table above is where that clarity starts.

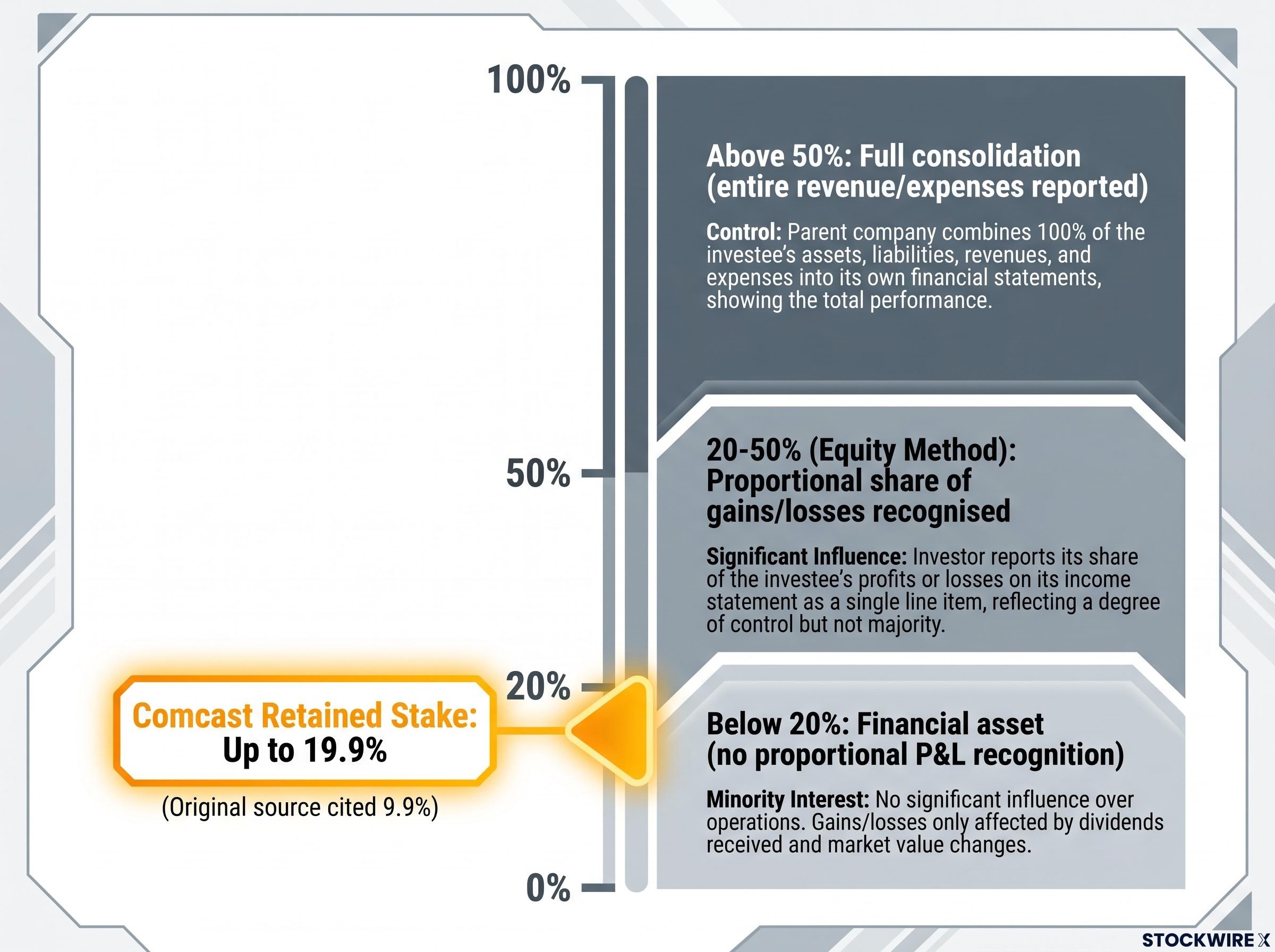

After the split, Comcast will retain an ownership stake in NBCUniversal of up to 19.9%, which it intends to monetise in a tax-efficient manner over time. The original source reporting cited a 9.9% figure; current public guidance indicates up to 19.9%. Both figures fall below a threshold that carries real accounting consequences.

The ownership percentage matters because it determines how NBCUniversal’s financial results flow through Comcast’s income statement. There are three accounting tiers:

Stopping just short of the 20% threshold appears to be a calculated choice on Comcast’s part. Keeping the stake below that accounting cut-off means the financial results of the two businesses will land on separate books from the outset, avoiding any blending of earnings during the post-spin monetisation window.

What this means in practice is straightforward: investors evaluating the connectivity entity will see a standalone P&L without NBCUniversal’s quarterly volatility bleeding into the numbers, and vice versa. That clean separation is precisely what the market was requesting.

The valuation case rests on a simple premise: separated, the two businesses should command higher combined multiples than the conglomerate traded at together. Testing that premise requires building the sum-of-the-parts from the bottom up.

The comparable company sets anchor the multiples. For the connectivity entity, Charter Communications, AT&T, and Verizon serve as the peer group; averaging their three-year price-to-earnings ratios produces a benchmark of approximately 7.4x earnings. For NBCUniversal/Sky, the peer range runs from Disney at the lower end to Netflix at the upper end, placing the implied multiple at approximately 20x earnings.

Netflix’s valuation re-rating from a peak multiple near 60x to its current level illustrates precisely the kind of multiple compression that NBCUniversal/Sky must avoid as it enters the public market as a standalone entity, where investor patience for earnings-multiple premiums has visibly shortened.

| Component | Multiple Used | Comparable Companies | Implied Value (Illustrative) |

|---|---|---|---|

| Connectivity | ~7.4x earnings | Charter, AT&T, Verizon | Majority of $190B gross |

| NBCUniversal/Sky | ~20x earnings | Disney, Netflix | Minority of $190B gross |

| Combined Gross SOTP | ~$190 billion implied market capitalisation | ||

These figures are illustrative analytical estimates based on the original source’s framework, not official Comcast pro forma financials. Precision will improve meaningfully once formal spin-off documentation is filed, expected approximately 60 days before closing.

The SEC Form 10 registration requirements mandate that the spun-off entity disclose audited financial statements, a full business description, identified risk factors, and post-separation capital structure details, which is precisely why the formal filing expected approximately 60 days before closing carries such analytical weight for investors modelling the debt allocation.

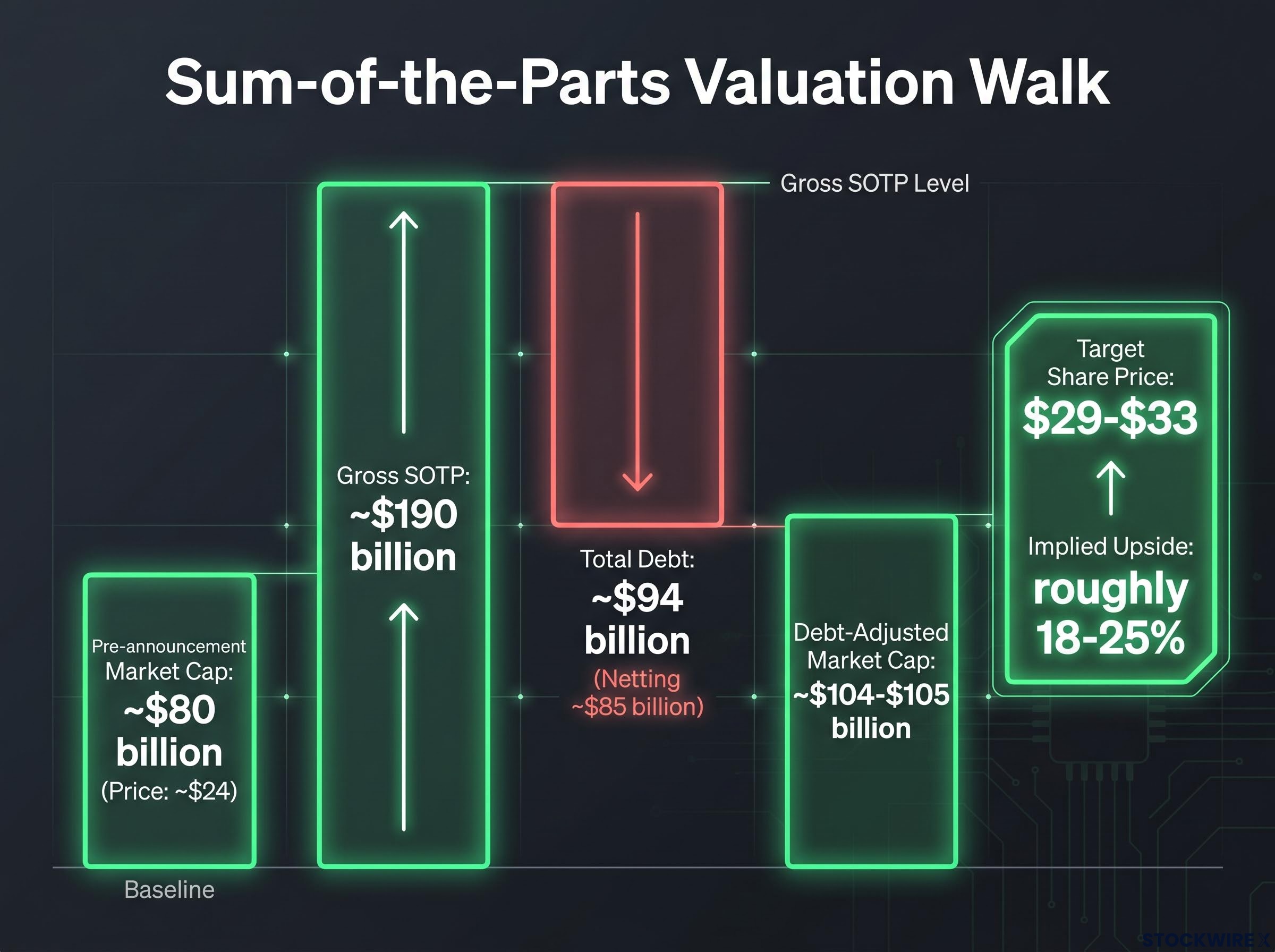

The gross sum-of-the-parts figure of approximately $190 billion is not what you can actually capture. The combined group carries roughly $94 billion in total debt, of which the connectivity business accounts for around $90 billion and the Sky/NBCUniversal segment for approximately $4 billion. Netting off approximately $85 billion in net debt from the gross implied value brings the debt-adjusted market capitalisation to approximately $104-$105 billion.

At the time of announcement, Comcast’s market capitalisation was approximately $80 billion with shares trading at approximately $24. Comparing that $80 billion market price to the $104 billion debt-adjusted implied value, and dividing through by shares outstanding, points to a per-share range of $29-$33, representing roughly 18-25% upside against the pre-announcement price.

The critical caveat: given yesterday’s sharp rally, some of that gap has already closed. The remaining upside should be calibrated from the current post-announcement price, not the original $24 figure. Official debt allocation between the two entities remains a key unknown.

The re-rating thesis is directionally sound, but four specific risk factors could compress the multiples assumed in the model:

Fixed wireless alternatives represent a structural constraint on the connectivity entity’s long-term multiple, not merely a cyclical headwind, because the capital-light economics of satellite and terrestrial wireless providers allow them to undercut cable broadband pricing in precisely the rural and suburban markets where Xfinity has historically faced the least competition.

In the analytical framework used by the original source, Comcast’s balance sheet scored the lowest possible financial health rating, with elevated debt relative to cash singled out as the primary concern. On the revenue and profit side, the business delivered little in the way of growth across roughly the past decade, although cash flow generation has strengthened over more recent years. Comcast also suspended share buybacks ahead of the spin-off to preserve financial flexibility.

The re-rating thesis is directionally sound, but the margin of safety available to investors who buy at today’s post-announcement price is materially narrower than it was before the rally, because a portion of the SOTP premium has already been captured in the share price move.

The value creation mechanism here is multiple expansion through cleaner business lines, not acceleration of underlying revenue or earnings growth. If you are sizing your upside expectation, that distinction is the one that prevents you from overstating what the split can deliver on an ongoing basis.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

The investor decision plays out in three sequential steps, each anchored to a specific data release rather than a vague monitoring directive:

If the debt burden on NBCUniversal/Sky proves modest and its growth assets are valued at the 20x multiple used in the SOTP framework, the media entity represents the higher-multiple, cleaner-growth holding. The connectivity company, by contrast, offers a stable but slow-growth cash flow profile better suited to income-oriented investors comfortable with elevated leverage.

The reader who waits for the formal filings and then evaluates both companies on their standalone merits will be in a materially better position than the investor making a permanent allocation decision today on incomplete information. The analytical framework is in place. The final inputs arrive in roughly 12 months.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors. The valuation estimates presented are illustrative and based on third-party analytical frameworks, not official company guidance.

The Comcast split, announced on 29 June 2026, separates the company into two listed entities: a connectivity business (Xfinity broadband, Xfinity Wireless, Comcast Business) and a media business (NBCUniversal, Peacock, Sky, Universal Studios). The restructuring is expected to take roughly 12 months to complete.

A conglomerate discount occurs when dissimilar businesses share a corporate umbrella, pulling the combined valuation multiple toward the lowest-valued segment. In Comcast's case, the connectivity division dominated earnings so heavily (approximately 90% of EBITDA) that NBCUniversal's streaming and entertainment assets were priced on a telecom multiple rather than the higher multiples those businesses would command as standalone entities.

The illustrative gross sum-of-the-parts valuation is approximately $190 billion; after netting off roughly $85 billion in net debt, the debt-adjusted implied market capitalisation falls to approximately $104-$105 billion, pointing to a per-share range of $29-$33 against the pre-announcement price of around $24.

Comcast plans to retain up to 19.9% of NBCUniversal and monetise that stake in a tax-efficient manner over time. Keeping the stake below the 20% accounting threshold means NBCUniversal's financial results will not flow through Comcast's income statement, ensuring clean separation of earnings from day one.

The four primary risks are: leverage concentration (the connectivity entity is expected to carry roughly $90 billion of the combined debt), a higher interest rate environment that makes that debt burden more costly, ongoing competitive pressure from fibre and fixed wireless alternatives eroding Xfinity's market position, and capital structure complexity that could affect the final trading multiple of each entity.